|

市场调查报告书

商品编码

1934738

轮胎材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Tire Material - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

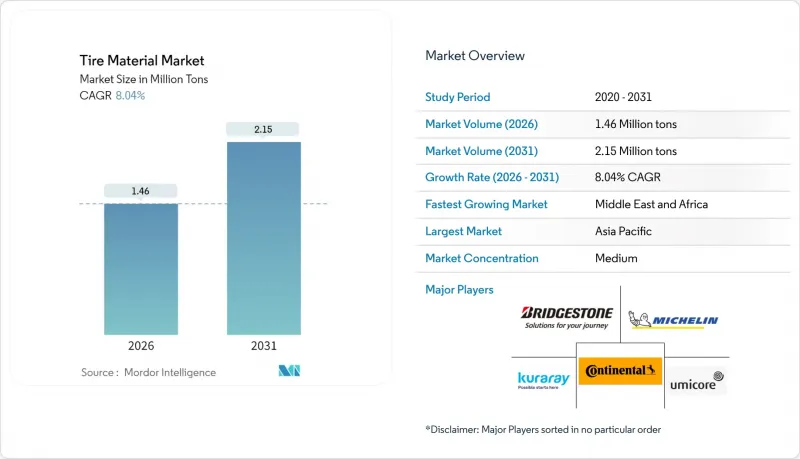

预计到 2026 年,轮胎材料市场规模将达到 146 万吨,高于 2025 年的 135 万吨,预计到 2031 年将达到 215 万吨。

预计从 2026 年到 2031 年,其复合年增长率将达到 8.04%。

电动车电池组导致车辆重量增加、欧7排放标准下更严格的轮胎磨损限制以及电商车辆更快的更换週期,正推动市场对合成弹性体和高硅含量系统的需求成长。综合轮胎製造商正在投资再生炭黑和生物基二氧化硅,这表明供应链稳定性比现货价格更为重要。亚太地区将引领全球生产,而中东地区政府主导的多元化计画预计将创造新的产能并重塑区域贸易流量。主要风险因素包括原油价格波动、PFAS法规的进展以及OEM厂商持续的库存去库存,这些因素共同导致规划週期缩短,并提升了循环原材料的价值。

全球轮胎材料市场趋势与洞察

全球电动车和混合动力汽车生产扩张

预计到2023年,电动卡车的销量将达到5.4万辆,年增35%,首次超过电动巴士。 300-500公斤的电池组会增加轮胎接地面积的负荷,使传统橡胶的使用寿命减半。轮胎製造商目前正在测试合成橡胶混合物,例如液态法尼烯橡胶,以在不增加发热量的情况下实现低滚动阻力目标。国际橡胶研究集团(IRSG)预测,到2030年,天然橡胶的需求量将达到1,690万吨,但电动车平台正使销售成长与传统弹性体的市场份额脱钩。供应商KURARAY CO. LTD.和JSR正在快速地将生物基聚合物商业化,这些聚合物的性能可与溶液法製备的S-SBR相媲美,但碳排放强度更低,这进一步凸显了轮胎材料市场向特种弹性体转变的趋势。

原始设备製造商转向使用低滚动阻力化合物

将于2026年中期生效的欧盟7排放标准将限制乘用车轮胎磨损量为7毫克/公里,轻型商用车轮胎磨损量为11毫克/公里,这将限制高炭黑配方的使用。目前,汽车製造商(OEM)指定使用硅硅烷基配方,该配方可在满足湿地抓地力性能目标的同时,将滚动阻力降低高达20%。生质乙醇的生物乙醇基ULTRASIL 9100 GR可在不影响表面积要求的前提下,减少60%的二氧化碳排放。 PPG的AGILON二氧化硅在实现类似牵引力优势的同时,也强调降低混合能耗,这在欧洲电力成本不断上涨的背景下显得尤为重要。北美卡车製造商仍然偏好能够承受80°C以上高温的富含炭黑的配方,这导致填料需求出现分化,迫使供应商维持重复的生产线。

原油和炭黑价格波动

受俄罗斯进口禁令的影响,欧洲炭黑价格在2024年6月上涨了18%,迫使轮胎製造商从土耳其和埃及采购价格更高的原料。由于FCC焦油等原料的价格与布兰特原油价格有三个月的滞后关係,如果原油价格上涨速度超过合约重新谈判的速度,利润率可能会受到压缩。由于价格不确定性导致客户延后库存补充,卡博特公司2024年第四季的增强材料销售量下降了7%。天然橡胶期货价格也波动剧烈,由于泰国和印尼的产量增加,2025年3月季减了2.1%。这迫使轮胎製造商持有60至90天的安全库存,占用了营运资金。

细分市场分析

到2025年,弹性体将占轮胎材料市场的42.88%,预计到2031年将以5.43%的复合年增长率增长,因为合成橡胶混合物将在电动车应用中取代纯天然橡胶。虽然天然橡胶因其卓越的抗撕裂强度仍是乘用车轮胎的主流,但日益严格的低滚动阻力法规正在加速向溶液型S-SBR、聚丁二烯和生物基液态法尼烯橡胶的过渡。KURARAY CO. LTD.在米其林的一项试验计画中报告称,其产品使轮胎生命週期二氧化碳排放减少了30%,滚动阻力降低了10%,这表明高端OEM厂商正在评估新型聚合物的性能。增强填充材约占轮胎总体积的三分之一,由于欧7磨损限制法规要求更高的二氧化硅含量,二氧化硅的占比正在增加。赢创和 PPG 的生质乙醇基二氧化硅产品正在缩小与炭黑的历史成本差距,这项变革正在推动轮胎材料市场供应商基础的进一步多元化。

由于REACH法规对芳烃含量的限制日益严格,轻质增塑剂正被加工馏分萃取物和妥尔油衍生物所取代。这些措施使化合物成本每公斤增加0.10至0.15美元,但有助于降低环境影响。奈米氧化锌可降低40%的重金属含量,使其更易于回收。同时,Bekar公司采用50%废钢丝,使化合物的二氧化碳排放减少了一半。随着原始设备製造商(OEM)从生产到处置的各个环节都追求永续性指标,这些渐进式的进步使材料供应商能够获得更高的溢价。

轮胎材料市场报告材料类型(弹性体、增强填料、增塑剂、化学品、金属增强材料、纤维增强材料)、车辆类型(乘用车、轻型商用车、重型卡车、巴士)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以吨为单位。

区域分析

2025年,亚太地区将占据轮胎材料市场52.05%的份额。这主要得益于中国3050万辆的轻型汽车产量以及该地区在全球天然橡胶供应中62%的份额。中国轮胎製造商如赛龙和临龙等,2024年净利成长超过70%,并在国内外扩大产能,显示对上游材料的需求持续强劲。日本的Bridgestone、住友橡胶和Yokohama Rubber在2025财年将其资本支出总合提高了10.6%,用于投资高附加价值电动车零件和海外工厂。东南亚的成本优势和丰富的天然橡胶资源吸引了新进入者,而符合欧盟标准的轮胎标籤规范也促使当地製造商采用低滚动阻力配方,从而创造了对先进填料的出口需求。

预计中东和非洲地区将成为成长最快的地区,到2031年将维持5.82%的复合年增长率,主要得益于沙乌地阿拉伯和阿联酋实施的产业多元化策略。生产力计画,可望建立自给自足的产业丛集,从而需要本地供应炭黑、二氧化硅和合成橡胶。欧洲和北美仍然是创新中心,监管压力加速了生物基二氧化硅和再生炭黑的采用,并引入了严格的可追溯性标准。这些经验最终将惠及新兴市场。南美洲的成长率为3-4%,受到货币波动和产能扩张放缓的限制。然而,巴西拥有7,000万辆汽车的庞大售后市场,对特种填料的进口需求仍然强劲。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球电动车和混合动力汽车产量扩大

- 原始设备製造商转向使用低滚动阻力化合物

- 电子商务活动的激增以及由此导致的轮胎更换里程增加

- 东南亚的再工业化正在催生新的本地轮胎工厂。

- 透过室温回收技术实现原料的再生利用

- 市场限制

- 原油和炭黑价格波动

- 2024-2025年OEM库存削减

- 欧盟即将实施的 PFAS 禁令将限制含氟添加剂的使用

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依材料类型

- 弹性体

- 天然橡胶

- 合成橡胶

- 增强填料

- 炭黑

- 二氧化硅

- 增塑剂

- 石蜡油

- 环烷油

- 芳香油

- 化学品

- 硫

- 氧化锌

- 硬脂酸

- 金属加固

- 钢丝

- 轮胎边缘线

- 纤维增强

- 尼龙

- 聚酯纤维

- 其他的

- 弹性体

- 按车辆类型

- 搭乘用车

- 轻型商用车(LCV)

- 大型卡车

- 公车

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 土耳其

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Bekaert

- Birla Carbon

- Bridgestone Corporation

- Cabot Corporation

- Continental AG

- Evonik

- Exxon Mobil Corporation

- JSR Corporation

- Kuraray Co., Ltd.

- LANXESS

- Linglong Tire

- Michelin

- Orion

- Sailun Group Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Umicore

- Zhongce Rubber Group Co., Ltd.

第七章 市场机会与未来展望

The tire material market size in 2026 is estimated at 1.46 million tons, growing from 2025 value of 1.35 million tons with 2031 projections showing 2.15 million tons, growing at 8.04% CAGR over 2026-2031.

Higher vehicle weight from electric-vehicle battery packs, tighter Euro 7 tire-abrasion limits, and accelerated replacement cycles in e-commerce fleets are shifting demand toward synthetic elastomers and high-silica filler systems. Integrated tire makers are investing in recovered carbon black and bio-based silica, signaling that supply-chain security now outweighs spot-price considerations. The Asia-Pacific region dominates the global volume, while sovereign diversification programs in the Middle East are unlocking greenfield capacity that will reshape regional trade flows. Headline risks center on crude oil volatility, pending PFAS restrictions, and lingering OEM inventory destocking that together shorten planning horizons and elevate the value of circular feedstocks.

Global Tire Material Market Trends and Insights

Global Ramp-Up of EV and Hybrid Vehicle Production

Electric trucks sold 54,000 units in 2023, 35% higher than in 2022, marking the first time the category outpaced electric buses. Battery packs weighing 300-500 kg place additional load on tire contact patches, cutting traditional compound life in half. Tire makers now test synthetic blends, such as liquid farnesene rubber, to meet lower rolling-resistance targets without increasing heat buildup. The International Rubber Study Group expects natural-rubber demand to hit 16.9 million tons by 2030, yet EV platforms are decoupling volume growth from historical elastomer ratios. Suppliers Kuraray and JSR are racing to commercialize bio-based polymers that match the performance of solution S-SBR at a lower carbon intensity, reinforcing why the tire material market is shifting toward specialty elastomers.

OEM Shift Toward Low Rolling Resistance Compounds

Euro 7 rules, effective mid-2026, cap tire abrasion at 7 mg/km for passenger cars and 11 mg/km for light commercial vehicles, which limits the use of high-carbon-black compounds OEMs now specify silica-silane systems that cut rolling resistance by up to 20% while meeting wet-grip targets. Evonik's ULTRASIL 9100 GR, produced from bio-ethanol, delivers a 60% CO2 reduction without compromising surface-area requirements. PPG's AGILON silica attains similar traction benefits but emphasizes lower mixing energy, a priority as European electricity costs rise. North American truck OEMs still prefer carbon-black-rich recipes that resist heat above 80 °C, fragmenting filler demand and obliging suppliers to maintain dual production lines.

Volatile Crude Oil and Carbon-Black Pricing

European carbon-black prices rose 18% in June 2024, following the ban on imports from Russia, which forced tire makers to source higher-priced material from Turkey and Egypt. Feedstocks, such as FCC tar, track Brent crude with a three-month lag, resulting in margin compression when oil rallies outpace contract renegotiations. Cabot's Q4 2024 reinforcement volumes fell 7% as customers delayed restocking amid price uncertainty. Natural-rubber futures also remain volatile, dropping 2.1% week-over-week in March 2025 as Thai and Indonesian output expanded, prompting tire makers to hold 60-90 days of safety stock, which ties up working capital.

Other drivers and restraints analyzed in the detailed report include:

- Surge in E-Commerce Activities and Replacement Tire Miles

- Re-Industrialization of Southeast Asia Creating New Local Tire Plants

- Looming EU PFAS Ban Limiting Fluorinated Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elastomers accounted for 42.88% of the tire material market size in 2025 and will expand at a 5.43% CAGR through 2031 as synthetic blends displace pure natural rubber in EV applications. Natural rubber still dominates passenger tires due to its superior tear strength, yet low-rolling-resistance mandates are accelerating the switch to solution S-SBR, polybutadiene, and bio-based liquid farnesene rubber. Kuraray reports lifecycle CO2 cuts of 30% and a 10% reduction in rolling resistance in Michelin pilot programs, illustrating how premium OEM specifications reward novel polymers. Reinforcing fillers, which occupy approximately one-third of the total compound volume, are witnessing a rise in silica's share as Euro 7 abrasion limits force higher-silica tread recipes. Bio-ethanol silica grades from Evonik and PPG are closing the historical cost gap with carbon black, a shift that further diversifies supplier bases within the tire material market.

Lightweight plasticizers face stricter REACH limits on aromatic content, prompting a shift toward treated distillate extracts and tall-oil derivatives, even though they add USD 0.10-0.15 per kilogram to compound cost. Nano-zinc-oxide grades cut heavy-metal loading by 40%, easing recycling, while Bekaert steel cord with 50% scrap content lowers compound CO2 by half. These incremental advances position material suppliers for premium pricing as OEMs chase cradle-to-grave sustainability metrics.

The Tire Material Market Report is Segmented by Material Type (Elastomers, Reinforcing Fillers, Plasticizers, Chemicals, Metal Reinforcements, and Textile Reinforcements), Vehicle Type (Passenger Cars, Light Commercial Vehicles, Heavy Trucks, Buses), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific held 52.05% of the tire material market share in 2025, underpinned by China's 30.5-million-unit light-vehicle output and the region's 62% share of global natural-rubber supply. Chinese tire makers, such as Sailun and Linglong, reported net profit growth exceeding 70% in 2024 and are expanding capacity both domestically and internationally, indicating sustained demand for upstream materials. Japan's Bridgestone, Sumitomo, and Yokohama raised their combined capital expenditure by 10.6% for FY 2025, directing funds toward high-value EV components and overseas plants. Southeast Asia's cost advantage and access to raw rubber encourage new entrants, while EU-aligned tire labeling standards prompt local producers to adopt low-rolling-resistance recipes, creating export-ready demand for advanced fillers.

The Middle East and Africa region is the fastest-growing geography, registering a 5.82% CAGR through 2031, as Saudi Arabia and the UAE deploy industrial diversification strategies. Projects such as the USD 550 million Pirelli-PIF plant and Egypt's USD 1.8 billion capacity pipeline promise to build a self-sufficient cluster that will need local carbon black, silica, and synthetic rubber supply. Europe and North America remain innovation hubs because regulatory pressure accelerates the adoption of bio-based silica, recovered carbon black, and stringent traceability standards, lessons that later cascade to emerging markets. South America's growth is at 3-4%, tempered by currency volatility and slower capacity additions; however, Brazil's 70 million vehicle parc offers a resilient aftermarket base that still imports specialty fillers.

- Bekaert

- Birla Carbon

- Bridgestone Corporation

- Cabot Corporation

- Continental AG

- Evonik

- Exxon Mobil Corporation

- JSR Corporation

- Kuraray Co., Ltd.

- LANXESS

- Linglong Tire

- Michelin

- Orion

- Sailun Group Co., Ltd.

- Sumitomo Rubber Industries, Ltd.

- Umicore

- Zhongce Rubber Group Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global ramp-up of EV and hybrid vehicle production

- 4.2.2 OEM shift toward low-rolling-resistance compounds

- 4.2.3 Surge in e-commerce activities and the corresponding rise in replacement tire miles

- 4.2.4 Re-industrialisation of Southeast Asia creating new local tire plants

- 4.2.5 Cold-in-place recycling enabling circular feedstocks

- 4.3 Market Restraints

- 4.3.1 Volatile crude-oil and carbon-black pricing

- 4.3.2 OEM inventory destocking in 2024-25

- 4.3.3 Looming EU PFAS ban limiting fluorinated additives

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Material Type

- 5.1.1 Elastomers

- 5.1.1.1 Natural Rubber

- 5.1.1.2 Synthetic Rubber

- 5.1.2 Reinforcing Fillers

- 5.1.2.1 Carbon Black

- 5.1.2.2 Silica

- 5.1.3 Plasticizers

- 5.1.3.1 Paraffinic Oil

- 5.1.3.2 Naphthenic Oil

- 5.1.3.3 Aromatic Oil

- 5.1.4 Chemicals

- 5.1.4.1 Sulfur

- 5.1.4.2 Zinc Oxide

- 5.1.4.3 Stearic Acid

- 5.1.5 Metal Reinforcements

- 5.1.5.1 Steel Cord

- 5.1.5.2 Bead Wire

- 5.1.6 Textile Reinforcements

- 5.1.6.1 Nylon

- 5.1.6.2 Polyester

- 5.1.6.3 Others

- 5.1.1 Elastomers

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles (LCV)

- 5.2.3 Heavy Trucks

- 5.2.4 Buses

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Turkey

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bekaert

- 6.4.2 Birla Carbon

- 6.4.3 Bridgestone Corporation

- 6.4.4 Cabot Corporation

- 6.4.5 Continental AG

- 6.4.6 Evonik

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 JSR Corporation

- 6.4.9 Kuraray Co., Ltd.

- 6.4.10 LANXESS

- 6.4.11 Linglong Tire

- 6.4.12 Michelin

- 6.4.13 Orion

- 6.4.14 Sailun Group Co., Ltd.

- 6.4.15 Sumitomo Rubber Industries, Ltd.

- 6.4.16 Umicore

- 6.4.17 Zhongce Rubber Group Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

永续轮胎材料市场:按材料、车辆类型、轮胎类型、分销管道和最终用途行业划分-2026-2032年全球市场预测

永续轮胎材料市场:按材料、车辆类型、轮胎类型、分销管道和最终用途行业划分-2026-2032年全球市场预测 轮胎增强材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

轮胎增强材料:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球轮胎材料市场规模、份额、趋势和成长分析报告(2026-2034年)

全球轮胎材料市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球轮胎材料市场报告永续轮胎市场:按技术、结构、应用、车辆类型和分销管道划分,全球预测(2026-2032年)

2026年全球轮胎材料市场报告永续轮胎市场:按技术、结构、应用、车辆类型和分销管道划分,全球预测(2026-2032年) 轮胎材料市场规模、份额和成长分析(按车辆类型、类型、材料类型、轮胎类型和地区划分)-2026-2033年产业预测

轮胎材料市场规模、份额和成长分析(按车辆类型、类型、材料类型、轮胎类型和地区划分)-2026-2033年产业预测 永续轮胎材料市场-全球产业规模、份额、趋势、机会和预测,依材料、车辆类型、地区和竞争格局划分,2020-2030年预测轮胎材料市场-全球产业规模、份额、趋势、机会及预测,依类型、最终用户类型、地区及竞争格局划分,2020-2030年预测

永续轮胎材料市场-全球产业规模、份额、趋势、机会和预测,依材料、车辆类型、地区和竞争格局划分,2020-2030年预测轮胎材料市场-全球产业规模、份额、趋势、机会及预测,依类型、最终用户类型、地区及竞争格局划分,2020-2030年预测 全球轮胎原料市场未来展望(至2030年)

全球轮胎原料市场未来展望(至2030年) 永续轮胎的全球市场:按材料类型、按推进类型、按结构、按车辆类型、按地区 - 预测(至 2029 年)

永续轮胎的全球市场:按材料类型、按推进类型、按结构、按车辆类型、按地区 - 预测(至 2029 年)