|

市场调查报告书

商品编码

1911726

喷墨头:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Inkjet Printhead - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

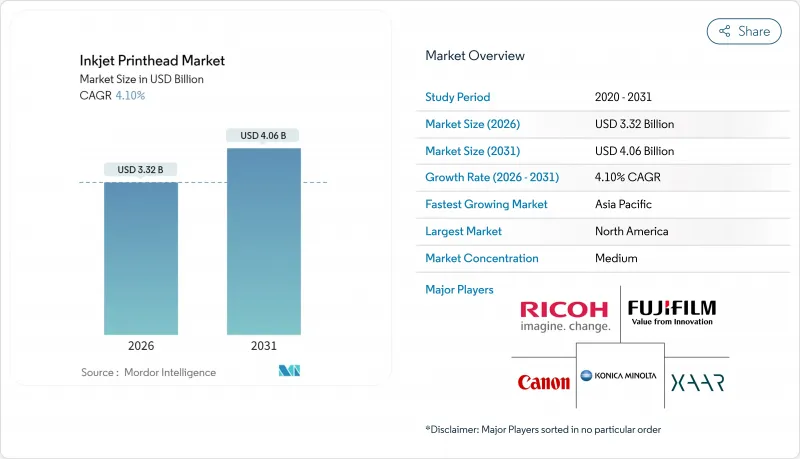

预计喷墨头市场将从 2025 年的 31.9 亿美元成长到 2026 年的 33.2 亿美元,并预计在 2031 年达到 40.6 亿美元,2026 年至 2031 年的复合年增长率为 4.1%。

从办公室列印向高精度工业应用的转变正在推动这一成长趋势。製造商正在利用电子机械系统 (MEMS)、薄膜压电致动器和单一途径列印架构。强劲的电子商务活动、品牌个人化策略以及日益增长的永续性需求正在推动对水性颜料墨水的需求,而增材製造技术则创造了新的、商机。现有供应商正透过多年专利组合和平台销售模式来巩固其市场地位,这些模式在不损害利润率的情况下扩大了基本客群。陶瓷和半导体供应链的波动持续对毛利率构成压力,但预测性维护分析正在降低停机风险并提高整体设备效率 (OEE)。

全球喷墨头市场趋势与洞察

单一途径印表机在包装和纺织品领域的快速扩张

单一途径印刷机省去了多个循环步骤,生产时间最多可缩短 70%,从而显着提高小批量生产的经济效益。 EFI 的 Nozomi C18000 印刷机已部署在一家欧洲加工商处,其线速度可达每分钟 400 英尺,分辨率为 1200 dpi,充分展现了其在提高生产效率方面的优势。纺织品製造商也获得了类似的成果,Kornit 的 Atlas MAX 印刷机能够在不牺牲色彩精度的前提下处理小批量、季节性生产。对更快週转时间的需求推动了印刷头订单的持续成长,尤其是那些能够处理各种黏度和高速印刷的型号。随着包装个人化程度的不断提高,单一途径系统将传统的静态生产线转变为灵活的、数据驱动的资产。由于每个单元都采用多排压电式印刷头,这项技术为零部件供应商提供了稳定的市场需求。

MEMS和薄膜压电技术能够以每分钟300公尺的线速度製造小于2皮升的液滴。

MEMS喷嘴阵列与薄膜致动器的结合,能够以300公尺/分钟的线速度喷射小于2皮升的液滴,从而实现药物涂层和微电路成型等精密加工。 Zaa公司2024年的一系列专利详细介绍了一种技术,该技术为每个喷嘴配备独立的驱动电子设备,从而在飞行过程中可变地控制液滴体积。京瓷的KJ4平台实现了这一概念的商业化,每英寸喷嘴数量达到600个,液滴尺寸可在1.5至42皮升之间调节,从而能够同时应用于图形印刷和功能性应用。这项技术进步减少了油墨浪费和营运成本,因为更小的液滴意味着每平方公尺所需的颜料更少。从长远来看,这些喷头对于支援生物列印和智慧包装等项目至关重要,在这些项目中,精度比速度更为重要。

与雷射和模拟探头相比,资本成本溢价较高。

先进的喷墨生产线比同等产能的雷射打码机或柔版印刷机贵40%至60%。价格敏感地区的小规模製造商虽然从长远来看设置和製版成本更低,但仍在推迟升级。 OEM厂商提供的融资方案可以降低初始门槛,但对于单色标记和超大批量SKU而言,传统套件的投资报酬率仍然更具优势。新兴经济体的货币波动加剧了这种犹豫,在一定程度上减缓了喷墨头市场的成长速度。

细分市场分析

到2025年,按需喷墨头将占据67.98%的市场份额,远超连续喷墨印表机头。压电式喷墨印表机头适用于需要亚2皮升精度且无热应力的工业应用,而热感墨盒式喷墨印表机头则继续在对成本敏感的办公室设备领域占有一席之地。预计该细分市场将以5.17%的复合年增长率成长,这主要得益于材料科学的持续进步,而非产品数量的激增。连续喷墨技术在编码领域仍占有一席之地,其不间断的喷墨列印速度极快,但精度不足限制了其更广泛的应用。

薄膜致致动器可降低功耗,并将原生解析度提升至 1200 dpi,进一步增强按需喷墨列印在高密度图形和功能性列印方面的优势。RicohMH5421F 采用多墨滴波形,可按需喷墨 4 至 42 皮升,适用于标誌基材和基板)。随着瓦楞纸板和纺织厂单一途径线的日益普及,每台机器都整合了数百个喷嘴,从而为喷墨头市场带来了可观的持续收入,主要来自替换备件。

水性油墨在监管激励措施和颜料包覆技术的进步支持下,预计2025年将占总收入的31.76%。紫外光固化油墨目前成长滞后,但预计到2031年将维持5.72%的复合年增长率,这主要得益于LED固化技术的广泛应用,该技术无需高温即可实现与塑胶和金属的即时黏合。溶剂型油墨将继续用于户外横幅应用,在这些应用中,耐候性比环境影响更为重要;而乳胶基混合油墨则正被应用于需要高弹性的纺织品领域。

随着品牌所有者将循环经济指标置于优先地位,生物基配方技术正成为一个新兴的成长领域。 INX 的植物来源产品系列表明,永续的原料不会影响色域或耐久性。同时,UV固化头正越来越多地应用于折迭纸盒生产线,其即时固化功能缩短了复合工艺,从而减少了整体生产前置作业时间。

区域分析

北美地区预计到2025年将维持39.70%的收入份额,这主要得益于其成熟的研发生态系统和预测性维护平台的快速普及。联邦环境法规对溶剂排放的限制推动了对水性油墨升级的投资,而成熟的电子商务基础设施则巩固了对可序列化和可扫描包装的需求。

亚太地区预计将以6.43%的复合年增长率成长,这主要得益于中国智慧工厂计画和日本的致动器技术。Epson在中国新建的组装工厂缩短了前置作业时间并规避了外汇波动风险,而配备高弹纤维昇华喷头的Mimaki TS200则瞄准了东南亚的聚酯纤维工厂。区域成本优势吸引了OEM外包,从而增强了陶瓷和MEMS晶片等喷墨列印机构关键部件的本地产业丛集。

欧洲技术发达,但成长已进入成熟阶段,替换需求超过了新装机量。 REACH法规正在加速向低VOC油墨的过渡,而柯尼希·鲍尔·杜斯特公司正在推出纸盒印刷机,这些印刷机能够满足高价值、小批量订单的高额资本投资。政府对可回收包装的支持也支撑了食品和製药加工商对印刷头替换件的稳定需求。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 单一途径印表机在包装和纺织品领域的快速扩张

- MEMS和薄膜压电元件能够以300公尺/分钟的速度达到小于2皮升的液滴喷射。

- OEM厂商转型销售开放平台印表机头(Epson、施乐)

- 向水性颜料墨水的永续性推广

- 利用人工智慧进行预测性维护,减少停机时间

- 新光EHD列印头适用于高黏度功能性流体

- 市场限制

- 雷射头与模拟头相比的资本支出溢价

- 奈米颗粒和白色墨水堵塞风险

- 专利拥堵限制了新进入者的扩充性

- 不稳定的陶瓷和半导体供应链

- 产业价值链分析

- 技术展望

- 宏观经济因素如何影响市场

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 监管环境

第五章 市场规模与成长预测

- 依技术类型

- 按需投放

- 热感的

- 压电式

- 连续的

- 按需投放

- 按墨水类型

- 水溶液

- 溶剂型

- 紫外线固化型

- 乳胶和染料昇华

- 其他墨水类型

- 透过使用

- 包装和标籤

- 纺织印花

- 电子和功能材料

- 3D/积层製造

- 编码和标记

- 其他用途

- 最终用户

- 办公室和消费者

- 工业印刷

- 图文印刷

- 其他最终用户

- 按地区

- 北美洲

- 美国

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Ricoh Company, Ltd.

- FUJIFILM Holdings Corporation

- Canon Inc.

- Konica Minolta, Inc.

- Xaar plc

- Memjet Holdings Ltd.

- Funai Electric Co., Ltd.

- Kyocera Corporation

- Toshiba Corporation

- HP Development Company, LP

- Seiko Epson Corporation

- Xerox Holdings Corporation

- Domino Printing Sciences plc

- Brother Industries, Ltd.

- Hitachi Industrial Equipment Systems Co., Ltd.

- Videojet Technologies, Inc.

- Lexmark International, Inc.

- Panasonic Holdings Corporation

- Durst Group AG

- Kodak Alaris, Inc.

第七章 市场机会与未来展望

The inkjet printhead market is expected to grow from USD 3.19 billion in 2025 to USD 3.32 billion in 2026 and is forecast to reach USD 4.06 billion by 2031 at 4.1% CAGR over 2026-2031.

A migration from office printing toward high-precision industrial use underpins this trajectory as manufacturers exploit micro-electromechanical systems, thin-film piezo actuators, and single-pass architectures. Robust e-commerce activity, brand personalization strategies, and rising sustainability mandates are reinforcing demand for water-based pigmented inks, while additive manufacturing creates fresh, high-margin opportunities. Established vendors defend their positions through multi-year patent portfolios and platform sales models that expand the accessible customer base without diluting margins. Supply chain volatility in ceramics and semiconductors continues to pressure gross profits, yet predictive-maintenance analytics soften downtime risks and lift overall equipment effectiveness.

Global Inkjet Printhead Market Trends and Insights

Explosion of Single-Pass Digital Presses in Packaging and Textiles

Single-pass presses eliminate multi-pass cycles and cut production time by up to 70%, making short runs financially viable. EFI's Nozomi C18000 installs across European converters and delivers 400 linear ft/min at 1,200 dpi, validating throughput economics. Textile producers observe similar gains; Kornit's Atlas MAX handles seasonal micro-batches without sacrificing color accuracy. Demand for agile turnaround fuels sustained printhead orders, especially those rated for diverse viscosities and high-speed operation. As personalization expands within packaging, single-pass systems transform once-static production lines into flexible, data-driven assets. Because each unit uses multiple rows of piezo heads, the technology generates a steady pull-through for component suppliers.

MEMS and Thin-Film Piezo Allowing < 2 pL Drops at 300 m/min

MEMS nozzle arrays paired with thin-film actuators achieve sub-2 picoliter droplets at line speeds of 300 m/min, unlocking precision tasks such as pharmaceutical coatings and fine-line circuitry. Xaar's 2024 patent series details independent drive electronics for each nozzle that modulate volume on the fly. Kyocera's KJ4 platform commercialized the concept with 600 nozzles/inch and variable drops from 1.5 to 42 pL, enabling both graphics and functional deposition. The advance reduces ink waste and lowers operating costs because smaller drops translate into less pigment usage per square meter. Over the long term, these heads underpin bioprinting and smart-packaging initiatives where accuracy outranks raw speed.

Cap-ex Premium versus Laser and Analog Heads

Advanced inkjet lines cost 40-60% more than laser coders or flexo presses with similar throughput. Small manufacturers in price-sensitive regions delay upgrades despite lower setup and plate costs over the long haul. Financing programs offered by OEMs soften initial barriers, yet ROI calculations still favor legacy kit for mono-color marking or ultra-high-volume SKUs. Currency volatility in emerging economies reinforces the hesitation, slightly tempering the inkjet printhead market growth pace.

Other drivers and restraints analyzed in the detailed report include:

- OEM Shift to Open-Platform Printhead Sales

- Sustainability Push for Water-Based Pigmented Inks

- Clogging Risk with Nanoparticle and White Inks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drop-on-Demand accounted for 67.98% of the inkjet printhead market share in 2025, far outpacing continuous-flow systems. Piezo-based variants supply industrial sites that require sub-2 pL accuracy without thermal stress, while thermal cartridges hold ground in cost-sensitive office devices. The segment is forecast to post a 5.17% CAGR, reflecting continuous material science refinements rather than unit-growth spikes. Continuous technology retains coding niches where uninterrupted streams enable top speeds, but precision shortfalls curb its broader penetration.

Thin-film actuators cut power draw and raise native resolution to 1,200 dpi, giving Drop-on-Demand an advantage in high-density graphics and functional printing. Ricoh's MH5421F ships with multi-drop waveforms that lay down 4-42 pL volumes on demand, serving both signage and PCB substrates. As single-pass lines spread across corrugated and textile plants, each machine integrates hundreds of nozzles, embedding a substantial replacement-spares annuity into the inkjet printhead market size.

Aqueous inks commanded 31.76% revenue in 2025, buoyed by regulatory incentives and stronger pigment-encapsulation chemistries. UV-curables trail but are set to log a 5.72% CAGR to 2031, lifted by LED curing that bonds instantly to plastics and metals without high-heat exposure. Solvent fluids persist in outdoor banners where weathering resistance overrides environmental trade-offs, and latex blends serve high-stretch textiles that need elasticity.

Bio-based formulations occupy a rising niche as brand owners target circular-economy metrics. INX's plant-derived portfolio shows that sustainable inputs no longer compromise gamut or durability. UV heads, meanwhile, penetrate folding carton lines because instant cure accelerates lamination steps, trimming total turnaround.

The Inkjet Printhead Market Report is Segmented by Technology Type (Drop-On-Demand, and Continuous), Ink Type (Aqueous, Solvent-Based, UV-Curable, and More), Application (Packaging and Labeling, Textile Printing, and More), End-User (Office and Consumer-Based, Industrial Printing, Graphic Printing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 39.70% of 2025 revenue on the strength of entrenched R&D ecosystems and swift uptake of predictive-maintenance platforms. Federal environmental rules that restrict solvent discharge spur investment in water-based upgrades, and a mature e-commerce backbone secures demand for serialized, scannable packaging.

Asia-Pacific is expected to post a 6.43% CAGR, propelled by Chinese smart-factory programs and Japanese actuator know-how. Epson's new Chinese assembly hubs shorten lead times and hedge currency swings, whereas Mimaki's TS200 aims at Southeast Asian polyester mills with sublimation heads attuned to high-stretch fabrics. Regional cost advantages attract OEM outsourcing, intensifying local component clusters for ceramics and MEMS chips integral to inkjet jets.

Europe remains technology-rich but growth-mature as replacement buying overtakes greenfield installations. REACH regulations accelerate switchover to low-VOC fluids, and Koenig and Bauer Durst deploys carton presses that justify high cap-ex via premium short-run jobs. Government incentives for circular packaging underpin steady head retrofits across food and pharma converters.

- Ricoh Company, Ltd.

- FUJIFILM Holdings Corporation

- Canon Inc.

- Konica Minolta, Inc.

- Xaar plc

- Memjet Holdings Ltd.

- Funai Electric Co., Ltd.

- Kyocera Corporation

- Toshiba Corporation

- HP Development Company, L.P.

- Seiko Epson Corporation

- Xerox Holdings Corporation

- Domino Printing Sciences plc

- Brother Industries, Ltd.

- Hitachi Industrial Equipment Systems Co., Ltd.

- Videojet Technologies, Inc.

- Lexmark International, Inc.

- Panasonic Holdings Corporation

- Durst Group AG

- Kodak Alaris, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosion of single-pass digital presses in packaging and textiles

- 4.2.2 MEMS and thin-film piezo allowing <2 pL drops at 300 m/min

- 4.2.3 OEM shift to open-platform printhead sales (Epson, Xerox)

- 4.2.4 Sustainability push for water-based pigmented inks

- 4.2.5 AI-driven predictive maintenance lowering downtime

- 4.2.6 Emerging EHD printheads for high-viscosity functional fluids

- 4.3 Market Restraints

- 4.3.1 Cap-ex premium vs. laser and analog heads

- 4.3.2 Clogging risk with nanoparticle and white inks

- 4.3.3 Patent thickets limiting new entrant scalability

- 4.3.4 Volatile ceramics and semiconductor supply chains

- 4.4 Industry Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 The Impact of Macroeconomic Factors on the Market

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Regulatory Landscape

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology Type

- 5.1.1 Drop-on-Demand

- 5.1.1.1 Thermal

- 5.1.1.2 Piezo-based

- 5.1.2 Continuous

- 5.1.1 Drop-on-Demand

- 5.2 By Ink Type

- 5.2.1 Aqueous

- 5.2.2 Solvent-based

- 5.2.3 UV-curable

- 5.2.4 Latex and Sublimation

- 5.2.5 Other Ink Types

- 5.3 By Application

- 5.3.1 Packaging and Labeling

- 5.3.2 Textile Printing

- 5.3.3 Electronics and Functional Materials

- 5.3.4 3D / Additive Manufacturing

- 5.3.5 Coding and Marking

- 5.3.6 Other Applications

- 5.4 By End-user

- 5.4.1 Office and Consumer-based

- 5.4.2 Industrial Printing

- 5.4.3 Graphic Printing

- 5.4.4 Other End-users

- 5.5 By Geographic

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ricoh Company, Ltd.

- 6.4.2 FUJIFILM Holdings Corporation

- 6.4.3 Canon Inc.

- 6.4.4 Konica Minolta, Inc.

- 6.4.5 Xaar plc

- 6.4.6 Memjet Holdings Ltd.

- 6.4.7 Funai Electric Co., Ltd.

- 6.4.8 Kyocera Corporation

- 6.4.9 Toshiba Corporation

- 6.4.10 HP Development Company, L.P.

- 6.4.11 Seiko Epson Corporation

- 6.4.12 Xerox Holdings Corporation

- 6.4.13 Domino Printing Sciences plc

- 6.4.14 Brother Industries, Ltd.

- 6.4.15 Hitachi Industrial Equipment Systems Co., Ltd.

- 6.4.16 Videojet Technologies, Inc.

- 6.4.17 Lexmark International, Inc.

- 6.4.18 Panasonic Holdings Corporation

- 6.4.19 Durst Group AG

- 6.4.20 Kodak Alaris, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment