|

市场调查报告书

商品编码

1934840

欧洲纸业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Europe Paper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

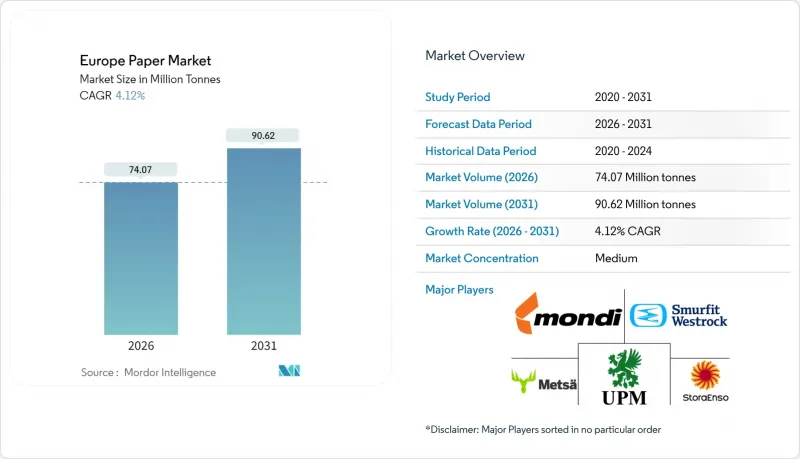

预计到 2026 年,欧洲纸张市场规模将达到 7,407 万吨,高于 2025 年的 7,114 万吨。

预计到 2031 年产量将达到 9,062 万吨,2026 年至 2031 年的复合年增长率为 4.12%。

儘管能源成本面临通膨压力,且印刷用纸逐渐被数位化替代,但欧洲纸张市场仍在持续扩张,这主要得益于严格的循环经济法规、电子商务包装需求的增长以及疫情后纸巾消费量增加。再生纤维的加速应用降低了原料采购风险,并加强了该地区为确保资源主权而采取的策略性措施。同时,大型垂直整合企业正将其印刷用纸产能转向利润更高的包装用纸,以维持盈利。在供应方面,瑞典木浆价格在2024年上涨30%,持续造成供应紧张,促使筹资策略更加重视长期合约和原物料来源多元化。

欧洲纸张市场趋势与分析

扩大永续包装材料的使用

欧盟第2025/40号法规规定的强制回收目标要求,到2030年,欧盟境内销售的所有包装都必须回收利用,这促使品牌所有者对纤维基包装的需求急剧转向纤维基包装。 Mondi公司87%的收入来自可重复使用、可回收和可堆肥的解决方案,这表明合规性如何转化为溢价价值提案。儘管宏观经济环境疲软,瓦楞纸包装加工商仍面临订单,这表明永续性在其采购标准中比成本更为重要。更多资金正转向用于餐饮服务的模塑纤维托盘,这些托盘受益于各成员国的塑胶禁令。随着原始设备製造商(OEM)竞相获得低碳认证,工厂可追溯性和再生材料含量的认证正成为获得零售货架空间的关键因素。

电子商务和餐饮业的需求不断增长

线上零售每笔交易使用的瓦楞纸板数量是实体零售的三倍之多,推动了欧洲纸张市场吨位结构性成长。同时,外带和配送需求的成长也带动了对防油防潮包装的需求。纸张生产商正积极回应,安装按需柔版印刷和喷墨印刷生产线,以经济高效的方式客製化小批量生产,从而降低电商的库存风险。都市区的微型仓配中心正在采用简化的折迭纸箱设计,以提高拣货和包装效率并减少空箱率。这些通路共同抵消了传统商业印刷需求的下降,并凸显了包装在欧洲纸张市场韧性中发挥的稳定作用。

木浆和再生纸价格波动

预计到2024年,瑞典原木成本将上涨30%,这挤压了造纸厂的利润空间,并暴露了非一体化生产商在商品价格波动面前的脆弱性。地缘政治因素限制了俄罗斯和白俄罗斯纤维的进口,导致本地供应来源紧张,迫使造纸厂签订多年销售合约或直接收购林业资产。由于司机短缺和柴油价格上涨,再生纸的收集成本也随之上升,削弱了其相对于原生纸浆的价格优势。垂直一体化如今已成为重要的对冲工具,斯道拉恩索公司透过出售部分林业资产并签订长期特许经营协议来抵销价格波动,便是一个例证。由于商品化纸浆的定价能力有限,中小型独立生产商在价格飙升期间面临现金流风险,凸显了原物料价格波动是其面临的最严峻的营运挑战之一。

细分市场分析

至2025年,纸箱材料将占欧洲纸张市场份额的33.78%,成为支撑电子商务、食品和工业供应链的包装基础。瓦楞纸箱的生产吸引了印刷厂向下游转移,无需前置作业时间工厂即可增加低成本产能。生产商正利用轻量化技术降低纸张重量,同时保持承重强度,并努力符合零售商的永续性评估标准。特种纸虽然小规模,到2025年仅892万吨,但其复合年增长率将达到5.95%,主要成长动力来自食品阻隔涂层、安全基材和电子产品用技术层压材料。这些细分市场为大型综合製造商提供了极具吸引力的多元化策略,因为更高的价格可以抵消配方成本和相容性测试费用的增加。

儘管印刷用纸持续面临结构性挑战,但高端杂誌和艺术书籍对触感的需求依然旺盛,超越了数位萤幕的局限,维持着一个虽已萎缩但仍具活力的细分市场。卫生和家庭用纸则受益于需求的防御性以及人们卫生意识的持续提高。包装纸和纸板正受益于零售商禁用塑胶袋和全通路零售包装的重新设计。展望未来,诸如用于包装材料的水性柔版印刷等工业印刷创新将带来新的增值收入来源,并巩固包装材料在欧洲纸张市场的核心地位。

到2025年,再生纤维将占欧洲纸张市场总量的52.64%,巩固了该地区在闭合迴路材料循环利用领域的主导地位。在生产者延伸责任制的支持下,欧洲的回收系统使得其回收率高于大多数其他地区。随着生态设计标准的不断发展,加工商正在重新设计脱墨包装和纤维保留工艺,从而加强了再生纤维的流通。在对感官纯净度和抗撕裂性要求极高的优质包装领域,原生纤维的使用量将以4.34%的复合年增长率快速增长。综合林业公司正利用其经认证的林业资产为这些细分市场提供原材料,并越来越多地将原生纸浆与其他领域中再生纤维的使用相结合,以实现整体永续性目标。

儘管农业残余纤维仍处于起步阶段,但由于小麦秸秆和芒草製浆的试点计画旨在分散采购风险并降低碳排放强度,它们正日益受到关注。欧洲大陆政策中加强的林业可追溯性要求进一步提升了再生纤维和替代纤维的相对吸引力。同时,造纸厂的酵素脱墨试验在提高再生纤维的白度方面取得了令人鼓舞的成果,拓展了其在高檔白纸中的应用范围,并强化了支撑欧洲纸张市场的循环经济模式。

欧洲纸张市场报告按产品类型(印刷用纸、纸箱材料、卫生及家庭用纸、包装用纸、纸板、特种纸)、原材料来源(原生纤维、再生纤维、农业废弃物纤维)、纸张重量(低于和高于90克/平方米)、终端用户行业(包装和工业等)以及地区(德国等)进行划分。市场预测以吨为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 扩大永续包装材料的使用

- 电子商务和餐饮服务业的需求不断增长

- 欧盟循环经济指令对纺织品包装的要求

- 新冠疫情后卫生纸消耗量增加

- 3D模塑纤维包装的商业化

- 推出按需喷墨瓦楞纸印刷服务

- 市场限制

- 木浆和再生纸价格波动

- 用数位媒体代替绘图纸

- 能源和碳信用价格上涨

- 对造纸厂用水量製定更严格的规定

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 图纸

- 报纸纸张

- 其他绘图纸

- 案例材料

- 卫生用品/家居用品

- 包装材料

- 纸板

- 特製纸张

- 图纸

- 按原料来源

- 原生纤维

- 再生纤维

- 农业残余纤维

- 按纸张重量

- 小于90克/平方公尺(轻质)

- 90-200克/平方公尺(中等重量)

- 200公克/平方公尺或以上(重磅)

- 按最终用途行业划分

- 包装/工业

- 印刷/出版

- 卫生和清洁

- 食品服务抛弃式

- 其他终端用户产业

- 按国家/地区

- 德国

- 法国

- 瑞典

- 义大利

- 西班牙

- 其他欧洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Stora Enso Group

- UPM-Kymmene Corporation

- Smurfit Westrock plc

- Mondi plc

- Metsa Group

- Holmen AB

- Svenska Cellulosa Aktiebolaget SCA

- Mayr-Melnhof Karton AG

- PRINZHORN HOLDING GmbH

- Norske Skog ASA

- Burgo Group SpA

- Lecta Group

- Reno de Medici SpA

- Sappi Limited

- Grigeo AB

- Iberpapel Gestion SA

- Heinzel Group

- Fedrigoni SpA

- Arctic Paper SA

第七章 市场机会与未来展望

Europe paper market size in 2026 is estimated at 74.07 million tonnes, growing from 2025 value of 71.14 million tonnes with 2031 projections showing 90.62 million tonnes, growing at 4.12% CAGR over 2026-2031.

Despite inflationary energy costs and digital substitution in graphic grades, the Europe paper market continues to expand on the back of strict circular-economy regulation, e-commerce packaging demand, and a post-pandemic rise in tissue consumption. Accelerated adoption of recycled fiber keeps material input risk in check and reinforces the bloc's strategic push for resource sovereignty. Meanwhile, vertically integrated leaders redirect graphic capacity toward higher-margin packaging grades to defend profitability. Supply-side dynamics remain tight as wood-pulp prices in Sweden jumped 30% in 2024, prompting procurement strategies that favor long-term contracts and diversified fiber sourcing.

Europe Paper Market Trends and Insights

Growth in Use of Sustainable Packaging

Mandatory recyclability targets under Regulation 2025/40 require all packaging sold in the bloc to be recyclable by 2030, pushing brand-owner demand sharply toward fiber-based formats. Mondi already derives 87% of revenue from reusable, recyclable, or compostable solutions, signalling how compliance has turned into a premium-priced value proposition. Corrugated converters report order backlogs even in a sluggish macro environment, indicating that sustainability now outweighs cost in purchasing criteria. Incremental capital has shifted toward molded-fiber trays for food service, a segment benefiting from plastic bans across member states. As OEMs scramble for low-carbon credentials, mill certifications around traceability and recycled content serve as gatekeepers to retail shelf space.

Expansion of E-commerce and Food-service Demand

Online retail requires up to three times more corrugated volume per transaction than store-based sales, adding structural tonnage growth to the Europe paper market. Parallel growth in takeaway and delivery meals inflates demand for grease- and moisture-resistant wraps. Mills have responded by installing on-demand flexo and ink-jet lines that cost-effectively customise small batches, lowering inventory risk for e-tailers. Urban micro-fulfilment hubs now specify easy-fold case designs that improve pick-pack efficiency and reduce void space. Together, these channels offset soft demand in legacy commercial print, underscoring packaging's role as the ballast of Europe paper market resilience.

Volatile Wood-Pulp and Recovered Paper Prices

Swedish roundwood cost inflation of 30% in 2024 eroded mill margins and exposed the vulnerability of non-integrated producers to commodity swings. Geopolitical constraints on Russian and Belarusian fiber imports have tightened the regional supply pool, pushing mills to secure multiyear offtake contracts or acquire forest assets outright. Recovered paper collection costs also escalated due to driver shortages and higher diesel prices, narrowing the price advantage versus virgin pulp. Vertical integration now confers a decisive hedge, illustrated by Stora Enso's partial forest divestiture balanced by long-term stumpage agreements. Without pricing power in commoditized grades, smaller independents risk negative cash flow during spikes, underscoring raw-material volatility as the most acute operational headwind.

Other drivers and restraints analyzed in the detailed report include:

- EU Circular-Economy Mandates on Fiber Packaging

- Rising Hygiene-Paper Consumption Post-COVID

- Digital Media Substitution of Graphic Papers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Case Materials represented 33.78% of Europe paper market share in 2025, underpinning the packaging backbone that services e-commerce, food, and industrial supply chains. Corrugated case grades captured downstream migration from graphic mills, adding low-cost capacity without green-field lead times. Producers leveraged lightweighting technology to cut grammage while maintaining stacking strength, aligning with retailer sustainability scorecards. Specialty Papers, though just 8.92 million tonnes in 2025, deliver a 5.95% CAGR, buoyed by food-grade barrier coatings, security substrates, and technical laminates for electronics. These niches command price premiums that offset higher formulation costs and compliance testing, making them an attractive diversification play for large integrated houses.

The structural headwinds facing Graphic Papers remain unabated; nonetheless, premium magazines and art books continue to demand tactile quality beyond digital screens, preserving a viable albeit shrinking niche. Sanitary and Household papers benefit from defensive demand characteristics and ongoing hygiene awareness. Wrappings and Carton Board capitalise on retailer plastic-bag bans and omnichannel retail packaging redesigns. Looking ahead, industrial printing innovation such as water-based flexo for Case Materials introduces new value-added revenue streams, cementing the central role of Case Materials in the Europe paper market.

Recycled Fiber accounted for 52.64% of Europe paper market size in 2025, confirming the region's leadership in closed-loop material flows. Collection systems supported by Extended Producer Responsibility schemes achieve recovery rates that outpace most other regions. As eco-design criteria evolve, converters redesign packaging for de-inkability and fiber retention, reinforcing recycled fiber throughput. Virgin Fiber usage posts the fastest 4.34% CAGR, owing to premium packaging where organoleptic purity and tear resistance are non-negotiable. Integrated forest companies exploit certified forestry assets to supply these segments, often pairing primary pulp with increased recycled content elsewhere to meet overall sustainability targets.

Agro-Residue Fiber remains nascent but garners interest as mills pilot wheat-straw and miscanthus pulping to diversify procurement risk and lower carbon intensity. Continental policy that tightens deforestation traceability requirements further elevates recycled and alternative fibers' relative attractiveness. Meanwhile, mill trials on enzymatic de-inking show promise in lifting recycled-fiber brightness, expanding its applicability in premium white grades, and bolstering the circular narrative that underpins the Europe paper market.

The Europe Paper Market Report is Segmented by Product Type (Graphic Papers, Case Materials, Sanitary and Household, Wrappings, Carton Board, and Specialty Papers), Raw-Material Source (Virgin Fiber, Recycled Fiber, and Agro-Residue Fiber), Basis-Weight (Below 90 Gsm, and More), End-Use Industry (Packaging and Industrial, and More), and Geography (Germany, and More). The Market Forecasts are Provided in Terms of Volume (Tonnes).

List of Companies Covered in this Report:

- Stora Enso Group

- UPM-Kymmene Corporation

- Smurfit Westrock plc

- Mondi plc

- Metsa Group

- Holmen AB

- Svenska Cellulosa Aktiebolaget SCA

- Mayr-Melnhof Karton AG

- PRINZHORN HOLDING GmbH

- Norske Skog ASA

- Burgo Group S.p.A

- Lecta Group

- Reno de Medici S.p.A

- Sappi Limited

- Grigeo AB

- Iberpapel Gestion S.A

- Heinzel Group

- Fedrigoni SpA

- Arctic Paper S.A

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Use of Sustainable Packaging

- 4.2.2 Expansion of E-commerce and Food-service Demand

- 4.2.3 EU Circular-Economy Mandates on Fiber Packaging

- 4.2.4 Rising Hygiene-Paper Consumption Post-COVID

- 4.2.5 Commercialisation of 3-D Molded-Fiber Packaging

- 4.2.6 On-demand Ink-jet Corrugated Printing Adoption

- 4.3 Market Restraints

- 4.3.1 Volatile Wood-Pulp and Recovered Paper Prices

- 4.3.2 Digital Media Substitution of Graphic Papers

- 4.3.3 Energy and Carbon-credit Price Inflation

- 4.3.4 Tighter Water-Use Regulations for Mills

- 4.4 Industry Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VOLUME)

- 5.1 By Product Type

- 5.1.1 Graphic Papers

- 5.1.1.1 Newsprint

- 5.1.1.2 Other Graphic Papers

- 5.1.2 Case Materials

- 5.1.3 Sanitary and Household

- 5.1.4 Wrappings

- 5.1.5 Carton Board

- 5.1.6 Specialty Papers

- 5.1.1 Graphic Papers

- 5.2 By Raw-Material Source

- 5.2.1 Virgin Fiber

- 5.2.2 Recycled Fiber

- 5.2.3 Agro-Residue Fiber

- 5.3 By Basis-Weight

- 5.3.1 Below 90 gsm (Lightweight)

- 5.3.2 90-200 gsm (Mediumweight)

- 5.3.3 Above 200 gsm (Heavyweight)

- 5.4 By End-use Industry

- 5.4.1 Packaging and Industrial

- 5.4.2 Printing and Publishing

- 5.4.3 Hygiene and Sanitary

- 5.4.4 Food-service Disposables

- 5.4.5 Other End-use Industries

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 France

- 5.5.3 Sweden

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Stora Enso Group

- 6.4.2 UPM-Kymmene Corporation

- 6.4.3 Smurfit Westrock plc

- 6.4.4 Mondi plc

- 6.4.5 Metsa Group

- 6.4.6 Holmen AB

- 6.4.7 Svenska Cellulosa Aktiebolaget SCA

- 6.4.8 Mayr-Melnhof Karton AG

- 6.4.9 PRINZHORN HOLDING GmbH

- 6.4.10 Norske Skog ASA

- 6.4.11 Burgo Group S.p.A

- 6.4.12 Lecta Group

- 6.4.13 Reno de Medici S.p.A

- 6.4.14 Sappi Limited

- 6.4.15 Grigeo AB

- 6.4.16 Iberpapel Gestion S.A

- 6.4.17 Heinzel Group

- 6.4.18 Fedrigoni SpA

- 6.4.19 Arctic Paper S.A

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

香蕉纸市场:2026-2032年全球市场预测(依产品类型、製造流程、应用、终端用户产业及通路划分)无涂布机械用纸市场:2026-2032年全球市场预测(依产品类型、製程、纺织原料、等级、销售管道及最终用途划分)贴纸市场:按产品类型、黏合剂类型、印刷技术、应用和终端用户产业划分-2026-2032年全球市场预测

香蕉纸市场:2026-2032年全球市场预测(依产品类型、製造流程、应用、终端用户产业及通路划分)无涂布机械用纸市场:2026-2032年全球市场预测(依产品类型、製程、纺织原料、等级、销售管道及最终用途划分)贴纸市场:按产品类型、黏合剂类型、印刷技术、应用和终端用户产业划分-2026-2032年全球市场预测 涂布机械纸捲市场规模、份额和成长分析:按涂布、纸张类型、表面处理/光泽度、最终用途和地区划分-2026-2033年产业预测咖啡滤纸市场:依材质、形状、产品类型、尺寸、相容性、通路和最终用途划分-全球预测,2026-2032年

涂布机械纸捲市场规模、份额和成长分析:按涂布、纸张类型、表面处理/光泽度、最终用途和地区划分-2026-2033年产业预测咖啡滤纸市场:依材质、形状、产品类型、尺寸、相容性、通路和最终用途划分-全球预测,2026-2032年 2026年全球纸张、塑胶、橡胶、木材和纺织品市场报告全球气流成网纸市场:按应用、产品类型、纸张重量、纤维成分和分销管道划分 - 2026-2032 年预测全球素色装饰纸市场(按产品类型、材料类型、应用和分销管道划分)预测(2026-2032年)可降解气流成网网纸市场:依产品类型、通路、最终用途产业、堆肥水准、纸张重量等级及应用划分-2026年至2032年全球预测按产品类型、材料类型、包装类型、纸张重量、应用、最终用途和分销管道气流成网产品市场-2026年至2032年全球预测

2026年全球纸张、塑胶、橡胶、木材和纺织品市场报告全球气流成网纸市场:按应用、产品类型、纸张重量、纤维成分和分销管道划分 - 2026-2032 年预测全球素色装饰纸市场(按产品类型、材料类型、应用和分销管道划分)预测(2026-2032年)可降解气流成网网纸市场:依产品类型、通路、最终用途产业、堆肥水准、纸张重量等级及应用划分-2026年至2032年全球预测按产品类型、材料类型、包装类型、纸张重量、应用、最终用途和分销管道气流成网产品市场-2026年至2032年全球预测