|

市场调查报告书

商品编码

1934720

特效颜料:市占率分析、产业趋势与统计、成长预测(2026-2031)Special Effect Pigments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

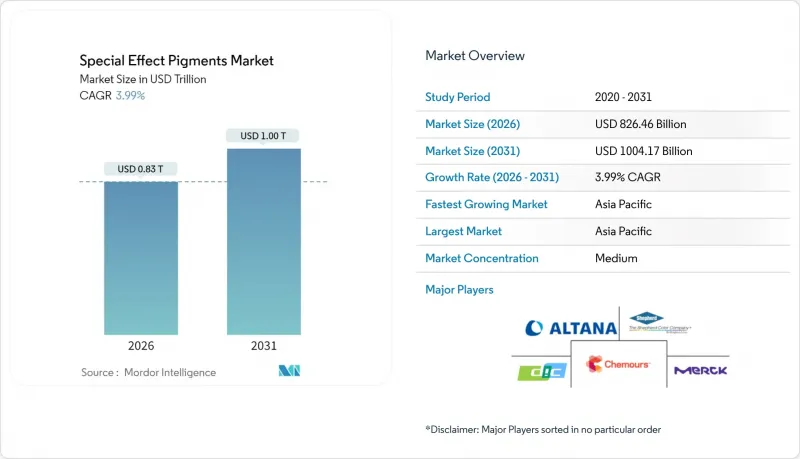

预计到 2026 年,特效颜料市场规模将达到 8,264.6 亿美元,高于 2025 年的 7,947.8 亿美元,预计到 2031 年将达到 1,0417 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 3.99%。

市场特征以结构性变化而非表面增长率为特征,行业快速整合、消费品和工业产品中高端饰面的激增以及向永续製造的转型共同塑造了竞争格局。珠光漆,尤其是基于合成云母基材的珠光漆,因其兼具金属光泽和符合法规要求,仍然是市场需求的关键。汽车原始设备製造商 (OEM) 正在收紧全球配色标准,这使得能够确保雷达渗透性和水性漆系统批次间一致性的供应商更有价值。同时,化妆品、塑胶和先进显示器领域的需求成长正在扩大客户群体,而亚太地区的生产基地则确保了原材料和劳动力的高效利用,从而压缩了整个价值链的成本曲线。

全球特效颜料市场趋势及洞察

汽车原厂配套和修补漆领域对优质涂装材料的需求激增

汽车设计工作室正在采用更深层的色彩空间和多层光学效果来打造差异化的下一代车型。BASF2025年的色彩趋势调色盘融合了红外线渗透性颜料和生物基树脂,以避免干扰自动驾驶感应器。雷达渗透性要求正在淘汰传统的金属薄片,从而推动珠光和水晶玻璃技术的发展,以兼顾美观和感测器性能。随着水性面漆在欧洲OEM生产线上逐渐普及,颜料製造商被要求证明其产品在低VOC含量下具有长期分散稳定性。这种转变在修补漆领域也十分普遍,钣金车间依靠光强度来重现原厂颜色。这确保了对能够将修补面板的颜色还原到原厂效果的特效颜料的持续需求。总而言之,这些要求正在推动供应商整合,因为全球汽车製造商倾向于选择能够以相同品质标准在多个大洲交付产品的精选供应商。

视觉效果显着的化妆品和个人保健产品迅速流行

智慧型手机主导的美妆文化已将光学奇观转变为主流期待,推动了对全像和珠光微孔盘的需求,这些微孔板可在肌肤和指甲上打造色彩晕染和光泽效果。美国食品药物管理局 (FDA) 将天然云母永久列入眼科用途清单,在消费者日益关注成分安全性的当下,提供了监管的确定性。各大品牌如今纷纷强制要求产品线不含重金属,推动了合成云母和硼硅酸玻璃基底的普及,这些材料具有更高的颗粒均匀性和更低的微量金属含量。亚洲的韩妆创新者正在加速潮流发展,缩短产品生命週期,并迫使颜料供应商采用灵活的小批量生产模式,以便在数週内交付客製化色号。虽然利润空间不断扩大,但由于每种新颜色都需要全球合规认证文件,因此维修成本也不断上升。

金属效果颜料需遵守严格的REACH法规和VOC限值。

REACH法规驱动的捲宗更新要求提供铝箔和铜箔的详尽毒性数据,迫使中小颜料生产商投入不成比例的合规预算,否则将退出该地区市场。同时,从溶剂型黏合剂向水性黏合剂的过渡,也迫使传统压片剂进行配方调整,因为这些压片剂在碱性介质中会溶解或气化。拥有专有封装和钝化技术的供应商可以将监管方面的阻力转化为能够建立客户忠诚度的服务,而后进企业面临更长的核准週期,从而侵蚀收入。

细分市场分析

珠光颜料在2025年占据了特效颜料市场51.02%的份额,预计到2031年将保持4.07%的最快增速,巩固主导地位。玻璃片和合成云母配方具有雷达渗透性和超低重金属含量,拓展了其应用范围,并在电动车外饰和高端化妆品粉末领域备受青睐。特效颜料市场受益于原始设备製造商(OEM)在透明涂层层中整合可变厚度薄片技术,该技术可产生色彩渐变效果,同时最大限度地减少油漆变色,减少喷涂工序,缩短生产週期。

金属颜料在保护性面漆领域仍占据核心地位,但在特效颜料市场份额正在下降,因为雷达相容性比亮度更为重要。拥有先进二氧化硅封装製程的供应商透过将技术授权给区域性代工加工商来保护利润,避免智慧财产权稀释并维持规模。光学可变颜料和全像颜料正被应用于安全油墨和品牌保护标籤。虽然整体市场规模较小,但它们仍然是策略性延伸,而非简单的产品添加物,因为它们能够提供高于平均水平的价格并增强产品组合的盈利。

特效颜料报告按颜料类型(金属色、珠光色及其他)、终端用户产业(涂料、化妆品、塑胶、印刷油墨及其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区以及中东和非洲地区)进行细分。市场预测以美元以金额为准。

区域分析

预计到2025年,亚太地区将占特效颜料市场规模的45.12%,并在2031年之前以4.55%的复合年增长率增长,巩固其作为全球製造地的地位。中国在汽车涂料领域的领先地位支撑了区域需求,而印度装饰涂料市场超过7%的成长则推动了珠光分散体的需求。政府为促进电动车在地化生产而推出的激励措施吸引了对整个亚太地区统一色库需求的外国製造商,促使颜料製造商在该地区建立技术服务实验室。越南和马来西亚等东南亚电子产业丛集正在进一步拓展其下游管道,吸收用于智慧型手机机壳和穿戴式装置外壳的高纯度特效颜料。

欧洲拥有强大的监管影响力,能够塑造全球配方标准。 REACH法规和2023年《微塑胶法规》正加速向生物基界面活性剂和包覆金属薄片的转变,而这种政策环境也为领先采用者提供了合理的溢价空间。德国和义大利的汽车製造商正在推动使用更薄的透明涂层,以提高每微米的光学提升效果,这就要求颜料供应商提供更高长宽比和更严格的粒径控制。在建筑涂料领域,北欧国家製定了近零VOC标准,这些标准正在欧洲迅速推广,从而提高了未获得水性涂料认证的进口配方的技术门槛。

在北美,汽车修补漆市场依然强劲,对金属漆和珠光漆修补产品的需求保持稳定。美国食品药物管理局(FDA)对云母的永久性着色剂豁免,稳定了化妆品效果颜料的原料选择,并简化了新颜色上市的认证流程。墨西哥汽车组装厂的扩张活性化了跨境颜料物流,美国供应商正利用近岸外包来缩短前置作业时间。中东和非洲地区拥有长期成长潜力,基础设施项目加速了装饰涂料的使用。然而,当地产能有限意味着进口依赖度仍然很高,这有利于拥有综合货运网络的跨国公司。南美洲的颜料需求集中在巴西的汽车产业带,但货币波动需要对冲策略来管理汇款收入。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车OEM和修补漆领域对优质涂装材料的需求激增

- 视觉特效化妆品和个人保健产品的快速普及

- 转型为永续性/转向水性涂料和粉末涂料

- 亚太地区工业基础的扩张正在推动对油漆和塑胶的需求。

- AR/VR和家用电子电器对光学活性颜料的需求

- 市场限制

- 对金属效果颜料实施严格的REACH和VOC限制

- 挥发性铝和二氧化钛的成本基础

- 合成云母颗粒的监管

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依颜料类型

- 金属

- 珍珠色调

- 其他颜料类型

- 按最终用户行业划分

- 油漆和涂料

- 化妆品

- 塑胶

- 印刷油墨

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 马来西亚

- 泰国

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 卡达

- 阿拉伯聯合大公国

- 奈及利亚

- 埃及

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- ALTANA(ECKART)

- DIC Corporation

- Merck KGaA

- NIHON KOKEN KOGYO CO.,LTD

- OXERRA Americas

- RPM International Inc.

- SCHLENK SE

- Shepherd Color

- Silberline Manufacturing Co., Inc.

- Sudarshan Chemical Industries Limited

- The Chemours Company

- VIAVI Solutions Inc.

第七章 市场机会与未来展望

Special Effect Pigments market size in 2026 is estimated at USD 826.46 billion, growing from 2025 value of USD 794.78 billion with 2031 projections showing USD 1004.17 billion, growing at 3.99% CAGR over 2026-2031.

Structural change rather than headline growth defines the landscape, with rapid consolidation, premium-finish adoption across consumer and industrial goods, and a pivot toward sustainable manufacturing dictating competitive outcomes. Pearlescent grades remain the fulcrum of demand because they deliver both metallic brilliance and regulatory compliance, especially when based on synthetic mica substrates. Automotive OEMs have tightened global color-matching standards, elevating suppliers that can guarantee batch-to-batch consistency in radar-transparent and water-borne systems. Parallel momentum in cosmetics, plastics, and advanced displays is deepening the customer mix, while the Asia-Pacific production base secures raw-material and labor efficiencies that compress cost curves for the entire value chain.

Global Special Effect Pigments Market Trends and Insights

Surging Demand for Premium Finishes in Automotive OEM and Refinish

Automotive design studios are specifying deeper color spaces and multilayer optical effects to differentiate next-generation vehicles. BASF's 2025 color trend palette integrates bio-based resins with infrared-transparent pigments that do not interfere with autonomous driving sensors. Radar transparency disqualifies conventional metallic flakes, adding urgency to pearlescent and crystal-glass innovations that marry aesthetics with sensor performance. Water-borne topcoats now dominate European OEM lines, compelling pigment makers to demonstrate long-term dispersion stability at low VOC levels. The shift extends to refinish operations, where body shops deploy spectrophotometers to replicate OEM shades, guaranteeing ongoing demand for effect pigments able to match factory finishes on repaired panels. These requirements collectively reinforce supplier consolidation because global automakers favor a tightly curated vendor list that can service multi-continent programs with identical quality metrics.

Rapid Uptake of Visual-Effect Cosmetics and Personal-Care Products

Smartphone-driven beauty culture has converted optical novelty into mainstream expectation, lifting demand for holographic and pearlescent microplates that create color-travel and sparkle on skin and nails. The permanent FDA listing of natural mica for eye-area use provides regulatory certainty just as consumers intensify scrutiny of ingredient safety. Major brands now stipulate heavy-metal-free portfolios, encouraging the migration toward synthetic mica and borosilicate glass bases that offer higher platelet uniformity and lower trace metals. Asia's K-beauty innovators accelerate trend cycles, shortening product lifetimes and forcing pigment suppliers to operate agile, small-batch manufacturing that can deliver bespoke shades within weeks. While margin potential rises, sustainment costs climb as firms must certify worldwide compliance dossiers for each new hue.

Stringent REACH and VOC Limits on Metal-Based Effect Pigments

REACH dossier updates demand exhaustive toxicological data for aluminum and copper flakes, obliging smaller pigment companies to allocate disproportionate compliance budgets or exit the region. Simultaneously, the move from solvent to water-borne binders forces reformulation because traditional leafing agents dissolve or gas in alkaline media. Suppliers equipped with proprietary encapsulation and passivation know-how can transform regulatory friction into loyalty-building service, but late adopters are confronting prolonged approval cycles that erode revenue.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability Shift to Water-Borne and Powder Coatings

- APAC Industrial Build-Out Boosting Coatings and Plastics Demand

- Volatile Aluminum and TiO2 Cost Base

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pearlescents held 51.02% of the special-effect pigments market share in 2025 and are forecast to maintain the fastest 4.07% CAGR to 2031, confirming their dual status as volume and growth leader. Glass-flake and synthetic mica formulations widen the application canvas by providing radar transparency and ultralow heavy-metal content, attributes prized in electric-vehicle exteriors and luxury-cosmetic powders. The special-effect pigments market benefits as OEM clear-coat layers integrate variable-thickness lamellae that produce color-travel with minimal flop, cutting paint-shop passes and lowering cycle times.

Metallic grades retain core positions in protective topcoats, yet their share of the special-effect pigments market is slipping where radar compliance outranks sparkle intensity. Vendors with advanced silica encapsulation processes defend margins by licensing technology to regional tollers, securing scale without dilution of intellectual property. Optically variable and holographic pigments serve security inks and brand-protection labels; although collectively smaller, they achieve above-average pricing and bolster portfolio profitability, ensuring they remain a strategic extension rather than a commodity add-on.

The Special-Effect Pigments Report is Segmented by Pigment Type (Metallic, Pearlescent, and Other Pigment Types), End-User Industry (Paints and Coatings, Cosmetics, Plastics, Printing Inks, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 45.12% of the special-effect pigments market size in 2025 and is tracking a 4.55% CAGR through 2031, consolidating its role as the global manufacturing hub. China's dominance in automotive coatings underpins regional demand, while India's 7%-plus growth in decorative paints generates incremental volume for pearlescent dispersions. Government incentives for electric-vehicle localization attract foreign assemblers that mandate identical color libraries across continents, encouraging pigment makers to establish in-region technical-service labs. Southeast Asian electronics clusters in Vietnam and Malaysia further diversify downstream channels, absorbing high-purity effect grades for smartphone casings and wearable housings.

Europe wields regulatory influence that shapes worldwide formulation standards. REACH and the 2023 microplastics restriction accelerate the pivot to bio-based surfactants and encapsulated metal flakes, a policy environment that rewards early movers with defensible premium pricing. German and Italian automotive OEMs commit to low-film-thickness clearcoats that intensify optical flop per micron, pushing pigment suppliers toward higher aspect-ratio platelets and tighter particle-size control. In architectural coatings, Nordic countries specify near-zero VOC benchmarks that quickly propagate across the continent, ratcheting technical barriers for imported formulations lacking water-borne credentials.

North America maintains a sizable automotive refinish ecosystem, ensuring predictable pull for metallic and pearlescent touch-up products. The U.S. Food and Drug Administration's permanent listing of mica as an exempt color additive stabilizes raw-material selection for cosmetics effect pigments, streamlining certification for new color launches. Mexico's ascendant vehicle assembly footprint heightens cross-border pigment logistics, with U.S. suppliers leveraging near-shoring to cut lead times. The Middle East and Africa offer long-run upside as infrastructure programs accelerate decorative-coatings use; however, limited local production capacity means import dependence persists, advantaging multinationals with integrated freight networks. South America's pigment demand centers on Brazil's automotive belt, though currency volatility necessitates hedging strategies to manage revenue repatriation.

- ALTANA (ECKART)

- DIC Corporation

- Merck KGaA

- NIHON KOKEN KOGYO CO.,LTD

- OXERRA Americas

- RPM International Inc.

- SCHLENK SE

- Shepherd Color

- Silberline Manufacturing Co., Inc.

- Sudarshan Chemical Industries Limited

- The Chemours Company

- VIAVI Solutions Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Demand for Premium Finishes in Automotive OEM And Refinish

- 4.2.2 Rapid Uptake of Visual-Effect Cosmetics and Personal-Care Products

- 4.2.3 Sustainability Shift to Water-Borne and Powder Coatings

- 4.2.4 APAC Industrial Build-Out Boosting Coatings and Plastics Demand

- 4.2.5 AR/VR and Consumer Electronics Requiring Optically Active Pigments

- 4.3 Market Restraints

- 4.3.1 Stringent REACH and VOC Limits on Metal-Based Effect Pigments

- 4.3.2 Volatile Aluminium and TiO? Cost Base

- 4.3.3 Regulatory Scrutiny of Synthetic-Mica Micro-Particles

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Pigment Type

- 5.1.1 Metallic

- 5.1.2 Pearlescent

- 5.1.3 Other Pigment Types

- 5.2 By End-user Industry

- 5.2.1 Paints and Coatings

- 5.2.2 Cosmetics

- 5.2.3 Plastics

- 5.2.4 Printing Inks

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Malaysia

- 5.3.1.6 Thailand

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Qatar

- 5.3.5.3 United Arab Emirates

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 South Africa

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ALTANA (ECKART)

- 6.4.2 DIC Corporation

- 6.4.3 Merck KGaA

- 6.4.4 NIHON KOKEN KOGYO CO.,LTD

- 6.4.5 OXERRA Americas

- 6.4.6 RPM International Inc.

- 6.4.7 SCHLENK SE

- 6.4.8 Shepherd Color

- 6.4.9 Silberline Manufacturing Co., Inc.

- 6.4.10 Sudarshan Chemical Industries Limited

- 6.4.11 The Chemours Company

- 6.4.12 VIAVI Solutions Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment