|

市场调查报告书

商品编码

1934918

网路印刷:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Web To Print - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

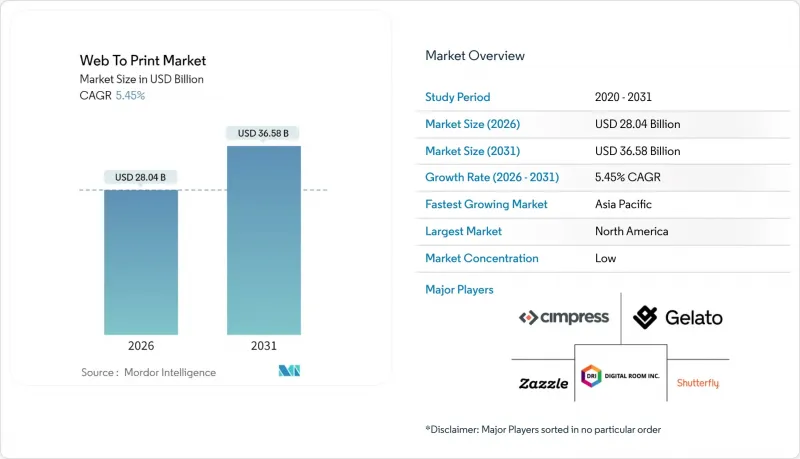

网路印刷市场预计将从 2025 年的 265.9 亿美元成长到 2026 年的 280.4 亿美元,到 2031 年将达到 365.8 亿美元,2026 年至 2031 年的复合年增长率为 5.45%。

电子商务活动的加速发展、人工智慧驱动设计工具的日趋成熟以及分散式製造网路的普及,正推动订单订单从模拟模式转变为软体定义工作流程的结构性。如今,客户期望的是小批量个人化产品的隔日送达,刺激了企业对加速印前流程和自动化色彩管理等技术的投资。主要平台供应商正积极回应,将设计编辑器直接嵌入电商平台,并将支付、校样和采购整合到单一介面。永续性措施也正加速推进,区域生产中心减少了跨境货运排放,并有助于实现可追溯性目标。竞争格局也反映出,企业正从追求纸本产品的规模经济转向追求数据规模经济,主要供应商将设计库、物流API和分析仪錶板捆绑销售,以提高客户的转换成本。

全球网路印刷市场趋势与洞察

全球电子商务卖家数量爆炸性成长

越来越多的创业者涌入电商平台,推动了平台整合式按需印刷服务的订单量成长。 Adobe 决定在 2024 年底将 Zazzle 的支付工具嵌入 Adobe Express,便是这一趋势的有力佐证。 Gelato 在 2023 年新增了超过 25,000 家店铺,目前服务覆盖 184 个国家,是无缝卖家支援如何拓展潜在需求的绝佳例证。随着微型品牌竞相推出季节性 SKU,整合设计和物流的线上印刷平台已成为不可或缺的基础设施。由此产生的网路效应将使那些能够大规模保持色彩一致性和交付可靠性的供应商受益。

高速数位印刷机的快速发展

喷墨印刷生产效率的提升和在线连续品质监控使得数位工作流程在中等批量包装生产领域能够与胶印相媲美。Konica Minolta预测,具备工业5.0能力的印刷机将融合人工智慧品管和人工监督,在不牺牲精度的前提下提高生产效率。例如,Gellert与Landa Digital Printing在2025年开展的伙伴关係就反映了商业性合理性。奈米印刷机能够提供与胶印相媲美的鲜艳色彩,而Gellert的软体则透过将作业分配到最近的认证节点来缩短週期时间并减少废弃物。这些设备技术的进步正在进一步增强行销资料、标籤和折迭纸盒等产品采用网路订购模式的经济效益。

对区域性胶印印刷商的持续偏好

注重人际关係的负责人更倾向于选择提供实物打样和灵活付款方式的本地印刷商,即使这意味着更高的单价。 Adobe 与 Zazzle 的合作引发了独立印刷商的强烈反对,他们担心绕过仲介业者,这反映了阻碍该平台普及的文化阻力。需要触觉材料验证和特殊加工的计划仍然倾向于面对面合作,这迫使线上供应商投资于样品包和颜色保证,从而打破了传统的客户忠诚度。

细分市场分析

基于模板的产品(从标准名片到易拉宝)将在2025年占据55.02%的收入份额,为设计知识有限的用户提供直觉的入门途径。该领域受益于人工智慧布局引擎,这些引擎可自动将徽标、文字和图像定位到预先已通过核准的网格中,从而降低放弃率,并赋予专利经营更大的品牌控制权。虽然完全可自订的工作流程可能不太常见,但预计到2031年,随着电力用户对更高编辑柔软性和可变资料处理能力的需求,其复合年增长率将达到7.15%。模板系统越来越融入人工智慧提案层,模糊了类别界限,并在保持品牌一致性的同时,实现了几乎无限的组合。因此,随着更先进的工具缩短设计时间,分配给客製化计划的网路印刷市场规模将会扩大。

相较之下,纯粹的空白编辑器需要高超的创造性技能,因此仍然受到设计专业人士和利基製造商的青睐。交叉销售行为表明,买家往往从模板入手,随着信心的增强,再转向高度客製化的产品,这种模式能够延长客户的终身价值。合规相关领域,尤其是食品和製药行业,更倾向于使用结构化模板来确保批号和过敏原标籤的准确性,这进一步巩固了引导式设计的长期重要性。

区域分析

到2025年,北美将占全球收入的41.20%,这主要得益于该地区密集的中小型企业丛集,这些企业依赖承包印刷平台来製作宣传材料。该地区成熟的小包裹网路、极具吸引力的运费以及较高的宽频普及率,促进了频繁的重复订购和后续加工升级的提升销售。食品包装主导法规(已在FDA规定的期限内实施)正在加速可变数据标籤的普及,并提高平均订单频率。在加拿大,双语包装强制要求使用相同素材的在地化版本,这推动了业务的增量成长;而在墨西哥,近岸外包趋势正将包装原型製作转移到服务于跨境品牌的网路供应商。

亚太地区预计到2031年将以7.25%的复合年增长率成长,表现突出,这反映了印度和东南亚地区数位化进程的快速发展。在中国,国家支持的电子商务生态系统和完善的数位付款基础为线上店铺插件提供了沃土,推动业务向广东和浙江等区域中心转移。随着低成本智慧型手机和UPI支付的普及,印度的微型、微企业(MSME)越来越多地使用在地化入口网站采购行销传单和快递信封。日本买家重视色彩精准度和FSC认证材料,日益要求供应商提供色域一致性和永续采购认证。

欧洲印刷业正经历温和的扩张,这得益于严格的环境指令,这些指令鼓励即时生产模式。欧盟的反森林砍伐法规要求印刷企业追溯纸张资料的来源,这促使企业采用可自动产生监管链文件的云端连接管理资讯系统(MIS)。德国、法国和英国主导市场,因此需要针对每个地区进行细緻的在地化,从符合GDPR的资料流到英国脱欧后的海关文件,无一例外。碳会计在斯堪地那维亚国家是优先事项,有些平台会为每笔订单计算二氧化碳排放量,创造了一个利基市场。东欧的印刷厂正将成本竞争力与不断提升的技术能力相结合,以吸引西方买家的额外订单,这些买家寻求的是欧洲製造的产品。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球电子商务商家的爆炸性成长

- 高速数位印刷机的快速发展

- 对大规模客製化行销材料的需求日益增长

- 中小企业的SaaS订阅成本正在下降

- AI驱动的设计自动化工作流程

- 按需印刷中的永续性倡议

- 市场限制

- 继续偏好区域性胶印印刷商

- 网路安全和资料隐私合规成本

- 有关纸张和油墨使用的环境法规

- 开放原始码模板的商品化对利润率带来压力

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 产业间竞争

第五章 市场规模与成长预测

- 依产品类型

- 完全可定制

- 基于模板

- 透过使用

- 服饰

- 行销资料

- 名片

- 包装

- 摄影集和相簿

- 标籤和贴纸

- 其他用途

- 按部署模式

- 本地部署

- 基于云端的

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 南美洲其他地区

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cimpress plc

- Shutterfly, LLC

- Zazzle Inc.

- Digital Room, LLC

- Overnight Prints, Inc.

- Gelato ASA

- MOO Print Ltd.

- CustomInk, LLC

- Snapfish LLC

- CEWE Stiftung & Co. KGaA

- PrintPlace, LLC

- Mixam Ltd.

- Redbubble Ltd.

第七章 市场机会与未来展望

The web-to-print market is expected to grow from USD 26.59 billion in 2025 to USD 28.04 billion in 2026 and is forecast to reach USD 36.58 billion by 2031 at 5.45% CAGR over 2026-2031.

Accelerating e-commerce activity, the maturation of AI-driven design tools, and the spread of distributed manufacturing networks reinforce a structural migration away from analog job intake and toward software-defined workflows. Customer expectations now center on next-day delivery of short-run, personalized pieces, stimulating technology investments that compress pre-press cycles and automate color management. Major platform providers respond by embedding design editors directly into e-commerce storefronts, consolidating payment, proofing, and procurement on one screen. Sustainability commitments add further momentum, as local production nodes reduce cross-border freight emissions and support the objectives of traceability. Competitive dynamics reflect a pivot toward scale economies in data, not paper, with leading vendors bundling design repositories, shipping APIs, and analytics dashboards to widen switching costs.

Global Web To Print Market Trends and Insights

Explosive Growth of Global E-commerce Sellers

The widening pool of marketplace entrepreneurs fuels order volumes for platform-integrated print-on-demand services, as evidenced by Adobe's decision to embed Zazzle checkout tools inside Adobe Express in late 2024. Gelato on-boarded more than 25,000 new store owners in 2023 and now serves 184 countries, illustrating how friction-free seller enablement amplifies addressable demand. As microbrands rush to publish seasonal SKU drops, web-to-print portals that combine design and logistics become indispensable infrastructure. The resulting network effects reward providers that can uphold color consistency and shipping reliability at scale.

Rapid Advances in High-Speed Digital Presses

Inkjet productivity gains and inline quality monitoring now allow digital workflows to compete against offset for mid-length packaging runs. Konica Minolta projects that Industry 5.0 press configurations will merge AI quality control with human oversight to raise throughput without sacrificing precision. Partnerships, such as Gelato's 2025 tie-up with Landa Digital Printing, demonstrate the commercial rationale: Nanographic presses provide offset-comparable vibrancy, while Gelato's software allocates jobs to the nearest certified node, reducing cycle time and waste. These equipment advances broaden the economic case for shifting marketing collateral, labels, and folding cartons to web-based ordering.

Persisting Preference for Local Offset Printers

Relationship-centric buyers often choose neighborhood print shops that offer tangible proofing and flexible payment terms, even when unit costs are higher. Adobe's venture with Zazzle sparked backlash among independent printers who fear being disintermediated, illustrating cultural resistance that slows platform penetration. Projects requiring tactile substrate reviews or specialty embellishments still favor in-person collaboration, obliging online vendors to invest in sample kits and color guarantees to erode legacy loyalties.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Mass-Customized Marketing Collateral

- AI-Driven Design-Automation Workflows

- Cyber-security and Data-Privacy Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Template-based items, ranging from standard business cards to pull-up banners, delivered 55.02% of 2025 revenue, providing an intuitive on-ramp for users with limited design expertise. The segment benefits from AI layout engines that auto-fit logos, text, and images into pre-approved grids, lowering abandonment rates and extending brand governance controls for franchisors. Fully customizable workflows trail in volume but register a healthy 7.15% CAGR to 2031 as power users demand granular editing flexibility and variable-data functionality. Template systems are increasingly incorporating AI suggestion layers, blurring categorical lines and enabling nearly limitless permutations while maintaining brand consistency. Consequently, the web-to-print market size allocated to bespoke projects is set to escalate as tool sophistication reduces design time.

In contrast, purely blank-canvas editors require higher creative skill and remain favored by design professionals and niche manufacturers. Cross-selling behaviors reveal that purchasers start with templates but migrate to advanced custom products as confidence builds, a pattern that lengthens customer lifetime value. Compliance-linked sectors, notably food and pharmaceutical, prefer structured templates to ensure the inclusion of lot codes and allergen statements, thereby cementing the long-term relevance of guided designs.

The Web To Print Market Report is Segmented by Product Type (Fully Customizable, and Template-Based), Application (Apparel, Marketing Materials, Business Cards, Packaging, Photo Books and Albums, Labels and Stickers, and More), Deployment Model (On-Premise, and Cloud-Based), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 41.20% of global revenue in 2025, driven by the presence of dense clusters of small businesses that rely on turnkey print portals for promotional materials. The region's mature parcel networks, attractive shipping rates, and high broadband penetration encourage frequent re-orders and upsell of finishing upgrades. Regulation-driven traceability for food packaging, enforced within FDA timelines, accelerates the adoption of variable-data labels, thereby boosting the average order frequency. Canada contributes incremental growth through bilingual packaging mandates that necessitate localized versions of the same asset, while Mexican near-shoring trends pull packaging prototypes toward web-enabled suppliers serving cross-border brands.

Asia Pacific stands out with a 7.25% forecast CAGR through 2031, reflecting leapfrog digitization in India and Southeast Asia. China's state-supported e-commerce ecosystem and extensive digital payment rails create fertile ground for storefront plug-ins that route jobs to regional hubs in Guangdong and Zhejiang. Indian MSMEs, empowered by low-cost smartphones and UPI transactions, increasingly use localized portals to procure marketing leaflets and courier sleeves. Japanese buyers emphasize color accuracy and FSC-certified substrates, pushing suppliers to prove gamut consistency and sustainable sourcing credentials.

Europe registers moderate expansion anchored in stringent environmental directives that reward just-in-time production models. The EU Deforestation Regulation compels printers to trace paper inputs back to origin, favoring cloud-connected MIS that automate chain-of-custody documentation. Germany, France, and the United Kingdom make up the lion's share, each demanding nuanced localization, whether GDPR-compliant data flows or post-Brexit customs documentation. Scandinavia prioritizes carbon accounting, creating niches for platforms offering embedded CO2 calculators per order. Eastern European print plants bind cost competitiveness with growing technical sophistication, attracting contractual overflow from Western buyers seeking continentally sourced merchandise.

- Cimpress plc

- Shutterfly, LLC

- Zazzle Inc.

- Digital Room, LLC

- Overnight Prints, Inc.

- Gelato ASA

- MOO Print Ltd.

- CustomInk, LLC

- Snapfish LLC

- CEWE Stiftung & Co. KGaA

- PrintPlace, LLC

- Mixam Ltd.

- Redbubble Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Explosive growth of global e-commerce sellers

- 4.2.2 Rapid advances in high-speed digital presses

- 4.2.3 Rising demand for mass-customised marketing collateral

- 4.2.4 Declining SaaS subscription costs for SMBs

- 4.2.5 AI-driven design-automation workflows

- 4.2.6 Sustainability push for just-in-time print-on-demand

- 4.3 Market Restraints

- 4.3.1 Persisting preference for local offset printers

- 4.3.2 Cyber-security and data-privacy compliance costs

- 4.3.3 Environmental regulations on paper and ink usage

- 4.3.4 Open-source template commoditisation squeezing margins

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Fully Customisable

- 5.1.2 Template-based

- 5.2 By Application

- 5.2.1 Apparel

- 5.2.2 Marketing Materials

- 5.2.3 Business Cards

- 5.2.4 Packaging

- 5.2.5 Photo Books and Albums

- 5.2.6 Labels and Stickers

- 5.2.7 Other Applications

- 5.3 By Deployment Model

- 5.3.1 On-premise

- 5.3.2 Cloud-based

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cimpress plc

- 6.4.2 Shutterfly, LLC

- 6.4.3 Zazzle Inc.

- 6.4.4 Digital Room, LLC

- 6.4.5 Overnight Prints, Inc.

- 6.4.6 Gelato ASA

- 6.4.7 MOO Print Ltd.

- 6.4.8 CustomInk, LLC

- 6.4.9 Snapfish LLC

- 6.4.10 CEWE Stiftung & Co. KGaA

- 6.4.11 PrintPlace, LLC

- 6.4.12 Mixam Ltd.

- 6.4.13 Redbubble Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment