|

市场调查报告书

商品编码

1934736

先进结构陶瓷:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Advanced Structural Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

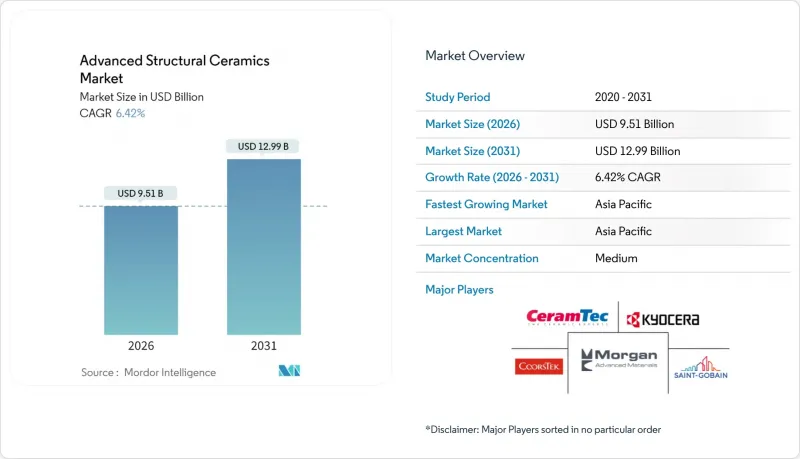

2025年先进结构陶瓷市场价值为89.4亿美元,预计2031年将达到129.9亿美元,高于2026年的95.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.42%。

这种材料的商业性优势源自于其在金属和聚合物性能不足的领域所展现出的能力,尤其是在电动动力传动系统、5G基础设施和氢能涡轮机等领域。随着航太製造商追求更节能的引擎、半导体晶圆厂采用低损耗基板以及能源公司设计更高效率、更高温度的涡轮机,市场需求正在加速成长。产业整合也在推动成长:CoorsTek以2.45亿美元收购Saint-Gobain 精密陶瓷将带来更大的规模和更低的供应风险。亚太地区凭藉其集中的半导体产业丛集和强大的汽车电气化政策,保持着生产优势。同时,积层製造技术减少了废弃物,并实现了更快的客製化,从而为特种等级材料开闢了新的收入来源。

全球先进结构陶瓷市场趋势与洞察

航太和国防领域对轻质耐高温材料的需求不断增长

喷射发动机製造商目前的目标是使进气温度超过1600°C,在此温度下,碳化硅和氮化硅仍能保持其全部机械强度。这些陶瓷材料使新型涡轮平台的燃油效率提高了15%至20%。同时,美国国防部正在资助一项高超音速飞行器项目,该项目依靠超高温复合材料来实现5马赫的飞行速度。太空飞行的需求进一步加剧了这个问题,可重复使用的运载火箭需要能够承受数百次循环而不增加质量的热防护系统。

动力传动系统电气化推动电动车温度控管陶瓷的发展

氮化铝和碳化硅基板的散热速度比聚合物填充材快 5 到 10 倍,能够更有效地散发电池和逆变器的热量。特斯拉在其 Model 3 的逆变器中使用了碳化硅,在提高效率约 9% 的同时,也降低了系统的整体品质。随着高阶电动车向 800V 架构过渡,陶瓷介面材质有助于在快速充电过程中将电池温度维持在安全范围内,从而延长电池组寿命并缩短充电次数。

与工程金属和聚合物相比,加工成本较高

全緻密碳化硅零件的成本是同类镍合金零件的三到五倍,因为其粉末纯度必须达到99.9%,而且需要钻石研磨和较长的烧结週期。由于2024年后供应受限,钇安定氧化锆原料价格上涨了17%。此外,无损检测和严格的统计控制要求将使加工成本再增加10%至15%,从而限制了其在价格敏感型电子产品和小型引擎零件中的应用。

细分市场分析

至2025年,氧化铝将占据先进结构陶瓷市场28.55%的份额,并持续保持其在耐磨环、基板和植入固定装置领域的主要应用地位。其广泛的性能和相对较低的成本确保了其持续的需求,尤其是在需要化学惰性的工业阀门和医疗设备领域。碳化硅预计将占据第二大市场份额,这主要得益于半导体和电动车牵引逆变器(需要在高开关速度下相容于宽能带隙)的需求。氧化锆8.45%的复合年增长率预示着其应用领域将转向超高温炉和涡轮机罩。在这些应用中,氧化锆的低热膨胀係数可减少应力开裂。为此,领先的製造商正在加大对喷雾干燥塔和等静压机的投资,以在保持孔径控制的同时扩大产量。

ISO 17025 测试的广泛应用,对于批次均一性和微量元素阈值的认证至关重要,也是其更广泛推广的关键。随着实验室达到这些标准,航太製造商对将新型化学物质整合到热端零件测试中也越来越有信心。同时,积层製造技术能够实现功能梯度双层层级构造,将氧化铝和锆酸盐结合在单一部件中,从而优化成本和应力分布。这些进步既保障了氧化铝的大规模生产,也提高了特种等级产品的利润率,使先进结构陶瓷市场走上了均衡成长的道路。

《先进结构陶瓷市场报告》按材料类型(氧化铝、碳化物、锆酸盐、氮化物及其他)、终端应用产业(汽车、半导体、医疗、能源、工业、航太与国防及其他)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以美元以金额为准。

区域分析

预计到2025年,亚太地区将占全球收入的53.45%,凭藉原材料粉末精炼、零件製造和最终产品组装之间的紧密合作,该地区的市场份额将以6.98%的复合年增长率持续增长。在中国,一座能够烧结温度高达2200℃的新型窑炉已投入运作;在日本,京瓷、NGK和DENKA COMPANY LIMITED之间的交叉授权合作正推动加工技术日趋成熟。

北美地区专注于航太、国防和医疗技术领域的高性能产品。 CoorsTek于2024年收购圣戈班精密陶瓷,新增了美国装甲瓦和半导体夹具的产能,并提高了国内供应的稳定性。严格的监管,包括FDA III类植入核准和AS9100品质审核,限制了新进业者的数量,同时确保了价格稳定,并使製造商能够收回研发成本。

欧洲在陶瓷基质复合材料、积层製造和氢能涡轮机领域保持主导。德国汽车供应商正在将氮化硅轴承应用于高速电驱动装置,而英国则在资助可重复使用航太引擎陶瓷材料的研发。欧盟的REACH法规和CE标誌体系确保了产品的环境相容性和统一的标籤标准。随着跨国公司将粉末製备和压制生产线集中到下一代电子产品组装基地附近,东南亚新兴地区和印度正开始抢占市场份额,但技术技能缺口仍是中期面临的挑战。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 航太和国防领域对轻质耐高温材料的需求不断增长

- 动力传动系统电气化推动电动车温度控管陶瓷的发展

- 由于5G和先进节点半导体的广泛应用,对陶瓷基板的需求增加。

- 氢气涡轮机对SiC/Si3N4热端零件的需求日益增长

- 积层製造技术可减少废弃物,并能实现复杂的陶瓷形状。

- 市场限制

- 加工成本高(与工程金属和聚合物相比)

- 脆性限制了动态应用中的设计柔软性

- 与重要原料(氧化钇、氧化锆、硼)供应相关的风险

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依材料类型

- 氧化铝

- 碳化物

- 锆酸盐

- 氮化物

- 其他的

- 按最终用户行业划分

- 车

- 半导体

- 医疗保健

- 活力

- 产业

- 航太与国防(包括航太)

- 其他的

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3M

- Advanced Ceramics Manufacturing

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek, Inc.

- Ferrotec Holdings Corporation

- KYOCERA Corporation

- MATERION CORPORATION

- Maxon

- Morgan Advanced Materials plc

- Murata Manufacturing Co., Ltd

- Nishimura Advanced Ceramics Co.,Ltd.

- Ortech Advanced Ceramics

- Paul Rauschert GmbH and Co. KG.

- Saint-Gobain

- Schunk Group

第七章 市场机会与未来展望

The Advanced Structural Ceramics Market was valued at USD 8.94 billion in 2025 and estimated to grow from USD 9.51 billion in 2026 to reach USD 12.99 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Commercial gains stem from the material's ability to operate where metals and polymers fall short, especially in electrified powertrains, 5G infrastructure, and hydrogen turbines. Demand accelerates as aerospace manufacturers seek fuel-saving engines, semiconductor fabs adopt low-loss substrates, and energy firms design hotter, leaner turbines. Consolidation also shapes growth: CoorsTek's USD 245 million purchase of Saint-Gobain Advanced Ceramics improves scale and cuts supply risk. Asia-Pacific retains a production edge thanks to deep semiconductor clusters and strong automotive electrification policies, while additive manufacturing reduces waste and speeds customization, opening fresh revenue pools for specialized grades.

Global Advanced Structural Ceramics Market Trends and Insights

Growing Demand for Lightweight, High-Temperature Materials in Aerospace and Defense

Jet-engine makers now target inlet temperatures above 1,600 °C, a range where silicon carbide and silicon nitride retain full mechanical strength. These ceramics raise fuel efficiency by 15-20% in new turbine platforms, while the U.S. Department of Defense funds hypersonic vehicle programs that rely on ultra-high-temperature composites for Mach 5 flight. Spaceflight demands compound the need, as reusable launch vehicles require thermal-protection systems that survive hundreds of cycles without mass penalties.

Electrification of Powertrains Boosting Thermal-Management Ceramics in EVs

Aluminum nitride and silicon carbide substrates dissipate battery and inverter heat at rates five to ten times higher than polymer fillers. Tesla uses silicon carbide in Model 3 inverters, improving efficiency by around 9% and trimming overall system mass. Premium electric cars now shift to 800 V architectures, and ceramic interface materials keep cells within safe temperature bands during fast charging, extending pack life and enabling shorter pit-stop times.

High Processing Cost Versus Engineered Metals and Polymers

Fully dense silicon carbide parts cost three to five times more than equivalent nickel alloys because powders require 99.9% purity, diamond grinding, and long sintering cycles. Yttria-stabilized zirconia feedstock prices rose 17% after 2024 supply constraints. Added requirements for non-destructive testing and tight statistical controls lift conversion expenses another 10-15%, discouraging use in price-sensitive electronics and small-engine components.

Other drivers and restraints analyzed in the detailed report include:

- Rising 5G and Advanced-Node Semiconductor Deployment Requiring Ceramic Substrates

- Additive Manufacturing Lowers Waste and Enables Complex Ceramic Geometries

- Brittleness Limits Design Flexibility in Dynamic Applications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alumina generated 28.55% of the advanced structural ceramics market size in 2025 and remains the workhorse for wear rings, substrates, and implant fixtures. Its broad property set and accessible cost profile ensure sustained demand, particularly in industrial valves and medical tools that require chemical inertness. Silicon carbide forms the next largest slice, lifted by semiconductor and EV traction inverters that need wide-band-gap compatibility at high switching speeds. Zirconate's 8.45% CAGR signals a pivot toward ultrahigh-temperature furnaces and turbine shrouds, where its lower thermal expansion shrinks stress cracks. In response, top producers invest in larger spray-dry towers and isostatic presses to scale volumes while preserving pore-size control.

Broader adoption also hinges on ISO 17025 testing that certifies batch homogeneity and trace element thresholds. As labs meet these standards, aerospace primes feel more confident integrating newer chemistries into hot-section tests. Meanwhile, additive manufacturing enables functionally graded bilayers that marry alumina and zirconate within a single part, optimizing cost and stress distribution. These advances protect alumina's volume base while unlocking higher margins for specialty grades, keeping the advanced structural ceramics market on a balanced growth path.

The Advanced Structural Ceramics Report is Segmented by Material Type (Alumina, Carbides, Zirconate, Nitrides, and Others), End-Use Industry (Automotive, Semiconductors, Medical, Energy, Industrial, Aerospace and Defense, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific posted 53.45% revenue in 2025 and will extend its lead with a 6.98% CAGR thanks to tight coupling between raw-powder refining, component fabrication, and end-product assembly. China commissions fresh kilns capable of 2,200 °C sintering, while Japan advances processing know-how through cross-licensing among KYOCERA, NGK, and Denka.

North America concentrates on high-performance segments tied to aerospace, defense, and medtech. CoorsTek's 2024 purchase of Saint-Gobain Advanced Ceramics folds in new U.S. capacity for armor tiles and semiconductor fixtures, improving domestic supply security. Regulatory rigor, including FDA class-III implant approval and AS9100 quality audits, limits competitive entrants yet stabilizes pricing, allowing producers to recoup research and development outlays.

Europe maintains leadership in ceramic matrix composites, additive manufacturing, and hydrogen-ready turbines. German auto suppliers embed silicon nitride bearings in high-speed e-drives, while the United Kingdom funds ceramics for reusable space engines. The bloc's REACH and CE frameworks ensure environmental compliance and consistent labeling. Emerging Southeast Asian hubs and India start to gain share as multinationals co-locate powder-prep and pressing lines near next-generation electronics assembly, but technical skill gaps remain a medium-term hurdle.

- 3M

- Advanced Ceramics Manufacturing

- Blasch Precision Ceramics, Inc.

- CeramTec GmbH

- CoorsTek, Inc.

- Ferrotec Holdings Corporation

- KYOCERA Corporation

- MATERION CORPORATION

- Maxon

- Morgan Advanced Materials plc

- Murata Manufacturing Co., Ltd

- Nishimura Advanced Ceramics Co.,Ltd.

- Ortech Advanced Ceramics

- Paul Rauschert GmbH and Co. KG.

- Saint-Gobain

- Schunk Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Lightweight, High-Temperature Materials in Aerospace and Defence

- 4.2.2 Electrification of Powertrains Boosting Thermal-Management Ceramics in EVs

- 4.2.3 Rising 5G and Advanced-Node Semiconductor Deployment Requiring Ceramic Substrates

- 4.2.4 Hydrogen Turbines Creating Need for Sic/Si3N4 Hot-Section Parts

- 4.2.5 Additive Manufacturing Lowers Waste and Enables Complex Ceramic Geometries

- 4.3 Market Restraints

- 4.3.1 High Processing Cost Versus Engineered Metals and Polymers

- 4.3.2 Brittleness Limits Design Flexibility in Dynamic Applications

- 4.3.3 Critical Raw-Material Supply Risks (Yttria, Zirconia, Boron)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material Type

- 5.1.1 Alumina

- 5.1.2 Carbides

- 5.1.3 Zirconate

- 5.1.4 Nitrides

- 5.1.5 Other

- 5.2 By End-User Industry

- 5.2.1 Automotive

- 5.2.2 Semiconductors

- 5.2.3 Medical

- 5.2.4 Energy

- 5.2.5 Industrial

- 5.2.6 Aerospace and Defense (including Space)

- 5.2.7 Others

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Ceramics Manufacturing

- 6.4.3 Blasch Precision Ceramics, Inc.

- 6.4.4 CeramTec GmbH

- 6.4.5 CoorsTek, Inc.

- 6.4.6 Ferrotec Holdings Corporation

- 6.4.7 KYOCERA Corporation

- 6.4.8 MATERION CORPORATION

- 6.4.9 Maxon

- 6.4.10 Morgan Advanced Materials plc

- 6.4.11 Murata Manufacturing Co., Ltd

- 6.4.12 Nishimura Advanced Ceramics Co.,Ltd.

- 6.4.13 Ortech Advanced Ceramics

- 6.4.14 Paul Rauschert GmbH and Co. KG.

- 6.4.15 Saint-Gobain

- 6.4.16 Schunk Group

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

特种高性能陶瓷市场:依材料、最终用户、製造流程和产品形式划分-2026-2032年全球市场预测

特种高性能陶瓷市场:依材料、最终用户、製造流程和产品形式划分-2026-2032年全球市场预测 陶瓷嵌件芯市场规模、份额和成长分析:依材质等级、製造流程、形状/复杂程度、应用领域和地区划分-产业预测,2026-2033年先进陶瓷市场:依材料、产品类型、终端用户产业及通路划分-2026-2032年全球市场预测

陶瓷嵌件芯市场规模、份额和成长分析:依材质等级、製造流程、形状/复杂程度、应用领域和地区划分-产业预测,2026-2033年先进陶瓷市场:依材料、产品类型、终端用户产业及通路划分-2026-2032年全球市场预测 全球先进陶瓷市场(至 2035 年):依材料类型、产品类别、应用类型、终端用户产业、地区、产业趋势及预测

全球先进陶瓷市场(至 2035 年):依材料类型、产品类别、应用类型、终端用户产业、地区、产业趋势及预测 特种先进陶瓷市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户及功能划分

特种先进陶瓷市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、材料类型、製程、最终用户及功能划分 2026-2034年全球特殊陶瓷市场规模、份额、趋势和成长分析报告

2026-2034年全球特殊陶瓷市场规模、份额、趋势和成长分析报告 先进陶瓷市场规模、份额和趋势分析报告:按材料、产品、应用、地区和细分市场预测(2026-2033 年)

先进陶瓷市场规模、份额和趋势分析报告:按材料、产品、应用、地区和细分市场预测(2026-2033 年) 2026年全球先进陶瓷市场报告

2026年全球先进陶瓷市场报告 全球先进陶瓷市场按材料、产品类型、终端应用产业及地区划分-预测至2030年

全球先进陶瓷市场按材料、产品类型、终端应用产业及地区划分-预测至2030年 先进陶瓷市场-全球产业规模、份额、趋势、机会和预测:按材料、类别、最终用户、地区和竞争格局划分,2021-2031年

先进陶瓷市场-全球产业规模、份额、趋势、机会和预测:按材料、类别、最终用户、地区和竞争格局划分,2021-2031年