|

市场调查报告书

商品编码

1934687

越南农业机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Vietnam Agricultural Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

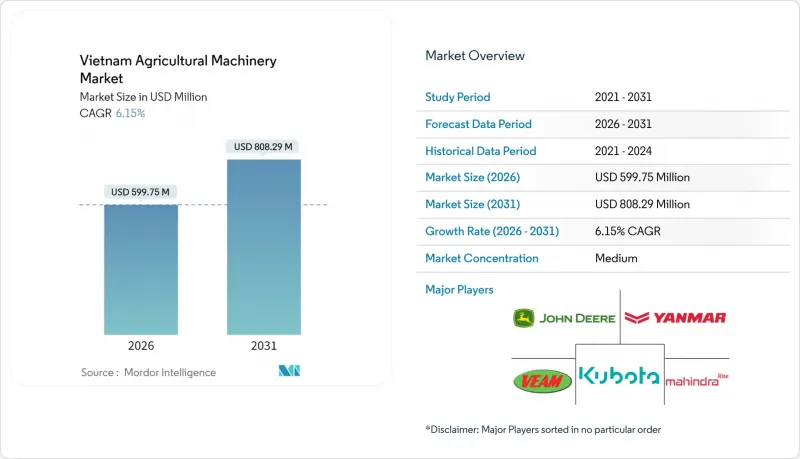

预计到 2026 年,越南农业机械市场规模将达到 5.9975 亿美元,高于 2025 年的 5.65 亿美元。

预计到 2031 年将达到 8.0829 亿美元,2026 年至 2031 年的复合年增长率为 6.15%。

政府的机械化措施、农村劳动力减少以及融资管道的改善正在推动市场成长。频繁的拖拉机升级换代、透过「百万公顷优质水稻」计画推广的精准播种设备以及完善的售后服务,都为市场扩张提供了支撑。不断增长的大米出口收入、合作机械共用系统的普及以及农村电气化项目,也进一步促进了市场的持续成长。电动车、自主农业机器人和数据驱动型农业解决方案在市场中展现出巨大的潜力。目前,该行业仍由几家成熟的企业占据,集中度适中。

越南农业机械市场趋势与展望

农业劳动力减少

随着年轻一代不断涌向都市区,越南的农业劳动力正逐渐老化。这种人口结构的变化推动了水稻、水果和经济作物种植系统对机械化的需求。土地集约化程度的提高使得拖拉机、收割机和机械播种机等农机设备更加经济实惠。季节性人事费用的上升正在影响农民的利润,尤其是在播种和收穫的高峰期。

加强机械化推广措施

越南政府透过财政奖励和政策改革支持农业机械化。政府为农民提供低利率贷款、税收优惠以及示范农场的使用机会,鼓励他们采用现代化设备。成立于2025年2月的农业与环境部旨在提高农业和农村部门的协调性和效率。农村智慧农场正在展示自动化灌溉和土壤分析系统的有效性。农民可以利用补贴信贷和低利率来取代老旧机械,从而促进先进农业机械的普及。

小规模农场的碎片化

越南农业以小规模为主,限制了机械化的经济效益。 70%的农民耕种面积不足0.5公顷,降低了机械投资报酬率。土地零散不仅降低了曳引机的效率,也使得农机具在多块地块间的使用更加复杂。土地整合改革初期取得了一些成效,但人们对祖传土地的文化依恋阻碍了改革的进展。合作社模式和客製化租赁服务透过资源共用提供了一些解决方案,但其有效性取决于强有力的管治和协调。在土地整合得到更广泛的应用和服务体係成熟之前,土地碎片化将继续阻碍农业机械的普及,限制生产力的提升和农业部门的转型。

细分市场分析

拖拉机在越南农业机械市场规模中占比高达54.40%,在土地耕作、运输和残茬管理等方面发挥关键作用。这一细分市场的重要性与越南的机械化目标和较高的土地耕作机械化率相符。小型拖拉机在北部分散的农田中仍然很受欢迎,而中型拖拉机则在南部集中的农业区得到越来越广泛的应用。四轮驱动系统和精准转向功能的集成,使得拖拉机的更新换代需求旺盛,通常以改造现有设备的方式进行。拖拉机仍然是越南农业机械化作业的基础,能够适应各种不同的地理条件和农场结构。

预计种植机械领域将以7.55%的复合年增长率达到最高成长,主要得益于农民从人工播种水稻转向使用条播机和插秧机。这些技术提高了种子发芽率并降低了种子消耗,尤其有利于农业合作社。在国家政策的支持下,种植设备市场份额可望扩大。由于农业劳动力短缺和粮食品质标准日益严格,收割机械领域维持了稳定成长。牧场和饲料设备领域为北部高地的畜牧业提供支援。 「其他产品类型」市场正在扩张,各公司纷纷推出无人机、自主机器人和基于服务的模式,以降低资本投入,这预示着农业自动化未来的发展趋势。久保田的多用途平台机器人引领多角色自动化的发展,能够在单一任务中执行多种功能。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 农业劳动力减少

- 加强机械化推广措施

- 优惠的贸易政策

- 与美国出口相关的现金流激增将足以支付设施更新的资本支出。

- 农业无人机服务合作社减少了农药的使用

- 原厂配套融资计划

- 市场限制

- 将土地分割成小规模农场

- 高昂的初始投资成本

- 农村地区电气化率低阻碍了电动拖拉机的普及。

- 配备远端资讯处理系统的机器面临日益严重的网路安全风险

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 联结机

- 引擎功率

- 不到15马力

- 15-30马力

- 31-45马力

- 46-75马力

- 超过75马力

- 引擎功率

- 种植机械

- 收割机

- 干草和饲料机械

- 其他产品类型

- 联结机

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Vietnam Engine & Agricultural Machinery Corp(VEAM)

- Iseki & Co., Ltd.

- Truong Hai Group Corporation(THACO)

- Deere & Company(TTC Bien Hoa)

- Mahindra & Mahindra Ltd.

- Yamabiko Corporation

- LS Group

- Zetor Tractors as(HTC Investments)

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Netafim Ltd.(Orbia)

第七章 市场机会与未来展望

The Vietnam agricultural machinery market size in 2026 is estimated at USD 599.75 million, growing from 2025 value of USD 565 million with 2031 projections showing USD 808.29 million, growing at 6.15% CAGR over 2026-2031.

Government mechanization initiatives, decreasing rural workforce availability, and improved financing options drive market growth. The market expansion is supported by frequent tractor upgrades, increased adoption of precision planting equipment through the "One Million Hectares of High-Quality Rice" program, and comprehensive after-sales services. The market's sustained growth is further supported by increased rice export revenues, growing adoption of cooperative machinery-sharing systems, and rural electrification programs. The market shows significant potential in electric vehicles, autonomous farming robots, and data-driven agricultural solutions. The industry remains moderately concentrated under these established companies.

Vietnam Agricultural Machinery Market Trends and Insights

Declining Agricultural Labor Availability

Vietnam's agricultural labor force continues to decline as younger generations migrate to urban areas, leaving an aging population of growers. This demographic shift increases the demand for mechanization across rice, fruit, and industrial crop systems. The consolidation of agricultural land makes tractors, harvesters, and mechanical planters more economically viable. Increasing seasonal labor costs impact farm margins, particularly during peak planting and harvesting periods.

Rising Mechanization Incentives

The Vietnamese government supports agricultural mechanization through financial incentives and policy reforms. Farmers receive soft loans, tax relief, and access to demonstration farms to encourage the adoption of modern equipment. The establishment of the Ministry of Agriculture and Environment in February 2025 aims to enhance coordination and efficiency in the agriculture and rural sector.Provincial smart farms demonstrate the effectiveness of automated irrigation and soil analytics systems. Farmers can access subsidized credit lines and reduced interest rates to replace outdated machinery, facilitating broader access to advanced agricultural equipment.

Small Farm-size Fragmentation

Vietnam's agricultural landscape is dominated by small farms, which limits the economic viability of mechanization. Seventy percent of farms operate on less than 0.5 hectares, weakening machinery payback ratios. The fragmented plots reduce tractor efficiency and complicate implement usage across multiple fields. While land consolidation reforms show early promise, cultural ties to ancestral land slow progress. Cooperative models and custom hire services offer partial solutions through resource pooling, but their effectiveness depends on strong governance and coordination. Until consolidation becomes more widespread and service ecosystems mature, fragmentation will continue to hinder agricultural machinery adoption, limiting productivity gains and sector transformation.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Trade Policy

- Surge in Rice-export-linked Cashflows Funding Equipment Upgrades

- High Up-front Capex

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The tractor segment accounts for 54.40% of the Vietnam agricultural machinery market size, serving essential functions in land preparation, transportation, and residue management. The segment's prominence aligns with national mechanization objectives and high mechanized land preparation rates. While compact tractors remain prevalent in the fragmented northern farmlands, mid-range models see increasing adoption in the consolidated southern agricultural regions. The integration of four-wheel drive systems and precision steering capabilities, often as retrofits to existing equipment, maintains strong replacement demand. Tractors remain fundamental to Vietnam's mechanized farming operations, serving diverse geographical conditions and farm structures.

The planting machinery segment demonstrates the highest growth rate at 7.55% CAGR, as farmers transition from manual rice seed broadcasting to drill seeders and transplanters. These technologies improve germination rates and reduce seed consumption, particularly benefiting agricultural cooperatives. The market share for planting equipment is projected to increase, supported by national initiatives promoting efficient input usage. The harvesting machinery segment maintains steady growth due to agricultural labor shortages and stricter grain quality requirements. The haying and forage equipment segment supports livestock operations in the northern highlands. The market sees companies entering the other product types category with drones and autonomous robots, introducing service-based models that reduce capital requirements and indicate future trends in agricultural automation. Kubota's versatile platform robots preview multirole automation that can perform multiple functions in a single pass.

The Vietnam Agricultural Machinery Market Report is Segmented by Product Type (Tractors, Planting Machinery, Harvesting Machinery, Haying and Forage Machinery, and Other Product Types). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Kubota Corporation

- Yanmar Holdings Co., Ltd.

- Vietnam Engine & Agricultural Machinery Corp (VEAM)

- Iseki & Co., Ltd.

- Truong Hai Group Corporation (THACO)

- Deere & Company (TTC Bien Hoa)

- Mahindra & Mahindra Ltd.

- Yamabiko Corporation

- LS Group

- Zetor Tractors a.s. (HTC Investments)

- Zoomlion Heavy Industry Science and Technology Co., Ltd.

- Netafim Ltd. (Orbia)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Declining Agricultural Labor Availability

- 4.2.2 Rising Mechanization Incentives

- 4.2.3 Favorable Trade Policy

- 4.2.4 Surge in Rice-export-linked Cashflows Funding Equipment Upgrades

- 4.2.5 Ag-drone Service Cooperatives Reducing Pesticide Spend

- 4.2.6 OEM Bundled-finance Programs

- 4.3 Market Restraints

- 4.3.1 Small Farm-size Fragmentation

- 4.3.2 High Up-front Capex

- 4.3.3 Low Rural Electrification Hindering Electric Tractors

- 4.3.4 Rising Cybersecurity Risk in Tele-matics-equipped Machines

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Tractors

- 5.1.1.1 Engine Power

- 5.1.1.1.1 Less than 15 HP

- 5.1.1.1.2 15 to 30 HP

- 5.1.1.1.3 31 to 45 HP

- 5.1.1.1.4 46-75 HP

- 5.1.1.1.5 More than 75 HP

- 5.1.1.1 Engine Power

- 5.1.2 Planting Machinery

- 5.1.3 Harvesting Machinery

- 5.1.4 Haying and Forage Machinery

- 5.1.5 Other Product Types

- 5.1.1 Tractors

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Kubota Corporation

- 6.4.2 Yanmar Holdings Co., Ltd.

- 6.4.3 Vietnam Engine & Agricultural Machinery Corp (VEAM)

- 6.4.4 Iseki & Co., Ltd.

- 6.4.5 Truong Hai Group Corporation (THACO)

- 6.4.6 Deere & Company (TTC Bien Hoa)

- 6.4.7 Mahindra & Mahindra Ltd.

- 6.4.8 Yamabiko Corporation

- 6.4.9 LS Group

- 6.4.10 Zetor Tractors a.s. (HTC Investments)

- 6.4.11 Zoomlion Heavy Industry Science and Technology Co., Ltd.

- 6.4.12 Netafim Ltd. (Orbia)

7 Market Opportunities and Future Outlook

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测

除草机器人市场:按组件、类型、运作方式、销售管道、应用和最终用途划分-2026-2032年全球市场预测农作物残渣处理机械市场:按类型、机械化程度、动力来源、应用、最终用途和分销管道划分-2026-2032年全球市场预测 2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分)

2026年全球自主作物残茬管理机器人市场报告农业橡胶履带市场:2026-2032年全球市场预测(依应用程式、销售管道、履带宽度、橡胶配方类型、履带长度及最终用户类型划分) 自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)

自主农业车辆市场:策略性洞察与预测(2026-2031年)全球农业机械市场规模、份额、趋势和成长分析报告(2026-2034年)溶离设备市场:2026-2032年全球市场预测(依设备类型、自动化程度、技术、应用、最终用户及销售管道)农业和施工机械市场:按产品类型、功率范围、发动机类型、应用、最终用户和分销管道划分——2026-2032年全球预测谷物螺旋输送机市场:按类型、动力来源、容量、应用、最终用户和分销管道划分-2026-2032年全球预测红外线沥青加热器市场:按产品类型、电源、移动性、应用、最终用户、分销管道划分,全球预测(2026-2032年)