|

市场调查报告书

商品编码

1937281

印度汽车产业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)India Automobile Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

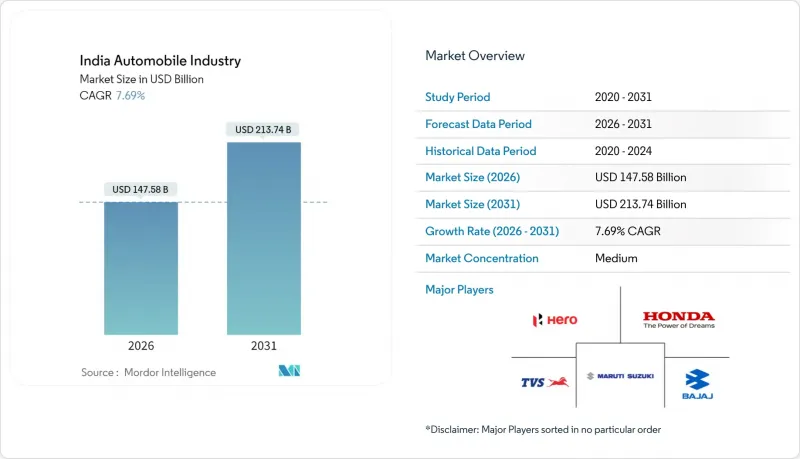

印度汽车市场预计将从 2025 年的 1,370.6 亿美元成长到 2026 年的 1,475.8 亿美元,预计到 2031 年将达到 2,137.4 亿美元,2026 年至 2031 年的复合年增长率为 7.69%。

人口成长、家庭收入提高、推动电气化的政策支持以及製造业基础(2024财年产量达2843万辆)共同支撑了不断增长的消费需求。两轮车、乘用车、商用车和三轮车的持续生产保持了行业的韧性,而诸如“总理乡村道路计划”(Pradhan Mantri Gram Sadak Yojana)等基础设施项目则扩大了其地理覆盖范围。儘管竞争依然激烈,但电动车、订阅式所有权和企业车队脱碳等领域仍蕴藏着许多机会。预计未来十年,半导体自给率的提高、更密集的农村道路网络以及数位化零售的发展,将成为印度汽车市场的新驱动力。

印度汽车产业趋势与洞察

可支配所得增加和快速都市化

收入的成长使汽车拥有更具吸引力,尤其是在土地资源丰富、交通拥堵较少的区域性城市(二、三线城市),这扩大了印度汽车市场的消费群。 65%的人口年龄在35岁以下,首次购车者正值收入高峰期。农村人口迁移刺激了双重需求:一方面,都市区购车者追求出行便利;另一方面,汇款也用于转换返乡生活。就业向郊区转移减少了人们对公共交通的依赖,从而支撑了对两轮车和小型汽车的需求。订阅模式透过避免高额首付扩大了购车管道,进一步推动了汽车的普及。

政府电动车与FAME-II奖励

印度于2019年启动的FAME(混合动力汽车和电动汽车燃料采用与製造)第二阶段计划,五年预算高达1150亿卢比(约13.1亿美元)。该计划旨在促销电动车,包括电动两轮车(e-2W)、电动三轮车(e-3W)和电动四轮车(e-4W)。泰米尔纳德邦和古吉拉突邦的额外补贴加剧了区域差距,而计划中的FAME-III修订版旨在扩大对更大型车辆的支援。这些激励措施缩短了投资回收期,并鼓励私人买家和车队营运商转向零排放车型。

监管变化、安全标准和商品及服务税过渡

随着印度实施BS-VII排放标准并强制要求安全配置,中小型组装组装商正面临高成本的动力传动系统升级和认证成本,这给车型利润率带来了压力。这些升级需要大量的研发投入和严格的测试才能符合法规标准。同时,零件商品及服务税(GST)的调整造成了价格的不确定性,并影响了製造商的整体成本结构。雪上加霜的是,各邦道路税制度的差异也使合规变得更加复杂,製造商需要应对不同地区的税收制度。这些因素可能大幅推高消费者的购车成本,导致消费者延后购车,并降低印度汽车市场的即时需求。此外,成本上涨可能会促使製造商探索其他策略,例如在地采购,以减轻财务负担。

细分市场分析

两轮车在印度汽车市场占据主导地位,市占率高达73.64%。这一主导地位凸显了印度消费者对两轮车的偏好,因为它们价格实惠、燃油效率高,且在拥挤的都市区易于操控。乘用车虽然规模较小,但其复合年增长率(CAGR)最高,达到8.84%,这主要得益于SUV和跨界车的推出,满足了中产阶级的需求。Scooter销量成长了21%,而摩托车销量仅成长了10%,凸显了消费者对自动变速箱和在都市区便利操控的偏好。

随着电动两轮车进入主流价格区间,以及金融机构向首次购车者提供长期贷款,成长动能持续强劲。同时,商用车受制于基础设施预算和工业生产週期,但正受益于正在进行的高速公路建设。三轮车在农村地区的「最后一公里」货运和客运中仍然发挥着重要作用。日益严格的排放气体标准正推动模组化平台的投资,预计将提升印度汽车市场现有企业的规模经济效益。

截至2025年,汽油引擎在印度汽车市场仍占59.27%的份额,这主要得益于炼油产能和相对于柴油的采购价格优势。纯电动车(BEV)虽然销量较低,但由于税收优惠、FAME-II补贴以及锂离子电池成本下降,其复合年增长率(CAGR)仍达到10.02%。混合动力汽车汽车消除了里程焦虑,并在不依赖新能源基础设施的情况下提高了效率。

在政府对国内发电的政策承诺和严格的燃油效率标准的推动下,汽车製造商正逐步将其产品系列组合转向电动驱动系统。为降低营运成本,液化石油气/压缩天然气的使用在寻求降低营运成本的商用车队中日益普及。同时,由于氢气供应短缺,燃料电池技术仍处于试点阶段。儘管充电网路和电池更换试点计画的推进将决定其普及速度,但印度汽车市场已显现出各细分市场消费者接受度加速提升的征兆。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 可支配所得增加和快速都市化

- 政府电动车与FAME-II奖励

- 国家和地方公路网的扩建

- 订阅所有权和租赁模式

- 区域半导体製造投资

- 企业车队脱碳需求

- 市场限制

- 监管变化、安全标准和商品及服务税过渡

- 全球半导体供应链的波动性

- 由于都市区拥挤而导致的使用限制

- 与车载资讯系统相关的保险费上涨

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额)

- 按车辆类型

- 摩托车

- 三轮车

- 搭乘用车

- 商用车辆

- 按燃料类型

- 汽油

- 柴油引擎

- LPG/CNG

- 电池电动车

- 油电混合车

- 插电式混合动力电动车

- 燃料电池电动车

- 按销售管道

- 原厂授权经销商

- 在线的

- 依所有权类型

- 个人使用

- 商业用途

- 按地区

- 印度北部

- 南印度

- 东印度

- 西印度群岛

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- TVS Motor Company

- Hero MotoCorp

- Honda Motorcycle

- Royal Enfield

- Bajaj Auto

- Suzuki Motorcycle India

- Maruti Suzuki India

- Tata Motors

- Hyundai Motor India

- Mahindra & Mahindra

- MG Motor India

- Volkswagen India

- Renault-Nissan Alliance

- Honda Cars India

- BYD India

- BMW Group India

- Mercedes-Benz India

- Kia India

- Ashok Leyland

- Eicher Motors(VE Commercial)

- Atul Auto

- Piaggio Vehicles

- Kinetic Green

第七章 市场机会与未来展望

The India automobile market is expected to grow from USD 137.06 billion in 2025 to USD 147.58 billion in 2026 and is forecast to reach USD 213.74 billion by 2031 at 7.69% CAGR over 2026-2031.

Demand is buoyed by population-led consumption, rising household incomes, policy-backed electrification, and a manufacturing base that produced 28.43 million vehicles in FY 2024. Sustained output across two-wheelers, passenger cars, commercial vehicles, and three-wheelers keeps the sector resilient, while infrastructure programs such as Pradhan Mantri Gram Sadak Yojana widen geographic reach. Competitive dynamics remain intense, yet opportunities persist in electric models, subscription ownership, and corporate fleet decarbonization. Semiconductor self-reliance, rural road density, and digital retail are additional levers set to lift the India automobile market through the decade.

India Automobile Industry Trends and Insights

Rising Disposable Incomes and Rapid Urbanization

Income growth is enlarging the consumer base for the Indian automobile market, especially in Tier-2 and Tier-3 cities, where land availability and lower congestion make vehicle ownership attractive. Sixty-five percent of the population is under 35, aligning prime earning years with first-time purchases. Migration from rural districts stimulates dual demand, urban buyers seek mobility, while remittances finance upgrades back home. The spread of suburban employment hubs reduces dependence on mass transit and supports two-wheelers and compact cars. Subscription programs extend access by sidestepping hefty down payments, further deepening penetration.

Government EV and FAME-II Incentives

India's FAME (Faster Adoption and Manufacturing of Hybrid & Electric Vehicles) Scheme Phase-II, launched in 2019, comes with a hefty budget of INR 11,500 crore (USD 1.31 billion), set to span five years. This initiative aims to boost the sales of electric vehicles, covering e-2Ws, e-3Ws, and e-4Ws. . State add-ons in Tamil Nadu and Gujarat enhance regional differentials, while the planned FAME-III revision aims to broaden support into heavier segments. These incentives shorten payback periods, encouraging personal buyers and fleet operators to pivot toward zero-emission models.

Regulatory Changes, Safety Standards and GST Shifts

As India implements BS-VII norms and mandates safety gear, small assemblers grapple with costly powertrain upgrades and validations, squeezing their model margins. These upgrades require significant research and development investments and rigorous testing to meet compliance standards. Meanwhile, GST realignments on components introduce pricing uncertainties, impacting the overall cost structure for manufacturers. Adding to the challenge, varying state road-tax regimes complicate compliance, as manufacturers must navigate differing tax policies across regions. These factors lead to noticeable price hikes for consumers, potentially delaying their purchases and dampening immediate demand in the Indian automobile market. Additionally, the increased costs may push manufacturers to explore alternative strategies, such as the localization of components, to mitigate the financial burden.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of National Highway and Rural Road Network

- Subscription-Based Ownership and Leasing Models

- Global Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In the Indian auto market, two-wheelers reign supreme, commanding a significant 73.64% share. This dominance highlights the preference for two-wheelers among Indian consumers, driven by factors such as affordability, fuel efficiency, and ease of navigation in congested urban areas. Although smaller, passenger cars are posting the swiftest 8.84% CAGR on the back of SUV and crossover launches tuned to aspirational middle-class tastes. Scooter sales climbed 21% versus the motorcycle segment's 10% gain, highlighting urban preference for automatic transmissions and ease of use.

Growth momentum continues as electric two-wheelers enter mainstream price points and as financiers extend longer tenures to first-time buyers. Conversely, commercial vehicles hinge on infrastructure budgets and industrial output cycles but benefit from ongoing highway upgrades. Three-wheelers retain relevance for last-mile goods and passenger movement in Tier-2 centers. Regulatory emission upgrades funnel investments toward modular platforms, potentially elevating scale efficiencies for incumbents in the Indian automobile market.

Petrol engines retained 59.27% of the India automobile market share in 2025, buoyed by refinery capacity and lower purchase prices relative to diesel. Battery electric vehicles, though smaller in volume, are advancing at a 10.02% CAGR thanks to tax rebates, FAME-II subsidies and falling lithium-ion cell costs. Hybrids bridge range-anxiety gaps, offering efficiency gains without new-energy infrastructure dependence.

Policy commitments to domestic power generation and stricter fuel-economy norms will gradually shift OEM portfolios toward electrified drivetrains. LPG/CNG use expands in commercial fleets seeking operating-cost relief. Meanwhile, fuel-cell technology remains exploratory due to hydrogen supply gaps. Charging-network rollouts and battery-swapping pilots dictate adoption pace but indicators already point to accelerating consumer acceptance across segments in the India automobile market.

The India Automobile Market Report is Segmented by Vehicle Type (Two-Wheelers, Three-Wheelers and More), Fuel Type (Petrol/Gasoline, Diesel, LPG/CNG, and More), Sales Channel (OEM-Authorized Dealers and Online), Ownership Type (Personal Use and Commercial Use), and by Region (North India, South India, East India, West India). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- TVS Motor Company

- Hero MotoCorp

- Honda Motorcycle

- Royal Enfield

- Bajaj Auto

- Suzuki Motorcycle India

- Maruti Suzuki India

- Tata Motors

- Hyundai Motor India

- Mahindra & Mahindra

- MG Motor India

- Volkswagen India

- Renault-Nissan Alliance

- Honda Cars India

- BYD India

- BMW Group India

- Mercedes-Benz India

- Kia India

- Ashok Leyland

- Eicher Motors (VE Commercial)

- Atul Auto

- Piaggio Vehicles

- Kinetic Green

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disposable Incomes and Rapid Urbanization

- 4.2.2 Government EV and FAME-II Incentives

- 4.2.3 Expansion of National Highway and Rural Road Network

- 4.2.4 Subscription-Based Ownership and Leasing Models

- 4.2.5 Local Semiconductor Fabrication Investments

- 4.2.6 Corporate Fleet-Decarbonization Mandates

- 4.3 Market Restraints

- 4.3.1 Regulatory Changes, Safety Standards and GST Shifts

- 4.3.2 Global Semiconductor Supply-Chain Volatility

- 4.3.3 Urban Congestion-Driven Usage Restrictions

- 4.3.4 Rising Telematics-Linked Insurance Premiums

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD billion)

- 5.1 By Vehicle Type

- 5.1.1 Two-wheelers

- 5.1.2 Three-wheelers

- 5.1.3 Passenger Cars

- 5.1.4 Commercial Vehicles

- 5.2 By Fuel Type

- 5.2.1 Petrol / Gasoline

- 5.2.2 Diesel

- 5.2.3 LPG / CNG

- 5.2.4 Battery Electric Vehicles

- 5.2.5 Hybrid Electric Vehicles

- 5.2.6 Plug-in Hybrid Electric Vehicles

- 5.2.7 Fuel-Cell Electric Vehicles

- 5.3 By Sales Channel

- 5.3.1 OEM-Authorised Dealers

- 5.3.2 Online

- 5.4 By Ownership Type

- 5.4.1 Personal Use

- 5.4.2 Commercial Use

- 5.5 By Region

- 5.5.1 North India

- 5.5.2 South India

- 5.5.3 East India

- 5.5.4 West India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 TVS Motor Company

- 6.4.2 Hero MotoCorp

- 6.4.3 Honda Motorcycle

- 6.4.4 Royal Enfield

- 6.4.5 Bajaj Auto

- 6.4.6 Suzuki Motorcycle India

- 6.4.7 Maruti Suzuki India

- 6.4.8 Tata Motors

- 6.4.9 Hyundai Motor India

- 6.4.10 Mahindra & Mahindra

- 6.4.11 MG Motor India

- 6.4.12 Volkswagen India

- 6.4.13 Renault-Nissan Alliance

- 6.4.14 Honda Cars India

- 6.4.15 BYD India

- 6.4.16 BMW Group India

- 6.4.17 Mercedes-Benz India

- 6.4.18 Kia India

- 6.4.19 Ashok Leyland

- 6.4.20 Eicher Motors (VE Commercial)

- 6.4.21 Atul Auto

- 6.4.22 Piaggio Vehicles

- 6.4.23 Kinetic Green