|

市场调查报告书

商品编码

1934876

接线端子:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Terminal Block - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

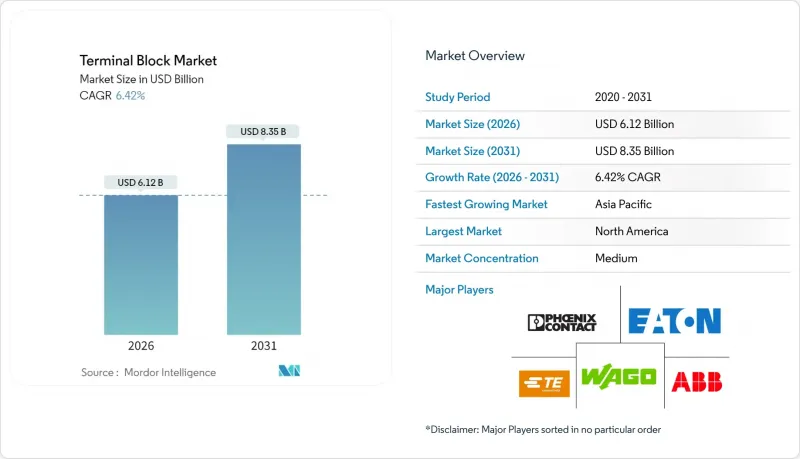

2025 年接线端子市场价值为 57.5 亿美元,预计到 2031 年将达到 83.5 亿美元,高于 2026 年的 61.2 亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 6.42%。

工业自动化的快速普及、可再生能源基础设施的扩张以及楼宇电气化项目的加速推进,都为这一增长提供了支撑,使接线端子市场成为全球电气化趋势的主要受益者。模组化布线架构与感测器密集生产环境的融合,推动了对高密度直通式接线端子和感测器/致动器接线端子的需求。可再生能源应用推动了额定电压为1500V的高压直流接线端子的普及,而北美和欧洲的建筑自动化维修则倾向于采用紧凑型DIN导轨解决方案,以缩短安装时间并简化维护。然而,铜铝价格的波动以及假冒伪劣产品的风险限制了现有供应商的利润成长。儘管如此,知名品牌仍在不断创新,推出推入式和插入式设计,以减少布线工作量并支援智慧工厂的可重构性,从而在接线端子市场保持竞争优势。

全球接线端子市场趋势与洞察

工业4.0推动模组化布线需求

製造商正在重新设计生产线,以实现更柔软性、感测器密集的操作,这需要快速更换线路。菲尼克斯电气已投资1亿欧元用于自动化物流,以支援这些智慧工厂的实施。魏德米勒的模组化侧入式推入式接线端子可将连接时间缩短50%,并支援生产线无停机重新配置。控制柜製造商受益于更短的组装週期和更少的熟练劳动力需求,这巩固了接线端子市场作为工业4.0架构核心驱动力的地位。 IO-Link和其他设备级网路进一步增加了每个控制柜的I/O点数量,从而推动了感测器/致动器模组的订单。随着自动化工厂在亚太和欧洲的日益普及,模组化布线密度的需求仍将是关键驱动因素。

稳健的电力分配对于扩大可再生能源至关重要。

全球太阳能和风能发电设施的兴起,对能够承受紫外线、振动和剧烈温度变化的接线端子提出了更高的要求。 TE Connectivity 收购 Hager 后,扩展了其能源产品线,为这些设施提供防雷和接地解决方案。电池能源储存系统需要高压直流模组来防止极性反转。菲尼克斯电气的极化连接器可满足 1500V 阵列的这项要求。电网营运商也开始指定使用整合电流感测功能的智慧接线端子,以优化间歇性发电的电力传输。这种不断增长的基础设施将扩大坚固耐用、可监控的连接硬体的装置量,从而增强接线端子市场的收入前景。

铜铝价格波动

2025年初,铜价突破每吨1万美元,挤压了大量消耗这种导电金属的模组製造商的利润空间。铝价飙升也给大截面电源模组带来了额外压力。虽然合约中的金属定价条款会将部分成本转嫁给买家,但竞标限制了成本的完全回收,从而抑制了整个接线端子市场的净利率。供应商正在探索铜包铝和轻量化导体设计以降低风险,但认证週期的延迟阻碍了这些技术的快速应用。

细分市场分析

至2025年,直通式接线端子将占接线端子市场规模的35.92%,成为工厂和机械设备配电的基础连接器。其坚固的螺丝夹紧设计使其能够相容于各种尺寸的导线,从而巩固其作为OEM标准产品目录产品的地位。同时,感测器/致动器接线端子将以8.28%的复合年增长率实现最快的成长,这主要得益于分散式I/O在状态监测和预测性维护领域的应用。其单位长度内的高接点密度符合机柜小型化的目标。栅栏式和麵板式接线端子满足能源和铁路应用的高压和安全要求,而熔断器式和隔离式接线端子则整合了电路保护功能,并将连接性进一步融入保护功能中。热电偶和LED状态指示灯接线端子则代表着向应用特定设计方向的转变,这种设计将讯号处理和布线功能结合。

儘管直通式端子仍将占据主导地位,但随着工业物联网 (IIoT) 的普及,感测器点数量增加,其市场份额预计将略有下降。因此,製造商正在扩展产品线,推出多级可拆卸感测器模组,兼顾节省空间和快速更换的优点。这一趋势正在推动产品组合的变化,从而推高端子模组市场的平均售价和收入成长。

到2025年,DIN导轨式接线端子将占据54.78%的接线端子市场份额,这主要得益于全球标准化和现场服务的便利性。其卡扣式设计简化了改造和扩展,并保持了面板製造商之间库存的通用。 PCB安装解决方案目前正以7.16%的复合年增长率成长,以满足驱动器、电源和物联网边缘节点中小批量、小型化组件的需求。贴片机相容性支援高速SMT生产线,从而降低了产品总成本,但同时也提高了单位成本。需要隔振和大电流接线片的重型机壳仍普遍采用面板安装和直接元件安装方式。

电子元件整合度的不断提高推动了PCB设计在规模和复杂性上的扩展,越来越多的混合讯号模组被整合到基板。然而,由于停机风险和布线复杂性,维修工程师仍然偏好DIN导轨布局,模组化设计更具优势。这种共生关係促进了接线端子市场健康的细分市场多样性。

区域分析

到2025年,北美将占据接线端子市场41.38%的份额,这得益于其在航太、汽车和製程工业领域成熟的製造基地。电网现代化和墨西哥的近岸外包将确保接线端子柜需求的稳定。 UL 1059标准的实施将增强消费者对高阶认证接线端子的偏好,从而维持平均价格。然而,随着现有设备的成熟,市场成长速度正在放缓,促使供应商将重心转向维修主导和智慧接线端子柜解决方案。

预计到2031年,亚太地区将以7.05%的复合年增长率成长,这主要得益于中国的电子产品生产和该地区的电气化进程。儘管中国本土製造商能够提供具有成本竞争力的PCB模组,但全球OEM厂商在可靠性要求高的领域仍保持着品质优势。印度和东协地区基础设施的不断改进正在推动DIN导轨在配电和工厂自动化领域的应用。然而,该地区假冒产品的氾滥给智慧财产权保护带来了挑战,并加剧了低端端子模组市场的价格压力。

在德国工业4.0倡议的推动下,欧洲保持其技术领先地位。绿色交易下对风能、太阳能和储能的投资正在推动对恶劣环境端子块的需求。魏德米勒11.02亿欧元的销售额及其在中国产能的扩张,凸显了欧洲在全球化世界中的竞争力。东欧蕴藏新增产能的潜力,英国脱欧则让英国的物流变得更加复杂。儘管中东和非洲地区的规模较小,但智慧电网和产业多元化被视为推动其稳步应用的催化剂,并使其端子块市场拓展至新兴基础设施计划。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 工业4.0推动模组化布线需求

- 扩大可再生能源的规模需要强大的电网。

- 成熟经济体的建筑自动化/暖通空调维修

- 由于面积且易于维护,DIN导轨解决方案是首选。

- 小型化物联网设备需要尺寸小于 3.5 毫米的 PCB 模组。

- 电动车快速充电器安全标准推动高电流阻断

- 市场限制

- 铜铝价格波动

- 低成本仿冒品的氾滥

- 网路安全回应迟缓会减缓「智慧」模组的普及。

- 精密弹簧钢短缺限制了产能。

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 直通式接线端子

- 隔离栅/面板接线端子

- 接地块

- 保险丝和断路器模组

- 感测器/致动器及其他类型

- 其他产品类型

- 透过安装方法

- DIN导轨安装型

- 印刷基板安装

- 面板/底盘安装

- 其他安装方法

- 透过连接技术

- 螺丝夹

- 弹簧夹

- 推入式/插入式

- 其他连接技术

- 按最终用户行业划分

- 工业控制与自动化

- 电力和能源

- 建筑/施工(暖通空调/楼宇管理系统)

- 交通运输(铁路、电动车充电)

- 电讯和资料通讯

- 其他终端用户产业

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Phoenix Contact GmbH & Co. KG

- WAGO Kontakttechnik GmbH & Co. KG

- Weidmuller Interface GmbH & Co. KG

- TE Connectivity Ltd.

- Wieland Electric GmbH

- Eaton Corporation plc

- Omron Corporation

- ABB Ltd

- Rockwell Automation, Inc.

- Siemens Aktiengesellschaft(Siemens AG)

- Schneider Electric SE

- Molex, LLC

- Amphenol Corporation

- On Shore Technology, Inc.

- Dinkle International Co., Ltd.

- Klemsan Elektrik Elektronik Sanayi ve Ticaret Anonim Sirketi

- Marathon Special Products Corporation

- Camden Boss Limited

- CONTA-CLIP Verbindungstechnik GmbH

- Ningbo Degson Electronics Co., Ltd.

- Hubbell Incorporated

- Luetze International GmbH

- Phoenix Mecano AG

- WECO Electrical Connectors Inc.

- SwitchLab Inc.

第七章 市场机会与未来展望

The terminal block market was valued at USD 5.75 billion in 2025 and estimated to grow from USD 6.12 billion in 2026 to reach USD 8.35 billion by 2031, at a CAGR of 6.42% during the forecast period (2026-2031).

Rapid adoption of industrial automation, expanding renewable-energy infrastructure, and accelerating building electrification programs underpin this advance, positioning the terminal block market as a core beneficiary of global electrification trends. Convergence of modular wiring architectures with sensor-rich production environments is lifting demand for high-density feed-through and sensor/actuator blocks. Renewable-energy applications are fuelling the uptake of high-voltage DC blocks rated to 1,500 V, while building-automation retrofits in North America and Europe favour compact DIN-rail solutions that shorten installation time and ease servicing. At the same time, copper and aluminium price swings and counterfeit component risks temper margin expansion for established suppliers. Nonetheless, established brands continue to innovate with push-in and pluggable designs that cut wiring labour and support smart-factory re-configurability, sustaining competitiveness within the terminal block market.

Global Terminal Block Market Trends and Insights

Industry 4.0-driven Demand for Modular Wiring

Manufacturers are re-engineering production lines for flexible, sensor-rich operations that demand fast-change wiring. Phoenix Contact invested EUR 100 million in automated logistics to support such smart-factory deployments. Modular side-entry push-in blocks introduced by Weidmuller cut connection time by 50%, allowing line re-configuration without downtime. Control-cabinet builders gain from shorter assembly cycles and reduced skilled-labour requirements, strengthening the terminal block market as a core enabler of Industry 4.0 architectures. IO-Link and other device-level networks further raise the number of I/O points per cabinet, boosting orders for sensor/actuator blocks. As automated plants proliferate across APAC and Europe, demand for modular wiring connection density will remain a primary catalyst.

Renewable-energy Build-out Needs Robust Power Distribution

Rising global solar and wind installations require terminal blocks rated for UV, vibration, and wide temperature exposure. TE Connectivity broadened its energy portfolio via the Harger acquisition to address lightning protection and grounding for these assets. Battery-energy-storage systems need high-voltage DC blocks that prevent polarity reversal; Phoenix Contact's pole connectors meet that requirement for 1,500 V arrays. Grid operators also specify smart terminal blocks with integrated current sensing to optimise dispatch from intermittent generation. This infrastructure push multiplies install-base growth for rugged, monitored connection hardware, reinforcing revenue visibility for the terminal block market.

Copper and Aluminium Price Volatility

Copper prices exceeded USD 10,000 per ton in early 2025, squeezing margins for block makers who consume tonnes of conductive metal. Aluminium cost spikes add pressure on large cross-section power blocks. While metal clauses in contracts pass some costs to buyers, competitive bidding limits full recovery, curbing net profitability across the terminal block market. Suppliers explore copper-clad aluminium and reduced conductor mass designs to mitigate exposure, though qualification cycles slow rapid adoption.

Other drivers and restraints analyzed in the detailed report include:

- Building-Automation/HVAC Retrofits in Mature Economies

- Preference for DIN-rail Solutions for Footprint and Serviceability

- Proliferation of Low-cost Counterfeits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Feed-through blocks accounted for 35.92% of the terminal block market size in 2025, acting as foundational connectors for power distribution across factories and machinery. Sturdy screw-clamp designs allow versatile conductor sizes, preserving their status as baseline catalogue items for OEMs. Sensor/actuator blocks, however, record the fastest 8.28% CAGR as users add distributed I/O to achieve condition monitoring and predictive maintenance. Higher contact density per unit length aligns with cabinet downsizing goals. Barrier and panel blocks fulfill high-voltage and safety mandates in energy and rail applications, while fuse and disconnect variants integrate circuit protection, further embedding connectivity within protective functions. Thermocouple and LED status blocks illustrate the transition toward application-specific designs that merge signal processing with wiring.

Feed-through dominance will persist but marginally erode as IIoT deployments multiply sensor points. Producers therefore broaden lines with multi-level and pluggable sensor blocks that combine space savings with quick swap-out. These dynamics reinforce a product-mix shift that elevates average selling prices and supports revenue growth across the terminal block market.

DIN-rail blocks contributed 54.78% of the terminal block market share in 2025 thanks to global standardisation and field-service convenience. Their snap-on design simplifies retrofits and expansions, keeping inventory commonality across panel builders. PCB-mount solutions, though smaller at present, are climbing at a 7.16% CAGR to address miniaturised assemblies in drives, power supplies, and IoT edge nodes. Pick-and-place compatibility enables high-speed SMT lines, shrinking total product cost despite premium unit pricing. Panel-mounted and direct-component variants continue in heavy-duty enclosures where vibration isolation or high-current lugs are needed.

Continued electronics convergence means PCB designs will gain both volume and complexity, pulling more mixed-signal blocks onto boards. However, service engineers still favour DIN-rail layouts where downtime risk and wiring complexity justify modularity. This coexistence supports healthy segment diversity inside the terminal block market.

The Terminal Block Market Report is Segmented by Product Type (Feed-Through Terminal Blocks, Barrier/Panel Terminal Blocks, and More), Mounting Method (DIN-Rail Mounted, PCB-Mounted, and More), Connection Technology (Screw Clamp, Spring Clamp, and More), End-User Industry (Industrial Controls and Automation, Power and Energy, Telecom and Data-Com, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 41.38% of terminal block market revenue in 2025, anchored by established manufacturing in aerospace, automotive, and process industries. Grid-modernisation and near-shoring to Mexico secure stable cabinet demand. UL 1059 standards reinforce preference for premium certified blocks, sustaining average prices. Growth nonetheless moderates as the installed base matures, so vendors focus on retrofit-driven upgrades and smart-cabinet solutions.

Asia-Pacific is projected to grow at a 7.05% CAGR through 2031, benefiting from Chinese electronics production and regional electrification programs. Local makers in China supply cost-competitive PCB blocks, but global OEMs maintain quality leadership in segments demanding reliability. India and ASEAN infrastructure drives DIN-rail adoption in power distribution and factory automation. The region's counterfeit prevalence, however, challenges intellectual-property protection and compresses pricing in lower tiers of the terminal block market.

Europe remains technologically advanced, led by Germany's Industry 4.0 rollouts. EU Green Deal investments in wind, solar, and energy storage raise demand for harsh-environment blocks. Weidmuller's EUR 1.102 billion turnover and China capacity expansion underline globalised European competitiveness. Eastern Europe offers fresh capacity-build potential, while Brexit complicates UK logistics. The Middle East and Africa, though smaller, view smart-grid and industrial diversification as catalysts for steady adoption, extending the reach of the terminal block market into emerging infrastructure projects.

- Phoenix Contact GmbH & Co. KG

- WAGO Kontakttechnik GmbH & Co. KG

- Weidmuller Interface GmbH & Co. KG

- TE Connectivity Ltd.

- Wieland Electric GmbH

- Eaton Corporation plc

- Omron Corporation

- ABB Ltd

- Rockwell Automation, Inc.

- Siemens Aktiengesellschaft (Siemens AG)

- Schneider Electric SE

- Molex, LLC

- Amphenol Corporation

- On Shore Technology, Inc.

- Dinkle International Co., Ltd.

- Klemsan Elektrik Elektronik Sanayi ve Ticaret Anonim ?irketi

- Marathon Special Products Corporation

- Camden Boss Limited

- CONTA-CLIP Verbindungstechnik GmbH

- Ningbo Degson Electronics Co., Ltd.

- Hubbell Incorporated

- Luetze International GmbH

- Phoenix Mecano AG

- WECO Electrical Connectors Inc.

- SwitchLab Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0-driven demand for modular wiring

- 4.2.2 Renewable-energy build-out needs robust power distribution

- 4.2.3 Building-automation/HVAC retrofits in mature economies

- 4.2.4 Preference for DIN-rail solutions for footprint and serviceability

- 4.2.5 Miniaturised IoT devices require sub-3.5 mm PCB blocks

- 4.2.6 EV fast-charger safety specs push high-amp blocks

- 4.3 Market Restraints

- 4.3.1 Copper and aluminium price volatility

- 4.3.2 Proliferation of low-cost counterfeits

- 4.3.3 Cyber-security compliance delays "smart" blocks

- 4.3.4 Precision spring-steel shortages constrain capacity

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Feed-through Terminal Blocks

- 5.1.2 Barrier/Panel Terminal Blocks

- 5.1.3 Grounding/Earthing Blocks

- 5.1.4 Fuse and Disconnect Blocks

- 5.1.5 Sensor/Actuator and Other Types

- 5.1.6 Other Product Types

- 5.2 By Mounting Method

- 5.2.1 DIN-Rail Mounted

- 5.2.2 PCB-Mounted

- 5.2.3 Panel/Chassis Mounted

- 5.2.4 Other Mounting Methods

- 5.3 By Connection Technology

- 5.3.1 Screw Clamp

- 5.3.2 Spring Clamp

- 5.3.3 Push-in/Pluggable

- 5.3.4 Other Connection Technologies

- 5.4 By End-user Industry

- 5.4.1 Industrial Controls and Automation

- 5.4.2 Power and Energy

- 5.4.3 Building and Construction (HVAC/BMS)

- 5.4.4 Transportation (Rail, EV Charging)

- 5.4.5 Telecom and Data-com

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Phoenix Contact GmbH & Co. KG

- 6.4.2 WAGO Kontakttechnik GmbH & Co. KG

- 6.4.3 Weidmuller Interface GmbH & Co. KG

- 6.4.4 TE Connectivity Ltd.

- 6.4.5 Wieland Electric GmbH

- 6.4.6 Eaton Corporation plc

- 6.4.7 Omron Corporation

- 6.4.8 ABB Ltd

- 6.4.9 Rockwell Automation, Inc.

- 6.4.10 Siemens Aktiengesellschaft (Siemens AG)

- 6.4.11 Schneider Electric SE

- 6.4.12 Molex, LLC

- 6.4.13 Amphenol Corporation

- 6.4.14 On Shore Technology, Inc.

- 6.4.15 Dinkle International Co., Ltd.

- 6.4.16 Klemsan Elektrik Elektronik Sanayi ve Ticaret Anonim ?irketi

- 6.4.17 Marathon Special Products Corporation

- 6.4.18 Camden Boss Limited

- 6.4.19 CONTA-CLIP Verbindungstechnik GmbH

- 6.4.20 Ningbo Degson Electronics Co., Ltd.

- 6.4.21 Hubbell Incorporated

- 6.4.22 Luetze International GmbH

- 6.4.23 Phoenix Mecano AG

- 6.4.24 WECO Electrical Connectors Inc.

- 6.4.25 SwitchLab Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment