|

市场调查报告书

商品编码

1934750

消毒剂和清洁剂:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Antiseptics And Disinfectants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

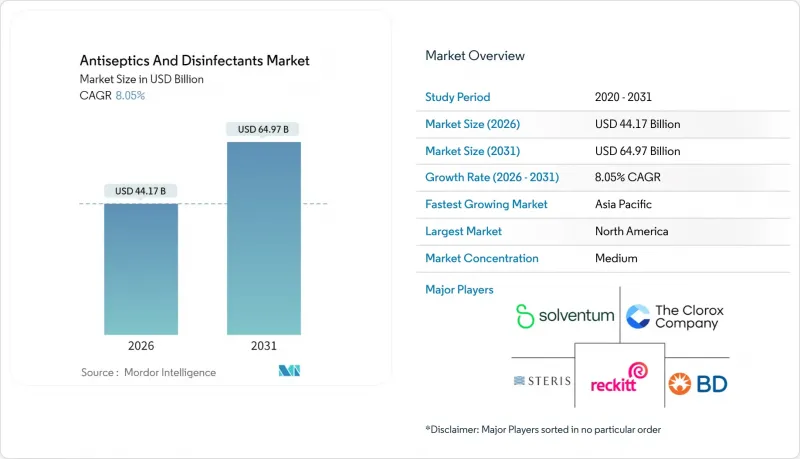

2025年消毒剂和清洁剂市值为408.8亿美元,预计2031年将达到649.7亿美元,高于2026年的441.7亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 8.05%。

目前的支出模式显示,感染控制预算与医院因医疗相关感染(HAI)而遭受的经济处罚之间有明显的关联。预防性技术的资金投入成长速度超过了治疗性药物,反映出医院采购部门在策略上优先考虑预防而非治疗。大量高频接触表面和需要每天多次消毒的可重复使用医疗设备的普及,进一步扩大了这个市场机会。稳定的市场扩张表明,由于感染控制是医疗机构的强制性支出项目,因此需求在很大程度上不受经济放缓的影响。因此,即使消费者市场的需求不断增长,製造商仍在优先考虑医院级产品的产能。

监管审查的加强非但没有抑制需求,反而加速了需求成长,因为医疗服务提供者更倾向于选择符合法规、未来处罚风险较低的下一代化学品。美国环保署 (EPA) 于 2024 年 3 月最终确定的环氧乙烷灭菌器排放90% 的要求就是一个典型的例子,这促使买家转向低残留酶基混合物和气化过氧化氢系统。围绕这些替代技术构建的智慧财产权组合在併购中获得了积极评价,反映出企业正在策略性地转向更安全、更环保的选择。投资者还指出,医院基础设施的使用寿命较长,确保了相容配方的持续供应,这意味着如果经济逆风有限,实际成长可能超过已公布的 8% 复合年增长率。

全球消毒剂和清洁剂市场趋势及洞察

本院获得性感染呈上升趋势

医院感染(HAI)持续上升,欧洲医疗机构每年报告的病例高达890万例,给公立和私立医院的预算都带来了压力。由于每例感染都会对医院造成收入损失,因此预防工作被列为优先事项,这也推动了消毒剂和清洁剂市场的成长。拥有先进监测系统的医疗机构往往更早采用高效消毒剂,因为数据透明化使经营团队能够清楚地了解预防投资的回报率。

手术数量增加

手术量持续成长,尤其是在门诊手术中心(ASC),其感染率仅为0.1%(相较之下,医院的感染率为1%)。这项成功促使医疗机构更加依赖专业的消毒通讯协定,以实现手术室的快速週转。供应商若能针对门诊手术中心的需求客製化消毒剂包装规格和作用时间,便可在不与现有医院产品线直接竞争的情况下,赢得消毒剂和清洁剂市场份额。

严格的监管要求

美国环保署 (EPA) 已强制要求将环氧乙烷灭菌设备的排放减少 90%,这将影响美国约一半的医疗设备灭菌流程。合规成本正促使医院考虑低温替代方法。新兴研究表明,采用这些替代方法的机构更有可能统一使用同一供应商提供的兼容表面消毒剂,从而加剧对供应商的依赖。

细分市场分析

根据市场规模估算,到2025年,季铵化合物(QACs)将占消毒剂和清洁剂市场的27.45%,而酵素製剂预计将在2031年之前以8.75%的复合年增长率(CAGR)实现最快成长。儘管医院重视QACs的残留效力,但日益严格的监管审查正推动采购转向酵素製剂,因为酵素製剂能够降解生物膜且不留有毒残留物。 QAC和酵素製剂的组合配方有望成为兼顾功效和环保目标的过渡性产品线。

由于成本低廉且起效迅速,氯化合物和醇醛混合物仍被广泛应用于高频擦拭巾消毒。而双胍类药物(如氯己定)因其持久的消毒效果,仍是术前皮肤消毒的首选。这意味着,即使整体市场趋势转向更环保的解决方案,与临床通讯协定相关的特定化学物质仍将保持其重要性。

到2025年,液体消毒剂将占消毒剂和清洁剂市场规模的51.10%,而擦拭巾预计年复合成长率将达到9.05%,因为医院需要剂量可控的一次性产品。此外,擦拭巾有助于库存管理,简化预算,因为其单位销售与患者数量密切相关。

虽然喷雾剂在大面积紧急消毒方面仍然很受欢迎,但凝胶和泡沫剂在慢性伤口诊所越来越受欢迎,因为它们兼具消毒和癒合功能。其原理是,泡棉包装可以精确地应用于垂直和不规则表面,从而减少浪费并提升顾客的价值感知。

区域分析

预计到2025年,北美将继续保持其在消毒剂和清洁剂市场的领先地位,占据37.60%的市场份额。这主要得益于医疗相关感染(HAI)的高额罚款以及美国环保署(EPA)针对环氧乙烷排放的新规。 EPA和FDA之间的监管协调缩短了技术升级的决策週期,并加快了产品更新换代的速度。在加州等感染率最高的州,医院往往反应更快,因为公共报告要求给经营团队带来了压力。

亚太地区以9.12%的复合年增长率呈现最快成长势头,主要得益于大规模的医院建设和对洗手卫生的重视。儘管本地产量不断提高,但高端进口产品在加护病房仍然占据主导地位,这表明在品质认知方面存在差距。当国际品牌进入区域性城市时,它们可能会在本地竞争对手提升配方标准之前抢占市场份额。

欧洲正经历稳定成长,主要得益于严格的环境毒性标准以及老年人口不断增长、感染疾病风险更高的现状。采购政策优先考虑挥发性有机化合物(VOC)含量低的产品,并鼓励製造商对传统产品进行配方改良。欧盟的环境法规往往成为事实上的全球标准,这使得率先采用这些法规的企业在出口到其他受监管市场时更具优势。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 本院获得性感染呈上升趋势

- 手术数量增加

- 提高卫生管理和感染控制意识

- 透过加强内视镜再处理强制性标准,促进高水准消毒剂的引入。

- 医疗领域的成长和住院人数的增加

- 创新的生产方法与技术

- 市场限制

- 严格的监管要求

- 先进医疗设备的灭菌消毒剂面临的挑战

- 挥发性季铵化合物原料成本

- 过渡到使用一次性设备/减少可重复使用设备的消毒次数

- 供应链分析

- 监管和技术趋势

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 季铵化合物

- 氯化合物

- 醇和醛类化合物

- 双胍类和碘衍生物

- 酵素

- 酚类和其他

- 配方

- 液体

- 喷雾剂和气雾剂

- 消毒纸巾

- 凝胶泡沫

- 透过使用

- 表面消毒剂

- 医疗设备消毒剂

- 酵素性清洁剂

- 皮肤和伤口消毒剂

- 最终用户

- 医院和诊所

- 门诊/日间手术中心

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东

- GCC

- 南非

- 其他中东地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度

- 市占率分析

- 公司简介

- Solventum Corporation

- STERIS plc

- Ecolab Inc.

- Reckitt Benckiser Group plc

- The Clorox Company

- Procter & Gamble Co.

- SC Johnson Professional

- Johnson & Johnson

- Cardinal Health Inc.

- Schulke & Mayr GmbH

- Metrex Research, LLC

- GSK plc

- Molnlycke Health Care AB

- Pal International Ltd.

- Diversey Holdings, Ltd.

- GOJO Industries, Inc.

- Zep Inc.

- Kimberly-Clark Corporation

第七章 市场机会与未来展望

The Antiseptics and Disinfectants market was valued at USD 40.88 billion in 2025 and estimated to grow from USD 44.17 billion in 2026 to reach USD 64.97 billion by 2031, at a CAGR of 8.05% during the forecast period (2026-2031).

Current spending patterns reveal a clear correlation between infection-control budgets and the financial penalties hospitals incur for healthcare-associated infections (HAIs). Capital allocations for preventive technologies are rising faster than for therapeutic drugs, reflecting a strategic preference for prevention over cure in hospital purchasing departments. The scale of the opportunity is reinforced by the large installed base of high-touch surfaces and reusable medical devices that require disinfection multiple times daily. Consistent market expansion suggests that demand is broadly resilient to economic slowdowns, as infection control is a non-discretionary purchase for healthcare providers. Manufacturers are therefore prioritizing production capacity for hospital-grade products, even as demand from consumer segments grows.

Regulatory scrutiny is accelerating rather than dampening demand, because providers prefer compliant, next-generation chemistries that are less likely to trigger future penalties. The United States Environmental Protection Agency's 90 % emission reduction mandate for ethylene oxide sterilizers, finalised in March 2024 is a prime example: it has pushed purchasers toward low-residue enzymatic blends and vaporised hydrogen peroxide systems . Intellectual property portfolios built around these alternatives are commanding premium valuations in mergers and acquisitions, reflecting a strategic shift toward safer, greener options. Investors also note the long useful life of hospital infrastructure, which locks in repeat sales of compatible formulations, suggesting that actual growth may exceed the headline 8 % CAGR if economic headwinds remain modest.

Global Antiseptics And Disinfectants Market Trends and Insights

Growing Incidences of Hospital Acquired Infections

HAIs continue to climb, with European facilities reporting 8.9 million annual cases, placing budgetary strain on public and private hospitals alike . Hospitals face lost revenue per infection episode, so prevention budgets are receiving priority, which in turn sustains growth in the Antiseptics and Disinfectants market. Facilities with advanced surveillance programs tend to adopt high-performance disinfectants early because data transparency makes the ROI on prevention visible to management.

Increasing Number of Surgical Procedures

Surgical volumes are rising, particularly in ambulatory surgery centers (ASCs) where infection rates sit at just 0.1 % compared with 1 % in hospitals. This success raises institutional confidence in specialized disinfectant protocols designed for rapid room turnover. Suppliers that tailor packaging sizes and contact times for ambulatory surgery centers can gain Antiseptics and Disinfectants market share without direct head-to-head competition with incumbent hospital product lines.

Stringent Regulatory Requirements

The Environmental Protection Agency (EPA) has mandated 90% emission cuts for ethylene oxide sterilizers, affecting roughly half of all device sterilization in the United States. Compliance costs encourage hospitals to trial on-site low-temperature alternatives. A fresh inference is that facilities adopting such alternatives will standardize on compatible surface disinfectants from the same suppliers, reinforcing vendor stickiness.

Other drivers and restraints analyzed in the detailed report include:

- Rising Awareness of Hygiene and Infection Control

- Growth in Healthcare Sector and Hospital Admissions

- Issues Related to Sterilization and Disinfectants of Advanced Medical Instruments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Market size estimates show Quaternary Ammonium Compounds (QACs) hold 27.45 % Antiseptics and Disinfectants market share in 2025, while enzymes record the fastest CAGR of 8.75 % through 2031. Hospitals value QACs for residual activity, but growing regulatory attention is nudging procurement teams toward enzymatic blends that degrade biofilms without leaving toxic residues. A clear inference is that formulators combining QACs with enzymes could offer a transitional product line that meets both efficacy and environmental goals.

Chlorine compounds and alcohol-aldehyde mixes continue serving high-frequency wipe-down tasks thanks to low cost and rapid action. Biguanides such as chlorhexidine remain favored for pre-operative skin prep owing to extended bactericidal persistence. The inference here is that niche chemicals sustain relevance when tied to clinical protocols, even if overall market momentum shifts toward greener solutions.

Liquids account for 51.10 % of Antiseptics and Disinfectants market size in 2025, but wipes display a 9.05% forecast CAGR as hospitals seek dose-controlled, single-use formats. The fresh inference is that wipes also aid inventory control because unit counts align closely with patient volumes, simplifying budgeting.

Sprays remain popular for emergency decontamination of wide areas, while gels and foams gain favor in chronic-wound clinics for their combined disinfectant and healing attributes. An inference is that foam packaging allows precise application on vertical or irregular surfaces, reducing wastage and boosting perceived value.

The Antiseptics and Disinfectants Market Report is Segmented by Product Type (Quaternary Ammonium Compounds, Chlorine Compounds, and More), Formulation (Liquid, Wipes, and More), Application (Enzymatic Cleaners, Medical Device Disinfectants, More), End User (Hospitals & Clinics, Ambulatory & Day-Surgery Centers, and Others), and Geography (North America and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America leads with 37.60% Antiseptics and Disinfectants market share in 2025, fueled by high HAI penalties and new EPA rules curbing ethylene oxide emissions. Regulatory alignment between the EPA and FDA is compressing decision cycles for technology upgrades, accelerating product replacement rates. Hospitals in states with the highest infection counts, such as California, are often the first to move because public reporting pressures executive teams.

The Asia-Pacific region shows the fastest growth rate of 9.12% CAGR, driven by large-scale hospital construction and a cultural emphasis on hand hygiene. Local production is increasing, yet premium imports still dominate critical care units, indicating gaps in quality perception. Global brands entering tier-2 cities may gain share before local competitors improve formulation standards.

Europe maintains steady growth underpinned by stringent eco-toxicity standards and a large aging population susceptible to infections. Procurement policies favor products with reduced volatile organic compounds, incentivizing manufacturers to reformulate legacy lines. EU environmental rules often serve as de facto global benchmarks, and early compliance can provide export advantages in other regulated markets.

- Solventum Corporation

- STERIS

- Ecolab

- Reckitt Benckiser Group

- The Clorox Company

- Procter & Gamble

- SC Johnson Professional

- Johnson & Johnson

- Cardinal Health

- Schulke & Mayr GmbH

- Metrex Research, LLC

- GlaxoSmithKline

- Molnlycke Health Care

- Pal International Ltd.

- Diversey Holdings, Ltd.

- GOJO Industries, Inc.

- Zep Inc.

- Kimberly-Clark Worldwide

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Incidences Of Hospital Acquired Infections

- 4.2.2 Increasing Number Of Surgical Procedures

- 4.2.3 Rising Awareness Of Hygeiene And Infection Control

- 4.2.4 Mandatory Endoscope Reprocessing Standards Strengthening High-Level Disinfectant Uptake

- 4.2.5 Growth In The Healthcare Sector And Hospital Admissions

- 4.2.6 Innovative Production Formulations And Technologies

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Requirements

- 4.3.2 Issues Related To The Sterilization And Disinfectants Of Advanced Medical Instruments

- 4.3.3 Volatile Quaternary Ammonium Compound Feedstock Costs

- 4.3.4 Shift To Single-Use Instruments Shrinking Reusable Disinfection Volumes

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Quaternary Ammonium Compounds

- 5.1.2 Chlorine Compounds

- 5.1.3 Alcohols & Aldehydes

- 5.1.4 Biguanides & Iodine Derivatives

- 5.1.5 Enzymes

- 5.1.6 Phenolic & Others

- 5.2 By Formulation

- 5.2.1 Liquids

- 5.2.2 Sprays & Aerosols

- 5.2.3 Wipes

- 5.2.4 Gels & Foams

- 5.3 By Application

- 5.3.1 Surface Disinfectants

- 5.3.2 Medical Device Disinfectants

- 5.3.3 Enzymatic Cleaners

- 5.3.4 Skin & Wound Antiseptics

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory & Day-Surgery Centers

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Solventum Corporation

- 6.3.2 STERIS plc

- 6.3.3 Ecolab Inc.

- 6.3.4 Reckitt Benckiser Group plc

- 6.3.5 The Clorox Company

- 6.3.6 Procter & Gamble Co.

- 6.3.7 SC Johnson Professional

- 6.3.8 Johnson & Johnson

- 6.3.9 Cardinal Health Inc.

- 6.3.10 Schulke & Mayr GmbH

- 6.3.11 Metrex Research, LLC

- 6.3.12 GSK plc

- 6.3.13 Molnlycke Health Care AB

- 6.3.14 Pal International Ltd.

- 6.3.15 Diversey Holdings, Ltd.

- 6.3.16 GOJO Industries, Inc.

- 6.3.17 Zep Inc.

- 6.3.18 Kimberly-Clark Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment

高级消毒服务市场分析及预测(至2035年):按类型、产品、服务、技术、应用、设备、流程、最终用户、设施和解决方案划分

高级消毒服务市场分析及预测(至2035年):按类型、产品、服务、技术、应用、设备、流程、最终用户、设施和解决方案划分 2026年全球抗菌食品消毒剂市场报告

2026年全球抗菌食品消毒剂市场报告 高级消毒服务市场-2026-2031年预测

高级消毒服务市场-2026-2031年预测 食品消毒剂市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、应用、最终用户、地区和竞争格局划分,2021-2031年)消毒剂和清洁剂市场-2026-2031年预测

食品消毒剂市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、应用、最终用户、地区和竞争格局划分,2021-2031年)消毒剂和清洁剂市场-2026-2031年预测 消毒剂和清洁剂市场规模、份额和成长分析(按类型、产品、销售管道、应用和地区划分)—产业预测(2026-2033 年)

消毒剂和清洁剂市场规模、份额和成长分析(按类型、产品、销售管道、应用和地区划分)—产业预测(2026-2033 年) Bronopol市场按应用、最终用途行业和剂型划分 - 全球预测 2025-2032抗菌食品消毒剂市场按产品类型、活性成分、应用、最终用户和分销管道划分-2025-2032年全球预测防腐剂市场按产品类型、剂型、应用、最终用户、分销管道和包装类型划分-2025-2032年全球预测防腐剂和消毒剂市场按产品类型、剂型、作用领域、应用、最终用户和销售管道划分-2025-2030 年全球预测

Bronopol市场按应用、最终用途行业和剂型划分 - 全球预测 2025-2032抗菌食品消毒剂市场按产品类型、活性成分、应用、最终用户和分销管道划分-2025-2032年全球预测防腐剂市场按产品类型、剂型、应用、最终用户、分销管道和包装类型划分-2025-2032年全球预测防腐剂和消毒剂市场按产品类型、剂型、作用领域、应用、最终用户和销售管道划分-2025-2030 年全球预测