|

市场调查报告书

商品编码

1934837

辅助胶凝材料(SCM):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Supplementary Cementitious Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

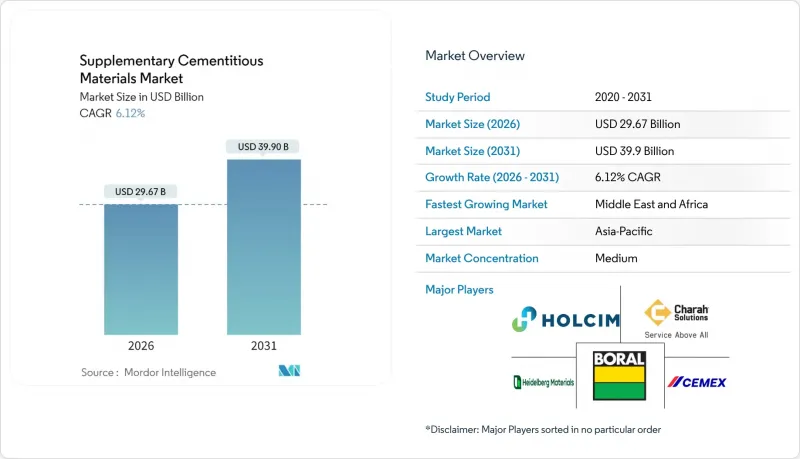

预计辅助胶凝材料 (SCM) 市场将从 2025 年的 279.6 亿美元成长到 2026 年的 296.7 亿美元,到 2031 年将达到 399 亿美元,2026 年至 2031 年的复合年增长率为 6.12%。

这一增长反映了建设产业在政府实施碳定价机制和公共工程强制使用低碳混凝土后,正迅速向永续建筑方法转型。沙乌地阿拉伯耗资1.1兆美元的「2030愿景」等加速基础设施投资计划,以及随着燃煤替代能源的减少,水泥产业需要降低水泥熟料用量,共同推动了对辅助胶凝材料的持续需求。煅烧粘土、火山灰和石灰石混合水泥等供应侧创新,缓解了飞灰和矿渣供应减少的问题;而快速煅烧技术则可将加工能耗降低高达40%,并扩大了可用原材料的来源。

全球辅助胶凝材料(SCM)市场趋势及展望

全球建筑和基础设施支出激增

大规模公共工程资金的投入正在推动辅助胶凝材料市场的发展。印度2023-2024财年的基础建设资本支出成长了5.7倍,达到361亿美元;沙乌地阿拉伯的「2030愿景」投资额超过1.1兆美元;非洲的基础建设支出平均每年达到930亿美元。这些计划都规定了提高混凝土中辅助胶凝材料(SCMs)的替代率。例如,雪梨地铁的替代率达到了38%-52%,并在整个计划中减少了12万吨二氧化碳排放。因此,建筑需求的激增使辅助胶凝材料的需求翻了一番,供应商得以获得长期合同,从而有理由投资于闪速煅烧设备和优化物流。

更严格的二氧化碳排放法规和碳定价

监管压力日益增加:法国的RE2020将蕴藏量建筑的碳排放量限制在640-740公斤二氧化碳当量/平方米;欧盟的碳边境调节机制对进口产品征收碳价;美国的《清洁采购法》要求联邦政府资助的混凝土采购必须提供环境产品声明(EPD);加州对建筑材料的碳定价政策则为高掺杂政策创造了MSC市场数据(MSCM这些法规使得脱碳混凝土成为一种经济上有吸引力的选择,并巩固了对SCM的结构性需求,将其视为一种监管应对措施。

由于燃煤电厂和高炉炼钢厂的减少,优质飞灰和炉渣的供应量下降。

自2010年以来,美国燃煤发电量下降了60%,导致优质飞灰供应量急剧减少。同时,随着钢铁企业转向电炉炼钢,高炉矿渣供应量也减少。剩余的粉煤灰库存价格溢价40%至60%,且运输距离更长,成本优势逐渐丧失。因此,混凝土生产商必须重新设计混凝土配比,采用替代性胶凝材料,否则将面临更高的原料成本,这将限制其在短期内的成长,直到新的供应来源成熟。

细分市场分析

儘管燃煤发电量下降,但飞灰凭藉其完善的物流网络和可预测的火山灰活性,预计到2025年仍将占据水泥基外加剂市场41.72%的份额。矿渣水泥(GGBFS)紧随其后,儘管高炉产量持续萎缩,仍将继续供应高性能混凝土领域。同时,由于闪速煅烧炉的广泛应用,煅烧黏土的复合年增长率(CAGR)达到6.88%,闪速煅烧炉降低了能源成本,使得经济高效地加工高岭土含量为15-25%的黏土成为可能。这种成长趋势使煅烧黏土成为日益减少的煤基原料的重要替代品,重塑了该地区的供应结构,并吸引了拥有丰富矿床的新进者。

製造商正大力投资建造专用煅烧和研磨设备,以实现超精确的粒度控制,从而将火山灰反应活性指数提高到 800 mg Ca(OH)2/g 以上,进而获得溢价。硅灰和高活性偏高岭土在超高性能混凝土中继续发挥其独特的作用,而石灰石填料则促进了波特兰石灰石水泥在全球范围内的普及,并强化了逐步脱水泥熟料的途径。总而言之,这些趋势表明,辅助胶凝材料的生产策略正从对工业废弃物的随意利用转向有计划、可扩展的市场化生产。

补充胶凝材料报告按补充胶凝材料类型(飞灰、矿渣水泥、硅灰)、最终用户(住宅建筑、商业/公共、工业等)、材料形态(粉末、浆料/悬浮液等)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以美元以金额为准。

区域分析

预计亚太地区仍将是辅助胶凝材料(SCM)市场的中心,到2025年将占据全球47.88%的市场。这主要得益于中国持续但成长放缓的建设活动,以及印度快速的基础建设支出(预计在2023-2024财年将达到361亿美元)。儘管煤灰和高炉矿渣的充足供应曾经支撑了低成本供应,但环保政策正在加速燃煤发电厂的淘汰,促使区域水泥巨头优先考虑位于高岭土矿床附近的煅烧粘土生产中心。东南亚国协正利用「一带一路」倡议的资金建设交通走廊,这些走廊需要大量高掺量辅助胶凝材料混凝土;与此同时,日本和韩国正在为抗震和海洋基础设施引入高品质的偏高岭土外加剂。

预计中东和非洲地区将经历最快的成长,到2031年复合年增长率将达到6.42%,这主要得益于沙乌地阿拉伯的NEOM和红海计划,以及该地区对低碳材料的强制性要求。阿联酋的Estidama标准和埃及的绿色建筑标准已将辅助胶凝材料(SCM)的使用标准纳入法规,推动了东非火山灰加工和萨赫勒地区粘土烧製计划的投资。物流挑战和品质保证的缺乏阻碍了即时规模化生产,但丰富的矿产资源有望在加工基础设施成熟后实现区域自给自足。在北美,燃煤发电量下降了60%,导致飞灰供应紧张,促使内华达州和犹他州加大对天然火山灰资源的探勘,并增加了从欧洲进口炉渣。联邦清洁采购法规和州级税额扣抵有利于早期采用高SCM配方的企业,儘管供应存在摩擦,但仍支撑了强劲的需求。在欧洲,成熟的碳定价机制和RE2020建筑标准正在挑战石灰石、煅烧粘土和再生细料在工业规模上应用的技术极限,巩固了其作为脱碳试验场的地位。南美洲虽然规模较小,但发展势头强劲,巴西的沿海韧性计划和智利的矿业基础设施都需要耐用、低碳的混凝土,当地的火山灰和稻壳灰企业也逐渐融入全球供应链。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球建筑和基础设施投资快速成长

- 更严格的二氧化碳排放法规和碳定价

- 混合水泥和环保水泥(例如,PLC)的快速推广

- 政府绿色采购奖励

- 煅烧粘土和天然火山灰计划激增,开闢了新的供应来源

- 市场限制

- 煤炭和高炉炼钢的减少导致优质飞灰和炉渣的供应减少。

- 供应链管理品质和规格差异很大

- 来自新型低水泥熟料接合材料的竞争,绕过了传统的供应链管理(SCM)链。

- 价值链分析

- 监管环境

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按类型分類的辅助胶凝材料 (SCM)

- 飞灰

- 矿渣水泥(细磨高炉矿渣)

- 硅灰

- 煅烧粘土/偏高岭土

- 石灰石填料

- 其他产品

- 最终用户

- 住宅

- 商业和公共设施

- 工业设施

- 交通基础建设(公路、铁路、港口、机场)

- 能源和公共产业基础设施

- 按物质形式

- 粉末

- 浆液/悬浮液

- 颗粒

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率/排名分析

- 公司简介

- Advanced Cement Technologies LLC

- ArcelorMittal SA

- Bharathi Cement Corporation Private Limited

- BASF SE

- Boral Ltd.

- CEMEX SAB de CV

- CemGreen ApS

- Charah Solutions

- CR Minerals Company LLC

- Dangote Cement Plc.

- Ecocem

- Ferroglobe PLC

- HeidelberCement

- Hoffmann Green Cement Technologies

- Holcim Group

- JSW Cement Ltd.

- Tata Steel Ltd.

- TITAN

- UltraTech Cement Ltd.

- Votorantim Cimentos

第七章 市场机会与未来展望

The Supplementary Cementitious Materials market is expected to grow from USD 27.96 billion in 2025 to USD 29.67 billion in 2026 and is forecast to reach USD 39.9 billion by 2031 at 6.12% CAGR over 2026-2031.

This expansion reflects the construction sector's rapid shift toward sustainable building practices as governments enforce carbon-pricing schemes and public-sector projects embed low-carbon concrete mandates. Accelerating infrastructure investment programs-such as Saudi Arabia's USD 1.1 trillion Vision 2030 pipeline-collide with the cement industry's need to reduce clinker content amid dwindling coal-fired by-products, creating durable demand for SCMs. Supply-side innovation in calcined clay, volcanic pozzolans, and limestone-blended cements mitigates the shrinking availability of fly ash and slag, while flash-calcination technology lowers processing energy requirements by up to 40% and broadens the viable feedstock base.

Global Supplementary Cementitious Materials Market Trends and Insights

Boom in Global Construction and Infrastructure Spending

Massive public-works funding underpins the supplementary cementitious materials market, with India's infrastructure capital expenditure swelling 5.7 times to USD 36.1 billion in 2023-24, Saudi Arabia's Vision 2030 exceeding USD 1.1 trillion, and African infrastructure outlays averaging USD 93 billion each year. These programs specify higher SCM substitution in concrete-Sydney Metro achieved 38-52% replacement, resulting in a 120,000-tonne CO2-e reduction across projects . The construction surge, therefore, multiplies SCM demand, enabling suppliers to secure long-term contracts that justify investments in flash-calciner capacity and logistics optimization.

Stricter CO2-Emissions Regulations and Carbon-Pricing Schemes

Regulatory pressure is intensifying. France's RE2020 caps embodied carbon in new buildings at 640-740 kg CO2-e/m2, while the EU's Carbon Border Adjustment Mechanism prices imports on a carbon basis. US Buy Clean rules require Environmental Product Declarations for federally funded concrete, and California applies carbon pricing to construction materials, creating premium markets for high-SCM mixes. These regulations make decarbonized concrete economically attractive, locking in structural demand for SCMs as a compliance pathway.

Dwindling Supply of Quality Fly Ash and Slag as Coal and BF Steel Decline

Coal-power output in the U.S. has fallen 60% since 2010, slashing high-grade fly ash volumes, while blast-furnace slag shrinks as steel producers pivot to electric arc furnaces. Remaining ash stockpiles command a 40-60% price premium, and transport distances lengthen, eroding cost advantages. Concrete producers must therefore re-engineer mix designs around alternative SCMs or pay higher inputs, constraining short-term growth until new supply sources mature.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Blended/Green Cements

- Government Green-Procurement Incentives

- High Variability in SCM Quality/Specifications

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fly ash held a 41.72% market share of the Supplementary Cementitious Materials market in 2025, supported by well-established logistics networks and predictable pozzolanic properties, despite declining coal generation. Slag cement (GGBFS) follows, supplying high-performance concrete segments even as blast-furnace output contracts. Calcined clay, however, is expanding at a 6.88% CAGR as flash-calciner units proliferate, lowering energy costs and enabling economic processing of clay with only 15-25% kaolinite. This trajectory positions calcined clay as the primary substitute for dwindling coal-derived sources, restructuring regional supply portfolios and inviting new entrants backed by mineral-rich deposits.

Manufacturers are funneling capital toward purpose-built calcination and grinding plants capable of ultraprecise particle-size control, raising pozzolanic reactivity indexes above 800 mg Ca(OH)2/g and drawing premium pricing. Silica fume and high-reactivity metakaolin maintain niche roles in ultra-high-performance concrete, while limestone filler underpins the global rollout of Portland Limestone Cement, reinforcing incremental de-clinkerization pathways. Collectively, these trends signal a pivot from opportunistic use of industrial waste toward deliberate, scalable supplementary cementitious materials market production strategies.

The Supplementary Cementitious Materials Report is Segmented by SCM Type (Fly Ash, Slag Cement, Silica Fume, and More), End User (Residential Construction, Commercial and Institutional, Industrial Facilities, and More), Material Form (Powder, Slurry/Suspension, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

The Asia-Pacific region remains the epicenter of the supplementary cementitious materials market, capturing 47.88% of the 2025 value, driven by China's continued but moderating construction activities and India's surge in infrastructure expenditure to USD 36.1 billion during 2023-24. Ready access to coal ash and blast-furnace slag once underpinned low-cost supplies; however, environmental policies are accelerating coal retirements, prompting regional cement majors to prioritize calcined-clay hubs near kaolinite-rich deposits. ASEAN economies are leveraging Belt and Road funding to build transport corridors that require high-SCM concrete volumes, while Japan and South Korea are deploying premium metakaolin blends in seismic-resistant and marine infrastructure.

The Middle East & Africa is projected to post the fastest 6.42% CAGR through 2031, underwritten by Saudi Arabia's NEOM, the Red Sea Project, and regional mandates for low-carbon materials. UAE's Estidama and Egypt's green-building codes codify SCM thresholds, attracting investment in volcanic-ash processing in East Africa and calcined-clay projects throughout the Sahel. Logistics hurdles and quality assurance gaps impede immediate scale-up; however, mineral abundance positions the region for self-sufficiency once the processing infrastructure matures. North America faces a tightening fly-ash pipeline after 60% coal-generation decline, driving exploration of natural pozzolan sources in Nevada and Utah, alongside increased slag imports from Europe. Federal Buy Clean rules and state-level tax credits reward early adopters of high-SCM mixes, keeping demand buoyant despite supply friction. Europe, with mature carbon-pricing and RE2020 building codes, pushes technical boundaries by integrating limestone-calcined clay and recycled fines at industrial scale, cementing its role as a decarbonization laboratory. South America, though smaller, gains momentum as Brazil's coastal resilience projects and Chile's mining infrastructure demand durable, low-carbon concrete, stimulating regional pozzolan and rice-husk ash ventures that gradually connect into global supply chains.

- Advanced Cement Technologies LLC

- ArcelorMittal SA

- Bharathi Cement Corporation Private Limited

- BASF SE

- Boral Ltd.

- CEMEX S.A.B. de C.V.

- CemGreen ApS

- Charah Solutions

- CR Minerals Company LLC

- Dangote Cement Plc.

- Ecocem

- Ferroglobe PLC

- HeidelberCement

- Hoffmann Green Cement Technologies

- Holcim Group

- JSW Cement Ltd.

- Tata Steel Ltd.

- TITAN

- UltraTech Cement Ltd.

- Votorantim Cimentos

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Boom in global construction and infrastructure spending

- 4.2.2 Stricter CO2-emissions regulations and carbon-pricing schemes

- 4.2.3 Rapid adoption of blended/green cements (e.g., PLC)

- 4.2.4 Government green-procurement incentives

- 4.2.5 Surging projects in calcined clay and natural pozzolans unlocking new supply

- 4.3 Market Restraints

- 4.3.1 Dwindling supply of quality fly ash and slag as coal and BF steel decline

- 4.3.2 High variability in SCM quality/specifications

- 4.3.3 Competition from novel low-clinker binders that bypass traditional SCM chains

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By SCM Type

- 5.1.1 Fly Ash

- 5.1.2 Slag Cement (Ground-granulated Blast-Furnace Slag)

- 5.1.3 Silica Fume

- 5.1.4 Calcined Clay / Metakaolin

- 5.1.5 Limestone Filler

- 5.1.6 Other Products

- 5.2 By End User

- 5.2.1 Residential Construction

- 5.2.2 Commercial and Institutional

- 5.2.3 Industrial Facilities

- 5.2.4 Transport Infrastructure (roads, rail, ports, airports)

- 5.2.5 Energy and Utilities Infrastructure

- 5.3 By Material Form

- 5.3.1 Powder

- 5.3.2 Slurry/Suspension

- 5.3.3 Granulated Pellets

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Nordic Countries

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Advanced Cement Technologies LLC

- 6.4.2 ArcelorMittal SA

- 6.4.3 Bharathi Cement Corporation Private Limited

- 6.4.4 BASF SE

- 6.4.5 Boral Ltd.

- 6.4.6 CEMEX S.A.B. de C.V.

- 6.4.7 CemGreen ApS

- 6.4.8 Charah Solutions

- 6.4.9 CR Minerals Company LLC

- 6.4.10 Dangote Cement Plc.

- 6.4.11 Ecocem

- 6.4.12 Ferroglobe PLC

- 6.4.13 HeidelberCement

- 6.4.14 Hoffmann Green Cement Technologies

- 6.4.15 Holcim Group

- 6.4.16 JSW Cement Ltd.

- 6.4.17 Tata Steel Ltd.

- 6.4.18 TITAN

- 6.4.19 UltraTech Cement Ltd.

- 6.4.20 Votorantim Cimentos

7 Market Opportunities & Future Outlook

- 7.1 White-space and Unmet-need Assessment