|

市场调查报告书

商品编码

1934733

装饰层压板:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Decorative Laminates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

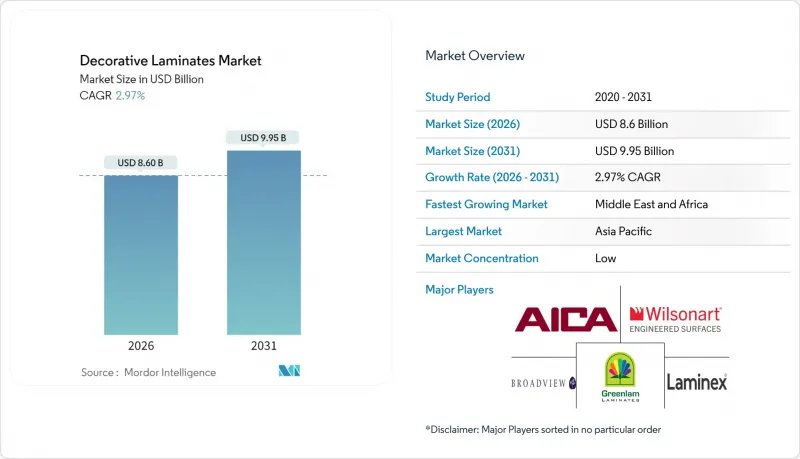

装饰层压板市场预计将从 2025 年的 83.5 亿美元增长到 2026 年的 86 亿美元,预计到 2031 年将达到 99.5 亿美元,2026 年至 2031 年的复合年增长率为 2.97%。

这一增长反映出,即使已开发地区的建筑週期放缓,住宅和商业室内装修计划对经济实惠的饰面材料的需求仍然稳定。亚太地区的快速都市化、印度的大规模公共住宅计划以及中国稳步推进的基础设施建设,都支撑着全球高压层压板和密实层压板的消费。中东和非洲建设活动的同步扩张以及模组化家具的普及,也保持了这一成长势头。同时,技术主导的表面创新使生产商能够获得溢价,并抵御替代材料的竞争,捍卫市场份额。随着遵守低甲醛化学品和木材可追溯性法规的成本不断增加,拥有强大研发能力的垂直整合型企业更具优势,产业整合的压力也日益增大。

全球装饰层压板市场趋势与洞察

快速的都市化和模组化家具的蓬勃发展

新兴市场城市每年迎来数百万新居民,推动了对采用轻质板材和装饰贴面製成的模组化家具的需求,以满足紧凑型生活空间的需求。预计到2050年,印度的城市人口将增加4.16亿,将带动对平板包装家具的需求,与实木家具相比,平板包装家具的运输重量可减轻40%。数位印刷技术使製造商能够小批量开发数百种新设计,Egger的2024+系列(超过300种设计和纹理组合)正是这项策略的体现。同时,贴面材料的需求也在增长,因为优质压花薄膜可以模仿石材和橡木的纹理,同时也具有防刮和防指纹的特性。都市区高密度化和模组化设计的双重驱动力持续推动装饰贴面市场的扩张,而不受新建筑经济週期的影响。

亚太地区住宅建设激增

印度、越南和泰国的政府主导住宅计画正在推动中等价位公寓的持续成长,强化复合地板比天然石材和实木地板更受青睐。光是印度就计画在2030年投入1兆美元用于建筑业,以弥补1亿套房的缺口。越南的建筑业预计到2024年将达到958亿美元,年增率达7%。像CFL Flooring在越南投资1.5亿美元的工厂这样的本地强化复合地板生产企业,缩短了前置作业时间,并有助于稳定价格敏感型市场的价格。该地区对经济适用住宅政策的重视,有助于锁定长期需求,抵销欧洲和美国新建住宅放缓的影响。

酚醛树脂和三聚氰胺树脂的价格波动

酚醛树脂和三聚氰胺树脂约占层压板材料成本的五分之一。 2024年,当其价格飙升18%至25%时,製造商无法即时将成本转嫁给家具OEM客户,导致利润率承压。特种树脂市场由五家跨国供应商主导,使得本地加工商议价能力薄弱,一旦供应中断,便会面临缺货风险,造成交货延迟,并削弱客户信心。

细分市场分析

到2025年,塑胶树脂将保持其在装饰层压板市场40.92%的份额,这凸显了其在将装饰纸黏合到基材上的关键作用。然而,覆膜预计将以3.39%的复合年增长率快速增长,因为数位印刷需要透明、有纹理且在紫外线照射下不会泛黄的薄膜。覆膜用装饰层压板的市场规模预计将稳步扩大,因为防指纹和触感柔软的表面处理工艺能够带来更高的价格差异。木材可追溯性法规以及《化学品註册、评估、授权和限制》(REACH)法规中规定的0.062 mg/m³的甲醛含量上限,正在推动对生物基树脂和无醛体系的投资。虽然这些措施会增加投入成本,但也有助于终端用户获得LEED(能源与环境设计先锋奖)认证积分。此外,低VOC(挥发性有机化合物)化学技术的日益普及也使黏合剂产业受益。

装饰箔和保护膜等辅助原料正变得日益重要,因为它们无需对生产线进行重大维修即可实现产品差异化。掌握抗菌层和刮痕修復微胶囊在线连续涂层技术的製造商,既能满足医疗计划规格要求,又能获得更高的价格。因此,原料创新预计将使供应商的议价能力向那些提供一体化化学包装和技术支援的供应商倾斜。

区域分析

预计到2025年,亚太地区将占全球收入的38.20%,并在2031年之前保持主导地位。这主要得益于印度高达1兆美元的住宅建设热潮以及中国的基础设施投资将支撑市场需求。越南和泰国新增产能将有助于缩短前置作业时间,并降低该地区的汇率风险。同时,日本和韩国预计将出现对老旧公寓翻新改造的稳定需求。因此,亚太地区装饰层压板市场规模的成长将受到高成长的待开发区计划和稳定的维修週期的共同推动。

中东和非洲地区正以3.45%的复合年增长率快速成长,这主要得益于阿联酋建筑需求7.4%的成长以及沙乌地阿拉伯「2030愿景」大型企划的推进。利雅德和杜拜的大规模饭店建筑指定使用高檔层压板作为墙板和家具材料,推动了对防火防潮等级层压板的需求。沙乌地阿拉伯工业区的在地化生产计画预计将促进对层压板生产线的投资,以避免进口关税。

在北美,劳动力短缺和房屋抵押贷款成本抑制了新建房屋的需求,但专业翻新的持续需求支撑了檯面和木地板材料的需求。预製单户住宅模组采用贴合加工墙板,缓解了劳动力短缺,并为板材创造了稳定的需求。在欧洲,成本上升和更严格的排放法规迫使锯木厂重新设计树脂系统。然而,与节能维修相关的维修补贴维持了室内升级的支出,低甲醛层压板在公共竞标中也获得了规格优势。

预计南美洲将实现个位数温和成长,这主要得益于巴西住宅支出復苏以及南方共同市场关税调整缓解了跨境供应摩擦。此外,当地单板短缺也促使加工商转向进口装饰纸和树脂,从而更加重视价值而非数量。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 快速的都市化和模组化家具的蓬勃发展

- 亚太地区住宅建设激增

- 经济实惠的美学设计推动了维修需求。

- 数位印刷和套暂存器压花技术的进步

- 采用层压整合板材的预製单户住宅

- 市场限制

- 酚醛树脂和三聚氰胺树脂的价格波动

- 其他选择:人造石材、LVT地板和热压膜

- 木质基材供应链可追溯性成本

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按原料

- 塑胶树脂

- 覆盖

- 黏合剂

- 木质基材

- 其他成分

- 透过使用

- 家具

- 内阁

- 地板材料

- 墙板

- 其他用途

- 按最终用户行业划分

- 住宅

- 非住宅

- 运输

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Abet Laminati

- Aica Kogyo Co., Ltd.

- Airolam Decorative Laminates

- Archidply

- Bell Laminates

- Broadview Holding

- Durianlam

- Egger

- Greenlam Industries Limited

- Kronoplus Limited

- Laminex

- Merino Industries Limited

- Rushil Decor Limited

- Sonae Arauco

- Stylam

- The Diller Corporation

- Wilsonart LLC

第七章 市场机会与未来展望

The Decorative Laminates market is expected to grow from USD 8.35 billion in 2025 to USD 8.6 billion in 2026 and is forecast to reach USD 9.95 billion by 2031 at 2.97% CAGR over 2026-2031.

This growth reflects stable demand for cost-effective finishes in residential and commercial interior projects, even as construction cycles in developed regions cool. Rapid Asia-Pacific urbanization, sizable public housing targets in India, and China's steady infrastructure pipeline underpin global consumption of high-pressure and compact laminates. Parallel expansion in Middle East and Africa construction activity and the shift toward modular furniture formats sustain momentum, while technology-driven surface innovations allow producers to secure price premiums and defend share against substitute materials. Consolidation pressure is mounting as compliance costs for low-formaldehyde chemistry and wood-traceability rules reward vertically integrated firms with robust research and development (R&D) capabilities.

Global Decorative Laminates Market Trends and Insights

Rapid Urbanization and Modular-furniture Boom

Emerging-market cities absorb millions of new residents each year, and compact living spaces require modular furnishings that rely on lightweight panels finished with decorative laminates. India expects its urban population to swell by 416 million people by 2050, spurring demand for flat-pack furniture that cuts shipping weight by 40% compared with solid wood. Digital printing lets producers roll out hundreds of new decors in small batches, a strategy showcased by EGGER's 2024+ lineup featuring more than 300 design-texture pairings. Overlay consumption rises in tandem because premium embossed films replicate stone and oak grains while resisting scratches and fingerprints. This dual push from urban density and modular design keeps the decorative laminates market expanding independently of cyclical new-build activity.

Residential Construction Surge in Asia-Pacific

Government-led housing programs across India, Vietnam, and Thailand inject sustained spending into mid-price apartments that favor laminates over natural stone or hardwood. India alone targets USD 1 trillion in construction outlays by 2030 to close a 100 million-unit deficit. Vietnam's construction sector reached USD 95.8 billion in 2024 and continues to grow at 7% annually. Localized laminate manufacturing, such as CFL Flooring's USD 150 million Vietnam plant, shortens lead times and holds prices in price-sensitive markets. The region's policy emphasis on affordable housing locks in long-cycle demand that offsets softer Western new-build volumes.

Volatile Prices of Phenolic and Melamine Resins

Phenolic and melamine account for roughly one-fifth of laminate bill-of-materials, and 18-25% price spikes in 2024 squeezed margins as producers could not immediately pass costs to OEM furniture accounts. Because five multinational suppliers dominate specialty resins, regional fabricators lack bargaining leverage and face stock-outs during outages, delaying deliveries and eroding customer trust.

Other drivers and restraints analyzed in the detailed report include:

- Cost-effective Aesthetics Driving Renovation Demand

- Advances in Digital Printing and Emboss-in-register Tech

- Substitution by Engineered Stone, LVT and Thermofoils

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic resin retained a 40.92% share of the decorative laminates market in 2025, reflecting its indispensability for bonding decorative papers to core materials. Yet overlays are set to grow fastest at a 3.39% CAGR as digital printing requires clear, textured films that do not yellow under UV exposure. The decorative laminates market size for overlays is projected to climb steadily as anti-fingerprint and soft-touch finishes command premium spreads. Wood-traceability rules and a 0.062 mg/m3 formaldehyde ceiling under Registration, Evaluation, Authorisation and Restriction of Chemicals (REACH) are steering investment into bio-based resins and aldehyde-free systems that raise input costs but unlock Leadership in Energy and Environmental Design (LEED) points for end-users. Adhesives also benefit as low-VOC (Volatile Organic Compound) chemistries gain traction.

Second-tier inputs such as decorative foils and protective films gain strategic value because they enable differentiation without major line overhauls. Producers who master in-line coating of antimicrobial layers or scratch-repair microcapsules can charge more while meeting healthcare project specifications. Consequently, raw-material innovation is expected to tilt bargaining power toward suppliers that offer integrated chemistry packages and technical support.

The Decorative Laminates Market Report is Segmented by Raw Material (Plastic Resin, Adhesives, Wood Substrate, and Other Raw Materials), Application (Furniture, Cabinets, Flooring, and Other Applications), End-User Industry (Residential, Non-Residential, and Transportation), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 38.20% of global revenue in 2025 and will stay dominant through 2031 as India's USD 1 trillion housing drive and China's infrastructure commitments underpin volume. New Vietnamese and Thai capacity shortens regional lead times and buffers currency risk, while Japan and South Korea provide steady replacement demand in aging condominiums. Therefore, the decorative laminates market size in Asia-Pacific combines high-growth greenfield projects with stable refurbishment cycles.

The Middle East and Africa are the fastest-growing regions at a 3.45% CAGR, reflecting 7.4% expansion in the United Arab Emirates (UAE) construction and Saudi Arabia's Vision 2030 megaprojects. Large hospitality builds in Riyadh and Dubai specify premium laminates for wall panelling and case goods, boosting demand for fire-rated and moisture-resistant grades. Localization initiatives in Saudi industrial zones will likely draw investments in lamination lines to skirt import duties.

North America faces constrained new-build activity due to labor shortages and mortgage costs, yet ongoing professional remodeling supports countertop and plank-floor demand. Prefab single-family modules with pre-installed laminated walls mitigate labor deficits and spur steady panel offtake. Europe is navigating cost inflation and stringent emission rules that force mills to re-engineer resin systems. Nevertheless, renovation subsidies tied to energy-efficient retrofits keep spending on interior upgrades afloat, and low-formaldehyde laminate earns specification points in public tenders.

South America delivers mid-single-digit growth as Brazilian residential spending recovers and Mercosur tariff alignment lowers cross-border supply friction. Local veneer shortages also push converters toward imported decor papers and resin, driving value rather than volume.

- Abet Laminati

- Aica Kogyo Co., Ltd.

- Airolam Decorative Laminates

- Archidply

- Bell Laminates

- Broadview Holding

- Durianlam

- Egger

- Greenlam Industries Limited

- Kronoplus Limited

- Laminex

- Merino Industries Limited

- Rushil Decor Limited

- Sonae Arauco

- Stylam

- The Diller Corporation

- Wilsonart LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Urbanisation and Modular-furniture Boom

- 4.2.2 Residential Construction Surge in Asia-Pacific

- 4.2.3 Cost-effective Aesthetics Driving Renovation Demand

- 4.2.4 Advances in Digital Printing and Emboss-in-register Tech

- 4.2.5 Prefab Single-family Housing with Laminate-integrated Panels

- 4.3 Market Restraints

- 4.3.1 Volatile Prices of Phenolic and Melamine Resins

- 4.3.2 Substitution by Engineered Stone, LVT and Thermofoils

- 4.3.3 Supply-chain Traceability Costs for Wood Substrates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Raw Material

- 5.1.1 Plastic Resin

- 5.1.2 Overlays

- 5.1.3 Adhesives

- 5.1.4 Wood Substrate

- 5.1.5 Other Raw Materials

- 5.2 By Application

- 5.2.1 Furniture

- 5.2.2 Cabinets

- 5.2.3 Flooring

- 5.2.4 Wall Panels

- 5.2.5 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Non-residential

- 5.3.3 Transportation

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Abet Laminati

- 6.4.2 Aica Kogyo Co., Ltd.

- 6.4.3 Airolam Decorative Laminates

- 6.4.4 Archidply

- 6.4.5 Bell Laminates

- 6.4.6 Broadview Holding

- 6.4.7 Durianlam

- 6.4.8 Egger

- 6.4.9 Greenlam Industries Limited

- 6.4.10 Kronoplus Limited

- 6.4.11 Laminex

- 6.4.12 Merino Industries Limited

- 6.4.13 Rushil Decor Limited

- 6.4.14 Sonae Arauco

- 6.4.15 Stylam

- 6.4.16 The Diller Corporation

- 6.4.17 Wilsonart LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

装饰层压板市场:按产品类型、材料类型、厚度、最终用途和分销管道划分-2026年至2032年全球预测

装饰层压板市场:按产品类型、材料类型、厚度、最终用途和分销管道划分-2026年至2032年全球预测 全球装饰层压板市场规模、份额、趋势和成长分析报告(2026-2034年)

全球装饰层压板市场规模、份额、趋势和成长分析报告(2026-2034年) 日本覆膜市场规模、份额、趋势和预测:按产品类型、应用和地区划分,2026-2034年

日本覆膜市场规模、份额、趋势和预测:按产品类型、应用和地区划分,2026-2034年 2026年全球装饰配件市场报告

2026年全球装饰配件市场报告 装饰层压板市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年

装饰层压板市场-全球产业规模、份额、趋势、机会、预测:按产品、应用、地区和竞争对手划分,2021-2031年 装饰性高压层压板市场规模、份额和成长分析(按产品类型、应用、表面处理、最终用户、分销管道和地区划分)—2026-2033年行业预测

装饰性高压层压板市场规模、份额和成长分析(按产品类型、应用、表面处理、最终用户、分销管道和地区划分)—2026-2033年行业预测 装饰层压板市场规模、份额和成长分析(按产品、应用、最终用户和地区划分)-2026-2033年产业预测

装饰层压板市场规模、份额和成长分析(按产品、应用、最终用户和地区划分)-2026-2033年产业预测 高压层压板(HPL):全球市场份额和排名、总收入和需求预测(2025-2031 年)

高压层压板(HPL):全球市场份额和排名、总收入和需求预测(2025-2031 年) 全球高压层压板市场

全球高压层压板市场 高压层压板和塑胶树脂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测

高压层压板和塑胶树脂市场机会、成长动力、产业趋势分析及 2025 - 2034 年预测