|

市场调查报告书

商品编码

1934808

木炭:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Charcoal - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

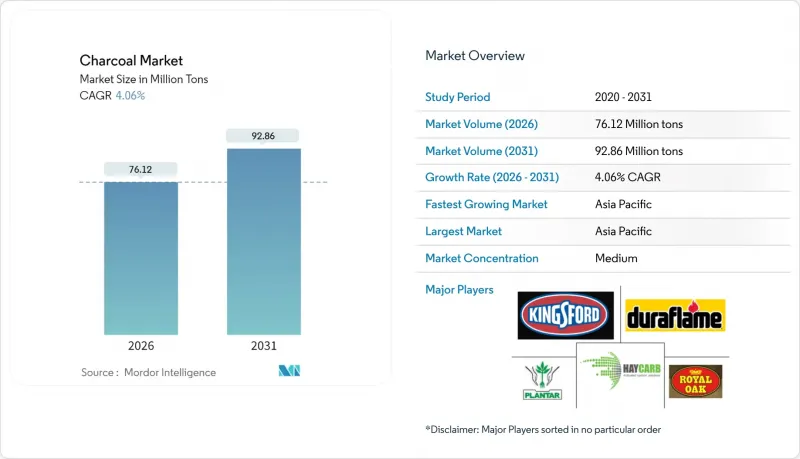

预计木炭市场将从 2025 年的 7,315 万吨增长到 2026 年的 7,612 万吨,到 2031 年将达到 9,286 万吨,2026 年至 2031 年的复合年增长率为 4.06%。

这项扩张受到两个截然相反的因素的影响:新兴经济体家庭烹饪对木炭的持续依赖,以及已开发地区烧烤和活性碳应用领域的高端市场成长。为了满足欧盟森林砍伐法规对永续性审核日益增长的需求,供应链正围绕人工林原料和椰子壳进行重组。同时,垂直整合有助于在认证成本不断上涨的情况下维持利润率。竞争格局正在改变:大型煤球生产商维持着产量,而强调不添加添加剂的天然块状木炭生产商则持续面临挑战。钢铁製造商和水泥厂正在测试生物炭混合物,一旦解决与堆积密度和磷含量相关的技术难题,这些混合物有望将收入来源多元化,拓展到新的工业需求领域。能够证明产品可追溯性并运作高温窑炉的生产商,将有机会抓住以环境、社会和治理(ESG)主导的出口机会,并在活性碳应用领域获得更高的吨附加价值。

全球木炭市场趋势与洞察

新兴经济体对家用烹饪燃料的需求不断增长

儘管液化石油气(LPG)得到了大力推广,但印度、中国和非洲国家的农村地区仍然依赖固态燃料,从而支撑了木炭市场。在印度,受益于「贫困阶级燃气计画」(PMUY)的家庭每年消耗的液化石油气钢瓶数量往往少于非受益家庭。这种差异表明,受益家庭有囤积燃料的倾向,尤其是在全球液化石油气价格超过一定水准时。在中国,相当一部分农村家庭的能源需求仍依赖生质能。此外,「十四五」规划中政策的模糊性阻碍了彻底摆脱生质能的进程。国际能源总署(IEA)警告说,如果目前的政策持续下去,到2030年,仍有很大一部分人口无法获得清洁的烹饪方式,从而维持对木炭的需求。值得注意的是,液化石油气的普及率与女性识字率和道路网络密度等因素更为密切相关,这表明基础设施和教育的作用比单纯的补贴更为重要。

已开发市场户外烧烤和烧烤文化的快速发展

随着优质化的不断推进,天然硬木炭和特殊备长炭越来越受到关注,其价值也超越了传统的通用木炭。虽然金斯福德(Kingsford)在美国木炭市场占据主导地位,但皇家橡树(Royal Oak)等竞争对手和利基市场品牌正凭藉专注于单一树种木材的天然木炭产品进入市场。在欧洲和北美,以耐高温着称的备长炭在专业厨房中越来越受欢迎。为了因应欧盟即将推出的森林砍伐法规,德国零售商正在调整产品线,专注于推广FSC认证产品。印尼和越南的供应商正在挑战市场,他们提供的荔枝桉木备长炭产品可取代日本纪州备长炭,同时仍能满足严格的耐高温标准。同时,北欧白天鹅生态标章透过强制使用认证木材来促进永续性,加速了向人工林原料的过渡。

严格的林业法规和遏制森林砍伐

欧盟的森林砍伐法规对违规行为处以罚款和货物扣押。 2020年后,无法证明零森林砍伐的出口商将面临更高的文件成本。森林管理委员会(FSC)的审核费用实际上将非洲和东欧的小规模生产商排除在外,使出口市场向大型认证企业集中。肯亚和坦尚尼亚的季节性伐木禁令推高了当地价格,但执法力度仍然参差不齐。供应风险促使欧洲买家增加从巴西采购尤加利树和从东南亚采购椰子壳,但行政的挑战持续延长前置作业时间。

细分市场分析

受印尼雄心勃勃的目标和越南根据HS4402.90.10编码给予的出口免税政策的推动,椰壳炭预计将以5.25%的复合年增长率增长,超过其他产品。在金斯福德公司令人瞩目的年产量支持下,炭块继续主导大众市场,预计到2025年将保持38.12%的木炭市场份额。同时,烧烤爱好者越来越多地转向硬木炭和备长炭,推高了天然块状木炭的价格,使其高于标准商品炭块。椰壳炭的微孔结构也推动了地方政府水质净化厂和工业VOC脱硫装置的需求成长,从而创造了双重收入来源。

与传统的露天焚烧相比,高压粘合剂压块技术显着提高了燃烧效率并降低了排放。这种环保方法符合北欧白天鹅等认证标准。巴西和巴拉圭的桉树种植园确保了产销监管链的可追溯性,这对欧盟买家来说至关重要。日本纪州备长炭依然保持着其超高端产品的声誉,而来自印尼和越南的白炭由于进口成本降低,其热性能与之相近,如今也更容易获得。

木炭市场报告按产品类型(煤球、硬木块状木炭、椰壳木炭、备长炭等)、应用领域(烹饪燃料、烧烤/户外烤炉、冶金燃料、水和空气净化、医疗、化妆品和个人护理等)以及地区(亚太地区、北美地区、欧洲地区等)进行细分。市场预测以吨为单位。

区域分析

预计到2025年,亚太地区将占全球整体的55.05%,并在2031年之前维持5.03%的年复合成长率,成为成长最快的地区。这一增长主要得益于印尼、越南和印度椰壳供应链的不断加强,以及农村地区持续的烹饪需求。印尼的出口受益于沙乌地阿拉伯和美国的需求。儘管印度的液化石油气连接数创历史新高,但其每月公用事业供应量(PMUY)的补充率低于预期。然而,该国的燃料储备活动支撑了木炭需求。同时,中国居民能源消耗仍主要依赖农村生物质能,凸显了都市区燃气管网与农村木炭依赖程度之间的巨大差距。

在北美,木炭产量成长缓慢,但利润率稳健。金斯福德(Kingsford)正利用规模经济效应,而皇家橡树(Royal Oak)的天然块状木炭销量激增,这两家公司都受益于整体优质化趋势。加拿大和墨西哥的产量小规模,而美国的特色餐厅则增加了备长炭的进口量。在欧洲,需求取决于是否符合认证标准,德国在烧烤木炭消费方面主导地位。北欧白天鹅生态标章推广人工林种植的木柴,波兰已成为主要出口国,而森林管理委员会(FSC)加强的生产审核也提高了供应链的透明度。

在南美洲,垂直整合的桉树种植园蓬勃发展,Plantal 和 Brikapal 等公司在欧洲市场获得了高价,尤其是在认证产品供应稀缺的地区。非洲是重要的产区,但主要以非正规通路运作。认证成本给当地的小规模生产商带来了挑战,许多生产商倾向于将未经认证的产品转售给中东或国内买家。在中东,主要来自沙乌地阿拉伯的进口商正转向印尼和中国市场,这些地区对传统烹饪和水烟馆的依赖程度很高,因此需求保持稳定。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新兴经济体对家用烹饪燃料的需求不断增长

- 户外烧烤文化在已开发市场蓬勃发展

- 净化和医疗领域对活性碳的需求不断增长

- 在钢铁和水泥工业中用作焦炭替代品。

- 优质认证永续木炭开闢了ESG出口通路

- 市场限制

- 严格的森林法规和遏制森林砍伐的措施

- 由于环境问题,木材原料供应受到限制

- 液化石油气和电炊具在非洲和亚洲都市区迅速普及

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 木炭煤球

- 硬木灯

- 椰子壳

- 备长炭

- 其他产品种类(糖蜜炭、红树林炭、水烟炭、锯末炭、根炭)

- 透过使用

- 烹饪燃料

- 烧烤炉/户外烧烤架(零售和餐饮业)

- 冶金燃料

- 水和空气净化

- 卫生保健

- 化妆品和个人护理

- 其他用途(烧烤和园艺)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- BRICAPAR SA Charcoal Briquettes

- Calgon Carbon Corporation

- Duraflame, Inc.

- E & C Charcoal

- Etosha

- Fire & Flavor

- Fogo Charcoal

- GRYFSKAND

- Haycarb PLC

- JACOBI CARBONS GROUP

- Kingsford Products Company

- MATSURI INTERNATIONAL CO. LTD

- Mesjaya Sdn Bhd

- NAMCHAR

- NamCo Charcoal and Timber Products

- Oxford Charcoal Company

- Paraguay Charcoal

- Plantar

- PT Cavron Global

- Royal Oak Enterprises, LLC

- Sagar Charcoal and Firewood Depot

- Subur Tiasa Holdings Berhad

- Timber Charcoal Company LLC

第七章 市场机会与未来展望

The Charcoal market is expected to grow from 73.15 million tons in 2025 to 76.12 million tons in 2026 and is forecast to reach 92.86 million tons by 2031 at 4.06% CAGR over 2026-2031.

This expansion is shaped by two contrasting forces: the sustained reliance on charcoal for household cooking across emerging economies and premium-segment growth in developed regions for barbecue and activated carbon uses. Supply chains are reorganizing around plantation feedstocks and coconut shells to meet the increasing demands of sustainability audits linked to the EU Deforestation Regulation, while vertical integration helps shield profit margins amid rising certification costs. Competitive dynamics are evolving as large briquette producers defend volume against natural-lump challengers that emphasize additive-free formulations. Steelmakers and cement plants are testing biochar blends, offering a nascent industrial demand stream that could diversify revenues once technical hurdles on bulk density and phosphorus content are resolved. Producers able to document traceability and operate high-temperature kilns are positioned to capture both ESG-driven export opportunities and higher value per ton in activated-carbon applications.

Global Charcoal Market Trends and Insights

Rising Demand for Household Cooking Fuel in Emerging Economies

Despite an aggressive LPG rollout, rural areas in India, China, and many parts of Africa continue to rely on solid fuels, thereby bolstering the charcoal market. In India, beneficiaries of the PMUY scheme consume fewer LPG cylinders annually compared to non-PMUY households. This discrepancy highlights a tendency to stack fuels, especially when global LPG prices exceed a certain threshold. In China, rural households continue to rely on biomass for a substantial portion of their energy needs. Furthermore, the policy ambivalence of the 14th Five-Year Plan is hindering a complete transition away from biomass. The International Energy Agency warns that if current policies persist, by 2030, a large population will still lack access to clean cooking solutions, ensuring a sustained demand for charcoal. Interestingly, the pace of LPG adoption is more closely tied to factors like female literacy and road density, suggesting that infrastructure and education play a more pivotal role than subsidies alone.

Outdoor Grilling and BBQ Culture Surge in Developed Markets

As premiumization takes center stage, lump hardwood and specialty Binchotan are gaining traction, edging out traditional commodity briquettes in terms of value. While Kingsford commands a dominant share of the U.S. briquette market, competitors like Royal Oak and other niche players are making inroads, especially with their natural-lump offerings that emphasize single-species sourcing. In Europe and North America, professional kitchens are turning to Binchotan, known for its ability to maintain high temperatures. In anticipation of the EU Deforestation Regulation, German retailers are adjusting their assortments to focus on FSC-certified lines. Suppliers from Indonesia and Vietnam are challenging the market by offering alternatives to Japan's Kishu Binchotan, utilizing lychee and eucalyptus feedstocks, all while adhering to stringent high-heat specifications. Meanwhile, the Nordic Swan Ecolabel promotes sustainability by mandating certified wood content, thereby accelerating the shift towards plantation feedstocks.

Stringent Forestry Regulations and Deforestation Curbs

The EU Deforestation Regulation imposes fines and allows for shipment confiscation in cases of non-compliance. Exporters failing to prove zero deforestation post-2020 face rising documentation costs. Audit fees from the Forest Stewardship Council (FSC) effectively sideline smallholders in Africa and Eastern Europe, leading to a concentration of export flows among larger, certified entities. While seasonal harvest bans in Kenya and Tanzania elevate local prices, their enforcement remains inconsistent. Due to supply risks, European buyers are increasingly sourcing eucalyptus from Brazilian plantations and coconut shells from Southeast Asia, though administrative challenges continue to extend lead times.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Activated-Charcoal Demand in Purification and Healthcare

- Industrial Use as Coke Substitute in Iron, Steel, and Cement

- Rapid LPG and Electric-Cooking Roll-Out in Africa/Asia Urban Hubs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Driven by Indonesia's ambitious target and Vietnam's export-tax exemption under HS4402.90.10, coconut-shell charcoal is expanding at a 5.25% CAGR, outpacing its counterparts. Briquettes continue to dominate the mass retail market with a 38.12% charcoal market share in 2025, bolstered by Kingsford's impressive annual output. While hardcore barbecue aficionados lean towards hardwood lump and Binchotan, this trend has propelled natural-lump prices to higher levels compared to standard commodity briquettes. The microporous structure of coconut-shell charcoal is fueling its growing demand from municipal water plants and industrial VOC scrubbers, creating a dual revenue stream.

Utilizing high-pressure, binder-free briquette technology, combustion efficiency improves significantly, resulting in reduced emissions compared to traditional open burning. This eco-friendly approach resonates with labels like the Nordic Swan. Eucalyptus plantations in Brazil and Paraguay are ensuring the chain-of-custody traceability that EU buyers prioritize. While Japan's Kishu Binchotan holds an ultra-premium reputation, Indonesian and Vietnamese white charcoals, boasting similar thermal specifications, are now more accessible due to their lower landed costs.

The Charcoal Market Report is Segmented by Product Type (Briquettes, Hardwood Lump, Coconut-Shell, Binchotan, and Other Product Types), Application (Cooking Fuel, Barbecue/Outdoor Grilling, Metallurgical Fuel, Water and Air Purification, Healthcare, Cosmetics and Personal Care, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific delivered 55.05% of global volume in 2025 and will log the fastest 5.03% CAGR to 2031. This growth is driven by Indonesia, Vietnam, and India strengthening their supply chains around coconut shells, alongside enduring demand for rural cooking. Indonesia's exports were buoyed by demand from Saudi Arabia and the U.S. Despite record LPG connections, India's PMUY refill rates lagged behind expectations; yet, the nation's fuel-stocking behavior cushioned charcoal volumes. Meanwhile, a significant portion of household energy in China continues to derive from rural biomass, highlighting a divide between urban gas grids and rural reliance on charcoal.

In North America, while tonnage growth is modest, profit margins are robust. Kingsford capitalizes on scale, and Royal Oak experiences a surge in natural-lump sales, all amidst a broader trend of premiumization. While Canada and Mexico contribute with modest production, specialty restaurants across the U.S. are increasingly importing Binchotan. In Europe, demand hinges on compliance with certification standards, with Germany leading the way in barbecue volumes. The Nordic Swan Ecolabel is championing plantation sources, and while Poland stands out as a key exporter, tightening FSC volume audits are enhancing transparency in the supply chain.

South America is capitalizing on vertically integrated eucalyptus plantations. Companies like Plantar and BRICAPAR are reaping premiums in European markets, especially where certified supplies are in short supply. Africa, though a significant player, operates largely in the informal realm. Here, the costs of certification pose challenges for smallholders, leading many to redirect uncertified outputs to buyers in the Middle East and domestically. In the Middle East, importers, predominantly from Saudi Arabia, are turning to Indonesian and Chinese sources, underscoring their reliance on both traditional cooking and hookah lounges, which ensures a consistent demand.

- BRICAPAR S.A. Charcoal Briquettes

- Calgon Carbon Corporation

- Duraflame, Inc.

- E & C Charcoal

- Etosha

- Fire & Flavor

- Fogo Charcoal

- GRYFSKAND

- Haycarb PLC

- JACOBI CARBONS GROUP

- Kingsford Products Company

- MATSURI INTERNATIONAL CO. LTD

- Mesjaya Sdn Bhd

- NAMCHAR

- NamCo Charcoal and Timber Products

- Oxford Charcoal Company

- Paraguay Charcoal

- Plantar

- PT Cavron Global

- Royal Oak Enterprises, LLC

- Sagar Charcoal and Firewood Depot

- Subur Tiasa Holdings Berhad

- Timber Charcoal Company LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for household cooking fuel in emerging economies

- 4.2.2 Outdoor grilling and BBQ culture surge in developed markets

- 4.2.3 Expansion of activated-charcoal demand in purification and healthcare

- 4.2.4 Industrial use as coke substitute in iron, steel and cement

- 4.2.5 Premium certified-sustainable charcoal unlocking ESG export channels

- 4.3 Market Restraints

- 4.3.1 Stringent forestry regulations and deforestation curbs

- 4.3.2 Environmental concerns limiting wood-feedstock supply

- 4.3.3 Rapid LPG and electric-cooking roll-out in Africa/Asia urban hubs

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Briquettes

- 5.1.2 Hardwood Lump

- 5.1.3 Coconut-Shell

- 5.1.4 Binchotan

- 5.1.5 Other Product Types (Sugar charcoal, Mangrove, Shisha, Sawdust, and Root)

- 5.2 By Application

- 5.2.1 Cooking Fuel

- 5.2.2 Barbecue/Outdoor Grilling (Retail and HoReCa)

- 5.2.3 Metallurgical Fuel

- 5.2.4 Water and Air Purification

- 5.2.5 Healthcare

- 5.2.6 Cosmetics and Personal Care

- 5.2.7 Other Applications (Barbeque and Horticulture)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BRICAPAR S.A. Charcoal Briquettes

- 6.4.2 Calgon Carbon Corporation

- 6.4.3 Duraflame, Inc.

- 6.4.4 E & C Charcoal

- 6.4.5 Etosha

- 6.4.6 Fire & Flavor

- 6.4.7 Fogo Charcoal

- 6.4.8 GRYFSKAND

- 6.4.9 Haycarb PLC

- 6.4.10 JACOBI CARBONS GROUP

- 6.4.11 Kingsford Products Company

- 6.4.12 MATSURI INTERNATIONAL CO. LTD

- 6.4.13 Mesjaya Sdn Bhd

- 6.4.14 NAMCHAR

- 6.4.15 NamCo Charcoal and Timber Products

- 6.4.16 Oxford Charcoal Company

- 6.4.17 Paraguay Charcoal

- 6.4.18 Plantar

- 6.4.19 PT Cavron Global

- 6.4.20 Royal Oak Enterprises, LLC

- 6.4.21 Sagar Charcoal and Firewood Depot

- 6.4.22 Subur Tiasa Holdings Berhad

- 6.4.23 Timber Charcoal Company LLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

炭市场:2026-2032年全球市场预测(依产品形式、应用、最终用途产业及通路划分)

炭市场:2026-2032年全球市场预测(依产品形式、应用、最终用途产业及通路划分) 2026年全球椰子木炭烧烤煤球市场报告2026年全球烧烤木炭市场报告

2026年全球椰子木炭烧烤煤球市场报告2026年全球烧烤木炭市场报告 木炭煤球市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、等级、分销管道、地区和竞争格局划分,2021-2031年酒桶市场 - 全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球全天然烧烤木炭市场:依产品类型、原料、包装、应用及通路划分,2026-2032年预测活性碳牙刷市场按刷毛类型、包装规格、分销管道和最终用户划分,全球预测(2026-2032年)煤球活性碳市场:依原料、活化方法、物理形态、应用和最终用途划分,全球预测(2026-2032年)

木炭煤球市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、等级、分销管道、地区和竞争格局划分,2021-2031年酒桶市场 - 全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年全球全天然烧烤木炭市场:依产品类型、原料、包装、应用及通路划分,2026-2032年预测活性碳牙刷市场按刷毛类型、包装规格、分销管道和最终用户划分,全球预测(2026-2032年)煤球活性碳市场:依原料、活化方法、物理形态、应用和最终用途划分,全球预测(2026-2032年) 木炭市场规模、份额和成长分析(按产品类型、原材料、应用、最终用户、通路、品质、永续和地区划分)-2026-2033年产业预测

木炭市场规模、份额和成长分析(按产品类型、原材料、应用、最终用户、通路、品质、永续和地区划分)-2026-2033年产业预测 竹炭纤维:全球市占率及排名、总收入及需求预测(2025-2031年)

竹炭纤维:全球市占率及排名、总收入及需求预测(2025-2031年)