|

市场调查报告书

商品编码

1934850

表面处理化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Surface Treatment Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

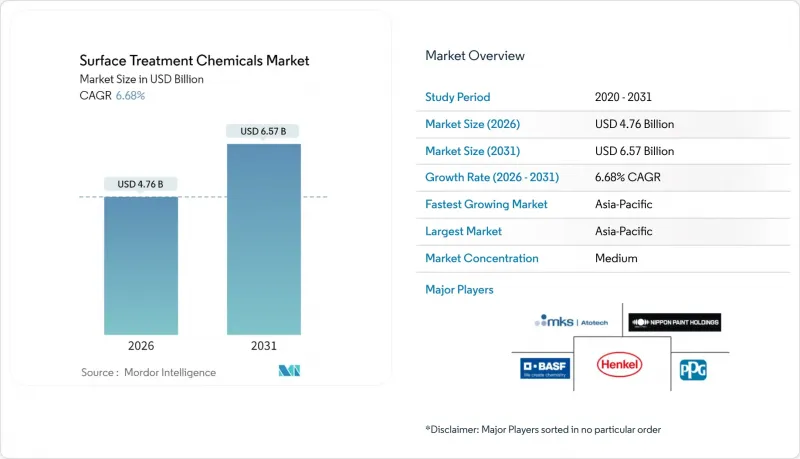

预计到 2026 年,表面处理化学品市场规模将达到 47.6 亿美元,高于 2025 年的 44.6 亿美元。

预计到 2031 年将达到 65.7 亿美元,2026 年至 2031 年的复合年增长率为 6.68%。

汽车电气化、半导体封装回收以及需要耐腐蚀系统的离岸风力发电电专案正在推动强劲的成长势头。儘管亚洲製造地占据了新增产能的大部分,但北美生产回收计画和欧洲永续性法规正在引导高端需求转向高性能、无铬配方。随着传统金属表面处理化学品的重要性下降,那些能够将半导体级纯度、多金属相容性和生物基创新相结合的供应商正在占据不断扩大的价值市场。由于对六价铬的限制日益严格,表面处理化学品市场正受益于监管趋同,这迫使终端用户采用符合严格职业健康和环境标准的替代涂料和清洁剂。

全球表面处理化学品市场趋势与洞察

亚洲汽车製造业快速扩张

亚洲汽车製造商正在扩展多材料车身结构,这些结构依赖能够防止铝和钢之间交叉污染的清洁剂。电动车电池外壳、结构铸件和温度控管板需要精密蚀刻和转化涂层,这些涂层能够承受混合合金的腐蚀,同时防止电流腐蚀。 Element Solutions公司报告称,其电子业务部门2024年第一季的销售额增长了10%,达到3.94亿美元,这表明汽车电气化正在推动对半导体级化学品的需求。然而,区域整合也带来了集中风险。中国对镓和锗的出口限制正在扰乱用于牵引逆变器的功率装置的电镀供应。在亚洲拥有多元化布局和原材料来源的供应商可以降低这些风险,同时利用持续的产量成长。

电子元件小型化需要高精度电镀。

半导体封装材料销售额在经历了2023年的下滑后,预计在2025年达到260亿美元,这主要得益于先进基板运转率的回升。覆晶和晶圆级封装对电解镍、浸金和无氧化物清洁剂的厚度公差要求为±1微米。杜邦公司在日本扩大其光阻剂业务,以及住友化学公司设定的到2030年晶片材料销售额达到3,000亿日圆的目标,都凸显了市场对超高纯度製程化学品日益增长的需求。一些能够提供低缺陷、高选择性配方的供应商正在涌现,以取代那些无法将微量污染物控制在万亿阈值之一以下的传统金属表面处理商。过高的资本密集度和严格的无尘室通讯协定提高了进入门槛,使得合格的供应商能够获得溢价,从而实现两位数的利润率。

对六价铬的监管更加严格

欧盟、加州和英国将于2024年同时实施六价铬禁令,预计将为整个供应链带来3.31亿美元至10.7亿美元的累积监管成本。替代方案包括三价铬、物理气相沉积溅镀和氮化钛陶瓷密封剂。航太主要製造商对替代技术实施多年的认证週期,导致电镀厂需要维修生产线,加剧了近期产能紧张。由于航空安全法规限制零件通过适航检验后更换供应商,早期采用氟锆酸盐或钼酸盐密封剂的厂商已获得独家供应地位。中小型合约加工厂面临资金壁垒,这可能会加速市场整合。

细分市场分析

到2025年,转化涂层将占表面处理化学品市场收入的42.39%,其中汽车、航太和通用工业涂料生产线将占据市场主导地位。受半导体封装工厂和增材製造中心对超低残留清洗液的需求推动,清洁剂预计将以6.77%的复合年增长率快速成长。这种差异体现了一种两极化:通用磷酸盐基转化製程需求旺盛但利润率较低,而精密清洗剂由于其纯度和选择性标准而保持高价。监管机构正在推动向锆钛体系的转变,该体係可减少污泥和能源消耗,这进一步凸显了拥有强大配方智慧财产权(IP)的供应商的优势。专业製造商利用捆绑式清洗和转换流程来确保多年工厂审核合约并降低客户流失。

用于铝电池机壳的第二代阳极氧化添加剂可在提高耐磨性的同时保持良好的焊接性能。其他类型的添加剂,例如生物基密封剂和无铬混合涂层,则满足医疗设备和风力发电机叶片等特定应用的需求。随着原始设备製造商 (OEM) 在全球范围内推行材料规格标准化,能够提供跨洲一致化学配方的供应商正在赢得主服务协议。因此,表面处理化学品市场的竞争焦点正从每公升价格转向生命週期成本,研发预算也逐渐转向旨在延长镀液寿命、控制发泡和提高污水处理性能的添加剂组合。

表面处理化学品报告按化学品类型(清洁剂、化学转化膜等)、基材(金属、塑胶、其他材料)、终端用户产业(汽车、建筑、电子、工业机械、其他)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以美元以金额为准。

区域分析

至2025年,亚太地区将占表面处理化学品市场收入的42.88%,并在2031年之前以7.05%的复合年增长率成长。在中国,随着国内经济奖励策略提振电动车(EV)供应链,预计化学品製造商的利润将在2025年復苏。印度的特种化学品销售额预计在2025年将达到3,000亿美元,这将支撑智慧型手机组装和汽车出口对高价值涂料的需求。

在北美,1.2兆美元的《基础设施投资和就业创造法案》正在加强工业基础,以支撑对重型设备和桥樑涂料的需求。亚利桑那州、德克萨斯州和纽约州的半导体工厂正在推动符合一级无尘室标准的超纯清洁化学品的本地消费。加拿大不断扩大的离岸风力发电供应链将进一步提升对ISO 20340认证涂料的需求。虽然北美地区的成长速度不如亚洲,但严格的环境法规以及接近性研发丛集的优势,创造了高价值的获利机会。

欧洲在海洋能源和航太领域保持技术领先地位。 2025年实施的NORSOK M-501 Rev 7标准要求涂料必须检验,能够承受长期浸泡和火灾环境。绿色交易协议促进了生物基化学的发展。德国和斯堪地那维亚国家对木质素基树脂提供补贴,并加速淘汰溶剂型铬酸盐。南美洲、中东和非洲的发展速度各不相同。巴西的盐层下油田需要高温腐蚀抑制剂,而波湾合作理事会国家正在投资建造与汽车出口走廊相关的铝材轧延厂。儘管总产量仍然不高,但当地的生产要求正迫使跨国供应商建立服务中心,以利用先发优势,加速工业化进程。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 亚洲汽车製造业快速扩张

- 电子元件小型化需要高精度电镀。

- 风力发电机塔架的严格防腐蚀标准

- 原位3D列印金属零件(需列印后表面处理)

- 电动车平台中铝材用量的快速成长需要多金属清洗机

- 市场限制

- 对六价铬的监管更加严格

- 向生物基涂料的转变将降低对传统化学品的需求。

- 自建金属精加工生产线的总拥有成本不断增加

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依化学类型

- 清洁工

- 化学转换涂层

- 阳极处理化学品

- 其他化学品

- 按基础材料

- 金属

- 塑胶

- 其他基材(玻璃、合金、木材)

- 按最终用户行业划分

- 汽车和运输设备

- 建造

- 电子设备

- 工业机械

- 其他(石油和天然气管道、发电、军事、包装等)

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Aalberts Surface Technologies GmbH

- ALANOD GmbH and Co. KG

- Asterion LLC

- BASF

- Bulk Chemicals Inc.

- ChemTech Surface Finishing Pvt. Ltd.

- Dow

- Element Solutions Inc

- Henkel AG and Co. KGaA

- MKS|Atotech

- Nihon Parkerizing Co., Ltd.

- Nippon Paint Holdings Co. Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- Quaker Chemical Corporation

- The Sherwin-Williams Company

- YUKEN INDUSTRY CO.,LTD.

第七章 市场机会与未来展望

Surface Treatment Chemicals Market size in 2026 is estimated at USD 4.76 billion, growing from 2025 value of USD 4.46 billion with 2031 projections showing USD 6.57 billion, growing at 6.68% CAGR over 2026-2031.

Strong momentum flows from automotive electrification, semiconductor packaging recovery, and offshore wind installations that demand corrosion-resistant systems. Asian manufacturing hubs account for most new capacity, while North American reshoring programs and European sustainability mandates redirect premium demand toward high-performance, chromium-free formulations. Suppliers that combine semiconductor-grade purity, multi-metal compatibility, and bio-based innovation capture rising value pools as legacy metal-finishing chemistries lose relevance. The surface treatment chemicals market benefits from regulatory convergence that penalizes hexavalent chromium, forcing end-users to adopt alternative coatings and cleaners that comply with strict occupational health and environmental limits.

Global Surface Treatment Chemicals Market Trends and Insights

Rapid Expansion of Automotive Production in Asia

Asia's automakers are scaling multi-material vehicle architectures that depend on cleaners able to prevent cross-contamination between aluminum and steel. Electric-vehicle battery housings, structural castings, and heat-management plates require precision etching and conversion coatings that tolerate mixed alloys without galvanic corrosion. Element Solutions recorded 10% electronics-segment sales growth to USD 394 million in Q1 2024, illustrating how automotive electrification lifts semiconductor-grade chemical volumes. Regional consolidation nonetheless concentrates risk: Chinese export controls on gallium and germanium disrupt plating supply for power-devices embedded in traction inverters. Suppliers with diversified Asian footprints and redundant raw-material sources mitigate these vulnerabilities while capitalizing on sustained output gains.

Electronics Miniaturisation Demanding High-Precision Plating

Semiconductor packaging materials revenues are forecast to climb to USD 26 billion in 2025 after a 2023 downturn, restoring capacity utilization across advanced substrate lines. Flip-chip and wafer-level packages impose +-1 µm thickness tolerances on electroless nickel, immersion gold, and oxide-free cleaners. DuPont's photoresist expansion in Japan and Sumitomo Chemical's JPY 300 billion chip-materials sales goal by 2030 underscore the pull for ultra-pure treatment chemicals. Suppliers that deliver low-defect, high-selectivity formulations displace traditional metal finishers whose processes cannot control trace contaminants below parts-per-trillion thresholds. Outsized capital intensity and strict cleanroom protocols raise barriers, enabling premium pricing that supports double-digit contribution margins for qualified vendors.

Regulatory Clamp-Down on Hexavalent Chromium

The European Union, California, and the United Kingdom enacted parallel bans on hexavalent chromium during 2024, triggering cumulative compliance outlays estimated between USD 331 million and USD 1.07 billion across the supply chain. Transition pathways include trivalent chromium, PVD sputtering, and ceramic titanium-nitride sealers. Aerospace primes impose multiyear qualification cycles for alternatives, tightening near-term capacity as plating shops retrofit lines. Early adopters of fluorozirconate or molybdate sealing chemistries secure sole-source positions because flight-safety regulations discourage supplier substitutions once parts pass airworthiness validation. Smaller job shops face capital barriers that may accelerate market consolidation.

Other drivers and restraints analyzed in the detailed report include:

- Stringent Anti-Corrosion Standards in Wind-Turbine Towers

- On-Site 3D-Printed Metal Parts Requiring Post-Print Surface Prep

- Shift Toward Bio-Based Coatings Reduces Legacy Chemical Demand

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conversion coatings generated 42.39% of 2025 revenue within the surface treatment chemicals market, anchored by automotive, aerospace, and general-industrial paint lines. Cleaners are projected to post the fastest 6.77% CAGR as semiconductor packaging plants and additive-manufacturing hubs demand ultra-low residue baths. This divergence signals a bifurcation: commodity phosphate-based conversions attract volume but modest margins, whereas precision cleaners command high price points due to purity and selectivity thresholds. Regulators are driving a shift to zirconium and titanium systems that lower sludge and energy usage, further differentiating suppliers that possess strong formulation IP. Specialty players leverage bundled cleaner-conversion packages to lock in multi-year plant audits, limiting churn.

Second-generation anodizing additives for aluminum battery enclosures strengthen wear resistance while maintaining weldability. Other types, including bio-derived sealers and chromium-free hybrid films, address niche specifications in medical instruments and wind-turbine blades. As OEMs standardize global material specifications, suppliers that offer consistent chemistries across continents win master-service agreements. Consequently, the surface treatment chemicals market sees a migration of research budgets toward additive packages that improve bath longevity, foaming control, and wastewater treatability, intensifying competition on lifecycle cost rather than per-liter pricing.

The Surface Treatment Chemicals Report is Segmented by Chemical Type (Cleaner, Chemical Conversion Coating, and More), Base Material (Metal, Plastic and Other Materials), End-User Industry (Automotive, Construction, Electronics, Industrial Machinery, and Others), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 42.88% of 2025 revenue within the surface treatment chemicals market and is expanding at a 7.05% CAGR to 2031. China forecasts a profit rebound for its chemical producers in 2025 amid a domestic stimulus that boosts EV supply chains. India's specialty-chemical turnover is scheduled to reach USD 300 billion in 2025, feeding demand for high-value coatings used in smart-phone assembly and automotive exports.

North America is reinforcing its industrial base through the USD 1.2 trillion Infrastructure Investment and Jobs Act, which underpins heavy-equipment and bridge-coating demand. Semiconductor fabs in Arizona, Texas, and New York fuel localized consumption of ultra-pure cleaners that meet Class 1 cleanroom thresholds. Canada's offshore wind supply-chain build-out further widens the need for ISO 20340-certified coatings. Although growth rates trail Asia, premium margin opportunities arise from tight environmental regulations and proximity to research and development clusters.

Europe retains technological leadership in offshore energy and aerospace. The implementation of NORSOK M-501 Rev 7 in 2025 demands coatings validated for long-term immersion and fire exposure. Green-deal policies advance bio-based chemistries; Germany and Scandinavia subsidize lignin-derived resins, accelerating the phase-out of solvent-borne chromates. South America and Middle East Africa are emerging at different paces: Brazil's pre-salt oilfields require high-temperature corrosion inhibitors, while Gulf Cooperation Council states invest in aluminum rolling mills linked to automotive export corridors. Although combined volumes remain modest, local production mandates push multinational suppliers to establish service hubs, unlocking early-mover advantages as industrialization accelerates.

- Aalberts Surface Technologies GmbH

- ALANOD GmbH and Co. KG

- Asterion LLC

- BASF

- Bulk Chemicals Inc.

- ChemTech Surface Finishing Pvt. Ltd.

- Dow

- Element Solutions Inc

- Henkel AG and Co. KGaA

- MKS | Atotech

- Nihon Parkerizing Co., Ltd.

- Nippon Paint Holdings Co. Ltd.

- OC Oerlikon Management AG

- PPG Industries, Inc.

- Quaker Chemical Corporation

- The Sherwin-Williams Company

- YUKEN INDUSTRY CO.,LTD.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Automotive Production in Asia

- 4.2.2 Electronics Miniaturisation Demanding High-Precision Plating

- 4.2.3 Stringent Anti-Corrosion Standards in Wind-Turbine Towers

- 4.2.4 On-Site 3D-Printed Metal Parts Requiring Post-Print Surface Prep

- 4.2.5 Surge in Aluminium Use in EV Platforms Necessitating Multi-Metal Cleaners

- 4.3 Market Restraints

- 4.3.1 Regulatory Clamp-Down on Hexavalent Chromium

- 4.3.2 Shift Toward Bio-Based Coatings Reduces Legacy Chemical Demand

- 4.3.3 Rising Total-Cost-of-Ownership of Captive Metal Finishing Lines

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Chemical Type

- 5.1.1 Cleaner

- 5.1.2 Chemical Conversion Coating

- 5.1.3 Anodizing Chemicals

- 5.1.4 Other Types of Chemicals

- 5.2 By Base Material

- 5.2.1 Metal

- 5.2.2 Plastic

- 5.2.3 Other Base Materials (Glass, Alloys, Wood)

- 5.3 By End-User Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction

- 5.3.3 Electronics

- 5.3.4 Industrial Machinery

- 5.3.5 Others (Oil and Gas Pipeline, Power, Military, Packaging, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aalberts Surface Technologies GmbH

- 6.4.2 ALANOD GmbH and Co. KG

- 6.4.3 Asterion LLC

- 6.4.4 BASF

- 6.4.5 Bulk Chemicals Inc.

- 6.4.6 ChemTech Surface Finishing Pvt. Ltd.

- 6.4.7 Dow

- 6.4.8 Element Solutions Inc

- 6.4.9 Henkel AG and Co. KGaA

- 6.4.10 MKS | Atotech

- 6.4.11 Nihon Parkerizing Co., Ltd.

- 6.4.12 Nippon Paint Holdings Co. Ltd.

- 6.4.13 OC Oerlikon Management AG

- 6.4.14 PPG Industries, Inc.

- 6.4.15 Quaker Chemical Corporation

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 YUKEN INDUSTRY CO.,LTD.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

混凝土表面处理剂市场:依处理类型、产品形式、应用方法及最终用途产业划分-2026-2032年全球市场预测

混凝土表面处理剂市场:依处理类型、产品形式、应用方法及最终用途产业划分-2026-2032年全球市场预测 表面处理市场机会、成长要素、产业趋势分析及2026-2035年预测。

表面处理市场机会、成长要素、产业趋势分析及2026-2035年预测。 2026年全球混凝土表面加固剂市场报告化学表面处理市场:按产品类型、基材、处理类型、流动类型、设备类型、应用和最终用户划分 - 全球预测 2026-2032船舶隔音材料市场按材料类型、船舶类型、应用领域、安装类型和供应来源划分-全球预测,2026-2032年

2026年全球混凝土表面加固剂市场报告化学表面处理市场:按产品类型、基材、处理类型、流动类型、设备类型、应用和最终用户划分 - 全球预测 2026-2032船舶隔音材料市场按材料类型、船舶类型、应用领域、安装类型和供应来源划分-全球预测,2026-2032年 2026-2034年全球交通运输路面材料市场规模、份额、趋势和成长分析报告全球成品生产线市场规模、份额、趋势及成长分析报告(2026-2034)

2026-2034年全球交通运输路面材料市场规模、份额、趋势和成长分析报告全球成品生产线市场规模、份额、趋势及成长分析报告(2026-2034) 全球工业低摩擦表面材料市场:预测(至2034年)-按材料类型、涂层技术、功能、应用、最终用户和地区进行分析2026年全球化学表面处理市场报告2026年全球成品生产线市场报告

全球工业低摩擦表面材料市场:预测(至2034年)-按材料类型、涂层技术、功能、应用、最终用户和地区进行分析2026年全球化学表面处理市场报告2026年全球成品生产线市场报告