|

市场调查报告书

商品编码

1937254

建筑涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

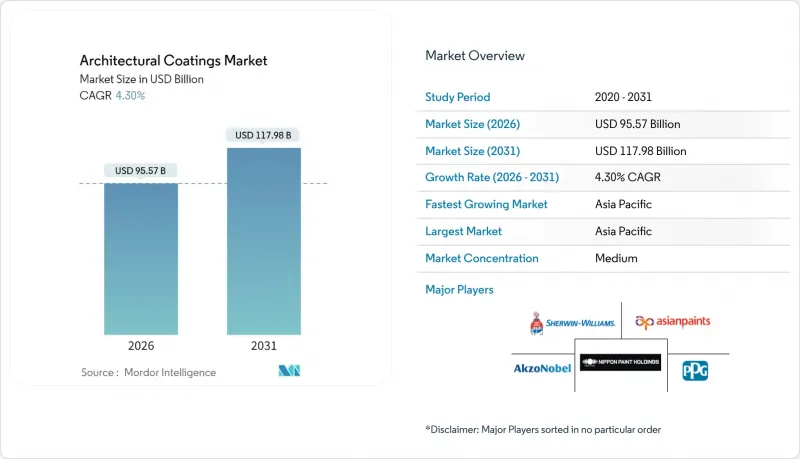

预计到 2026 年,建筑涂料市场规模将达到 955.7 亿美元,高于 2025 年的 916.2 亿美元。

预计到 2031 年,市场规模将达到 1,179.8 亿美元,2026 年至 2031 年的复合年增长率为 4.3%。

低VOC配方法规的要求、水性涂料技术的加速普及以及老旧住宅存量维修的需求,共同支撑着这一稳步增长的趋势。美国炎热气候州强制性的「冷屋顶」法规推动了反射涂料的普及,而中国二、三线城市正迅速转向水性涂料,推动全球产品结构向永续化学技术转型。同时,劳动力短缺和环氧树脂原料价格波动挤压了利润空间,促使企业投资于省力施工工具和智慧涂料技术。

全球建筑涂料市场趋势及展望

美国老旧住宅存量的维修需求激增

由于房屋抵押贷款居高不下,住宅更倾向于维修房屋而非搬迁,这推动了对符合加州第24号法规规定的具有冷屋顶的优质外墙涂料的需求。由于涂料的使用已纳入建筑许可流程,而非可选项,因此合规性带来了可预测的需求。洛杉矶的绿色建筑规范规定了太阳反射率指数(SRI)阈值,当地公共产业也提供每平方英尺0.20美元的补贴,鼓励计划预算转向更高价值的配方。人口老化加剧,越来越多的人选择居家养老,延长了重新粉刷的周期,并促使人们投资于能够减少长期维护的长寿命系统。与新建项目相比,维修支出波动较小,製造商可以从中受益,从而能够制定更稳定的生产计画。专业供应商正利用这一转变,将色彩视觉化应用程式和承包商配对服务相结合,以简化消费者的决策过程。

美国炎热气候州强制实施冷屋顶标准

加州和国际节能规范 (IECC) 要求 1-3 区的低坡度屋顶在老化后太阳反射率达到 0.55 或更高,热辐射率达到 0.75 或更高,这鼓励建筑商采用中车 (CRRC) 认证的产品。此认证项目缩小了竞争格局,并鼓励研发高反射颜料和耐用弹性黏合剂。由于与许可证申请挂钩,供应商能够更准确地预测需求并协商长期原材料合约。空气间隔屋顶结构的例外情况可能会影响建筑设计,并鼓励采用将涂料与透气基材结合的混合系统。德克萨斯州和亚利桑那州等州也在修订其标准,加速了全国的推广应用。

由于欧盟加强了除生物剂的监管,罐头内防腐剂的使用受到限制。

2023年生效的法规限制了二异氰酸酯的含量并限制了全氟烷基和多氟烷基物质(PFAS)的使用,迫使欧洲製造商重新设计其硬化剂和防污剂的化学配方。虽然具有类似货架稳定性的替代品正在研发中,但配方调整的成本却在上升。农业领域禁用杂酚油进一步限制了木材防腐剂的选择,并提高了泛欧产品线的技术门槛。跨国公司推动规范统一的措施正在产生全球连锁反应,导致合规投资增加和产品开发週期延长。

细分市场分析

到2025年,水性涂料将占据建筑涂料市场52.02%的份额,年复合成长率(CAGR)为4.70%,这主要得益于从上海到深圳等地政府对挥发性有机化合物(VOC)排放的限制以及对含溶剂产品的禁令。这些措施表明,与溶剂型产品相比,水性涂料的VOC含量降低了50%以上,巩固了其市场主导地位。儘管溶剂型涂料在一些需要渗透性和极强防潮性能的特定应用领域仍然占据一席之地,但粉末涂料和辐射固化涂料技术正在工厂预涂饰面领域取得稳步进展。水性涂料的快速普及使其成为建筑涂料市场的技术基础,供应商正在扩大产能并完善本地化配方基础设施,以满足监管主导的需求激增。

欧盟和北美地区监管的持续收紧将加速水性涂料技术在中端和入门级价格市场的渗透,缩小其与溶剂型涂料之间长期存在的成本差距。为了满足环境、社会和治理(ESG)报告要求并降低未来的合规风险,原始设备製造商(OEM)和承包商越来越多地指定使用水性涂料生产线。因此,大型製造商正在投资水性树脂反应器,而中型企业则在探索授权协议和合资企业,以获取专有的聚合物平台。随着规模经济效应导致每公升成本下降,水性涂料的普及形成良性循环,巩固了其在建筑涂料市场整体成长的核心地位。

建筑涂料报告按技术(水性、溶剂型及其他)、树脂类型(丙烯酸、醇酸、环氧树脂、聚酯、聚氨酯及其他树脂类型)、应用领域(住宅、商业)和地区(亚太、北美、欧洲、南美、中东和非洲)进行细分。市场预测以美元以金额为准。

区域分析

到2025年,亚太地区将占全球建筑涂料收入的46.10%,年复合成长率达5.52%,这主要得益于都市化的快速发展、智慧城市投资的增加以及住宅的蓬勃发展。中国水性涂料强制令的实施正在推动大规模的技术变革,而DIFM(自行施工、安装和维护)服务模式以及可支配收入的增长则推动了东南亚国协对高品质涂料的采用。

北美市场在维修週期和法规主导的对冷屋顶的需求推动下保持稳定成长。加州第24号法规和IECC法规为高反射涂料创造了稳定的需求,即使整体住宅开工量依然低迷。然而,熟练油漆工短缺和人事费用上涨限制了近期成长,促使企业采用省力喷涂设备和快干涂料来维持施工能力。

在欧洲成熟市场,企业面临日益复杂的营运环境,挥发性有机化合物 (VOC)、杀菌剂和全氟烷基物质 (PFAS) 的监管标准不断收紧。儘管配方调整成本给盈利带来挑战,但该地区对永续性和循环经济原则的承诺正在推动高端低 VOC 水基解决方案的发展。东欧在基础设施计划和维修补贴的推动下实现了高于平均水平的成长,而西欧则专注于高性能外墙维修,以实现碳减排目标。拉丁美洲和中东及非洲市场规模仍然小规模,但经济多元化和大型住宅项目带来的成长潜力吸引了策略性收购,例如圣戈班收购墨西哥 Ovnivel 集团。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国老旧住宅存量维修需求激增

- 美国炎热气候州强制执行「冷屋顶」标准

- 中国二、三线城市迅速转向水基技术

- 东协地区「DIFM(直接检验和正式涂装服务)」网路的快速发展

- 智慧着色自清洁外墙涂料

- 市场限制

- 环氧树脂原料价格上涨/2024年起供应中断

- 由于欧盟加强了对除生物剂的监管,罐头内防腐剂的使用受到限制。

- 北美熟练油漆工短缺

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 透过技术

- 水系统

- 溶剂型

- 其他的

- 依树脂类型

- 丙烯酸纤维

- 醇酸树脂

- 环氧树脂

- 聚酯纤维

- 聚氨酯

- 其他树脂类型

- 按最终用途

- 住宅

- 商业的

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 印尼

- 越南

- 泰国

- 菲律宾

- 新加坡

- 澳洲和纽西兰

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 波兰

- 北欧国家

- 俄罗斯

- 其他欧洲

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- 3 TREES Group

- AkzoNobel NV

- Asian Paints

- BASF

- Beckers Group

- Benjamin Moore and Company

- Berger Paints India Ltd.

- Brillux GmbH and Co. KG

- CIN SA

- DAW SE

- Flugger group AS

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Masco Corporation

- Nippon Paint Holdings Co., Ltd

- PPG Industries Inc.

- RPM International Inc.

- Sniezka SA

- The Sherwin-Williams Company

第七章 市场机会与未来展望

Architectural Coatings market size in 2026 is estimated at USD 95.57 billion, growing from 2025 value of USD 91.62 billion with 2031 projections showing USD 117.98 billion, growing at 4.3% CAGR over 2026-2031.

Regulatory mandates for low-VOC formulations, rapid water-borne technology adoption, and renovation-led demand in mature housing stocks underpin this steady trajectory. Mandatory cool-roof codes in U.S. hot-climate states are accelerating reflective-coating uptake, while China's Tier-2 and Tier-3 cities are fast-tracking water-borne conversions that shift global product mix toward sustainable chemistries. At the same time, labor shortages and epoxy-raw-material volatility are tightening margins, fostering investment in labor-saving application tools and smart-coating technologies.

Global Architectural Coatings Market Trends and Insights

Surging Renovation Demand in Aging U.S. Housing Stock

Homeowners are choosing upgrades over relocation as high mortgage rates persist, lifting volumes of premium exterior paints with cool-roof properties mandated by California Title 24. Compliance drives predictable demand because coatings are embedded in building-permit workflows rather than discretionary cycles. Los Angeles' Green Building Code stipulates Solar Reflectance Index thresholds, while local utilities pay USD 0.20 per ft2 rebates that widen project budgets for higher-value formulations. Aging-in-place preferences extend repaint cycles, increasing willingness to invest in long-life systems that curb long-term maintenance. Manufacturers benefit as renovation spending is less volatile than new-build activity, allowing steadier production planning. Specialty suppliers leverage the shift by bundling color-visualization apps and contractor-matching services that streamline consumer decisions.

Mandatory Cool-Roof Codes in Hot-Climate U.S. States

California and the International Energy Conservation Code now require aged solar-reflectance levels more than or equal to 0.55 and thermal-emittance more than or equal to 0.75 for low-slope roofs in zones 1-3, compelling builders to select CRRC-listed products. Certification narrows the competitive field and pushes formulation research and development toward high-reflectance pigments and durable elastomeric binders. Compliance linkage to permitting enables suppliers to forecast volume more accurately and negotiate longer-term raw-material contracts. Exception pathways for air-gap roof assemblies influence architectural design and may spur hybrid systems combining coatings with vented substrates. States such as Texas and Arizona are amending codes, escalating nationwide adoption momentum.

Stricter EU Biocide Rules Limiting In-Can Preservatives

Regulations enacted in 2023 cap diisocyanate content and restrict PFAS, forcing European producers to redesign hardeners and stain-repellent chemistries. Reformulation costs rise as suppliers search for drop-in alternatives with equivalent shelf stability. Creosote bans in agriculture further squeeze wood-preservative ranges, raising technical hurdles for pan-European lines. The ripple extends globally as multinationals harmonize specifications, increasing compliance investments and elongating product-development cycles.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Water-Borne Technologies in China's Tier-2 and Tier-3 Cities

- Smart-Pigmented Self-Cleaning Facade Coatings

- Skilled-Painter Shortages in North America

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems generated 52.02% of the architectural coatings market share in 2025 and are growing at a 4.70% CAGR as regulators curb VOC emissions and municipalities from Shanghai to Shenzhen outlaw solvent-rich products. These advances, combined with demonstrated VOC reductions of more than 50% versus solvent lines, cement water-borne leadership. Solvent-borne coatings persist in niche uses requiring penetration or extreme moisture tolerance, whereas powder and radiation-curable technologies make incremental gains in factory-applied finishes. Adoption momentum positions water-borne as the technology backbone of the architectural coatings market, with suppliers scaling capacity and localized tinting infrastructure to meet code-driven demand surges.

Continued legislative tightening in the EU and North America will accelerate the technology's penetration into mid-tier and entry-level price points, narrowing historical cost gaps with solvent alternatives. OEM and contract applicators increasingly specify water-borne lines to align with ESG reporting and to mitigate future compliance liabilities. Consequently, tier-one producers channel capital toward water-borne resin reactors, while second-tier firms explore licensing or joint ventures to access proprietary polymer platforms. As economies of scale lower per-liter costs, water-borne adoption becomes self-reinforcing, underpinning its central role in overall architectural coatings market growth.

The Architectural Coatings Report is Segmented by Technology (Water-Borne, Solvent-Borne, Others), Resin Type (Acrylic, Alkyd, Epoxy, Polyester, Polyurethane, and Other Resin Types), End-Use (Residential and Commercial), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 46.10% of worldwide architectural coatings revenue in 2025 and is climbing at a 5.52% CAGR, powered by urbanization, smart-city investments, and rapid residential construction. China's enforcement of water-borne mandates is propelling large-scale technology switching, while ASEAN nations leverage DIFM service models and rising disposable incomes to adopt higher-quality finishes.

North America delivers steady growth through renovation cycles and regulatory-driven cool-roof demand. California Title 24 and IECC provisions convert code compliance into steady volumes of high-reflectance coatings, even as overall housing starts moderate. However, skilled-painter shortages and escalating labor rates temper near-term expansion, prompting uptake of labor-saving spray rigs and quick-set formulations to sustain application capacity

Europe's mature market navigates a complex regulatory environment that tightens VOC, biocide, and PFAS thresholds. Reformulation costs challenge profitability, yet the region's commitment to sustainability and circular-economy principles favors premium, low-VOC water-borne solutions. Eastern European infrastructure projects and renovation subsidies offer pockets of above-average growth, while Western Europe focuses on high-performance envelope upgrades to meet carbon-reduction targets. Latin America, the Middle East, and Africa remain smaller segments but present upside tied to economic diversification and large-scale housing initiatives, attracting strategic acquisitions such as Saint-Gobain's purchase of Mexico's Ovniver Group .

- 3 TREES Group

- AkzoNobel N.V.

- Asian Paints

- BASF

- Beckers Group

- Benjamin Moore and Company

- Berger Paints India Ltd.

- Brillux GmbH and Co. KG

- CIN S.A.

- DAW SE

- Flugger group AS

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Masco Corporation

- Nippon Paint Holdings Co., Ltd

- PPG Industries Inc.

- RPM International Inc.

- Sniezka SA

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Renovation Demand in Aging U.S. Housing Stock

- 4.2.2 Mandatory "Cool-Roof" Codes in Hot-Climate U.S. States

- 4.2.3 Rapid Shift to Water-Borne Technologies in China's Tier-2 And Tier-3 Cities

- 4.2.4 Booming Do-It-For-Me (DIFM) Trade Painter Networks in ASEAN

- 4.2.5 Smart-Pigmented Self-Cleaning Facade Coatings

- 4.3 Market Restraints

- 4.3.1 Epoxy Raw-Material Price Spikes Post-2024 Supply Disruptions

- 4.3.2 Stricter EU Biocide Rules Limiting In-Can Preservatives

- 4.3.3 Skilled-Painter Shortages in North America

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-borne

- 5.1.2 Solvent-borne

- 5.1.3 Others

- 5.2 By Resin Type

- 5.2.1 Acrylic

- 5.2.2 Alkyd

- 5.2.3 Epoxy

- 5.2.4 Polyester

- 5.2.5 Polyurethane

- 5.2.6 Other Resin Types

- 5.3 By End-Use

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Indonesia

- 5.4.1.6 Vietnam

- 5.4.1.7 Thailand

- 5.4.1.8 Philippines

- 5.4.1.9 Singapore

- 5.4.1.10 Vietnam

- 5.4.1.11 Australia and Newzealand

- 5.4.1.12 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Poland

- 5.4.3.7 Nordic Countries

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3 TREES Group

- 6.4.2 AkzoNobel N.V.

- 6.4.3 Asian Paints

- 6.4.4 BASF

- 6.4.5 Beckers Group

- 6.4.6 Benjamin Moore and Company

- 6.4.7 Berger Paints India Ltd.

- 6.4.8 Brillux GmbH and Co. KG

- 6.4.9 CIN S.A.

- 6.4.10 DAW SE

- 6.4.11 Flugger group AS

- 6.4.12 Hempel A/S

- 6.4.13 Jotun

- 6.4.14 Kansai Paint Co., Ltd.

- 6.4.15 Masco Corporation

- 6.4.16 Nippon Paint Holdings Co., Ltd

- 6.4.17 PPG Industries Inc.

- 6.4.18 RPM International Inc.

- 6.4.19 Sniezka SA

- 6.4.20 The Sherwin-Williams Company

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

住宅建筑涂料市场:2026-2032年全球市场预测(按产品类型、配方、饰面类型、应用、最终用户和分销管道划分)水性建筑涂料市场:依功能、产品类型、应用、通路和最终用途划分-2026-2032年全球市场预测

住宅建筑涂料市场:2026-2032年全球市场预测(按产品类型、配方、饰面类型、应用、最终用户和分销管道划分)水性建筑涂料市场:依功能、产品类型、应用、通路和最终用途划分-2026-2032年全球市场预测 2026年全球压克力墙面标牌支架市场报告建筑涂料市场:2026-2032年全球市场预测(依产品类型、技术、树脂类型、应用方法、用途及通路划分)建筑翻新涂装市场:依产品类型、应用方法、涂装技术及最终用户划分-2026-2032年全球预测

2026年全球压克力墙面标牌支架市场报告建筑涂料市场:2026-2032年全球市场预测(依产品类型、技术、树脂类型、应用方法、用途及通路划分)建筑翻新涂装市场:依产品类型、应用方法、涂装技术及最终用户划分-2026-2032年全球预测 建筑涂料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材质、製程、最终用户、功能、应用方法及解决方案划分

建筑涂料市场分析及预测(至2035年):依类型、产品类型、技术、应用、材质、製程、最终用户、功能、应用方法及解决方案划分 全球建筑涂料市场:市场规模、份额和趋势分析(按树脂类型、技术、应用和地区划分),细分市场预测(2026-2033 年)2026年全球含锌底漆市场报告2026年全球外墙涂料市场报告2026年全球富锌涂料市场报告

全球建筑涂料市场:市场规模、份额和趋势分析(按树脂类型、技术、应用和地区划分),细分市场预测(2026-2033 年)2026年全球含锌底漆市场报告2026年全球外墙涂料市场报告2026年全球富锌涂料市场报告