|

市场调查报告书

商品编码

1934872

数控工具机:市场占有率分析、产业趋势与统计、成长预测(2026-2031)CNC Machines - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

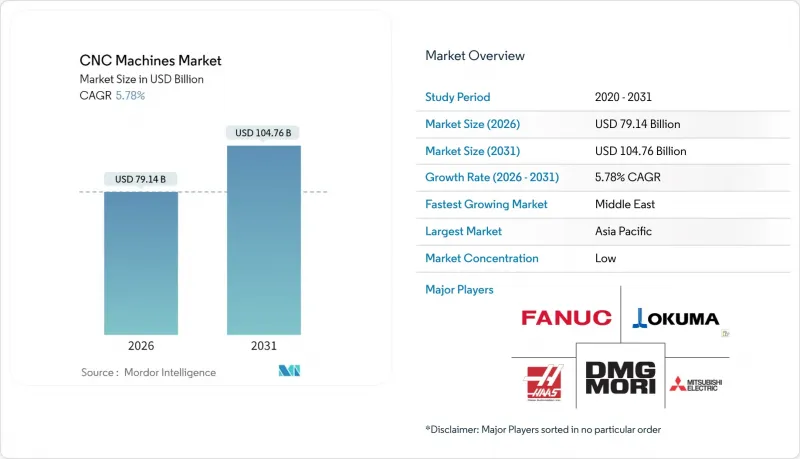

预计到 2026 年,CNC工具机市场价值将达到 791.4 亿美元,高于 2025 年的 748.2 亿美元,预计到 2031 年将达到 1,047.6 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 5.78%。

对数位化生产日益增长的需求、电动车和航太专案对公差要求的提高,以及工厂现代化改造的财政激励措施,共同推动了这一扩张。供应商正不断整合硬体、软体和预测服务,使客户能够在扩大产能的同时提高资产利用率并推迟新设备的采购。筹资策略目前优先考虑与工业5G和边缘运算平台的互通性,这可以将废品率降低高达30%,并将备件前置作业时间缩短10%。地缘政治供应链问题也促使原始设备製造商(OEM)将关键加工业务迁回国内,增强了对北美和欧盟本土设备的需求。

全球CNC工具机市场趋势与洞察

工业4.0主导的自动化升级

製造商正从孤立的工具机转向完全连网的单元式加工中心。物联网感测器将即时运作状态传输到边缘伺服器,从而减少30%的废品率和10%的备件库存。第五代无线技术消除了传统的延迟问题,为操作人员提供可靠的连接,防止程式中断。数位双胞胎技术能够在切削开始前模拟热漂移和主轴动态特性,从而将推出40%。人工智慧辅助的刀具路径代理将程式设计工作量减少50%,同时提高了表面光洁度的重复性。这些升级正在将CNC工具机从独立设备转变为自主生产循环中的节点。

汽车和航太产业对高精度产品的需求日益增长

电动汽车电池外壳、逆变器极板和电机定子如今对精度的要求已达到以往航太结构的水平,这推动了汽车工厂对五轴加工技术的应用。航太航太的加工週期缩短35%,同时维持尺寸精度。监管追溯要求进一步要求建立数位化加工日誌,以证明微米级精度。这两个行业日益增长的需求正使高精度数控加工能力成为一项基本要求,而非高级选项。

高昂的资本成本和生命週期成本

五轴加工中心整合了高精度旋转轴、线性马达和热补偿系统,使其购置成本超过50万美元,对小规模工厂来说构成了一道障碍。 Okuma估计,生命週期成本中只有15%是在购买时产生的,而85%则与维护、能源和非计画性停机有关。数位双胞胎授权和人工智慧模组也会增加企业资源规划的成本。研究表明,混合积层和减材加工单元在实现合理的投资回收期之前,需要进行全面的批量分析,尤其是在粉末成本较高的情况下。因此,高昂的拥有成本限制了它们在小批量製造商中的应用。

细分市场分析

到2025年,CNC车床将占总收入的26.95%,这印证了其在多个价值链中製造旋转零件(例如轴和衬套)的关键作用。简单的编程和刚性刀具使其能够快速换刀,从而成为一级汽车和油压设备供应商的主力设备。铣床位居第二,因为它们用于加工需要多方面精度的矩形形状。同时,雷射切割机是成长最快的细分市场,年复合成长率达8.55%,这主要得益于光纤雷射光源能够以最小的变形切割钢、铝和复合材料层压板。

Prima Power 的 Laser Next 2130 雷射切割机与西门子的 SINUMERIK ONE控制设备结合,使汽车车体线的动态响应速度提升了 20%,生产效率提高了 13%。这表明雷射加工正在取代冲压工艺,成为复杂面板加工的主流选择。电火花加工和研磨在模具和轴承製造商中仍然占据着重要的地位。积层製造和减材製造相结合的混合型工具机能够实现镍基高温合金的近净成形沉积,并在同一工作台上完成精加工,从而显着简化了一家领先的航太製造商的物流流程。这使得CNC工具机市场能够在车床需求趋于稳定的同时,实现雷射技术的快速创新。

区域分析

到2025年,亚太地区将占全球收入的46.10%,这主要得益于中国、日本和印度扩大国内产能以降低进口风险并满足国内需求。中国第一瑞沃自动化公司融资1亿元人民币(约1,390万美元)用于研发国产高端控制设备,反映了中国政府推动策略性工具机技术国产化的决心。日本则透过持续升级控制设备来巩固其高端市场地位。大隈研吾的OSP-P500将自适应加工与网路安全云端连接结合,展现了传统技术向资料驱动型服务的转型。

北美维持了第二的位置,这得益于回流补贴、航太整合以及国防需求。橡树岭国家实验室和MSC工业供应公司合作开发了攻丝测试软体,旨在透过公私合营提高允许切削速度并提升生产效率。加拿大充分利用了安大略省的汽车产业丛集,而墨西哥的巴希奥走廊则吸收了电子产品和白色家电的加工业务,以满足美国的需求。

欧洲凭藉德国、义大利和斯堪的纳维亚等国的专业企业向全球出口高精度加工单元,保持技术优势。然而,随着产油国实现多元化发展,预计到2031年,中东地区的复合年增长率将达到8.85%,成为该地区成长最快的地区。艾默生在萨勒曼国王能源园区新建的13,000平方公尺工厂以及先进精密工业服务公司在达曼扩建的54,000平方公尺工厂,将为该地区的能源、航太和石化产业提供重型机械加工服务。这些投资将降低进口依赖性,并为当地的零件维修创造下游机会。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业4.0主导的自动化升级

- 汽车和航太领域对高精度产品的需求日益增长

- 政府对工厂现代化改造的激励措施

- 五轴加工技术在电动车和植入的快速应用

- 混合增材製造及切削数控集成

- 利用数位双胞胎进行预测编程

- 市场限制

- 高昂的资本成本和生命週期成本

- 熟练的CNC编程人员短缺

- 联网控制设备的网路安全风险

- 零件供应链不稳定(滚珠螺桿、导轨)

- 价值/供应链分析

- 监管环境

- 技术展望

- 产业吸引力—五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值,单位:十亿美元)

- 按模型

- CNC车床

- CNC铣床

- 数控雷射切割机

- 数控等离子切割机

- CNC电火花加工(电火花成型和线切割)

- CNC研磨

- 数控钻孔/攻牙中心

- 其他专用CNC工具工具机

- 轴类型

- 三轴加工工具机

- 四轴加工工具机

- 五轴加工工具机

- 6 个或更多轴

- 按最终用户行业划分

- 车

- 航太/国防

- 电子装置和半导体

- 医疗设备

- 建筑和重型设备

- 电力和能源

- 造船

- 一般製造和合约工厂

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 秘鲁

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 东协(印尼、泰国、菲律宾、马来西亚、越南)

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 科威特

- 土耳其

- 埃及

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- FANUC Corporation

- DMG Mori Co. Ltd

- Haas Automation Inc.

- Okuma Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Yamazaki Mazak Corporation

- Bosch Rexroth AG

- GSK CNC Equipment Co. Ltd

- Hurco Companies Inc.

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Doosan Machine Tools

- Hyundai Wia Corp.

- Biesse Group

- Brother Industries Ltd

- FFG Europe & Americas

- Makino Milling Machine Co. Ltd

- Chiron Group SE

- JTEKT Corporation(Toyoda)

第七章 市场机会与未来展望

CNC Machines Market size in 2026 is estimated at USD 79.14 billion, growing from 2025 value of USD 74.82 billion with 2031 projections showing USD 104.76 billion, growing at 5.78% CAGR over 2026-2031.

Rising demand for digitally enabled production, tighter tolerance requirements in electric-vehicle and aerospace programs, and fiscal incentives for factory modernization collectively underpin this expansion. Vendors increasingly bundle hardware, software, and predictive services, allowing customers to raise asset utilization and defer new-equipment purchases while still expanding productive capacity. Procurement strategies now prioritize interoperability with industrial 5G and edge-computing platforms that reduce scrap rates by up to 30% and shorten spare-parts lead times by 10%. Geopolitical supply-chain concerns are also encouraging OEMs to reshore critical machining work, strengthening demand for domestic installations in North America and the European Union.

Global CNC Machines Market Trends and Insights

Industry 4.0-driven Automation Upgrades

Manufacturers are migrating from isolated machine tools to fully networked cells where IoT sensors stream real-time conditions to edge servers, cutting scrap by 30% and trimming spare-parts inventories by 10%. Fifth-generation wireless closes previous latency gaps, giving operators steady connectivity that prevents program interruptions. Digital twins now model thermal drift and spindle dynamics before a single chip is cut, trimming ramp-up times by 40%. AI-assisted toolpath agents lower programming workloads by 50% while improving surface finish repeatability. Collectively, these upgrades reposition CNC equipment as nodes within autonomous production loops rather than stand-alone capital assets.

Rising Precision Demand in Automotive & Aerospace

Electric-vehicle battery housings, inverter plates, and motor stators impose tolerance bands once limited to aerospace structures, prompting wider 5-axis adoption in automotive shops. Aerospace recovery adds a second precision stream, with titanium and carbon-fiber components requiring stable tool engagement beyond conventional parameters. Hybrid additive-subtractive processes can shave 35% off cycle times for intricate aerospace brackets while preserving dimensional integrity. Regulatory traceability rules further compel digital machining logs that prove micron-level accuracy. This dual-sector pull cements high-precision CNC capability as a baseline requirement rather than a premium option.

High Capital & Lifecycle Costs

Five-axis centers integrate high-precision rotary axes, linear motors, and thermal-compensation systems, lifting purchase tickets well above USD 500,000, a hurdle for small shops. Okuma estimates only 15% of lifetime spending happens at acquisition, with 85% tied to maintenance, energy, and unplanned outages. Digital twin licenses and AI modules pile extra costs onto enterprise resource plans. Studies show hybrid additive-subtractive cells demand thorough batch-size analyses before payback is viable, especially when powders carry premium prices. High ownership burden, therefore, limits penetration among low-volume manufacturers.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Factory Modernization

- Rapid Adoption of 5-Axis Machining for EV & Implants

- Skilled CNC Programmer Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CNC lathes captured 26.95% of 2025 revenue, underscoring their indispensable role in shafts, bushings, and other rotational parts across multiple value chains. Their straightforward programming and rigid tooling allow quick changeovers, making them staples for Tier 1 automotive and hydraulic suppliers. Milling machines follow, serving prismatic geometries where multi-surface accuracy matters. Laser cutters, however, are climbing fastest at an 8.55% CAGR thanks to fiber-laser sources that pierce steel, aluminum, and composite stacks with minimal distortion.

Prima Power's Laser Next 2130, paired with Siemens' SINUMERIK ONE control, boosted dynamic response by 20% and productivity by 13% in automotive body-in-white lines, illustrating why lasers are displacing stamping on complex panels. Electro-discharge machining and grinding sustain niche dominance in die-makers and bearing producers. Hybrid additive-subtractive units enable near-net deposition of nickel superalloys, then finishing on the same table, saving aerospace primes multiple logistics steps. The CNC machines market thus balances mature turning demand with rapid laser innovation.

The CNC Machines Market Report is Segmented by Machine Type (CNC Lathes, CNC Milling Machines, and More), by Axis Type (3-Axis, 4-Axis, and More), by End-User Industry (Automotive, Aerospace & Defense, Electronics & Semiconductor, and More), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific secured 46.10% of global revenue in 2025 as China, Japan, and India expanded domestic capacity to mitigate import risk and satisfy internal demand. China's First Automation raised RMB 100 million (USD 13.9 million) to develop native high-end controllers, signaling official intent to localize strategic machine-tool technology. Japan protects its premium segment through continual control upgrades; Okuma's OSP-P500 pairs adaptive machining with cyber-secure cloud links, demonstrating how legacy expertise evolves into data-driven services.

North America ranks second, combining reshoring subsidies, aerospace consolidation, and defense imperatives. Oak Ridge National Laboratory and MSC Industrial Supply co-developed tap-testing software that raises permissible material-removal rates, showing public-private collaboration on productivity. Canada leverages automotive clusters in Ontario, whereas Mexico's Bajio corridor absorbs electronics and white-goods machining to serve the United States' demand.

Europe retains technical leadership through German, Italian, and Nordic specialists who export high-tolerance cells worldwide. The Middle East, though, will post the strongest 8.85% CAGR to 2031 as oil-rich nations diversify. Emerson's 13,000 m2 plant at King Salman Energy Park and Advanced Precision Industrial Services' 54,000 m2 expansion in Dammam equip the region with heavy-duty machining for energy, aerospace, and petrochemical needs. These investments reduce import reliance and open downstream opportunities for localized component repair.

- FANUC Corporation

- DMG Mori Co. Ltd

- Haas Automation Inc.

- Okuma Corporation

- Mitsubishi Electric Corporation

- Siemens AG

- Yamazaki Mazak Corporation

- Bosch Rexroth AG

- GSK CNC Equipment Co. Ltd

- Hurco Companies Inc.

- Dr. Johannes Heidenhain GmbH

- Trumpf Group

- Doosan Machine Tools

- Hyundai Wia Corp.

- Biesse Group

- Brother Industries Ltd

- FFG Europe & Americas

- Makino Milling Machine Co. Ltd

- Chiron Group SE

- JTEKT Corporation (Toyoda)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0-driven automation upgrades

- 4.2.2 Rising precision demand in automotive & aerospace

- 4.2.3 Government incentives for factory modernization

- 4.2.4 Rapid adoption of 5-axis machining for EV & implants

- 4.2.5 Hybrid additive-subtractive CNC integration

- 4.2.6 Digital-twin-enabled predictive programming

- 4.3 Market Restraints

- 4.3.1 High capital & lifecycle costs

- 4.3.2 Skilled CNC programmer shortage

- 4.3.3 Cyber-security risks to connected CNC controls

- 4.3.4 Component supply-chain instability (ball screws, guides)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts(Value, In USD Billion)

- 5.1 By Machine Type

- 5.1.1 CNC Lathes

- 5.1.2 CNC Milling Machines

- 5.1.3 CNC Laser Cutting Machines

- 5.1.4 CNC Plasma Cutters

- 5.1.5 CNC EDM (Die-sink & Wire)

- 5.1.6 CNC Grinding Machines

- 5.1.7 CNC Drilling/Tapping Centers

- 5.1.8 Other Specialty CNC Machines

- 5.2 By Axis Type

- 5.2.1 3-Axis Machines

- 5.2.2 4-Axis Machines

- 5.2.3 5-Axis Machines

- 5.2.4 6-Axis & Above

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Aerospace & Defense

- 5.3.3 Electronics & Semiconductor

- 5.3.4 Medical Devices

- 5.3.5 Construction & Heavy Machinery

- 5.3.6 Power & Energy

- 5.3.7 Shipbuilding

- 5.3.8 General Manufacturing & Job Shops

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Peru

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Kuwait

- 5.4.5.5 Turkey

- 5.4.5.6 Egypt

- 5.4.5.7 South Africa

- 5.4.5.8 Nigeria

- 5.4.5.9 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 FANUC Corporation

- 6.4.2 DMG Mori Co. Ltd

- 6.4.3 Haas Automation Inc.

- 6.4.4 Okuma Corporation

- 6.4.5 Mitsubishi Electric Corporation

- 6.4.6 Siemens AG

- 6.4.7 Yamazaki Mazak Corporation

- 6.4.8 Bosch Rexroth AG

- 6.4.9 GSK CNC Equipment Co. Ltd

- 6.4.10 Hurco Companies Inc.

- 6.4.11 Dr. Johannes Heidenhain GmbH

- 6.4.12 Trumpf Group

- 6.4.13 Doosan Machine Tools

- 6.4.14 Hyundai Wia Corp.

- 6.4.15 Biesse Group

- 6.4.16 Brother Industries Ltd

- 6.4.17 FFG Europe & Americas

- 6.4.18 Makino Milling Machine Co. Ltd

- 6.4.19 Chiron Group SE

- 6.4.20 JTEKT Corporation (Toyoda)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

工业分板铣床市场(按铣床类型、切割技术、轴配置、自动化程度和最终用途行业划分)-全球预测,2026-2032年按玻璃材料、介面类型、测量范围、解析度和终端用户产业分類的CNC玻璃尺市场,全球预测,2026-2032年电动捲材矫直机市场按材料、最终用户、机器类型、自动化程度、厚度范围、驱动类型和部署方式划分-全球预测,2026-2032年金属板材矫直机市场(按机器类型、最终用途行业、材料类型、板材厚度、自动化程度、配置、驱动类型和分销渠道划分),全球预测,2026-2032年

工业分板铣床市场(按铣床类型、切割技术、轴配置、自动化程度和最终用途行业划分)-全球预测,2026-2032年按玻璃材料、介面类型、测量范围、解析度和终端用户产业分類的CNC玻璃尺市场,全球预测,2026-2032年电动捲材矫直机市场按材料、最终用户、机器类型、自动化程度、厚度范围、驱动类型和部署方式划分-全球预测,2026-2032年金属板材矫直机市场(按机器类型、最终用途行业、材料类型、板材厚度、自动化程度、配置、驱动类型和分销渠道划分),全球预测,2026-2032年 数控切割机市场规模、份额及成长分析(按机器类型、技术类型、应用产业、最终用户和地区划分)-2026-2033年产业预测CNC等离子切割台市场按檯面类型、功率、操作模式、驱动类型、材质、切割厚度、应用和最终用户划分-2026-2032年全球预测按冷却类型、工具机类型、冷却液配方、终端用户产业和分销管道分類的CNC工具机冷却市场,全球预测,2026-2032年按技术、自动化程度、机器尺寸、最终用户和分销管道分類的数控熔融机市场—2026-2032年全球预测按自动化程度、驱动类型、控制系统、材料类型和最终用户分類的数控等离子切割机市场,全球预测,2026-2032年数控工具机市场:按工具机类型、轴数、材料、最终用途产业、应用和销售管道,全球预测,2026-2032年

数控切割机市场规模、份额及成长分析(按机器类型、技术类型、应用产业、最终用户和地区划分)-2026-2033年产业预测CNC等离子切割台市场按檯面类型、功率、操作模式、驱动类型、材质、切割厚度、应用和最终用户划分-2026-2032年全球预测按冷却类型、工具机类型、冷却液配方、终端用户产业和分销管道分類的CNC工具机冷却市场,全球预测,2026-2032年按技术、自动化程度、机器尺寸、最终用户和分销管道分類的数控熔融机市场—2026-2032年全球预测按自动化程度、驱动类型、控制系统、材料类型和最终用户分類的数控等离子切割机市场,全球预测,2026-2032年数控工具机市场:按工具机类型、轴数、材料、最终用途产业、应用和销售管道,全球预测,2026-2032年