|

市场调查报告书

商品编码

1911740

中东和非洲瓦楞纸包装市场:市场份额分析、行业趋势、统计数据和成长预测(2026-2031 年)Middle-East And Africa Corrugated Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

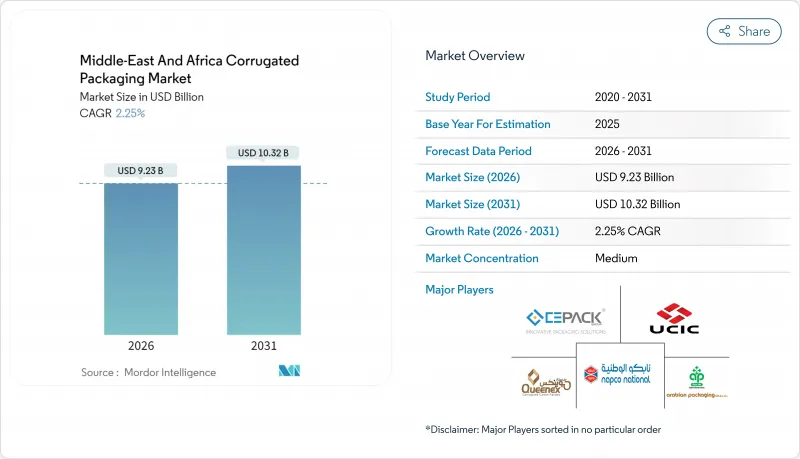

2025年中东和非洲瓦楞纸包装市场价值为90.3亿美元,预计到2031年将达到103.2亿美元,高于2026年的92.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 2.25%。

当前市场表现反映了该地区的双重动态:成熟的快速消费品(FMCG)需求和快速增长的电子商务交易量,都对尺寸合适、可印刷的包装盒青睐有加。沙乌地阿拉伯透过规模经济推动成长,而土耳其则凭藉其出口导向纸厂注入了竞争动力。政府的产业扶持政策、不断提升的回收能力以及非洲大陆自由贸易区(AfCFTA)的建立,共同扩大了潜在需求。同时,供应方面的摩擦,例如牛皮纸价格波动和用水限制,迫使生产商优化纤维采购和提高纸厂效率。

中东和非洲瓦楞纸包装市场趋势及洞察

电子商务的快速成长推动了最后一公里包装的发展。

中东和非洲瓦楞纸包装市场电子商务交易量的激增,迫使加工商设计出能够承受多个都市区配送网路衝击,同时提升顾客开箱体验的包装盒。沙乌地阿拉伯和阿联酋的履约中心越来越多地采用尺寸合适的模切型材,以减少填充材物和运输废弃物。 Smurfit Kappa 的区域数位印刷机能够实现定製图案的快速交货,并降低季节性产品的最低订购量。订阅模式提高了对再出货性能的要求,促使纸板供应商提高边缘抗压强度和抗穿刺性能。全通路实体零售商正在其线上订购线下取货模式中复製这些由电子商务主导的规范,加速了全部区域设计风格的融合。

日常消费品和有组织零售业的快速扩张

现代零售业在埃及、奈及利亚和南非的渗透推动了对即用型瓦楞纸托盘日益增长的需求。这些托盘简化了库存管理和视觉商品行销。跨国快速消费品集团正在区域工厂内统一包装尺寸,使加工商能够简化模具并提高生产效率。不断增长的都市区使需求集中在大都会圈,促使企业新建瓦楞纸生产设施,以最大限度地降低运输成本。折扣连锁店和便利商店倾向于选择可直接上架的系统,这显着减少了店内操作,进一步巩固了瓦楞纸作为主要二级包装的地位。不断提高的外包装图形标准也推动了中东和非洲瓦楞纸包装市场对多色柔版印刷和数位印刷生产线的采用。

牛皮纸供应和价格波动

欧洲箱板纸厂的暂时停产以及红海航线的改道,使得中东和非洲的瓦楞纸包装市场面临现货价格大幅上涨的局面。缺乏外汇对冲的小型加工商被迫自行承担成本飙升,进一步压缩了本已微薄的利润空间。沙乌地阿拉伯和土耳其的大型生产商已透过提高自产再生纤维的比例来应对,而非洲的小规模加工商仍依赖进口。海运的长期中断可能导致箱板纸的到货时间延迟长达四周,迫使终端用户分散供应合约并建立安全库存。

细分市场分析

到2025年,开槽纸箱将占据中东和非洲瓦楞纸包装市场45.35%的份额,这主要得益于其成本效益高的模切工艺、多样化的尺寸选择以及优异的纸板产量比率。此细分市场现有的资产基础支援高速自动化生产线,有利于实现可预测的纸箱坯料配置。运输常温食品和工业零件的品牌商继续指定使用标准开槽纸箱(RSC)以优化托盘布局。然而,模切纸箱预计将以2.86%的复合年增长率(CAGR)占据市场主导地位,但随着直接面向消费者的品牌寻求客製化配置以最大限度地减少空隙并提升开启时的展示效果,其市场份额将受到侵蚀。零售商也正在转向五面折迭式纸箱,可直接上架销售,进一步扩大了专业加工商的价值基础。

水性数位列印头的应用使得小批量模切件的生产更具经济效益,而高性能平板绘图仪的引入则缩短了新设计的前置作业时间。在表面印刷的模切件上醒目地印上可持续发展讯息,即使是小订单也能获得更高的价格。同时,虽然伸缩纸箱目前仍属于小众市场,但其高度调整功能可适应不同尺寸的农产品,这正有助于它们在娇贵的生鲜食品出口领域成长。中东和非洲瓦楞纸包装市场的成功加工商将大批量开槽生产线与灵活的数位生产线相结合,从而实现按需模切。

预计到2025年,在中东和非洲瓦楞纸包装市场中,单层瓦楞纸板将占53.40%的市场份额。这主要是因为国内快速消费品(FMCG)货物的运输路线很少超过500公里。随着非洲大陆自由贸易区(AfCFTA)内部贸易的活性化,对三层瓦楞纸板的需求将以3.03%的复合年增长率增长,为白色家电和汽车零件提供长途运输保护。双层瓦楞纸板则适用于中等重量的货物,因为其运输成本的节省超过了材料成本的增加。化学产品出口商需要最高的抗穿刺性和防漏性,因此他们会订购固体纤维板,但这仍然是一个较小众的专业市场。

沙乌地阿拉伯和土耳其的综合造纸厂正在扩大瓦楞纸板的加工能力,以满足三层瓦楞纸板的需求。回收网路的改进也使再生纸面纸的利用率超过55%。客户越来越要求供应商透过高温高湿测试来检验纸板的性能,这种测试模拟了沙漠转运环境。因此,结合了原生牛皮纸面纸和再生纸芯的工程纸板配方正在成为中东和非洲瓦楞包装市场的主流,以满足成本和压缩率的双重目标。

其他福利

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 价值/供应链分析

- 监管环境

- 技术展望

- 市场驱动因素

- 电子商务的快速成长推动了最后一公里包装的发展。

- 日常消费品和有组织零售业的快速扩张

- 政府鼓励国内製造业和回收利用

- 出口导向型生鲜食品物流的成长

- 非洲大陆自由贸易协定(AfCFTA)下非洲内部贸易激增-此一趋势鲜为人知

- 微型品牌(一个尚未充分开发的领域)采用数位印刷技术

- 市场限制

- 牛皮纸供应和价格波动

- 来自柔软性塑胶包装的竞争

- 依赖进口原料的物流风险

- 由于缺水导致工厂停工(未被重视)

- 定价分析

- 进出口分析

- PESTEL 分析

- 资本投资趋势

- 瓦楞纸箱生产对环境的影响

- 产业生态系分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 供应商的议价能力

第五章 市场规模与成长预测

- 按盒子类型

- 有缝隙的容器

- 模製容器

- 五面折迭盒

- 伸缩盒

- 其他类型的盒子

- 按板材等级

- 单层板

- 双层墙板

- 三层墙板

- 固体纤维板

- 按笛子尺寸

- A 长笛

- 低音长笛

- C调长笛

- E 长笛

- F调长笛

- 其他长笛

- 按最终用户行业划分

- 食物

- 饮料

- 家用电器和电气设备

- 个人护理和家居用品

- 工业和化学产品

- 农业和生鲜食品

- 电子商务与零售

- 其他的

- 按国家/地区

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 南非

- 奈及利亚

- 土耳其

- 其他中东和非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Arabian Packaging Co. LLC

- Queenex Corrugated Carton Factory LLC

- United Carton Industries Company(JSC)

- Napco National CJSC

- Cepack Group SARL

- Falcon Pack IND LLC

- World Pack Industries LLC

- Universal Carton Industries Group LLC

- Express Pack Print LLC

- Green Packaging Boxes Industries LLC

- Tarboosh Packaging Co. LLC

- Unipack Containers & Carton Products LLC

- Al Rumanah Packaging LLC

- NBM Pack LLC

- Mondi plc

- Smurfit Kappa Group plc

- International Paper Company

- Middle East Paper Company(SASE:1202)

- INDEVCO Paper Containers SAL

- Obeikan Paper Industries Co.

- National Paper Company SAE

- RAK Packaging LLC

- Al Bayader International LLC

- Hadera Paper Ltd.(Amnir Corrugated)

第七章 市场机会与未来展望

The Middle East and Africa corrugated packaging market was valued at USD 9.03 billion in 2025 and estimated to grow from USD 9.23 billion in 2026 to reach USD 10.32 billion by 2031, at a CAGR of 2.25% during the forecast period (2026-2031).

Current performance mirrors the region's dual character: mature fast-moving consumer goods (FMCG) demand alongside rapidly scaling e-commerce volumes that favor right-sized, print-ready boxes. Saudi Arabia anchors growth through scale, while Turkey's export-oriented plants inject competitive momentum. Government industrial policies, rising recycling capacity, and the African Continental Free Trade Area (AfCFTA) collectively widen addressable demand. At the same time, supply-side friction from kraft paper price swings and water scarcity regulations forces producers to optimize fiber sourcing and mill efficiency.

Middle-East And Africa Corrugated Packaging Market Trends and Insights

E-commerce Boom Driving Last-Mile-Friendly Packaging

E-commerce volumes in the Middle East and Africa corrugated packaging market compel converters to engineer boxes that survive multi-touch urban delivery networks while delighting consumers during unboxing. Saudi and UAE fulfillment centers increasingly specify right-sized die-cut formats that curb void fill and freight waste. Smurfit Kappa's regional digital presses now turn around custom artwork in days, lowering order minimums for seasonal drops.Subscription models elevate repeat-shipment performance requirements, nudging board suppliers toward higher edge-crush and puncture resistance. Brick-and-mortar retailers adopting omnichannel setups replicate these e-commerce-driven specs across click-and-collect programs, accelerating design convergence region-wide.

Rapid Expansion of FMCG and Organised Retail

Modern retail penetration in Egypt, Nigeria, and South Africa fuels volume uptake for shelf-ready corrugated trays that simplify stocking and visual merchandising. Multinational FMCG groups harmonize pack dimensions across regional plants, allowing converters to rationalize tooling and scale output more efficiently. Urban population growth consolidates demand near mega-cities, justifying new corrugator installations that minimize outbound freight. Discount chains and convenience formats prefer shelf-ready systems that slash in-store labor, further embedding corrugated as a primary secondary pack. Elevated graphic standards on outer packs also spur adoption of multi-color flexo and digital printing lines across the Middle East and Africa corrugated packaging market.

Volatility in Kraft Paper Supply and Prices

Temporary shutdowns at European containerboard mills and Red Sea shipping reroutes expose the Middle East and Africa corrugated packaging market to spot-price surges. Smaller converters lacking currency hedges absorb cost spikes that compress already thin margins. Saudi and Turkish integrated producers respond by lifting in-house recycled fiber ratios, yet smaller African converters remain tied to import flows. Any extended ocean freight disruption can delay linerboard arrivals by four weeks, prompting end-users to diversify supply contracts or hold higher safety stocks.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Local Manufacturing and Recycling

- Export-Oriented Fresh-Produce Logistics Growth

- Competition from Flexible Plastic Packaging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Slotted containers commanded 45.35% of the Middle East and Africa corrugated packaging market in 2025 due to their cost-efficient die-cutting, universal dimensions, and favorable board yield. The segment's legacy installed base supports high-speed automation lines that favor predictable blank geometry. Brand owners shipping ambient groceries and industrial parts continue to specify regular slotted containers (RSC) for pallet optimization. Die-cut containers, however, recorded the highest 2.86% CAGR and are set to erode share as direct-to-consumer brands pursue bespoke geometries that minimize void space and elevate unboxing theatre. Retailers also migrate toward five-panel folders that double as shelf-ready units, further enlarging the value pool for specialty converters.

Adoption of water-based digital print heads unlocks shorter run economics on die-cut formats, while upgraded flat-bed plotters slash lead times on new designs. Sustainability messaging is more prominent on top-printed die-cuts, supporting premium price realization even at low order volumes. Conversely, telescopic boxes remain niche but gain ground in delicate fresh-produce exports where height variability accommodates heterogeneous crop sizing. Across the Middle East and Africa corrugated packaging market, successful converters balance high-volume slotted production with agile digital lines capable of on-demand die-cut runs.

Single-wall board captured 53.40% share of the Middle East and Africa corrugated packaging market size in 2025 because FMCG freight routes inside national borders rarely exceed 500 km. As AfCFTA trade intensifies, triple-wall demand rises at 3.03% CAGR, enabling longer haul protection for whitegoods and automotive sub-assemblies. Double-wall offerings cater to mid-weight loads where savings on freight outweigh incremental material cost. Solid fiber board is ordered by chemical exporters that need maximum puncture resistance and leak containment, though it remains a specialist niche.

Integrated mills in Saudi Arabia and Turkey debottleneck fluting section capacity to keep pace with triple-wall enquiries, while recycled liner content climbs above 55% thanks to better collection networks. Customers increasingly ask vendors to validate board grade performance in hot-box and humidity tests reflecting desert trans-shipment conditions. The Middle East and Africa corrugated packaging market therefore tilts toward engineered board recipes that blend virgin kraft top liners with recycled medium to meet both cost and compression targets.

The Middle East and Africa Corrugated Packaging Market Report is Segmented by Box Type (Slotted Containers, Die-Cut Containers, and More), Board Grade (Single-Wall Board, Double-Wall Board, and More), Flute Size (A-Flute, B-Flute, C-Flute, E-Flute, and More), End-User Industry (Food, Beverage, Consumer Electronics and Electrical Appliances, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Arabian Packaging Co. LLC

- Queenex Corrugated Carton Factory LLC

- United Carton Industries Company (JSC)

- Napco National CJSC

- Cepack Group SARL

- Falcon Pack IND LLC

- World Pack Industries LLC

- Universal Carton Industries Group LLC

- Express Pack Print LLC

- Green Packaging Boxes Industries LLC

- Tarboosh Packaging Co. LLC

- Unipack Containers & Carton Products LLC

- Al Rumanah Packaging LLC

- NBM Pack LLC

- Mondi plc

- Smurfit Kappa Group plc

- International Paper Company

- Middle East Paper Company (SASE:1202)

- INDEVCO Paper Containers SAL

- Obeikan Paper Industries Co.

- National Paper Company SAE

- RAK Packaging LLC

- Al Bayader International LLC

- Hadera Paper Ltd. (Amnir Corrugated)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Value / Supply-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Market Drivers

- 4.5.1 E-commerce boom driving last-mile-friendly packaging

- 4.5.2 Rapid expansion of FMCG and organised retail

- 4.5.3 Government incentives for local manufacturing and recycling

- 4.5.4 Export-oriented fresh-produce logistics growth

- 4.5.5 Inter-African trade surge under AfCFTA (under-the-radar)

- 4.5.6 Digital printing adoption for micro-brands (under-the-radar)

- 4.6 Market Restraints

- 4.6.1 Volatility in kraft paper supply and prices

- 4.6.2 Competition from flexible plastic packaging

- 4.6.3 Import-dependent raw-material logistics risk

- 4.6.4 Water-scarcity-driven mill regulations (under-the-radar)

- 4.7 Pricing Analysis

- 4.8 Import and Export Analysis

- 4.9 PESTLE Analysis

- 4.10 Capital Expenditure Trends

- 4.11 Environmental Impact of Corrugated Box Production

- 4.12 Industry Ecosystem Analysis

- 4.13 Porter's Five Forces

- 4.13.1 Bargaining Power of Suppliers

- 4.13.1.1 Bargaining Power of Buyers

- 4.13.1.2 Threat of New Entrants

- 4.13.1.3 Threat of Substitute Products

- 4.13.1.4 Intensity of Competitive Rivalry

- 4.13.1 Bargaining Power of Suppliers

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Box Type

- 5.1.1 Slotted Containers

- 5.1.2 Die-cut Containers

- 5.1.3 Five-panel Folder Boxes

- 5.1.4 Telescopic Boxes

- 5.1.5 Other Box Types

- 5.2 By Board Grade

- 5.2.1 Single-wall Board

- 5.2.2 Double-wall Board

- 5.2.3 Triple-wall Board

- 5.2.4 Solid Fiber Board

- 5.3 By Flute Size

- 5.3.1 A-Flute

- 5.3.2 B-Flute

- 5.3.3 C-Flute

- 5.3.4 E-Flute

- 5.3.5 F-Flute

- 5.3.6 Other Flutes

- 5.4 By End-User Industry

- 5.4.1 Food

- 5.4.2 Beverage

- 5.4.3 Consumer Electronics and Electrical Appliances

- 5.4.4 Personal Care and Household Care

- 5.4.5 Industrial and Chemicals

- 5.4.6 Agriculture and Fresh Produce

- 5.4.7 E-commerce and Retail

- 5.4.8 Other End-Users

- 5.5 By Country

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Egypt

- 5.5.4 South Africa

- 5.5.5 Nigeria

- 5.5.6 Turkey

- 5.5.7 Rest of Middle East and Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Arabian Packaging Co. LLC

- 6.4.2 Queenex Corrugated Carton Factory LLC

- 6.4.3 United Carton Industries Company (JSC)

- 6.4.4 Napco National CJSC

- 6.4.5 Cepack Group SARL

- 6.4.6 Falcon Pack IND LLC

- 6.4.7 World Pack Industries LLC

- 6.4.8 Universal Carton Industries Group LLC

- 6.4.9 Express Pack Print LLC

- 6.4.10 Green Packaging Boxes Industries LLC

- 6.4.11 Tarboosh Packaging Co. LLC

- 6.4.12 Unipack Containers & Carton Products LLC

- 6.4.13 Al Rumanah Packaging LLC

- 6.4.14 NBM Pack LLC

- 6.4.15 Mondi plc

- 6.4.16 Smurfit Kappa Group plc

- 6.4.17 International Paper Company

- 6.4.18 Middle East Paper Company (SASE:1202)

- 6.4.19 INDEVCO Paper Containers SAL

- 6.4.20 Obeikan Paper Industries Co.

- 6.4.21 National Paper Company SAE

- 6.4.22 RAK Packaging LLC

- 6.4.23 Al Bayader International LLC

- 6.4.24 Hadera Paper Ltd. (Amnir Corrugated)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-needs Assessment

瓦楞纸包装软体市场:依功能、平台、使用者规模和应用程式划分-2026-2032年全球市场预测瓦楞纸包装市场:按材料类型、瓦楞纸板类型、印刷技术、最终用户和销售管道-全球预测,2026-2032年

瓦楞纸包装软体市场:依功能、平台、使用者规模和应用程式划分-2026-2032年全球市场预测瓦楞纸包装市场:按材料类型、瓦楞纸板类型、印刷技术、最终用户和销售管道-全球预测,2026-2032年 东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

东南亚瓦楞纸包装:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年)

单层纸匣全球市场规模、份额、趋势和成长分析报告(2026-2034年) 日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年)

日本纸盒包装市场规模、份额、趋势及预测(按材料类型、产品类型、最终用户和地区划分,2026-2034年) 2026年全球瓦楞纸包装市场报告北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

2026年全球瓦楞纸包装市场报告北美瓦楞纸包装市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测

瓦楞纸包装市场规模、份额和成长分析:按壁型、箱型、瓦楞数、印刷技术、最终用户、通路和地区划分-2026-2033年产业预测 快速折迭门市场按类型、操作方式、最终用途领域和区域划分

快速折迭门市场按类型、操作方式、最终用途领域和区域划分 瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测

瓦楞包装市场-全球产业规模、份额、趋势、机会和预测,按产品类型、包装类型、最终用途、地区和竞争细分,2020-2030 年预测