|

市场调查报告书

商品编码

1934722

纺织染料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Textile Dye - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

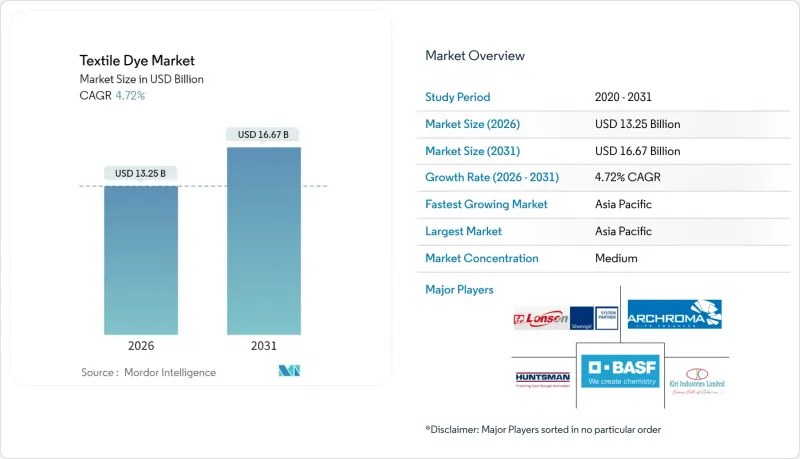

2025年纺织染料市场价值为126.5亿美元,预计到2031年将达到166.7亿美元,而2026年为132.5亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.72%。

快时尚产量不断增长、按需数位印花技术的日益普及以及品牌方日益严格的永续性目标,都推动了对天然系和合成染料系统的需求。同时,持续的产业整合为主要供应商提供了必要的规模,使其能够投资于更环保的化学技术。分散染料因其在聚酯加工中的高价值,将继续保持其在染料类型中的领先地位,预计到2024年将占据32.08%的市场份额,这得益于其在高温加工中的高效性。亚太地区仍是生产中心。中国、印度和越南的政府支持计划,以及电子商务主导的小批量订单,持续推动产能的强劲扩张。同时,欧盟和美国的废水法规正在加速向闭合迴路系统和生物基染料的转型,为能够根据未来数位产品护照要求认证更环保化学技术的供应商创造了近期机会。

全球纺织染料市场趋势及展望

新兴经济体快时尚生产的快速成长

快时尚品牌正在缩短产品系列週期,并鼓励中国、印度和越南的纺纱厂整合高速染色和后整理生产线,以在大批量生产的情况下满足品质要求。光是中国就计画在2025年数位化。在印度,与生产连结奖励计画和新建的综合产业园区已投资72.6亿卢比用于织造、印染设施,从而减少了原材料进口,并提高了对消费趋势的反应速度。越南正在扩大其经济高效的聚酯纤维项目,目标是到2025年实现480亿美元的纺织品出口额,优先发展可快速换色的分散性化学品,以满足全球买家的需求。

按需数位纺织印花技术的兴起

数位设备无需丝网、印版和多余的油墨,即可实现色彩鲜艳的小批量印刷,与旋转印刷工艺相比,节水高达95%。这推动了纺织染料市场对高纯度微胶囊分散染料和活性油墨的需求成长,这些染料和油墨能够以工业级速度可靠地喷射。汽车和航太製造商以及服装品牌已开始试用数位印刷技术,用于对色彩匹配精度和增重要求极低的纺织品——这一细分市场历来难以被传统的批量染色工艺充分满足。

全球加强废水排放法规

欧盟的生态设计法规已将纺织品列为其2025-2030年工作计画的优先事项,要求工厂记录化学品使用情况、延长产品寿命并回收纤维。法国对全氟烷基和多氟烷基物质(PFAS)的禁令进一步强化了这项政策措施。同样,加州的SB 707法案要求美国生产商承担报废回收的成本,这将在闭合迴路基础设施成熟之前加剧成本压力。

细分市场分析

2025年,分散染料在纺织染料市场中占比31.34%,预计到2031年将以5.44%的复合年增长率成长,这主要得益于聚酯材料的持续流行。在合成纤维染料市场,分散染料由于其不溶于水的特性,在120至130°C的温度下能够快速扩散,从而获得鲜艳的色彩和优异的湿牢度。目前,供应商根据均匀性、昇华性和快速批量加工等因素,将产品分为E、SE、S、P和RD系列。同时,对酰肼-Hydrazone偶氮结构的研究可望在较低的pH值范围内达到更高的显色强度。活性染料系统在棉织物中仍发挥重要作用,透过单锚定和多锚定化学的共用锚定,能够达到家用洗涤耐久性标准。肠线染料和硫化染料虽然应用范围较小,但对于需要最高耐光牢度的应用(例如在极端气候下销售的工作服)至关重要。

第二代分散染料也支援无水工艺,例如超临界二氧化碳染色和数位喷墨高固态含量油墨,这两项工艺都优先考虑低浴比。这些创新技术的结合正在推动其在时尚、休閒和产业用纺织品领域的应用,进一步巩固分散染料在纺织染料市场的主导地位。

区域分析

预计到2025年,亚太地区将占全球纺织染料市场的49.10%,并在2031年之前保持最快增速,年复合成长率达5.58%,这主要得益于中国大力推进数位化工厂建设以及印度450亿美元的出口目标。政府支持的产业园区正在整合染色、印花和表面处理工程,以缩短供应链;而越南的出口目标则加剧了区域内对大型运动服装订单的竞争。在地采购纯对苯二甲酸和乙二醇为分散染料生产商提供了支持,确保了在全球运输中断的情况下原材料供应的持续性。

欧洲的法规正在重塑市场需求,并鼓励买家转向透明、可追溯且低风险的染色系统。计划于2030年前实施的数位产品护照和不含PFAS的强制规定,将促使纺纱厂对其助剂进行审核,投资于离子交换废水处理,并采用能够最大限度减少下游排放的原液染色方案。义大利和法国的奢侈品中心正利用这些变化,推出采用永续染色工艺的高端系列产品;而斯堪地那维亚的零售商则在试点回收计划,将机器和化学回收的纤维纳入循环染色工艺。

类似的趋势也出现在北美。加州SB 707法案在美国率先建立了生产者延伸责任制(EPR),促进了许多合作,例如北卡罗来纳州的Cerenis-Cire聚酯回收项目,该项目计划于2025年中期投入运作。同时,Archroma计划在南卡罗来纳州投资75万美元进行扩建,这凸显了生产回流的趋势,旨在确保当地能够获得所需的特种配方,同时降低对某些偶氮中间体的进口依赖。儘管该地区的产量落后于亚洲,但高价值细分市场以及严格的合规要求为创新供应商提供了可观的利润空间。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴经济体快时尚生产的快速成长

- 按需数位纺织印花技术的兴起

- 扩大技术性和防护性纺织品的使用

- 零售品牌永续性要求(生物基染料)

- 电子商务通路小批量服装订单增加

- 市场限制

- 全球废水标准日益收紧

- 石油衍生染料中间体的价格波动

- 天然色棉带来的竞争威胁

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按染料类型

- 活性染料

- 去中心化

- 直接地

- VAT

- 酸性

- 碱性染料

- 其他染料类型

- 依纤维类型

- 棉布

- 聚酯纤维

- 尼龙

- 羊毛

- 丙烯酸纤维

- 黏胶纤维

- 其他纤维类型

- 透过使用

- 服饰

- 家用纺织品

- 工业纤维

- 其他用途

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 埃及

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- AkikDye

- Archroma

- Atul Ltd

- BASF

- Clariant

- Colourtex Industries Private Limited

- Huntsman International LLC

- Jiangsu World Chemical Co., Ltd

- KeyColour

- Kiri Industries Ltd

- Longsheng Group

- Mahickra Chemicals Limited

- NICCA CHEMICAL CO.,LTD.

- Sun Chemical

- TAIYO HOLDINGS CO., LTD.

- Vipul Organics Ltd

第七章 市场机会与未来展望

The Textile Dye Market was valued at USD 12.65 billion in 2025 and estimated to grow from USD 13.25 billion in 2026 to reach USD 16.67 billion by 2031, at a CAGR of 4.72% during the forecast period (2026-2031).

Rising fast-fashion output, wider adoption of on-demand digital printing, and stricter brand sustainability targets are strengthening demand across both natural and synthetic colorant systems, while ongoing consolidation gives large suppliers the scale needed to invest in lower-impact chemistries. Dispersive formulations, prized for polyester processing, held the largest dye-type share at 32.08% in 2024 and continue to benefit from high-temperature application efficiency. Asia-Pacific remains the production hub: supportive government programs in China, India and Vietnam converge with e-commerce-led small-lot orders to keep capacity additions brisk. At the same time, EU and US effluent rules are accelerating the shift toward closed-loop systems and bio-based shades, creating near-term opportunities for suppliers able to certify greener chemistries under future Digital Product Passport requirements.

Global Textile Dye Market Trends and Insights

Soaring Fast-Fashion Output in Emerging Economies

Fast-fashion brands have shortened collection cycles and pushed mills in China, India and Vietnam to integrate high-speed dyeing and finishing lines that meet quality expectations at volume; China alone seeks 70% digitalization of its textile businesses by 2025. Indian production-linked incentives and new integrated parks allocate INR 726 crore for combined weaving, printing and dyeing assets that trim raw-material imports and tighten response times to consumer trends. Vietnam, targeting USD 48 billion in textile exports by 2025, is scaling cost-effective polyester programs that favor dispersive chemistries capable of rapid color changeovers to serve global buyers.

Expansion of On-Demand Digital Textile Printing

Eliminating screens, plates and excess liquor, digital equipment supports vivid short-run designs and drops water use by as much as 95% compared with rotary workflows. The textile dyes market is therefore seeing incremental demand for high-purity, micro-encapsulated dispersive and reactive inks that jet reliably at industrial speeds. Automotive and aerospace makers have joined apparel brands in piloting digitally printed technical textiles that require exact color matches and minimal weight gain, a niche previously underserved by traditional batch dyeing.

Tightening Global Effluent Discharge Norms

The EU Ecodesign regulation prioritizes textiles in its 2025-2030 workplan, compelling mills to document chemical inputs, extend product life and recover fibers, with PFAS bans in France reinforcing the policy push. California's SB 707 similarly obliges US producers to finance end-of-life collection, adding cost pressure until closed-loop infrastructure matures.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Technical & Protective Textile Usage

- Retail Brand Sustainability Mandates Drive Bio-Based Dye Adoption

- Volatility in Petro-Derived Dye Intermediates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dispersive chemistries accounted for 31.34% of the textile dyes market in 2025 and are forecast to rise at 5.44% CAGR through 2031 on the back of polyester's continued popularity. Within the textile dyes market size for colorants applied to synthetics, their water-insoluble nature enables rapid diffusion at 120-130 °C, delivering bright shades and high wet-fastness. Suppliers now segment offerings into E-, SE-, S-, P- and RD-series to target leveling, sublimation or rapid batch objectives, while research into hydrazide-hydrazone azo structures promises even higher color strength at lower pH windows. Reactive systems retain critical roles in cotton, leveraging mono- and multi-anchor chemistry to achieve covalent fixation that passes home-laundry durability standards. Vat and sulfur options remain niche but indispensable where maximum light fastness is mandated, for example on workwear sold into extreme climates.

Second-generation dispersive grades also anchor the drive toward water-free routes such as super-critical CO2 dyeing and digitally jetted high-solids inks, both prioritizing low process-liquor ratios. Combined, these innovations support broader adoption across fashion, athleisure and technical textiles, reinforcing the leadership position of dispersive chemistry in the textile dyes market.

The Textile Dyes Market Report is Segmented by Dye Type (Reactive, Dispersive, Direct, Vat, Acidic, Basic, Other Dye Types), Fiber Type (Cotton, Polyester, Nylon, Wool, Acrylic, Viscose, Other Fiber Types), Application (Apparel, Household Textiles, Industrial Fabrics, Other Applications), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 49.10% of the global textile dyes market in 2025 and is on track to sustain the fastest 5.58% CAGR through 2031, powered by China's digital-factory push and India's USD 45 billion export ambition. Government-backed parks integrate dyeing, printing and finishing to shorten supply chains, while Vietnam's export targets intensify regional rivalry for large sportswear orders. Local access to purified terephthalic acid and mono-ethylene glycol supports dispersed-dye producers, ensuring raw-material continuity despite global shipping disruptions.

Europe's regulatory stance reshapes demand, steering buyers toward transparent, traceable and low-hazard colorant systems. The upcoming Digital Product Passport and a PFAS-free mandate by 2030 will force mills to audit auxiliaries, invest in ion-exchange effluent treatment and adopt dope-dyed solutions that minimize downstream releases. Luxury hubs in Italy and France leverage these changes to market premium sustainably dyed collections, while Scandinavian retailers pilot take-back programs that feed mechanically and chemically recycled fibers into circular dyeing loops.

North America is moving in parallel: California's SB 707 establishes the first US extended-producer system, catalyzing alliances such as the Selenis-Syre polyester recycling venture in North Carolina set for mid-2025 start-up. Concurrently, Archroma's USD 750,000 South Carolina expansion underlines the reshoring trend, ensuring regional access to specialty formulations as import reliance on certain azo intermediates diminishes. While the region sits behind Asia on volume, higher added-value segments and stricter compliance requirements translate to attractive margins for innovative suppliers.

- AkikDye

- Archroma

- Atul Ltd

- BASF

- Clariant

- Colourtex Industries Private Limited

- Huntsman International LLC

- Jiangsu World Chemical Co., Ltd

- KeyColour

- Kiri Industries Ltd

- Longsheng Group

- Mahickra Chemicals Limited

- NICCA CHEMICAL CO.,LTD.

- Sun Chemical

- TAIYO HOLDINGS CO., LTD.

- Vipul Organics Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring Fast-Fashion Output in Emerging Economies

- 4.2.2 Expansion of On-Demand Digital Textile Printing

- 4.2.3 Growth in Technical & Protective Textile Usage

- 4.2.4 Retail Brand Sustainability Mandates (Bio-Based Dyes)

- 4.2.5 E-commerce Led Rise in Small-Lot Apparel Orders

- 4.3 Market Restraints

- 4.3.1 Tightening Global Effluent Discharge Norms

- 4.3.2 Volatility in Petro-Derived Dye Intermediates

- 4.3.3 Competitive Threat from Naturally-Colored Cotton

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Dye Type

- 5.1.1 Reactive

- 5.1.2 Dispersive

- 5.1.3 Direct

- 5.1.4 Vat

- 5.1.5 Acidic

- 5.1.6 Basic

- 5.1.7 Other Dye Types

- 5.2 By Fiber Type

- 5.2.1 Cotton

- 5.2.2 Polyester

- 5.2.3 Nylon

- 5.2.4 Wool

- 5.2.5 Acrylic

- 5.2.6 Viscose

- 5.2.7 Other Fiber Types

- 5.3 By Application

- 5.3.1 Apparel

- 5.3.2 Household Textiles

- 5.3.3 Industrial Fabrics

- 5.3.4 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 AkikDye

- 6.4.2 Archroma

- 6.4.3 Atul Ltd

- 6.4.4 BASF

- 6.4.5 Clariant

- 6.4.6 Colourtex Industries Private Limited

- 6.4.7 Huntsman International LLC

- 6.4.8 Jiangsu World Chemical Co., Ltd

- 6.4.9 KeyColour

- 6.4.10 Kiri Industries Ltd

- 6.4.11 Longsheng Group

- 6.4.12 Mahickra Chemicals Limited

- 6.4.13 NICCA CHEMICAL CO.,LTD.

- 6.4.14 Sun Chemical

- 6.4.15 TAIYO HOLDINGS CO., LTD.

- 6.4.16 Vipul Organics Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

全球纺织染料市场规模、份额、趋势和成长分析报告(2026-2034年)全球纺织染料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球纺织染料市场规模、份额、趋势和成长分析报告(2026-2034年)全球纺织染料市场规模、份额、趋势和成长分析报告(2026-2034年) 日本纺织染料市场规模、份额、趋势和预测:按染料类型、纤维类型、应用和地区划分,2026-2034年

日本纺织染料市场规模、份额、趋势和预测:按染料类型、纤维类型、应用和地区划分,2026-2034年 2026年全球纺织染料市场报告

2026年全球纺织染料市场报告 纺织染料市场规模、份额及成长分析(依原料、染料类型、产品形式、纤维类型、应用、最终用途及地区划分)-产业预测,2026-2033年

纺织染料市场规模、份额及成长分析(依原料、染料类型、产品形式、纤维类型、应用、最终用途及地区划分)-产业预测,2026-2033年 纺织染料市场规模、份额及成长分析(按染料类型、纤维类型、应用和地区划分)-产业预测(2026-2033 年)

纺织染料市场规模、份额及成长分析(按染料类型、纤维类型、应用和地区划分)-产业预测(2026-2033 年) 纤维用染料的全球市场:各类型,各纤维类型,各来源,各用途,各地区-市场规模,产业动态,机会分析,预测(2025年~2033年)

纤维用染料的全球市场:各类型,各纤维类型,各来源,各用途,各地区-市场规模,产业动态,机会分析,预测(2025年~2033年) 纺织染料市场按类型、应用、纤维类型、形态和来源划分-2025-2032年全球预测2025-2033年纺织染料市场报告(依染料类型、纤维类型、应用和地区)全球纺织染料市场规模(按染料类型、纤维类型、类型、最终用户、区域范围和预测)

纺织染料市场按类型、应用、纤维类型、形态和来源划分-2025-2032年全球预测2025-2033年纺织染料市场报告(依染料类型、纤维类型、应用和地区)全球纺织染料市场规模(按染料类型、纤维类型、类型、最终用户、区域范围和预测)