|

市场调查报告书

商品编码

1937252

汽车内装:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Interior - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

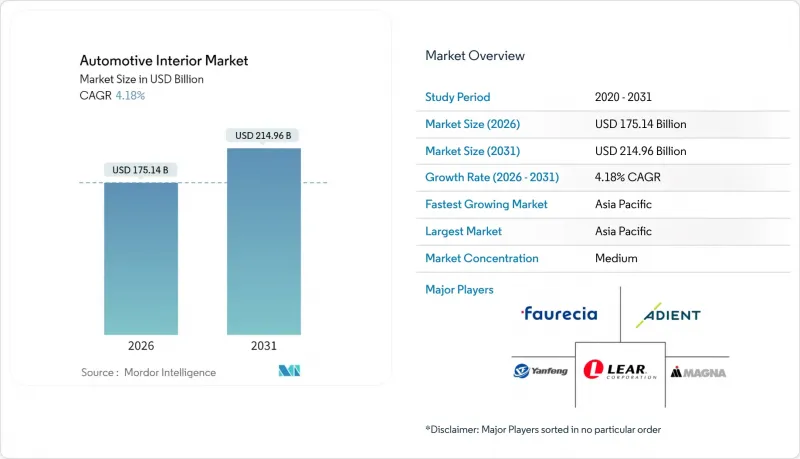

预计到 2026 年,汽车内装市场规模将达到 1,751.4 亿美元,高于 2025 年的 1,681.1 亿美元,预计到 2031 年将达到 2,149.6 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 4.18%。

在这稳步扩张的背后,是更深层的变革。诸如软体定义驾驶座、生物识别监控和永续材料等技术正从利基选择走向主流应用。汽车製造商正围绕高密度显示器和中央运算单元重新设计座舱布局,而供应商则在拓展与空中升级功能相关的订阅收入。在电动车平台上,随着静音车辆配置的日益完善,高端表面处理、环境照明和健康功能的重要性也与日俱增。亚太地区已引领这些升级的步伐,其规模优势促进了本地快速改装。同时,售后市场需求仍然强劲,车队营运商和零售商持续用长寿命、可数位化升级的模组替换磨损的装饰件,缓解了人们对共享出行会缩短更换週期的担忧。

全球汽车内装市场趋势与洞察

向软体定义汽车和高清显示器的转变

以软体为中心的设计将座舱功能与固定硬体分离,并透过安全的空中昇级实现持续升级。大陆集团目前提供的驾驶座解决方案配备三个或更多超高分辨率显示屏,并由性能超过 1000 DMIPS 的处理器驱动。高通骁龙数位底盘为众多车型提供动力,展现了半导体製造商对座舱电子设备的影响力。将电子元件、软体和使用者体验设计结合的供应商,即使在产品停产后也能透过新功能获得收益,从而将成本加成合约转变为持续收入模式。预测性维护和基于使用量的保险是基于相同数据基础,进一步拓展了车内感测器套件的商业价值。传统的纯零件公司若不与数位人才合作或收购数位人才,可能面临失去竞争优势的风险。

中国和东协对高端和电动SUV的需求不断增长

在中国销售的高阶电动SUV的内装组件成本比内燃机(ICE)车型高出约20%。这主要是由于环境照明、多萤幕资讯娱乐系统和先进的监控系统等因素造成的。蔚来和小鹏等公司甚至在中阶车型上也开始标配生物识别感测器,这促使全球供应商在常州、武汉和罗勇等地建立先进模组的本地生产基地。泰国快速成长的电动车出口基地吸引了座椅、内装和驾驶座製造商落脚东南亚,帮助日本、韩国和西方的汽车製造商透过本地组装缩短前置作业时间。东协地区的中等收入家庭在购买首款SUV时越来越重视车内体验,这促使当地一级供应商在曼谷和胡志明市附近建立色彩、材料和饰面工作室。高端内装的高毛利率降低了价格敏感性,使供应商能够更快地收回研发成本。本地化还可以保护供应商免受跨境零件可能面临的地缘政治关税的影响。

车载资讯娱乐系统晶片组持续短缺

汽车处理器的前置作业时间仍维持在26至52週之间,这对内装生产计画造成了不利影响。这迫使汽车製造商优先考虑安全控制设备,而非资讯娱乐主机。虽然采用晶片无关架构的一级供应商可以降低部分风险,但规模较小的供应商在与大型消费性电子公司谈判时处于劣势。供应商也以现货价格高峰囤积半导体元件,占用营运资金并挤压利润空间。在新兴市场,注重成本的汽车製造商正在简化内装规格,并推迟多摄影机监控系统的引入。这种短缺正在加速垂直整合,像大陆集团和采埃孚这样的公司正在增加内部ASIC设计,以确保策略性元件的供应。在亚利桑那州、萨克森州和槟城的新工厂全面运作之前,显示器密集型内饰的短期增长可能仍将受到限制。

细分市场分析

到2025年,乘用车将占总收入的66.13%,这表明该细分市场在汽车内装市场中占据主导地位。电动乘用车是成长最快的细分市场,复合年增长率达4.21%,这得益于车载技术的进步提升了单车价值。电动车内装市场规模的成长得益于诸多优势,例如宽敞平坦的地板释放了储物空间、舒适的座椅以及全景显示器。轻型商用车的成长与宅配的扩张密切相关,但其驾驶室的改进侧重于实用性,因此成长要素主要由强制性的驾驶员监控系统而非豪华配置驱动。由于中型和重型卡车更容易运作,供应商正在向车队采购商提案耐用面料和抗菌表面。

电气化浪潮使得供应商能够推出一些先前成本高昂的健康功能,例如主动降噪和空气离子产生器。虽然特斯拉在极简主义布局方面引领潮流,但老牌汽车製造商已经证明,市场对配备多萤幕丛集的坚固耐用的开关设备仍然有需求。欧盟新规强制要求重型卡车安装车内监视录影机,这进一步推高了对乘员监控套件的需求。随着时间的推移,车厢内部的差异化将从机械工艺转向软体驱动的个人化定制,并在车辆的整个生命週期内持续更新,从而拓展售后市场的可能性,甚至惠及商用车队。

即使到了2025年,内燃机汽车仍将继续主导整个汽车内装市场,占72.47%的销售份额。然而,电动车车型将维持4.27%的年增长率,并凭藉先进的设计语言主导。随着电池布局的改进,无需再设置传动轴通道,因此,安装在地板上的传感器模组和带照明的储物格将变得越来越重要。车内噪音的降低将使乘客更容易察觉到异响和麵板缝隙,从而对製造公差提出更高的要求,进而扩大电动车专用内装组件的市场份额。混合动力汽车属于过渡产品,儘管纯电动续航里程有限,但通常会透过更大的显示器和更高级的布料来为其更高的价格辩护。

电动车架构推动了对即时能量视觉化的需求,促使供应商重新设计丛集图形和中控台用户体验,以显示充电数据。车厢静谧性凸显了声学品质的重要性,促使汽车製造商指定使用高功率扬声器和隔振垫,进一步增加了每辆车的设备配置。电池寿命的温度控管影响暖通空调管道系统,这为在双区和三区自动空调方面拥有经验的供应商提供了竞争优势。

区域分析

预计到2025年,亚太地区将占全球营收的37.43%,并保持最快成长速度,到2031年复合年增长率将达到4.31%。中国本土品牌甚至在紧凑型SUV中也配备了多萤幕驾驶座和健康座椅,提高了消费者在内饰方面的平均支出水平。中国当地不断扩大的产能和区域自由贸易区的设立,促使延锋、麦格纳和福比亚等公司加大本地研发投入,并在OEM设计中心附近建立材料研究实验室。泰国正在扩大面向澳洲和中东市场的电动车组装,这促进了座椅框架、内饰和萤幕等二级供应商集群的形成。日本和韩国正越来越多地采用先进的感测器演算法进行乘员监控,并在全球授权软体。印尼和越南消费者可支配收入的成长推动了对舒适性配置的需求,即使在宏观经济波动的情况下,也保持了成长势头。

北美被视为第二大收入来源。在美国,随着联邦机动车辆安全标准 (FMVSS) 覆盖范围的扩大,驾驶监控要求也随之提高,感测器整合标准也随之提高。皮卡和SUV的流行扩大了车内面积,刺激了高利润的座椅翻新和资讯娱乐系统升级。加拿大严酷的冬季促使方向盘和座椅加热功能普及,进一步推动了车辆配置的成长。墨西哥具有竞争力的人事费用和美墨加协定 (USMCA) 的原产地规则,使得汽车内饰製造业蓬勃发展,既满足了本地市场需求,也促进了出口。

严格的环境和安全法规将维持欧洲的适度成长。欧盟通用安全法规要求所有新车自2026年起必须配备被动式驾驶员监控系统,这将确保对车内摄影机的需求。德国高端品牌在高解析度OLED丛集和再生复合材料的试验方面主导,这些技术使得在东欧大规模生产车型的组装更具成本效益。监管机构对循环经济的关注正迫使供应商采用闭合迴路材料流。英国脱欧后的供应链重组将为那些能够无关税风险地向英国工厂供货的欧洲大陆製造商创造市场份额机会。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 向软体定义汽车和高清显示器的转变

- 中国和东协地区对高端SUV和电动SUV的需求不断增长

- 可透过空中昇级的驾驶座架构

- 汽车製造商的碳排放目标要求使用轻质、永续材料

- 采用车载健康、安全和生物识别法规(GSR-EU、NCAP)

- 固态连续照明作为品牌差异化优势

- 市场限制

- 车载资讯娱乐系统晶片组持续短缺

- 共享出行车队更新周期的缩短给售后市场带来了压力。

- 聚氨酯和生物基聚合物原料价格上涨

- 人机介面软体堆迭中知识产权的碎片化和标准化问题

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 依推进类型

- 内燃机(ICE)

- 电动车(EV)

- 依组件类型

- 仪表板和驾驶座模组

- 资讯娱乐和连网显示器

- 座椅系统

- 室内照明(间接照明、功能性照明)

- 车门和车身装饰板

- 暖通空调和热舒适性

- 内部装潢建材/表面材料

- 驾驶员/乘客监控系统

- 其他部分

- 依材料类型

- 合成皮革(PU、PVC)

- 真皮

- 织物和纺织品

- 塑胶和复合材料

- 天然及可回收材料

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adient plc

- Faurecia SE

- Lear Corporation

- Magna International Inc.

- Yanfeng Automotive Interiors

- Grupo Antolin

- Toyota Boshoku Corp.

- Hyundai Mobis Co.

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Continental AG

- DENSO Corp.

- Valeo SA

- JVCKENWOOD Corp.

- Pioneer Corp.

- Visteon Corp.

- Grammer AG

- Haartz Corporation

- Huayu Automotive Systems(HASCO)

- Seoyon E-Hwa

第七章 市场机会与未来展望

Automotive Interior Market size in 2026 is estimated at USD 175.14 billion, growing from 2025 value of USD 168.11 billion with 2031 projections showing USD 214.96 billion, growing at 4.18% CAGR over 2026-2031.

This measured expansion conceals a more profound transformation as software-defined cockpits, biometric monitoring, and sustainable materials move from niche options to mainstream specifications. Automotive OEMs re-engineer cabin layouts around high-density displays and centralized compute units, while suppliers explore subscription revenue tied to over-the-air feature upgrades. Electric vehicle platforms add further content per car because silent cabins heighten the importance of premium surfaces, ambient lighting, and wellness features. The Asia-Pacific region already sets the pace for these upgrades, and its volume advantage encourages fast local iteration. Simultaneously, aftermarket demand stays resilient because fleet operators and retail owners keep refreshing worn trim with longer-life, digitally upgradable modules, dampening fears that shared mobility would erode replacement cycles.

Global Automotive Interior Market Trends and Insights

Shift Toward Software-Defined Vehicles & HD Displays

Software-centric design decouples cabin functions from fixed hardware and allows continuous upgrades through secure over-the-air patches. Continental now delivers cockpit domains that host three or more ultra-high-resolution displays driven by processors exceeding 1,000 DMIPS . Qualcomm's Snapdragon Digital Chassis powers numerous vehicle models and underscores how semiconductor players influence cabin electronics . Suppliers that blend electronics, software, and user-experience design monetize new features long after production, reshaping cost-plus contracts into recurring revenue frameworks. Predictive maintenance and usage-based insurance ride on the same data backbone, expanding the business case for interior sensor suites. Traditional component-only firms risk erosion unless they partner or acquire digital talent.

Rising Demand for Premium & Electric SUVs in China & ASEAN

Electric premium SUVs sold in China carry a one-fifth higher interior bill-of-materials than their ICE peers, mainly due to ambient lighting, multi-screen infotainment, and advanced monitoring. Companies like NIO and XPeng have normalized biometric sensing even in mid-range trims, prompting global suppliers to localize advanced modules in Changzhou, Wuhan, and Rayong. Thailand's fast-growing EV export base pulls seat, trim, and cockpit makers into Southeast Asia, lowering lead times for Japanese, Korean, and Western OEMs that assemble there. ASEAN's middle-income families increasingly weigh the in-cabin experience when buying a first SUV, so local Tier-1s invest in color, material, and finish studios close to Bangkok and Ho Chi Minh City. The high gross margins on premium interiors soften price sensitivity, letting suppliers recoup R&D more quickly. Localization further shields vendors from potential geopolitical tariffs on cross-border components.

Persistent Chipset Shortages in the Infotainment Domain

Lead times for automotive-grade processors still range from 26 to 52 weeks, hurting interior build schedules and forcing OEMs to prioritize safety controllers over infotainment head units. Tier-1s that adopt chip-agnostic architectures buffer some risk, yet smaller players lose allocation clout against consumer electronics giants. Margins narrow because suppliers stockpile semiconductors at peak spot prices, tying up working capital. In emerging markets, cost-sensitive OEMs downgrade cabin specs or postpone rollouts of multi-camera monitoring. The shortage accelerates vertical integration as Continental, ZF, and others add internal ASIC design to secure strategic components. Until new fabs in Arizona, Saxony, and Penang ramp, the constraint will continue to clip near-term upside for display-heavy interiors.

Other drivers and restraints analyzed in the detailed report include:

- Over-The-Air Upgradable Cockpit Architectures

- Lightweight Sustainable Materials Mandated by OEM Carbon Targets

- High Raw-Material Volatility for PU & Bio-Based Polymers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars sustained 66.13% of overall revenue in 2025, showing the segment's scale advantage in the automotive interior market. Electric passenger cars represent the fastest growing slice at a 4.21% CAGR as higher in-cabin technology density lifts basket value per unit. The automotive interior market size for electric cars benefits from wide, flat floors that free up storage modules, lounge-style seating, and panoramic display surfaces. Light commercial vehicles track parcel delivery expansion, but cabin upgrades stay utilitarian, so growth stems mainly from mandated driver monitoring rather than luxury trim. Medium and heavy trucks remain sensitive to downtime; therefore, suppliers pitch durable fabrics and antimicrobial surfaces to fleet buyers.

The electrification wave lets suppliers insert wellness functions such as active noise cancellation and air ionizers that were previously cost-prohibitive. Tesla sparked minimalist layouts, yet legacy OEMs show there is still an appetite for robust switchgear coupled with multi-screen clusters. New EU rules that require inward-facing cameras on heavy trucks generate incremental demand for occupant monitoring kits. Over time, cabin differentiation shifts from mechanical craftsmanship to software-driven personalization that updates throughout the vehicle's life, extending aftermarket potential even in commercial fleets.

Internal combustion vehicles still accounted for 72.47% revenue in 2025, anchoring volumes across the automotive interior market. Nonetheless, electric models grow 4.27% annually and dictate forward design language. Battery layouts remove transmission tunnels, so floor-mounted sensor pods and illuminated storage compartments gain prominence. The automotive interior market share for EV-specific components expands as low cabin noise raises occupant awareness of rattles and panel gaps, forcing tighter manufacturing tolerances. Hybrids serve as transition products and often bundle larger displays and premium fabrics to justify higher price tags despite modest pure-electric range.

EV architecture increases demand for real-time energy visualizations, prompting suppliers to reconfigure cluster graphics and center-stack UX to display charging data. Silence inside the cabin accentuates audio quality and encourages OEMs to specify higher wattage speakers and vibration-damping mats, further boosting content per car. Thermal management for battery longevity influences HVAC routing, giving suppliers experienced in dual-zone and tri-zone climate control a competitive edge.

The Automotive Interior Market Report is Segmented by Vehicle Type (Passenger Cars and More), Propulsion Type (Internal-Combustion Engine and Electric Vehicle), Component Type (Instrument Panels & Cockpit Modules and More), Material Type (Synthetic Leather, Genuine Leather, Fabrics & Textiles, and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific delivered 37.43% of global revenue in 2025 and will post the fastest 4.31% CAGR through 2031. China's indigenous brands fit multi-screen cockpits and wellness seats even on compact SUVs, lifting average interior spend. Mainland volume plus regional free-trade zones entice Yanfeng, Magna, and FORVIA to localize R&D and build material labs close to OEM design centers. Thailand scales EV assembly for export to Australia and the Middle East, catalyzing new Tier-2 clusters that supply seat frames, trims, and screens. Japan and South Korea use advanced sensor algorithms for occupant monitoring, often licensing software globally. Rising disposable incomes across Indonesia and Vietnam elevate demand for comfort features, sustaining growth even if macroeconomics fluctuate.

North America stands as the second-largest revenue pool. The United States pushes driver-monitoring requirements through the expanding FMVSS docket, raising baseline sensor content. Pickup and SUV popularity inflates cabin surface area, which favors high-margin upholstery and infotainment upgrades. Canada's harsh winters boost heated steering wheel usage and seat usage, further enlarging vehicle content. Mexico's competitive labor costs and USMCA rules-of-origin keep interior manufacturing vibrant for regional and export volumes.

Europe maintains moderate growth backed by stringent green and safety mandates. The EU General Safety Regulation obliges all new cars to include passive driver monitoring from 2026, guaranteeing demand for inward-facing cameras. Germany's premium marques lead experimentation with high-resolution OLED clusters and recycled composites, while Eastern Europe offers cost-effective assembly for volume models. Regulatory focus on circularity pushes suppliers to adopt closed-loop material flows. Supply-chain rerouting post-Brexit opens share opportunities for continental producers who can supply UK plants without tariff risk.

- Adient plc

- Faurecia SE

- Lear Corporation

- Magna International Inc.

- Yanfeng Automotive Interiors

- Grupo Antolin

- Toyota Boshoku Corp.

- Hyundai Mobis Co.

- Panasonic Holdings Corp.

- Robert Bosch GmbH

- Continental AG

- DENSO Corp.

- Valeo SA

- JVCKENWOOD Corp.

- Pioneer Corp.

- Visteon Corp.

- Grammer AG

- Haartz Corporation

- Huayu Automotive Systems (HASCO)

- Seoyon E-Hwa

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Software-Defined Vehicles & HD Displays

- 4.2.2 Rising Demand For Premium & Electric SUVs In China & Asean

- 4.2.3 Over-The-Air Upgradable Cockpit Architectures

- 4.2.4 Lightweight Sustainable Materials Mandated By OEM Carbon Targets

- 4.2.5 Adoption Of In-Cabin Health, Safety & Biometrics Regulations (GSR-EU, NCAP)

- 4.2.6 Solid-State Ambient Lighting As A Brand Differentiator

- 4.3 Market Restraints

- 4.3.1 Persistent Chipset Shortages In Infotainment Domain

- 4.3.2 Lower Refresh-Cycle In Shared-Mobility Fleets Squeezing Aftermarket

- 4.3.3 High Raw-Material Volatility For PU & Bio-Based Polymers

- 4.3.4 IP- & Standards-Fragmentation For HMI Software Stacks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.2 By Propulsion Type

- 5.2.1 Internal-Combustion Engine (ICE)

- 5.2.2 Electric Vehicle (EV)

- 5.3 By Component Type

- 5.3.1 Instrument Panels & Cockpit Modules

- 5.3.2 Infotainment & Connected Displays

- 5.3.3 Seating Systems

- 5.3.4 Interior Lighting (Ambient, Functional)

- 5.3.5 Door & Body Trim Panels

- 5.3.6 HVAC & Thermal Comfort

- 5.3.7 Upholstery & Surface Materials

- 5.3.8 Driver / Occupant Monitoring Systems

- 5.3.9 Other Components

- 5.4 By Material Type

- 5.4.1 Synthetic Leather (PU, PVC)

- 5.4.2 Genuine Leather

- 5.4.3 Fabrics & Textiles

- 5.4.4 Plastics & Composites

- 5.4.5 Natural & Recycled Materials

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle-East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 Egypt

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle-East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Adient plc

- 6.4.2 Faurecia SE

- 6.4.3 Lear Corporation

- 6.4.4 Magna International Inc.

- 6.4.5 Yanfeng Automotive Interiors

- 6.4.6 Grupo Antolin

- 6.4.7 Toyota Boshoku Corp.

- 6.4.8 Hyundai Mobis Co.

- 6.4.9 Panasonic Holdings Corp.

- 6.4.10 Robert Bosch GmbH

- 6.4.11 Continental AG

- 6.4.12 DENSO Corp.

- 6.4.13 Valeo SA

- 6.4.14 JVCKENWOOD Corp.

- 6.4.15 Pioneer Corp.

- 6.4.16 Visteon Corp.

- 6.4.17 Grammer AG

- 6.4.18 Haartz Corporation

- 6.4.19 Huayu Automotive Systems (HASCO)

- 6.4.20 Seoyon E-Hwa

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

全球及中国汽车产业消费后树脂(PCR)产业调查及「十五」规划分析报告(2026-2032年)

全球及中国汽车产业消费后树脂(PCR)产业调查及「十五」规划分析报告(2026-2032年) 日本汽车内装市场规模、份额、趋势和预测:按零件、材料、车辆类型和地区划分,2026-2034年

日本汽车内装市场规模、份额、趋势和预测:按零件、材料、车辆类型和地区划分,2026-2034年 汽车内装市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、零件、地区及竞争格局划分,2021-2031年)

汽车内装市场-全球产业规模、份额、趋势、机会及预测(依车辆类型、零件、地区及竞争格局划分,2021-2031年) 汽车开关按钮市场按产品类型、操作模式、应用、最终用途和分销管道划分-全球预测,2026-2032年汽车木饰市场按材料类型、表面处理类型、车辆类型、最终用户和应用划分,全球预测(2026-2032)

汽车开关按钮市场按产品类型、操作模式、应用、最终用途和分销管道划分-全球预测,2026-2032年汽车木饰市场按材料类型、表面处理类型、车辆类型、最终用户和应用划分,全球预测(2026-2032) 汽车绒面革:全球市占率排名、总销售量与需求预测(2025-2031年)

汽车绒面革:全球市占率排名、总销售量与需求预测(2025-2031年) 2025年全球汽车超细绒面革市场

2025年全球汽车超细绒面革市场 全球汽车电动座椅开关市场全球汽车触控萤幕控制系统市场全球汽车内装件市场

全球汽车电动座椅开关市场全球汽车触控萤幕控制系统市场全球汽车内装件市场