|

市场调查报告书

商品编码

1934875

铸铁:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Cast Iron - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

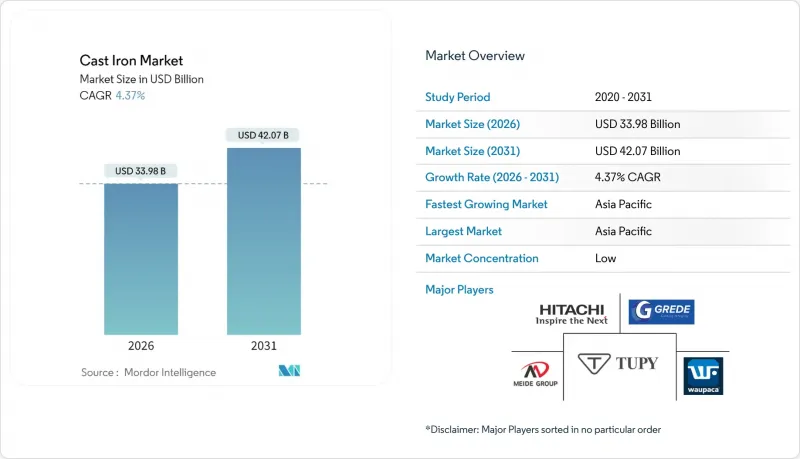

2025年,铸铁市场价值为325.6亿美元,预计到2031年将达到420.7亿美元,而2026年为339.8亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.37%。

这种稳定成长反映了该材料在成熟产业中的强势地位,其可靠性、可加工性和成本优势持续超越轻量化和新型合金的吸引力。汽车煞车系统、球墨铸铁管安装和工具机底座等应用领域对球墨铸铁的需求主要来自这些领域,这些应用需要球墨铸铁具备减振和热稳定性。亚太地区的产能投资,特别是中国新建高炉和印度持续扩大高炉,确保了供应并降低了下游製造商的交付成本。铸造厂也正在抓住可再生能源领域的机会,利用球墨铸铁製造风力发电机轮毂和高压氢气管道。同时,积层製造技术和电炉改造正在帮助生产商降低能耗,并在永续性指标方面脱颖而出。

全球铸铁市场趋势与洞察

汽车产业需求显着

灰铸铁仍然是转子的首选材料,因为其导热性和阻尼性能在反覆煞车循环中均符合安全标准。球墨铸铁(CGI)在不影响可回收性的前提下减轻了重量,帮助汽车製造商在满足排放气体法规的同时保持铸造效率。混合动力和增程器动力传动系统正在开闢新的成长领域,这些小型、高温引擎需要更高的强度重量比。同时,电气化的兴起正在为铸铁创造新的用途,例如电机外壳和电池组结构框架,预计即使传统引擎的需求下降,铸铁的订单仍将保持稳定。

建筑和基础设施领域的扩张

政府基础设施规划正在加速采用球墨铸铁管进行供水和污水处理系统维修,理由是该材料使用寿命长达100年且完全可回收。美国铸铁管公司斥资2.85亿美元对熔炉进行现代化改造,熔炼能力提高了25%,二氧化碳排放减少了62%,这表明公共产业可以在不影响其脱碳目标的前提下指定使用铸铁管。新兴市场越来越重视降低生命週期成本而非初始投资,这推动了排水系统、桥樑支座和建筑建筑幕墙对铸铁管的强劲需求,因为其耐久性弥补了较高的初始投资。这一趋势也正在中东和拉丁美洲的供水事业蔓延,有助于缓解北美住宅速度放缓的影响。

能源和焦炭价格上涨推高了成本。

传统高炉每生产一吨铁水大约消耗0.6吨焦炭,使得铸造厂极易受到煤炭进口价格波动和碳排放税的影响。欧洲的铸造厂受电价上涨和地缘政治不确定性导致的成本上升影响最为严重,这迫使一些小规模铸造厂停产甚至倒闭。干式淬火系统和生物炭取代焦炭可以减少热损失和碳排放强度,但需要大量的资本投入,只有大型生产商才能摊提这些成本。在再生能源价格下降和高炉改造普及之前,能源消耗仍将是利润率的一大拖累,这促使企业将生产转移到成本更低的地区。

细分市场分析

截至2025年,灰铸铁将占据铸铁市场47.12%的份额,这主要得益于其在刹车盘、引擎壳体和工具机机床身等领域的应用,这些应用依赖于灰铸铁的导热性和减振性能。此外,由于硬质雷射表面处理显着提高了灰铸铁的耐磨性,预计其在破碎设备和农业犁地工具等领域的需求也将成长。

虽然展性铸铁在电气配件和手动工具领域的需求不断增长,但球墨铸铁在水利基础设施和风力发电铸件领域(这些领域对抗拉强度和延伸率要求较高)的份额正在扩大。用于耐磨矿井衬砌的白口铸铁将继续保持其小众市场地位,而熔铸铁(CGI)则随着原始设备製造商不断检验其疲劳性能,呈现出逐步扩张的趋势。

区域分析

到2025年,亚太地区将占全球铸铁产量的38.45%,年复合成长率达5.12%。该地区的铸铁市场依赖于密集的价值链丛集,该集群整合了矿石开采、焦炉和下游加工等环节。河北和山东两省新建的高炉采用高压富氧设计,比传统设施节省10-12%的焦炭,缩小了与欧洲製造商在能源效率上的差距。以菲律宾为首的东南亚地区已宣布一系列基础建设计划,旨在将年钢铁消费量提升至1,000万吨。

北美在自动化技术领域的领先地位,加上联邦政府的激励措施,正在推动关键零件的生产回流。美国铸造协会的会员企业数量已超过1050家,显示产能更新和技术纯熟劳工的需求正在增加。流程数位化和3D砂型列印技术使区域製造商能够在国防、航太以及高价值、快速週转的电动汽车零件等高利润领域实现灵活生产。然而,像史密斯铸造厂这样的工厂因严格的排放法规而关闭,凸显了平衡合规成本与竞争力的必要性。

在欧洲,能源供应衝击导致炼钢厂转向使用电炉,并试行生物炭炼钢以弥补焦炭短缺。预计2024年钢铁表观消费量将下降2.3%,而建设产业已连续七季处于萎缩状态。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 来自汽车产业的庞大需求

- 建筑和基础设施领域的扩张

- 工业机械投资成长

- 高强度零件采用球墨铸铁

- 利用3D砂型列印技术实现小批量生产

- 市场限制

- 能源和焦炭价格上涨推高了成本。

- 铸铁的轻质替代品

- 铁矿石关税波动与贸易壁垒

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按年级

- 灰铸铁

- 球墨铸铁

- 展性铸铁

- 白铁

- 透过铸造工艺

- 砂型铸造

- 离心铸造

- 壳模铸造

- 精密铸造

- 其他流程

- 透过使用

- 汽车/运输设备

- 建筑和基础设施

- 工业机械

- 电力和能源

- 炊具和家居用品

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 泰国

- 越南

- 马来西亚

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 埃及

- 奈及利亚

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)*/排名分析

- 公司简介

- AKP Ferrocast Pvt. Ltd.

- Brakes India

- CALMET

- Castings PLC

- Chamberlin

- Crescent Foundry

- GIS

- Grede LLC

- Hitachi Power Solutions Co.,Ltd.

- LIAONING BORUI MACHINERY CO., LTD(DANDONG FOUNDRY)

- MEIDE GROUP

- NDC FOUNDRY

- Newby Holdings Limited

- OSCO Industries

- superironfoundry

- Tupy

- WAUPACA FOUNDRY, INC.

- Xinxing Ductile Iron Pipe Co.,ltd.

第七章 市场机会与未来展望

The Cast Iron Market was valued at USD 32.56 billion in 2025 and estimated to grow from USD 33.98 billion in 2026 to reach USD 42.07 billion by 2031, at a CAGR of 4.37% during the forecast period (2026-2031).

This steady growth reflects the material's entrenched role in mature industries where reliability, machinability, and cost advantages continue to outweigh the appeal of lighter or novel alloys. Demand is underpinned by automotive brake systems, ductile iron pipe installations, and machine-tool bases that require vibration damping and thermal stability. Capacity investments in Asia Pacific, particularly new blast furnaces in China and ongoing expansions in India, safeguard supply and lower delivered costs for downstream manufacturers. Foundries are also capturing opportunities in renewable energy, leveraging spheroidal graphite iron for wind-turbine hubs and ductile iron for high-pressure hydrogen pipelines. At the same time, additive manufacturing and electric furnace retrofits help producers trim energy intensity and differentiate on sustainability metrics.

Global Cast Iron Market Trends and Insights

Significant Demand from Automotive Sector

Gray iron continues as the default rotor material because its thermal conductivity and damping characteristics match safety standards under repetitive braking cycles. Compact graphite iron (CGI) reduces mass without sacrificing recyclability, helping automakers meet emissions rules while retaining casting efficiencies. Hybrid and range-extender powertrains add growth avenues where downsized, high-temperature engines demand higher strength-to-weight ratios. Concurrently, electrification shifts spur novel cast iron applications in motor housings and battery-pack structural frames, sustaining metal orders long after traditional engine content recedes.

Expansion in Construction and Infrastructure

Government infrastructure programs accelerate ductile iron pipe uptake for water and wastewater upgrades, attracted by the material's 100-year service life and full recyclability. AMERICAN Cast Iron Pipe Company's USD 285 million furnace modernization raises melting capacity by 25% while cutting CO2 emissions 62%, signalling that utilities can specify cast iron without compromising decarbonization goals. Emerging economies prioritize lifecycle savings over initial cost, reinforcing demand in drainage, bridge bearings, and architectural facades where cast iron's durability offsets higher upfront spend. The momentum cascades into Middle East and Latin America water projects, balancing softer North American housing starts.

High Energy and Coke Prices Inflate Costs

Traditional blast furnaces consume nearly 0.6 tons of coke per ton of hot metal, exposing foundries to volatile coal import prices and carbon taxes. European operations shoulder the heaviest burden as power tariffs and geopolitical uncertainty elevate cost bases, prompting some small foundries to idle or close. Coke dry quenching systems and biochar substitution cut thermal losses and carbon intensity but demand sizable capital outlays that only large producers can amortize. Until renewable electricity prices fall and furnace retrofits scale, energy remains a drag on margins and an incentive for production shifts toward lower-cost regions.

Other drivers and restraints analyzed in the detailed report include:

- Growth in Industrial Machinery Investments

- Adoption of Ductile Iron for High-Strength Parts

- Light-Weight Materials Substituting Cast Iron

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gray iron controlled 47.12% of the cast iron market share in 2025, anchored in brake rotors, engine housings, and machine-tool beds that depend on its thermal conductivity and vibration-damping attributes. Hard-laser surface treatments extend wear life, opening opportunities in crushing equipment and agricultural tillage tools.

Rising malleable iron demand for electrical fittings and hand tools underpins a 4.84% CAGR, while ductile iron gains share in water infrastructure and wind-energy castings that necessitate high tensile strength and elongation. White iron stays niche for abrasion-resistant mining liners, and CGI scales slowly as OEMs validate fatigue properties.

The Cast Iron Market Report is Segmented by Grade (Gray Iron, Ductile Iron, Malleable Iron, & White Iron), Casting Process (Sand Casting, Centrifugal Casting, and More), Application (Automotive and Transportation, Construction and Infrastructure, Industrial Machinery, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific supplied 38.45% of global output in 2025 and is growing at a 5.12% CAGR. Asia Pacific's cast iron market rests on dense value-chain clusters that integrate ore mining, coke ovens, and downstream machining. New furnaces built in Hebei and Shandong use high-top-pressure, oxygen-enrichment designs that consume 10-12% less coke than legacy units, narrowing the energy gap with European producers. Southeast Asia, led by the Philippines, unveils infrastructure pipelines that drive annual steel consumption toward 10 million tons.

North America combines automation leadership with federal incentives to reshore critical components. American Foundry Society membership crossing 1,050 companies indicates capacity renewal and skilled-worker recruitment tailwinds. Process digitization and 3D sand printing give regional producers agility for defense, aerospace, and short-run EV parts that carry premium margins. Yet stringent emission limits closed facilities such as Smith Foundry, underscoring the need to balance compliance costs with competitiveness.

Europe's energy supply shock drives furnace electrification and biochar trials to offset coke shortages. Apparent steel consumption slipped 2.3% in 2024, with the construction industry contracting for seven consecutive quarters.

- AKP Ferrocast Pvt. Ltd.

- Brakes India

- CALMET

- Castings P.L.C

- Chamberlin

- Crescent Foundry

- GIS

- Grede LLC

- Hitachi Power Solutions Co.,Ltd.

- LIAONING BORUI MACHINERY CO., LTD (DANDONG FOUNDRY)

- MEIDE GROUP

- NDC FOUNDRY

- Newby Holdings Limited

- OSCO Industries

- superironfoundry

- Tupy

- WAUPACA FOUNDRY, INC.

- Xinxing Ductile Iron Pipe Co.,ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Significant Demand from the Automotive Sector

- 4.2.2 Expansion in Construction and Infrastructure

- 4.2.3 Growth in Industrial Machinery Investments

- 4.2.4 Adoption of Ductile Iron for High-Strength Parts

- 4.2.5 3-D Sand-Printing Enabling Short Production Runs

- 4.3 Market Restraints

- 4.3.1 High Energy and Coke Prices Inflate Costs

- 4.3.2 Light-Weight Materials Substituting Cast Iron

- 4.3.3 Volatile Iron-Ore Tariffs and Trade Barriers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Gray Iron

- 5.1.2 Ductile Iron

- 5.1.3 Malleable Iron

- 5.1.4 White Iron

- 5.2 By Casting Process

- 5.2.1 Sand Casting

- 5.2.2 Centrifugal Casting

- 5.2.3 Shell-Mold Casting

- 5.2.4 Investment Casting

- 5.2.5 Other Processes

- 5.3 By Application

- 5.3.1 Automotive and Transportation

- 5.3.2 Construction and Infrastructure

- 5.3.3 Industrial Machinery

- 5.3.4 Power and Energy

- 5.3.5 Cookware and Domestic

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Thailand

- 5.4.1.7 Vietnam

- 5.4.1.8 Malaysia

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 Egypt

- 5.4.5.5 Nigeria

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)*/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AKP Ferrocast Pvt. Ltd.

- 6.4.2 Brakes India

- 6.4.3 CALMET

- 6.4.4 Castings P.L.C

- 6.4.5 Chamberlin

- 6.4.6 Crescent Foundry

- 6.4.7 GIS

- 6.4.8 Grede LLC

- 6.4.9 Hitachi Power Solutions Co.,Ltd.

- 6.4.10 LIAONING BORUI MACHINERY CO., LTD (DANDONG FOUNDRY)

- 6.4.11 MEIDE GROUP

- 6.4.12 NDC FOUNDRY

- 6.4.13 Newby Holdings Limited

- 6.4.14 OSCO Industries

- 6.4.15 superironfoundry

- 6.4.16 Tupy

- 6.4.17 WAUPACA FOUNDRY, INC.

- 6.4.18 Xinxing Ductile Iron Pipe Co.,ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment