|

市场调查报告书

商品编码

1934643

汽车轴承:市占率分析、产业趋势与统计、成长预测(2026-2031)Automotive Bearings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

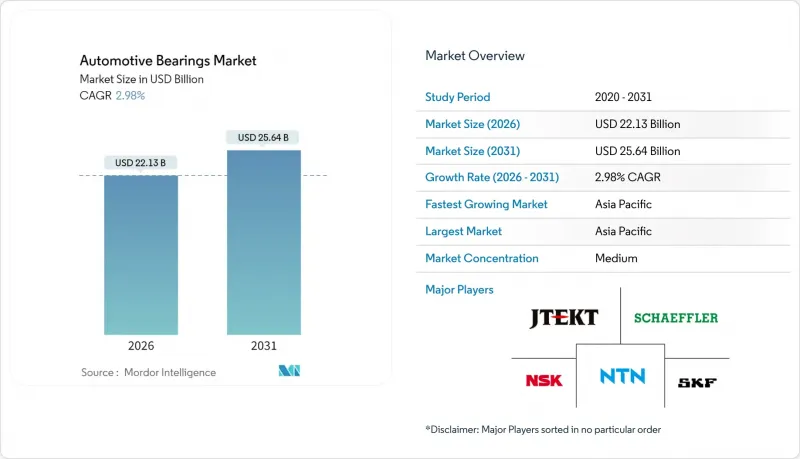

汽车轴承市场预计将从 2025 年的 214.9 亿美元成长到 2026 年的 221.3 亿美元,预计到 2031 年将达到 256.4 亿美元,2026 年至 2031 年的复合年增长率为 2.98%。

此次扩张正值稳定内燃机生产与加速电气化、重塑轴承规格、减少每辆车平均轴承数量以及推动对低摩擦、高效率解决方案的需求交汇之际。滚动轴承设计在轮端、变速箱和电动动力传动系统总成核心零件中仍然占据主导地位。然而,随着原始设备製造商 (OEM) 追求节能和紧凑模组化布局,陶瓷混合轴承、整合感测器单元和增材製造保持架正在获得高端市场份额。亚太地区轻型汽车产量的成长和电动车在当地的普及,正为全球成长提供支撑。同时,北美和欧洲则专注于智慧轴承的售后升级和预测性维护。钢铁价格波动、关税以及假冒仿冒品的涌入持续挤压利润率,迫使主要供应商转向垂直整合、尖端材料和循环经济的经营模式。

全球汽车轴承市场趋势与洞察

电气化推动了对低摩擦电动动力传动系统轴承的需求

电动车需要超低摩擦和高电绝缘性的轴承,这促使供应商转向陶瓷球、特殊涂层和全新设计的保持架几何形状,以减少能量损失并防止静电放电。 SKF 的超低摩擦轮毂轴承系列透过降低扭矩阻力来满足电动车轮毂的需求,而舍弗勒的离心式盘形球轴承则可将摩擦降低 80%,并将使用寿命延长 10 倍,体现了电动动力传动系统单元目前所需的性能飞跃。原始设备製造商 (OEM) 也面临着杂散电流可能导致点蚀的威胁,因此混合氮化硅解决方案对于高速马达轴线至关重要。儘管零件数量有所下降,但汽车轴承市场仍在继续受益于电气化,因为对专用电动车生产线的投资和高价策略抵消了单车销量下降的影响。

车辆使用寿命延长,动售后市场扩张

随着美国车辆保有量的成长,零件更换週期不断延长,尤其是轮毂轴承和传动系统轴承。表面处理技术的进步延长了这些零件的使用寿命,使车主能够在保证安全的前提下缩短保养週期。车队营运商越来越多地利用数据分析来预测机械故障,售后市场也正从被动维修转向基于状态监控的预防性采购。通路和直销模式使得高性能轴承产品在首次安装后仍能保持其价值。这种不断发展的市场结构有助于稳定汽车轴承市场的需求,即使在新车销售波动的情况下也是如此。

假冒低价轴承侵蚀了原厂/售后市场的利润。

捷太格特(JTEKT)的测试发现,假轮毂单元的疲劳测试寿命仅为正品的十分之一。 SKF销毁了15吨查获的仿冒品,但全像标籤的改良和区块链溯源技术的引进仍不足以彻底遏制仿冒品的涌入。在新兴市场,法律制裁力度不足导致假冒产品屡屡上当,迫使合法供应商承担教育宣传活动和法务审核的成本。这些声誉风险和保固成本给汽车轴承市场的OEM和售后市场都带来了沉重的负担。

细分市场分析

预计到2025年,滚动轴承产品将占总收入的53.10%,并在2031年之前以5.08%的复合年增长率成长。其优势在于成本、负载和速度性能的平衡,使其适用于轮毂、变速箱和电力驱动桥。圆柱滚子轴承和圆锥滚子轴承在重型传动系统中表现出色,而深沟球轴承则在高速电动车马达中表现优异,因为低摩擦和静音至关重要。电动车的长期保固使得永久密封轴承单元更受欢迎,从而推动了对整合润滑和感测器组件的需求。

在小型内燃机和空调周边设备设备中,由于往復运动占主导地位,光滑轴承仍存在一定的市场,但其市场份额持续下降。同时,交叉滚子轴承和滚针轴承的创新应用瞄准了紧凑型转向柱和电动驻煞车系统,逐步提升了价值密度。随着轮毂模组设计向配备ABS编码器的第三代双滚子轴承过渡,高端市场对滚动轴承的需求将会增加,从而巩固其在汽车轴承市场的核心地位。

到2025年,钢製轴承将占全球出货量的76.10%,这反映了其成熟的熔炼製程、久经考验的疲劳寿命和成本优势。然而,随着原始设备製造商(OEM)推进电气化平台,漏电流隔离变得日益重要,钢製轴承细分市场的成长速度将会放缓。陶瓷和混合轴承的复合年增长率(CAGR)将达到6.02%。

聚合物和涂层钢轴承在腐蚀性环境和对噪音敏感的应用中占据了一定的市场空白,而表面处理技术的创新(例如类类金刚石碳离子氮化)则无需更换材料即可延长使用寿命。随着窑炉运转率的提高,陶瓷轴承的成本有望下降,从而降低溢价并促进其在中檔电动车中的应用。然而,受经济实惠、量产型内燃机(ICE)和混合动力汽车需求的推动,预计到2031年,钢轴承仍将占据汽车轴承市场近三分之二的份额。

区域分析

预计到2025年,亚太地区将占全球营收的43.40%,年复合成长率达6.55%,主要得益于中国的规模优势、印度两位数的组装成长以及东协地区供应商网路的快速扩张。中国整车製造商正在整合本地生产的混合陶瓷轮毂,以满足电动车的保固要求;而印度的「印度製造」计画预计将在2020年代中期将进口依赖度从40%降低至25%。政府对纯电动两轮车的补贴正在提振对紧凑型深沟球轴承产品的需求,从而增强该地区对汽车轴承市场的贡献。

由于皮卡和SUV产量高,以及成熟的换代週期,北美仍占据着较大的市场份额。拜登政府的关税政策每年使零件成本增加80亿美元,促使舍弗勒等供应商在俄亥俄州投资2.3亿美元开设了一家电力驱动桥工厂,缩短了供应链,并获得了原始设备製造商(OEM)的核准。墨西哥成本效益高的机械加工丛集正在吸引环锻造投资,以弥补美国的产能缺口。加拿大则充分利用其钢铁原料供应能力。由于该地区车辆的平均车龄超过12.8年,汽车售后市场依然强劲,儘管新车销量有所波动,但仍支撑着汽车轴承市场的收入。

欧洲轻型汽车产量放缓,而电动车强制令的实施却在加速推进,这推动了对整合感测器和混合陶瓷解决方案的需求。德国在研发投入方面主导,总部位于瑞典的SKF正在试行一项符合欧盟绿色交易目标的循环性能涂层计画。舍弗勒正透过重组业务、关闭位于奥地利贝尔恩多夫的工厂并升级其位于斯洛伐克基什采的工厂,持续优化成本。英国、法国和义大利正在推动区域性电力驱动桥生产,打造以本地采购为重点的轴承供应链,以确保欧洲大陆即使在汽车轴承市场份额略有下降的情况下,也能保持其战略影响力。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电气化正在推动对低摩擦电动动力传动系统轴承的需求成长。

- 亚洲汽车製造业的快速成长推动了销售需求。

- 随着车辆使用寿命延长,售后市场不断扩大。

- 原始设备製造商 (OEM) 专注于轻量化和紧凑型模组集成

- 用于ADAS和自动驾驶的整合式感测器轴承

- 积层製造的笼架改良了客製化的高转速设计

- 市场限制

- 合金钢和特殊钢价格的波动对利润率造成压力。

- 假冒低价轴承侵蚀了原厂/售后市场的利润。

- 贸易摩擦和物流成本导致供应链中断

- 简化电动车传动系统:减少每辆车的轴承数量

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按轴承类型

- 滑动轴承

- 滚动轴承

- 滚珠轴承

- 滚轮轴承

- 圆柱滚子

- 滚锥轴承

- 材料

- 钢

- 陶瓷混合材料

- 聚合物及其他

- 按车辆类型

- 搭乘用车

- 轻型商用车(LCV)

- 重型商用车(HCV)

- 摩托车

- 非公路用途(农业、建筑、矿业)

- 透过使用/安装

- 轮端

- 引擎和涡轮增压器

- 变速箱/传动系统

- 转向和悬吊

- 暖通空调、交流发电机及其他配件

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲和纽西兰

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- SKF Ltd.

- Schaeffler AG

- NSK Ltd.

- NTN Corp.

- JTEKT Corp.

- The Timken Company

- MinebeaMitsumi Inc.

- Nachi-Fujikoshi Corp.

- Federal-Mogul(Tenneco)

- Rheinmetall Automotive

- ILJIN Group

- C&U Group

- Wafangdian Bearing Co.(ZWZ)

- ABC Bearings(Timken India)

- Hubei New Torch Science & Tech

- GKN Automotive

- Denso Corp.

- CW Bearing GmbH

- Luoyang LYC Bearing

- SNL Bearings Ltd.

第七章 市场机会与未来展望

The automotive bearings market is expected to grow from USD 21.49 billion in 2025 to USD 22.13 billion in 2026 and is forecast to reach USD 25.64 billion by 2031 at 2.98% CAGR over 2026-2031.

The expansion sits at the intersection of stabilizing internal-combustion volumes and accelerating electrification, reshaping bearing specifications and reducing the average bearing count per vehicle while driving demand for low-friction, high-efficiency solutions. Rolling-element designs continue to dominate core wheel-end, transmission, and e-powertrain positions. Yet, ceramic hybrids, sensor-integrated units, and additive-manufactured cages carve a premium share as OEMs chase energy savings and compact modular layouts. Asia-Pacific anchors global growth on rising light-vehicle builds and local EV adoption. At the same time, North America and Europe focus on aftermarket upgrades and predictive maintenance enabled by intelligent bearings. Margins remain under pressure from steel volatility, tariff levies, and counterfeit inflows, pushing leading suppliers toward vertical integration, advanced materials, and circular-performance business models.

Global Automotive Bearings Market Trends and Insights

Electrification-Led Demand for Low-Friction E-Powertrain Bearings

Electric vehicles require bearings with ultra-low friction and high electrical insulation, pushing suppliers toward ceramic balls, specialized coatings and new cage geometries that curb energy loss and avert electrical discharge. SKF's ultra-low-friction wheel bearing series targets EV hubs by cutting torque drag, while Schaeffler's centrifugal-disc ball bearing lowers friction by 80% and multiplies service life tenfold, highlighting the performance leap now expected in e-powertrain units. Manufacturers also confront stray-current threats that cause pitting, which makes hybrid silicon-nitride solutions a strategic necessity in high-speed motor shafts . Investment flows into dedicated EV lines, with premium pricing offsetting reduced per-vehicle volume, ensuring the automotive bearings market continues to monetize electrification despite lower component counts

Aftermarket Expansion of Longer Vehicle Service Life

The aging vehicle fleet in the United States prompts longer intervals between component replacements, particularly for hub and drivetrain bearings. Advances in surface treatment technologies are helping extend the lifespan of these parts, allowing owners to maintain safety while reducing service frequency. Fleet operators increasingly use data analytics to anticipate mechanical issues, shifting the aftermarket landscape from reactive repairs to proactive, condition-based purchasing. Streamlined distribution channels and direct-to-consumer models enable high-performance bearing products to retain value beyond their initial installation. This evolving structure is helping stabilize demand across the automotive bearings sector, even as new vehicle sales fluctuate

Counterfeit Low-Cost Bearings Eroding OEM/Aftermarket Revenue

JTEKT testing shows counterfeit hub units failing fatigue tests in one-tenth the life of genuine parts . SKF destroyed 15 tons of seized knock-offs, yet improved holographic labels and blockchain traceability only partially stem the tide. In emerging markets, weak legal penalties allow repeat offenders, forcing legitimate suppliers to finance education campaigns and forensic audits. The reputational and warranty costs weigh on the automotive bearings market's OEM and aftermarket segments.

Other drivers and restraints analyzed in the detailed report include:

- Integrated Sensor Bearings Enabling ADAS and Autonomy

- Additive-Manufactured Cages Improving Custom High-RPM Designs

- Supply-Chain Disruptions from Trade Tensions and Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rolling-element products generated 53.10% of 2025 revenue, and are forecast to grow at 5.08% CAGR through 2031. Their dominance stems from balanced cost, load, and speed capabilities that suit wheel hubs, transmissions, and e-axles. Cylindrical and tapered rollers serve heavy-duty drivelines, while deep-groove ball bearings excel in high-speed EV motors where low friction and acoustic comfort are paramount. Longer EV warranty terms favor sealed-for-life units, stimulating demand for integrated lubrication and sensor packages.

The plain-bearing niche persists in tight-package combustion engines and HVAC ancillaries where oscillatory motion prevails, yet its share continues to erode. Meanwhile, cross-roller and needle innovations target compact steering columns and electric park brakes, incrementally lifting value density. As hub module designs migrate to third-generation double-row formats with ABS encoders, rolling-element volumes will rise within premium segments, reinforcing their centrality to the automotive bearings market.

Steel accounted for 76.10% of global shipments in 2025, reflecting mature melting routes, proven fatigue life, and favorable cost. The segment expands more slowly as OEMs pursue electrified platforms where stray-current insulation becomes critical. Ceramic and hybrid units advance at 6.02% CAGR.

Polymer and coated-steel variants fill corrosive or noise-sensitive niches, while surface-engineering breakthroughs-diamond-like carbon, plasma nitriding-prolong service intervals without material substitution. Ceramic costs could drop as kiln utilization rises, trimming the price premium and enticing mid-range EV models. Nonetheless, the automotive bearings market share of steel is expected to remain near two-thirds by 2031, sustained by affordable mass-market ICE and hybrid volumes

The Automotive Bearings Market Report is Segmented by Bearing Type (Plain Bearings and Rolling Element Bearings), Material (Steel, Ceramic and Hybrid, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application/Position (Wheel End, Engine and Turbocharger, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific owned 43.40% of 2025 revenue and is forecast to grow at a 6.55% CAGR, buoyed by China's scale, India's double-digit assembly additions, and ASEAN's fast-rising supplier networks. Chinese OEMs integrate locally produced hybrid-ceramic hubs to meet EV warranty demands, while India's Make-in-India drive cuts import dependence from 40% toward 25% by mid-decade. Government subsidies for battery electric two-wheelers broaden demand for compact deep-groove products, reinforcing the region's contribution to the automotive bearings market.

North America sustains a sizeable share anchored by high pickup and SUV output plus a mature replacement cycle. The Biden-era tariff landscape adds USD 8 billion in annual components costs, nudging suppliers like Schaeffler to open the USD 230 million Ohio e-axle plant that shortens supply chains and secures OEM approvals. Mexico's cost-effective machining clusters attract ring-forging investments that backfill U.S. shortages, while Canada leverages raw-steel availability. The region's aftermarket remains resilient as average vehicle age climbs past 12.8 years, propping revenue inside the automotive bearings market despite volatile new-car sales.

Europe wrestles with slower light-vehicle production yet accelerates EV mandates that lift demand for sensor-integrated and hybrid-ceramic solutions. Germany leads R&D spending; Sweden-based SKF pilots circular-performance reclad programs that align with EU Green Deal objectives. Schaeffler's consolidation-closing Austria's Berndorf plant while upgrading Slovakia's Kysuce site-highlights ongoing cost realignment. The U.K., France and Italy pursue localized e-axle builds that favor regional bearing sourcing, ensuring the continent holds strategic sway even as its share modestly contracts within the automotive bearings market.

- SKF Ltd.

- Schaeffler AG

- NSK Ltd.

- NTN Corp.

- JTEKT Corp.

- The Timken Company

- MinebeaMitsumi Inc.

- Nachi-Fujikoshi Corp.

- Federal-Mogul (Tenneco)

- Rheinmetall Automotive

- ILJIN Group

- C&U Group

- Wafangdian Bearing Co. (ZWZ)

- ABC Bearings (Timken India)

- Hubei New Torch Science & Tech

- GKN Automotive

- Denso Corp.

- CW Bearing GmbH

- Luoyang LYC Bearing

- SNL Bearings Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-Led Demand for Low-Friction E-Powertrain Bearings

- 4.2.2 Rapid Vehicle Production Growth in Asia Driving Volume Demand

- 4.2.3 Aftermarket Expansion of Longer Vehicle Service Life

- 4.2.4 OEM Focus on Lightweight, Compact Module Integration

- 4.2.5 Integrated Sensor Bearings Enabling ADAS and Autonomy

- 4.2.6 Additive-Manufactured Cages Improving Custom High-RPM Designs

- 4.3 Market Restraints

- 4.3.1 Volatile Alloy and Specialty-Steel Prices Squeezing Margins

- 4.3.2 Counterfeit Low-Cost Bearings Eroding OEM/Aftermarket Revenue

- 4.3.3 Supply-Chain Disruptions from Trade Tensions and Logistics Costs

- 4.3.4 EV Driveline Simplification: Reducing Bearing Count Per Vehicle

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value in USD)

- 5.1 By Bearing Type

- 5.1.1 Plain Bearings

- 5.1.2 Rolling Element Bearings

- 5.1.2.1 Ball Bearings

- 5.1.2.2 Roller Bearings

- 5.1.2.2.1 Cylindrical Roller

- 5.1.2.2.2 Tapered Roller

- 5.2 By Material

- 5.2.1 Steel

- 5.2.2 Ceramic & Hybrid

- 5.2.3 Polymer & Others

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCV)

- 5.3.3 Heavy Commercial Vehicles (HCV)

- 5.3.4 Two-Wheelers

- 5.3.5 Off-Highway (Agriculture, Construction, Mining)

- 5.4 By Application / Position

- 5.4.1 Wheel End

- 5.4.2 Engine & Turbocharger

- 5.4.3 Transmission & Driveline

- 5.4.4 Steering & Suspension

- 5.4.5 HVAC, Alternator & Other Accessories

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia & New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle-East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle-East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 SKF Ltd.

- 6.4.2 Schaeffler AG

- 6.4.3 NSK Ltd.

- 6.4.4 NTN Corp.

- 6.4.5 JTEKT Corp.

- 6.4.6 The Timken Company

- 6.4.7 MinebeaMitsumi Inc.

- 6.4.8 Nachi-Fujikoshi Corp.

- 6.4.9 Federal-Mogul (Tenneco)

- 6.4.10 Rheinmetall Automotive

- 6.4.11 ILJIN Group

- 6.4.12 C&U Group

- 6.4.13 Wafangdian Bearing Co. (ZWZ)

- 6.4.14 ABC Bearings (Timken India)

- 6.4.15 Hubei New Torch Science & Tech

- 6.4.16 GKN Automotive

- 6.4.17 Denso Corp.

- 6.4.18 CW Bearing GmbH

- 6.4.19 Luoyang LYC Bearing

- 6.4.20 SNL Bearings Ltd.

7 Market Opportunities & Future Outlook

汽车轴承市场:2026-2032年全球市场预测(按轴承类型、材质、安装位置、车辆类型、销售管道和应用划分)汽车止推垫圈市场:依设计、材料类型、厚度、製造流程、通路、应用与车辆类型划分-2026-2032年全球市场预测

汽车轴承市场:2026-2032年全球市场预测(按轴承类型、材质、安装位置、车辆类型、销售管道和应用划分)汽车止推垫圈市场:依设计、材料类型、厚度、製造流程、通路、应用与车辆类型划分-2026-2032年全球市场预测 乘用车衬套市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年

乘用车衬套市场规模、份额、成长及全球产业分析:按类型、应用和地区划分,并预测至2026-2034年 中重型商用车轴承市场-全球产业规模、份额、趋势、机会及预测(按应用、轴承类型、地区及竞争格局划分,2021-2031年)乘用车轴承市场 - 全球产业规模、份额、趋势、机会、预测:按应用、轴承类型、地区和竞争格局划分,2021-2031年乘用车轴承市场 - 全球产业规模、份额、趋势、机会与预测:车辆类型、应用类型、轴承类型、地区和竞争格局,2021-2031年汽车轴承市场-全球产业规模、份额、趋势、机会和预测:按轴承类型、应用类型、车辆类型、地区和竞争格局划分,2021-2031年轻型商用车轴承市场 - 全球产业规模、份额、趋势、机会及预测(按应用、轴承类型、地区和竞争格局划分,2021-2031年)车轮轴承密封件市场按产品类型、材料、车辆类型、最终用户和分销管道划分,全球预测(2026-2032年)商用车轴承市场-全球产业规模、份额、趋势、机会及预测,依车辆类型、应用类型、轴承类型、地区及竞争格局划分,2021-2031年预测

中重型商用车轴承市场-全球产业规模、份额、趋势、机会及预测(按应用、轴承类型、地区及竞争格局划分,2021-2031年)乘用车轴承市场 - 全球产业规模、份额、趋势、机会、预测:按应用、轴承类型、地区和竞争格局划分,2021-2031年乘用车轴承市场 - 全球产业规模、份额、趋势、机会与预测:车辆类型、应用类型、轴承类型、地区和竞争格局,2021-2031年汽车轴承市场-全球产业规模、份额、趋势、机会和预测:按轴承类型、应用类型、车辆类型、地区和竞争格局划分,2021-2031年轻型商用车轴承市场 - 全球产业规模、份额、趋势、机会及预测(按应用、轴承类型、地区和竞争格局划分,2021-2031年)车轮轴承密封件市场按产品类型、材料、车辆类型、最终用户和分销管道划分,全球预测(2026-2032年)商用车轴承市场-全球产业规模、份额、趋势、机会及预测,依车辆类型、应用类型、轴承类型、地区及竞争格局划分,2021-2031年预测