|

市场调查报告书

商品编码

1934908

自动识别与资料撷取(AIDC):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automatic Identification And Data Capture (AIDC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

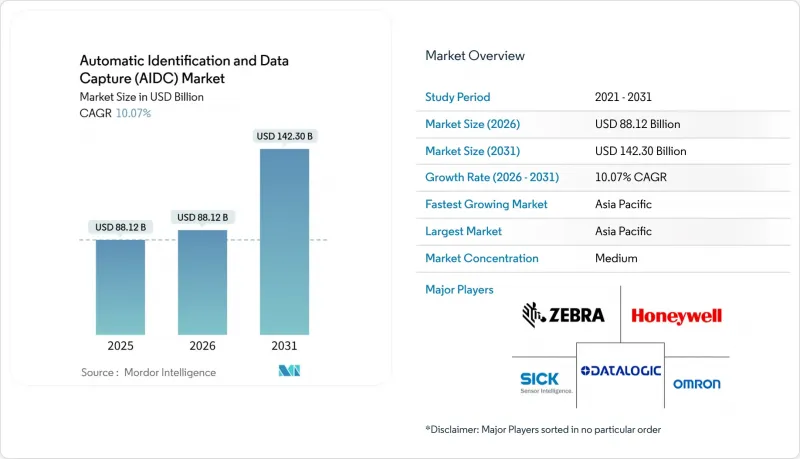

自动识别和资料撷取(AIDC) 市场预计到 2026 年将达到 881.2 亿美元,高于 2025 年的 800.5 亿美元。

预计到 2031 年将达到 1,423 亿美元,2026 年至 2031 年的复合年增长率为 10.07%。

预计累积成长率将达到 62.7%,这反映了製造业、零售业和医疗保健行业的结构性数位化,使得自动识别成为提高吞吐量、合规性和消除错误的关键组成部分。劳动力短缺、日益复杂的监管以及实时可视性带来的显着投资回报率共同造就了市场需求,使得自动识别和资料撷取(AIDC) 市场被视为基础设施而非可自由支配的支出 (biometricupdate.com)。二维条码、被动式超高频射频识别 (UHF-RFID) 和国家电子识别计划的日益普及,为能够构建集成设备、中间件和云端分析的统一生态系统的解决方案供应商创造了机会。

全球自动识别与资料撷取(AIDC) 市场趋势与洞察

加速全通路零售向二维/QR码转型

为了迎接GS1 Sunrise 2027的实施,全球零售商正积极迁移至二维码/QR码。此标准允许将有效期限、批号和行销连结嵌入到单一高密度符号中。早期采用者报告称,二维码/二维码的使用减少了食物废弃物,并带来了更流畅的全通路体验,丰富的数据支援自动折扣和动态客户参与。投资回报体现在减少人工操作、提高销售点扫描准确率、利用消费者智慧型手机开展新型互动行销方式等。硬体供应商预计,随着零售商用能够解码多种符号的成像器取代传统的1D扫描器,销售额将会增加;而软体供应商则将从POS韧体更新带来的升级成本中获益。

UHF-RFID在物品级库存管理中的应用迅速成长

沃尔玛强制要求在2024年部署物品等级RFID标籤,这正在推动零售业全面采用该技术。供应商鼓励零售连锁店在收货点、仓库和货架上嵌入可扫描的嵌体。每个被动式标籤的成本已降至0.04美元以下,这使得在服装和家居用品等关键品类中采用即时库存可见性成为可能。部署RFID技术已将库存准确率提高了25%,显着减少了缺货情况的发生。持续扫描的数据还可用于安全分析,使RFID技术兼具提高利润率和防止库存损耗的双重优势。

旧版ERP系统之间资料格式不相容

仍在使用90年代ERP系统的公司往往难以原生整合RFID和影像数据,必须部署中间件层,导致计划成本增加高达40%。因此,自动识别和资料撷取(AIDC)市场面临着销售週期延长的挑战,因为整合、测试和迁移成本必须纳入预算。在多站点网路中,不同的资料模式会增加复杂性,并造成资料孤岛,从而削弱预期的投资报酬率。儘管供应商透过提供预先建置连接器和咨询服务来降低风险,但将新系统整合到现有系统中仍然是一大障碍。

细分市场分析

到2025年,硬体收入将占总收入的62.50%,这主要得益于零售和医疗保健产业的基础设施更新换代。然而,价格压缩、标准化和供应链波动正在挤压利润空间,并加速向利润率更高的咨询和支援合约模式转变。提供硬体即服务(HaaS)的供应商在调整产品组合的同时,也维持了销售量。因此,自动识别和资料撷取(AIDC)市场的竞争优势正向那些掌握混合收入模式(将资本设备与持续服务结合)的供应商倾斜。

服务领域的成长速度超过硬体领域,复合年增长率高达 11.64%,这主要得益于企业越来越多地采用基于结果的合约模式,涵盖整合、维护和云端分析等服务。许多大型零售商正从资本支出购买转向託管服务,以确保扫描器、印表机和 RFID 入口网站的运作。服务供应商正凭藉其在边缘到云端编配、增强型网路安全和多站点部署方面的专业知识脱颖而出,而硬体 OEM 厂商则透过收购系统整合商来保障全生命週期收入。

条码作为一种通用的支付和合规标识符,在全通路营运中占据了 46.20% 的收入份额。随着零售店面面积的扩大,与条码列印机、成像器和标籤相关的自动识别和资料撷取(AIDC) 市场规模持续温和成长。然而,被动式超高频射频识别 (UHF-RFID) 的复合年增长率 (CAGR) 高达 12.05%,反映出强制性的单品级部署,该技术能够同时扫描多个商品并进行即时库存确认。投资报酬率源自于商品流失率的降低和交付准确率的提高,从而推动了时尚、运动用品和消费性产品类型的广泛应用。

被动式RFID成本的下降和中间件的日趋成熟将支援混合部署,其中RFID连接上游价值链运营,而条码则在商店保持面向消费者的展示。主动式RFID将在高价值资产监控领域,尤其是在航太和医疗设备,继续发挥其独特作用。嵌入式人工智慧OCR系统将实现物流和製造领域的字母数位资料撷取,从而拓展缺失或损坏标籤的应用场景。

区域分析

北美地区预计到2025年将占全球收入的34.00%,这主要得益于该地区作为早期采用者,已将产品级RFID和数位化患者安全管理制度化。沃尔玛的政策推动了嵌体转换器、印表机编码器和中介软体整合商等供应商生态系统的蓬勃发展。同时,美国正优先发展生物识别边境管制,促进了多种技术的普及应用。自动识别和资料撷取(AIDC)市场参与企业正利用更新周期和先进的仓库自动化技术,连接加拿大和墨西哥的跨境供应链。

亚太地区以11.44%的复合年增长率领先全球,主要得益于製造业自动化和国家识别计划的推进。中国作为全球最大的RFID标籤生产国,正透过出口规模经济来控制全球标籤价格。韩国、日本和印度正在实施融合生物识别识别项目,推动了对智慧卡和感测器的需求。电商巨头加速推动仓库机器人化,进一步促进了自动识别和资料撷取(AIDC)市场的应用。

监管合规性持续推动欧洲市场的稳定成长。医疗设备法规强制要求使用标准化的UDI标籤,而数位身分框架法规则为公民电子钱包奠定了基础。在法国和瑞士,整合身分和医疗保健解决方案的开发正在推动对生物识别和智慧卡的需求。 AIDC市场参与者正在调整其产品以符合严格的资料保护标准,从而在确保合规性的同时实现创新应用。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 加速全通路零售向二维/QR码转型

- UHF频段 RFID在物品级库存管理中的应用迅速成长

- 推出政府核发的电子身分证和数位健康卡

- 劳动力短缺背景下的仓库自动化

- 强制性即时低温运输追踪

- 旅行安检通道上的非接触式生物识别闸机

- 市场限制

- 旧版ERP系统之间资料格式不相容

- 将基于视觉的AIDC引入现有工厂需要较高的初始资本投入。

- 来自灰色市场的假冒低价条码扫描器

- 生物识别资料储存引发隐私反弹

- 价值/供应链分析

- 监理展望

- 扩展 ISO/IEC 19762;欧盟医疗设备法规 (MDR) UDI 截止日期 2027 年

- 技术展望

- 投资趋势分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 报价

- 硬体

- 固定式阅读器/扫描仪

- 行动计算机和手持终端机

- 印表机/编码器

- 软体

- 服务

- 整合与咨询

- 维护和支援

- 硬体

- 副产品

- 条码

- 1D

- 2D/QR

- RFID

- 被动式(低频、高频、超高频)

- 积极的

- 智慧卡

- 联繫类型

- 非接触式

- 生物识别系统

- 指纹

- 脸部认证/虹膜辨识

- 光学字元辨识(OCR)

- 其他产品

- 磁条、NFC、BLE标籤

- 条码

- 按媒体类型

- 标籤

- 标籤

- 卡片

- 按最终用户行业划分

- 製造业

- 零售与电子商务

- 运输/物流

- 医疗/製药

- BFSI

- 饭店业

- 政府/公共部门

- 能源与公共产业

- 其他的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- ASEAN

- 澳洲

- 纽西兰

- 亚太其他地区

- 中东和非洲

- 中东

- GCC

- 土耳其

- 以色列

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Zebra Technologies Corporation

- Honeywell International Inc.

- Datalogic SpA

- SICK AG

- Cognex Corporation

- Omron Corporation

- Toshiba Tec Corporation

- SATO Holdings Corporation

- Newland AIDC

- Bluebird Inc.

- Impinj Inc.

- Alien Technology LLC

- Avery Dennison Corporation

- Axicon Auto ID Ltd.

- Opticon Sensors Europe BV

- Zebex Industries Inc.

- Brady Corporation

- Thales Group(Gemalto)

- NEC Corporation

- HID Global Corporation

第七章 市场机会与未来展望

Automatic Identification And Data Capture (AIDC) market size in 2026 is estimated at USD 88.12 billion, growing from 2025 value of USD 80.05 billion with 2031 projections showing USD 142.3 billion, growing at 10.07% CAGR over 2026-2031.

The projected 62.7% cumulative expansion reflects structural digitization across manufacturing, retail, and healthcare, where automated identification has become mission-critical to throughput, compliance, and error elimination. Labor-scarcity, increasing regulatory specificity, and proven ROI for real-time visibility collectively shape a demand environment in which the Automatic Identification And Data Capture (AIDC) market is viewed as infrastructure rather than discretionary spend biometricupdate.com. Heightened adoption of 2D codes, passive UHF-RFID, and national e-ID programs widens the opportunity set for solution providers able to integrate devices, middleware, and cloud analytics within cohesive ecosystems.

Global Automatic Identification And Data Capture (AIDC) Market Trends and Insights

Accelerated Migration to 2D/QR Codes in Omnichannel Retail

Global retailers are transitioning to 2D/QR codes in preparation for the GS1 Sunrise 2027 deadline, embedding expiry dates, lot numbers, and marketing links inside a single dense symbol. Early adopters report lower food waste and smoother omnichannel experiences because richer data supports automated markdowns and dynamic customer engagement. Investment returns manifest through fewer manual interventions, higher scan accuracy at point-of-sale, and emerging interactive marketing formats that leverage consumer smartphones. Hardware vendors gain incremental unit sales as retailers replace legacy 1D scanners with imagers capable of decoding stacked symbologies, while software providers capture upgrade fees tied to POS firmware refreshes.

Surge in UHF-RFID Adoption for Item-Level Inventory

Walmart's 2024 mandate for item-level RFID tags catalyzed broad retail adoption, pushing suppliers to embed inlays that retail chains read at dock, stockroom, and shelf. Cost per passive tag has fallen below USD 0.04, enabling mainstream categories such as apparel and home goods to justify real-time inventory visibility. Deployments deliver up to 25% accuracy improvement and materially reduce out-of-stock events . Continuous reads also power loss-prevention analytics, making RFID a dual lever for margin expansion and shrink mitigation.

Inter-System Data-Format Incompatibility Across Legacy ERPs

Enterprises with 1990s-era ERP stacks struggle to ingest RFID and image data natively, often funding middleware layers that inflate project cost by up to 40%. The Automatic Identification And Data Capture (AIDC) market therefore faces elongated sales cycles because budgets must include integration, testing, and migration. In multi-site networks, disparate schema multiply complexity, generating data silos that erode promised ROI. Vendors mitigate risk by offering pre-built connectors and consulting engagements, yet the barrier remains meaningful for brown-field rollouts.

Other drivers and restraints analyzed in the detailed report include:

- Government E-ID & Digital Health-Card Roll-outs

- Labor-Scarcity-Led Warehouse Automation

- High Initial CAPEX for Vision-Based AIDC in Brown-Field Plants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware dominated 62.50% of 2025 turnover due to foundational equipment refresh across retail and healthcare. Yet pricing compression, standardization, and supply-chain contingencies squeeze margins, accelerating the pivot toward higher-margin consulting and support contracts. Vendors bundling hardware-as-a-service maintain volume while shifting mix. Consequently, Automatic Identification And Data Capture (AIDC) market competitive advantage tilts toward providers mastering hybrid revenue models that unite capital equipment with recurring service matrices.

The services layer contributed 11.64% CAGR, outpacing hardware because enterprises increasingly award outcome-based contracts covering integration, maintenance, and cloud analytics. Many tier-1 retailers migrate from capex procurement to managed services that ensure uptime for scanners, printers, and RFID portals. Services players differentiate through domain expertise in edge-to-cloud orchestration, cybersecurity hardening, and multi-site rollouts, while hardware OEMs acquire systems integrators to secure lifecycle revenue.

Barcodes retained 46.20% revenue share as ubiquitous checkout and compliance identifiers underpin omnichannel operations. The Automatic Identification And Data Capture (AIDC) market size tied to barcode printers, imagers, and labels continues to expand modestly alongside retail floor space growth. However, passive UHF-RFID expands at 12.05% CAGR, reflecting item-level mandates that unlock simultaneous multi-item scans and real-time inventory verification. ROI stems from shrink reduction and fulfillment accuracy, prompting fashion, sports equipment, and consumer electronics categories to convert.

Passive RFID's cost curve decline and middleware maturity support hybrid deployments where RFID bridges upstream supply-chain workflows while barcodes remain consumer-facing on the shelf. Active RFID preserves niche roles in high-value asset monitoring, particularly aerospace and healthcare equipment. OCR systems incorporating AI extract alphanumeric data in logistics and manufacturing, widening addressable scenarios where labels are absent or damaged.

The Automatic Identification and Data Capture (AIDC) Market Report is Segmented by Offering (Hardware, Software, Services), Product (Barcodes, RFID, Smart Cards, and More), Media Type (Labels, Tags, Cards), End-User Industry (Manufacturing, Retail and E-Commerce, and More), and by Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 34.00% of revenue in 2025 as early adopters institutionalized item-level RFID and digital patient safety. Walmart's mandate created a robust supplier ecosystem of inlay converters, printer-encoders, and middleware integrators. Meanwhile, the United States prioritizes biometric border control, reinforcing multi-technology adoption. Automatic Identification And Data Capture (AIDC) market participants capitalize on replacement cycles and advanced warehouse automation in Canada and Mexico that link cross-border supply chains.

Asia Pacific posts 11.44% CAGR, the fastest globally, fueled by manufacturing automation and national identity projects. China, the world's largest RFID tag producer, exports scale efficiencies that compress global tag pricing. South Korea, Japan, and India implement e-ID programs integrating biometrics, driving smart-card and sensor demand. E-commerce giants accelerate warehouse robotization, further expanding Automatic Identification And Data Capture (AIDC) market deployments.

Europe sustains steady growth through regulatory compliance. EU Medical Device Regulation mandates standardized UDI labeling, while the Digital Identity Framework Regulation sets a foundation for citizen wallets. France and Switzerland progress toward integrated identity-health solutions, reinforcing biometrics and smart-card volume. Automatic Identification And Data Capture (AIDC) market players align offerings with stringent data-protection norms, ensuring adoption remains compliant yet innovative.

- Zebra Technologies Corporation

- Honeywell International Inc.

- Datalogic S.p.A.

- SICK AG

- Cognex Corporation

- Omron Corporation

- Toshiba Tec Corporation

- SATO Holdings Corporation

- Newland AIDC

- Bluebird Inc.

- Impinj Inc.

- Alien Technology LLC

- Avery Dennison Corporation

- Axicon Auto ID Ltd.

- Opticon Sensors Europe B.V.

- Zebex Industries Inc.

- Brady Corporation

- Thales Group (Gemalto)

- NEC Corporation

- HID Global Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated migration to 2D/QR codes in omnichannel retail

- 4.2.2 Surge in UHF-RFID adoption for item-level inventory

- 4.2.3 Government e-ID and digital health-card roll-outs

- 4.2.4 Labor-scarcity-led warehouse automation

- 4.2.5 Real-time cold-chain tracking mandates

- 4.2.6 Contactless biometric gates in travel-security corridors

- 4.3 Market Restraints

- 4.3.1 Inter-system data-format incompatibility across legacy ERPs

- 4.3.2 High initial CAPEX for vision-based AIDC in brown-field plants

- 4.3.3 Counterfeit low-cost barcode scanners from grey markets

- 4.3.4 Privacy pushback on biometric data storage

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.5.1 ISO/IEC 19762 expansion; EU MDR UDI deadline 2027

- 4.6 Technological Outlook

- 4.7 Investment Trend Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.1.1 Fixed Readers/Scanners

- 5.1.1.2 Mobile Computers and Handhelds

- 5.1.1.3 Printers/Encoders

- 5.1.2 Software

- 5.1.3 Services

- 5.1.3.1 Integration and Consulting

- 5.1.3.2 Maintenance and Support

- 5.1.1 Hardware

- 5.2 By Product

- 5.2.1 Barcodes

- 5.2.1.1 1D

- 5.2.1.2 2D/QR

- 5.2.2 RFID

- 5.2.2.1 Passive (LF, HF, UHF)

- 5.2.2.2 Active

- 5.2.3 Smart Cards

- 5.2.3.1 Contact

- 5.2.3.2 Contactless

- 5.2.4 Biometric Systems

- 5.2.4.1 Fingerprint

- 5.2.4.2 Facial/Iris

- 5.2.5 Optical Character Recognition (OCR)

- 5.2.6 Other Products

- 5.2.6.1 Magnetic Stripe, NFC, BLE Tags

- 5.2.1 Barcodes

- 5.3 By Media Type

- 5.3.1 Labels

- 5.3.2 Tags

- 5.3.3 Cards

- 5.4 By End-user Industry

- 5.4.1 Manufacturing

- 5.4.2 Retail and E-commerce

- 5.4.3 Transportation and Logistics

- 5.4.4 Healthcare and Pharma

- 5.4.5 BFSI

- 5.4.6 Hospitality

- 5.4.7 Government and Public Sector

- 5.4.8 Energy and Utilities

- 5.4.9 Others

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Nordics

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 ASEAN

- 5.5.4.6 Australia

- 5.5.4.7 New Zealand

- 5.5.4.8 Rest of Asia Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 GCC

- 5.5.5.1.2 Turkey

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Zebra Technologies Corporation

- 6.4.2 Honeywell International Inc.

- 6.4.3 Datalogic S.p.A.

- 6.4.4 SICK AG

- 6.4.5 Cognex Corporation

- 6.4.6 Omron Corporation

- 6.4.7 Toshiba Tec Corporation

- 6.4.8 SATO Holdings Corporation

- 6.4.9 Newland AIDC

- 6.4.10 Bluebird Inc.

- 6.4.11 Impinj Inc.

- 6.4.12 Alien Technology LLC

- 6.4.13 Avery Dennison Corporation

- 6.4.14 Axicon Auto ID Ltd.

- 6.4.15 Opticon Sensors Europe B.V.

- 6.4.16 Zebex Industries Inc.

- 6.4.17 Brady Corporation

- 6.4.18 Thales Group (Gemalto)

- 6.4.19 NEC Corporation

- 6.4.20 HID Global Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment

ID卡证件阅读器市场:按阅读器类型、最终用户、应用、分销管道划分,全球预测(2026-2032年)

ID卡证件阅读器市场:按阅读器类型、最终用户、应用、分销管道划分,全球预测(2026-2032年) 医疗保健自动识别和资料收集市场:依产品、技术、应用和地区,至2036年全球预测全球坚固型工业手持阅读器市场(按类型、连接方式、作业系统、操作模式、价格范围、应用和最终用户产业划分)预测(2026-2032年)

医疗保健自动识别和资料收集市场:依产品、技术、应用和地区,至2036年全球预测全球坚固型工业手持阅读器市场(按类型、连接方式、作业系统、操作模式、价格范围、应用和最终用户产业划分)预测(2026-2032年) 自动识别系统 (AIS) 市场规模、份额和成长分析(按类别、平台、应用、最终用户和地区划分)—2026-2033 年行业预测

自动识别系统 (AIS) 市场规模、份额和成长分析(按类别、平台、应用、最终用户和地区划分)—2026-2033 年行业预测 AIS(自动识别系统):市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

AIS(自动识别系统):市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) AIT防止的全球市场:2024-2029年

AIT防止的全球市场:2024-2029年 自动识别系统 (AIS) 市场 - 全球市场规模、份额、趋势分析、机会、预测报告,2019-2030

自动识别系统 (AIS) 市场 - 全球市场规模、份额、趋势分析、机会、预测报告,2019-2030