|

市场调查报告书

商品编码

1934765

亚太地区白水泥:市占率分析、产业趋势与统计、成长预测(2026-2031年)Asia-Pacific White Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

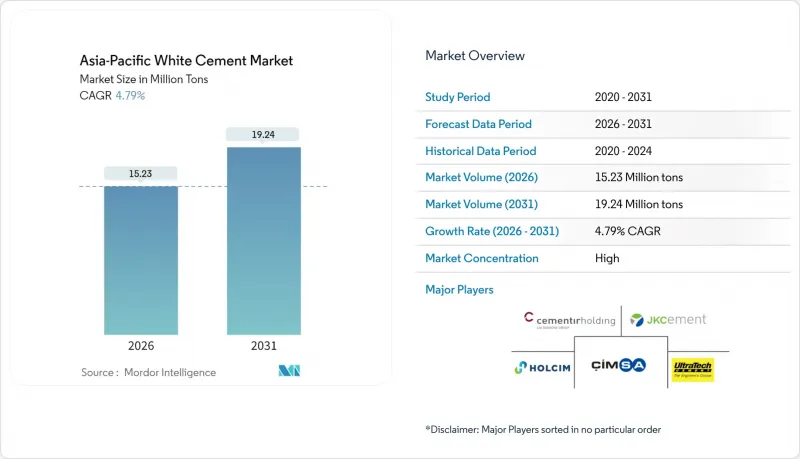

亚太地区白水泥市场预计将从 2025 年的 1,453 万吨成长到 2026 年的 1,523 万吨,预计到 2031 年将达到 1,924 万吨,2026 年至 2031 年的复合年增长率为 4.79%。

稳健的基础设施发展规划、不断增长的可支配收入以及日益严格的能源效率法规正在推动市场需求,房地产开发商寻求兼具美观性和低热负荷的材料。高端策略使生产商能够在燃料成本上涨的情况下保持高利润率,而印度和中国製造商之间日益加剧的整合正在实现规模经济并缓解价格波动。持续的都市区化进程使住宅保持在高位,而机场、地铁和综合用途开发项目的期货合约签署预示着商业机会的不断扩大。製造商也在积极利用永续性认证。白水泥的高反射率符合冷屋顶法规要求,并有助于实现 LEED 和绿色建筑标誌认证目标,从而持续吸引建筑师和计划业主的需求。

亚太地区白水泥市场趋势及洞察

建筑业需求不断成长

菲律宾等市场的基础设施投资占GDP的比重超过5%,而印度的「总理住房计画」(Pradhan Mantri Awas Yojana)已批准兴建2,564万套农村住宅,从而提振了对高品质接合材料的需求。泰国东部经济走廊持续吸引物流设施和半导体工厂,预计2026年将维持3-4%的年建设成长率。水泥价格上涨尤其令生产商受益,因为白水泥的价格比灰水泥高出15-20%。

预製混凝土生产规模扩大

工厂化生产的模组化建筑满足了开发商对更快施工速度和减少现场劳动力的需求。日本太平洋水泥株式会社在宿雾运作了一条价值2.66亿美元的生产线,使其在菲律宾的产能提高了50%,尤其适用于那些依赖白水泥颜色稳定性的建筑幕墙和板材产品。 Ultratech的「Very Amazing Concrete」产品线代表了印度类似的转型,它将耐用添加剂与光亮饰面相结合,打造出建筑师指定的用于幕墙和景观家具的产品。 Semcor公司试生产了一种烧结黏土混合料,生产了3000吨低碳预製构件,这项製程创新体现了环境目标与生产力目标的融合。

高成本生产

白水泥熟料的烧成温度接近摄氏1500度,不仅增加了燃料成本,也加剧了窑内耐火材料的磨损。印尼水泥厂目前的产运转率仅54.2%,固定成本分摊到较小的产量上,导致利润率下降。同时,世界水泥协会警告称,碳排放税可能导致每吨水泥成本增加4至6美元,迫使小型生产商升级生产线,否则将市场份额拱手让给那些已经开始转向替代燃料的大型综合企业。

细分市场分析

预计到2025年,I型水泥将占亚太地区白水泥市场份额的51.92%,并在2031年之前以5.05%的复合年增长率成长。需求成长的驱动因素是其与主流外加剂的兼容性以及标准化的抗压强度等级,这简化了塔楼、桥樑和地铁计划工程师的规范制定工作。预计到2024年,该细分市场将占亚太地区白水泥市场规模的一半以上,这反映了其作为建筑预製件、水磨石和游泳池等工程中默认接合材料的地位。

I型水泥在产能部署上具有优势。窑炉只需进行少量化学成分调整即可在生产灰水泥和白水泥之间切换,这使得像UltraTech这样的公司能够满足季节性需求高峰,避免库存积压。多样化的终端用途增强了与优先考虑快速周转率库存的经销商的议价能力。随着预製构件製造商扩大对日本和澳洲的出口,基于ASTM C150标准的统一规范已将I型水泥确立为标竿产品,并透过网路效应进一步巩固了其优势。

亚太地区白水泥市场报告按类型(I型、III型、其他等级)、应用(商业、住宅、基础设施、工业及公共)和地区(中国、印度、日本、韩国、泰国、印尼、马来西亚、越南、澳洲、亚太其他地区)进行细分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 建筑业需求不断成长

- 预製混凝土生产规模扩大

- 奢华建筑中的美学至上

- 对太阳能反射屋顶涂料的需求激增

- 净零能耗建筑规范(新加坡和韩国)

- 市场限制

- 高昂的生产成本

- 与无机颜料的竞争

- 碳边境调节成本

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型

- 一型

- III型

- 其他年级

- 透过使用

- 商业的

- 住宅

- 基础设施

- 工业和公共设施

- 按地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 印尼

- 马来西亚

- 越南

- 澳洲

- 亚太其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Ambuja Cement(Adani Group)

- Cementir Holding NV

- CEMEX SAB. de CV

- CIMSA

- HOLCIM

- Hume Cement Sdn Bhd

- India Cements Ltd

- JK Cement Ltd

- Royal El Minya Cement

- SCG International Corporation

- SUMITOMO OSAKA CEMENTCo.,Ltd.

- UltraTech Cement Ltd

第七章 市场机会与未来展望

The Asia-Pacific White Cement Market is expected to grow from 14.53 million tons in 2025 to 15.23 million tons in 2026 and is forecast to reach 19.24 million tons by 2031 at 4.79% CAGR over 2026-2031.

Solid infrastructure pipelines, rising disposable incomes, and stricter energy-efficiency rules are reinforcing demand as real estate developers seek materials that combine visual appeal with lower thermal loads. Premium positioning enables producers to secure higher margins despite rising fuel costs, while consolidation among Indian and Chinese manufacturers is unlocking scale benefits that temper price volatility. Ongoing migration to urban centers keeps residential starts elevated, yet forward contracts signed for airports, metros, and mixed-use complexes point to a widening commercial opportunity set. Makers are also capitalizing on sustainability credentials: white cement's high albedo supports cool-roof mandates and helps projects meet LEED and Green Mark targets, fostering a durable pull from architects and project owners.

Asia-Pacific White Cement Market Trends and Insights

Growing Demand from Construction Sector

Infrastructure allocations now exceed 5% of GDP in markets such as the Philippines, while India's Pradhan Mantri Awas Yojana has sanctioned 25.64 million rural homes, sustaining intake of premium binders. Thailand's Eastern Economic Corridor continues to attract logistics and semiconductor plants, underpinning a 3%-4% annual build-rate through 2026. Because white cement commands a 15%-20% price premium over gray cement, producers benefit disproportionately from the upswing of cement prices.

Expanding Precast Concrete Manufacturing

Factory-controlled modules meet developers' need for faster schedules and reduced on-site labor. Japan-headquartered Taiheiyo Cement commissioned a USD 266 million line in Cebu that raises Philippines capacity 50%, specifically to serve facade and panel products that rely on white cement's color stability. UltraTech's "Very Amazing Concrete" portfolio illustrates the parallel shift in India, merging durability additives with bright finishes that architects specify for curtain walls and landscape furniture. Trial runs using calcined-clay blends at Cemcor delivered 3,000 tons of low-carbon precast elements, signalling process convergence between environmental and productivity goals.

High Production Cost

White clinker firing temperatures approach 1,500 °C, elevating fuel costs and kiln refractory wear. Indonesian plants run at just 54.2% utilization, leaving fixed overheads spread across fewer tons and eroding margins. Meanwhile, the World Cement Association cautions that carbon levies add USD 4-6/ton, forcing smaller producers either to upgrade lines or cede share to integrated majors already migrating to alternative fuels.

Other drivers and restraints analyzed in the detailed report include:

- Aesthetic Premium in High-End Architecture

- Surge in Solar-Reflective Roof Coatings

- Competition from Inorganic Pigments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Type I captured 51.92% Asia-Pacific white cement market share in 2025 and is on track for a 5.05% CAGR to 2031. Volume traction stems from compatibility with mainstream admixtures and standardized compressive-strength classes, simplifying specification work for engineers on tower, bridge, and metro projects. In 2024, the segment accounted for more than half of the Asia-Pacific white cement market size, reflecting its role as the default binder for architectural precast, terrazzo, and swimming pools.

Capacity deployment favors Type I as kilns can switch between gray and white campaigns with fewer chemistry adjustments, allowing firms like UltraTech to meet seasonal surges without idle inventory. The breadth of end-use cases reinforces bargaining power with distributors who prioritize fast-moving stock. As precasters scale exports to Japan and Australia, uniform specifications around ASTM C150 increasingly lock in Type I as the reference product, reinforcing its dominance through network effects.

The Asia-Pacific White Cement Market Report is Segmented by Type (Type I, Type III, and Other Grades), Application (Commercial, Residential, Infrastructure, and Industrial and Institutional), and Geography (China, India, Japan, South Korea, Thailand, Indonesia, Malaysia, Vietnam, Australia, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- Ambuja Cement (Adani Group)

- Cementir Holding NV

- CEMEX SAB. de CV

- CIMSA

- HOLCIM

- Hume Cement Sdn Bhd

- India Cements Ltd

- J.K. Cement Ltd

- Royal El Minya Cement

- SCG International Corporation

- SUMITOMO OSAKA CEMENTCo.,Ltd.

- UltraTech Cement Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from Construction Sector

- 4.2.2 Expanding Precast Concrete Manufacturing

- 4.2.3 Aesthetic Premium in High-End Architecture

- 4.2.4 Surge in Solar-Reflective Roof Coatings

- 4.2.5 Net-Zero Building Codes (SG and KR)

- 4.3 Market Restraints

- 4.3.1 High Production Cost

- 4.3.2 Competition from Inorganic Pigments

- 4.3.3 Carbon-Border-Adjustment Costs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Type I

- 5.1.2 Type III

- 5.1.3 Other Grades

- 5.2 By Application

- 5.2.1 Commercial

- 5.2.2 Residential

- 5.2.3 Infrastructure

- 5.2.4 Industrial and Institutional

- 5.3 By Geography

- 5.3.1 China

- 5.3.2 India

- 5.3.3 Japan

- 5.3.4 South Korea

- 5.3.5 Thailand

- 5.3.6 Indonesia

- 5.3.7 Malaysia

- 5.3.8 Vietnam

- 5.3.9 Australia

- 5.3.10 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Ambuja Cement (Adani Group)

- 6.4.2 Cementir Holding NV

- 6.4.3 CEMEX SAB. de CV

- 6.4.4 CIMSA

- 6.4.5 HOLCIM

- 6.4.6 Hume Cement Sdn Bhd

- 6.4.7 India Cements Ltd

- 6.4.8 J.K. Cement Ltd

- 6.4.9 Royal El Minya Cement

- 6.4.10 SCG International Corporation

- 6.4.11 SUMITOMO OSAKA CEMENTCo.,Ltd.

- 6.4.12 UltraTech Cement Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

白色水泥:市场占有率分析、产业趋势与统计、成长预测(2026-2031)

白色水泥:市场占有率分析、产业趋势与统计、成长预测(2026-2031) 全球白水泥市场规模、份额、趋势和成长分析报告(2026-2034年)

全球白水泥市场规模、份额、趋势和成长分析报告(2026-2034年) 日本白水泥市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年

日本白水泥市场规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年 2026年全球白水泥市场报告

2026年全球白水泥市场报告 白水泥市场按产品类型、应用、最终用户和销售管道划分-2025-2032年全球预测2025-2033年白水泥市场规模、份额、趋势及预测(按类型、应用和地区)

白水泥市场按产品类型、应用、最终用户和销售管道划分-2025-2032年全球预测2025-2033年白水泥市场规模、份额、趋势及预测(按类型、应用和地区) 白水泥市场机会、成长动力、产业趋势分析及2025-2034年预测

白水泥市场机会、成长动力、产业趋势分析及2025-2034年预测 白水泥市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2025-2030

白水泥市场规模、份额、趋势分析报告:按产品、按应用、按地区、细分市场预测,2025-2030 全球白水泥市场2024-2028

全球白水泥市场2024-2028