|

市场调查报告书

商品编码

1937308

种子加工机械:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Seed Processing Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

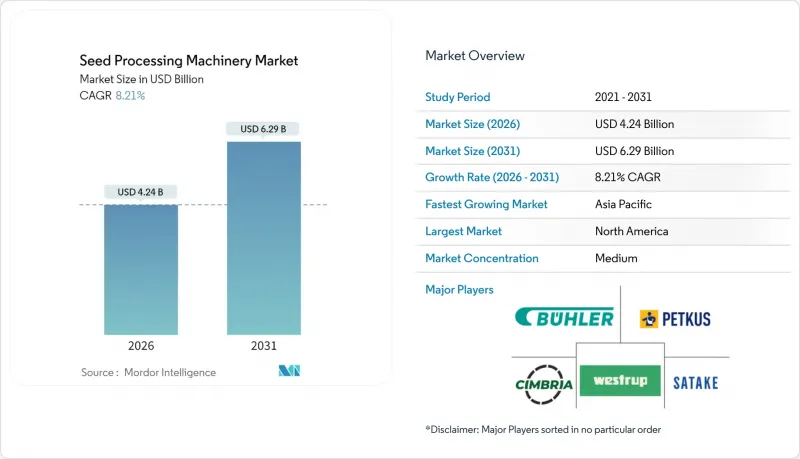

预计种子加工机械市场将从 2025 年的 39.2 亿美元成长到 2026 年的 42.4 亿美元,到 2031 年将达到 62.9 亿美元,2026 年至 2031 年的复合年增长率为 8.21%。

这一成长主要受农业机械化程度提高、人工智慧光学分类机的应用以及对加工增值种子需求不断增长的推动。预计到2050年,全球人口将达到97亿,提高农业生产力对粮食安全至关重要。高品质种子在提高作物产量方面的重要性日益凸显,推动了对先进种子加工机械的需求。印度、印尼和波兰等国的政府补贴促进了设备的采购,而中型商业工厂和研究机构也正在扩大其精准育种计画的产能。市场参与企业正透过维护服务合约、具备网路安全安全功能的物联网连接以及适用于商业设施和小规模行动单元的模组化设计展开竞争。

全球种子加工机械市场趋势与洞察

自动化光学分类机的应用迅速成长

配备人工智慧的光学分类机缺陷去除率高达99.5%以上,与机械设备相比,返工率降低,产能提升高达40%。机器学习演算法持续优化颜色、密度和X射线参数,无需在产品类型变更时进行人工重新校准。这些系统的早期采用者提供加值服务合同,保证运作和远端最佳化。半导体供应的稳定性以及相关组件成本的下降预计将推动中型加工厂更多地采用此类系统。在种子加工机械市场,视觉系统和边缘运算正逐渐成为标准配置而非可选功能,这加大了工厂升级的压力。儘管初始成本较高,但光学分选具有很高的投资报酬率,使其成为资本投资的重点领域。

对经过处理和增值处理的种子需求不断增长

商业种子处理技术正从基础的杀菌剂处理发展到包含微量元素和有益微生物的先进包衣技术。经处理的种子批次可使利润率提高15-25%,促使加工商投资于能够以克为单位精确计量聚合物用量的精密包衣设备。欧洲法规将于2028年禁止在包衣中使用微塑料,这加速了对兼容可生物降解组合药物的新型设备的升级。使用含有滑石粉和氧化钙混合物的颗粒状材料可使种子发芽率提高23%,证明了包衣品质的农艺价值。优质种子生产的扩大使包衣设备具有重要的战略意义,并有助于提高整个种子加工机械市场的收入。

智慧机器的初始成本很高

将人工智慧和自动化控制系统整合到先进的种子加工设备中,导致价格高昂,这给小规模营运商和新兴市场参与企业带来了采用障碍。人工智慧光学分类机的价格比机械式分选机高出40%至60%,中型工厂的投资回收期延长至3至5年。市场挑战,例如软商品价格波动和利率上升,加剧了价格敏感度。虽然有租赁和计量收费等替代资金筹措方案,但供应商被迫开发新的信用风险评估工具。由于资金筹措管道有限,中小型业者的市场渗透率仍然有限,尤其是在南亚和撒哈拉以南非洲地区。

细分市场分析

到2025年,清选机将占种子加工机械市场31.85%的份额,成为加工生产线的重要组成部分。清选机用途广泛,可加工多种谷物、油籽和蔬菜,这推动了工厂扩建和设备升级带来的稳定需求。出口法规对杂草种子有着严格的控制和发芽标准,促使人们对多级筛分机和重力分离器的需求不断增长。光学辨识系统的整合使得在单一工序中即可高效去除异物,从而提高生产效率并减少人工劳动。大规模商业加工设施的发展趋势也增加了对高容量自动化清选系统的需求,进一步巩固了其显着的市场份额。

预计到2031年,包衣设备市场将以7.98%的复合年增长率成长,这主要得益于无微塑胶包衣材料和生物活性添加剂的日益普及。先进的计量系统可确保包衣均匀,从而促进种子发芽并符合相关法规。水溶性粘合剂的进步使得低温固化製程成为可能,并有助于与节能干燥系统整合。研发特种杂交种子的研究机构正在创造对小批量包衣设备的需求,并扩大基本客群。随着加工商更加重视生产高品质种子,预计包衣设备市场的成长速度将进一步加快。

区域分析

到2025年,北美将占据全球种子加工机械市场34.02%的份额,这主要得益于玉米带和太平洋西北地区的大规模工厂。先正达斥资1500万美元对其位于帕斯科的工厂维修,以及贝克公司在密苏里州新建的大豆加工厂等大规模投资,都支撑了持续的更新换代需求。儘管关税的不确定性影响了整体销售,但加工商仍在不断升级改造其设施,以满足出口市场的植物检疫要求。该地区的种子加工机械市场受益于完善的资金筹措管道和广泛的服务承包商网络,这些都确保了高效的运作。

亚太地区预计将以6.86%的复合年增长率实现最高增长,这主要得益于印度50%的补贴计划、印尼的设备扩建计划以及KPAGRO和AdvantaSeed的资本投资。本地製造商提供经济实惠的清洗机和半自动分类机,而国际公司则供应先进的光学分类机。水稻和杂交蔬菜商业种子的日益普及推动了市场成长。中国对美国製造的设备征收10%的关税,正在推动供应链本地化,并增强区域製造能力。

在欧洲,环境法规和现代化措施支撑着市场的稳定运作。向Incotec公司无微塑胶涂层技术的过渡需要对加工设施进行升级和更换。波兰的「农业4.0」计画(资金达25亿欧元,约27亿美元)正在支持先进生产线的投资。德国和法国的节能奖励鼓励采用低温烘干机和太阳能辅助洗衣机。儘管面临经济挑战,但环境法规的要求确保了欧洲各地企业设备升级的一致性。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 自动化光学分选系统的快速普及

- 对经过处理和增值处理的种子需求不断增长

- 政府对农业机械化的补贴

- 扩大商业种子繁殖中心

- 整合基于人工智慧的预测性维护

- 增加对减少收穫后损失的投资

- 市场限制

- 智慧机器的初始成本很高

- 特殊零件供应链波动

- 资料所有权和网路安全问题

- 小规模农户模式投资报酬的不确定性

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按机器类型

- 预清洁器

- 洗衣机

- 烘干机

- 平土机

- 涂布机

- 分离装置

- 磨床

- 光学分类机

- 种子包装商

- 其他类型的机器(例如种子处理设备)

- 按操作模式

- 自动的

- 半自动

- 最终用户

- 商业种子加工厂

- 种子生产商

- 研究所

- 农场设施

- 粮食处理设施

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 法国

- 义大利

- 西班牙

- 英国

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 印度

- 日本

- 澳洲

- 韩国

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Cimbria A/S(American Industrial Partners)

- PETKUS Technologie GmbH

- Westrup A/S(John Fowler(India)Private Ltd.)

- Buhler AG(ASKO Holdings)

- Satake Corporation

- Alvan Blanch Development Company Limited

- Lewis M. Carter Manufacturing, Inc.

- Ag Growth International Inc.

- Spectrum Industries

- Shijiazhuang Synmec International Trading Limited(Hebei Ruixue Grain Selecting Machinery CO.,Ltd)

- Agrosaw Private Limited

- Bratney Companies

- Zhengzhou Weiwei Machinery Co., Ltd.

- SKIOLD A/S

- Sukup Manufacturing Co.

第七章 市场机会与未来展望

The seed processing machinery market is expected to grow from USD 3.92 billion in 2025 to USD 4.24 billion in 2026 and is forecast to reach USD 6.29 billion by 2031 at 8.21% CAGR over 2026-2031.

This growth is driven by increased agricultural mechanization, adoption of AI-enabled optical sorters, and higher demand for treated, value-added seeds. The projected increase in world population to 9.7 billion by 2050 necessitates enhanced agricultural productivity for food security. The importance of high-quality seeds in improving crop yields has increased the demand for advanced seed processing machinery. Government subsidies in India, Indonesia, and Poland are encouraging equipment purchases, while mid-scale commercial plants and research institutes are expanding their capacity for precision breeding programs. Companies in the market compete through maintenance service contracts, IoT connectivity with cybersecurity features, and modular designs suitable for both commercial facilities and small-scale mobile units.

Global Seed Processing Machinery Market Trends and Insights

Surge in Automated Optical Sorting Adoption

Optical sorters equipped with artificial intelligence achieve defect-removal accuracy exceeding 99.5%, reducing rework and increasing throughput by up to 40% compared to mechanical units. Machine learning algorithms continuously optimize color, density, and X-ray parameters, eliminating the need for manual recalibration during variety changes. Companies that implemented these systems early now offer premium service contracts featuring guaranteed uptime and remote optimization. The projected stabilization of semiconductor supply and subsequent reduction in component costs are likely to increase adoption among mid-sized processing plants. The seed processing machinery market now includes vision systems and edge computing as standard features rather than optional additions, creating pressure for facilities to upgrade their equipment. The strong return on investment, despite higher initial costs, makes optical sorting a primary focus for capital expenditure.

Rising Demand for Treated, Value-added Seeds

Commercial seed treatment has progressed from basic fungicide applications to advanced coatings containing micronutrients and beneficial microorganisms. Treated seed batches yield 15-25% higher margins, driving processors to invest in precision coating equipment that measures polymer application with gram-level accuracy. European regulations prohibiting microplastics in coatings by 2028 are accelerating equipment upgrades, as new machinery must be compatible with biodegradable formulations. The use of pelleting materials, including talcum-calcium-oxide mixtures, has improved seed emergence rates by 23%, demonstrating the agronomic value of coating quality. The expansion of premium seed production has increased the strategic importance of coating equipment, contributing to higher overall revenue in the seed processing machinery market.

High Upfront Cost of Smart Machinery

The integration of AI and automated controls in advanced seed processing equipment results in premium pricing, creating adoption barriers for smaller operations and emerging market participants. AI-enabled optical sorters are 40-60% more expensive than mechanical models, extending payback periods to three to five years for mid-volume plants. Market challenges, including soft commodity price fluctuations and rising interest rates, increase price sensitivity. While leasing and pay-per-use contracts provide alternative financing options, they require vendors to develop new credit risk assessment tools. Market penetration among smaller players remains limited, particularly in South Asia and sub-Saharan Africa, due to insufficient financing ecosystems.

Other drivers and restraints analyzed in the detailed report include:

- Government Subsidies for Agro-Mechanization

- Growing Investment in Post-Harvest Loss Reduction

- Data Ownership and Cybersecurity Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cleaners held a 31.85% of the seed processing machinery market share in 2025, serving as essential components in processing lines. Their versatility in handling cereals, oilseeds, and vegetables generates consistent demand from both facility expansions and equipment replacement initiatives. Export regulations requiring strict weed-seed control and germination standards drive the need for multi-deck screeners and gravity separators. The integration of optical recognition systems enables efficient removal of foreign materials in a single pass, increasing productivity and reducing manual labor requirements. The trend toward larger commercial processing facilities has increased demand for high-capacity, automated cleaning systems, reinforcing their significant market share.

The coaters segment is projected to grow at an 7.98% CAGR through 2031, driven by increased adoption of microplastic-free coating materials and bioactive inoculants. Advanced dosing systems ensure consistent coating application that supports seed germination and complies with regulations. The development of water-soluble binding agents enables lower temperature curing processes, facilitating integration with energy-efficient drying systems. Research institutions developing specialized hybrid seeds create demand for small-batch coating equipment, expanding the customer base. The coating equipment segment's growth is anticipated to accelerate as processors focus on premium seed production.

Seed Processing Machinery Market Report is Segmented by Machinery Type (Pre-Cleaners, Cleaners, Dryers, Graders, Coaters, Separators, Polishers, and More), by Operation Mode (Automatic and Semi-Automatic), by End-User (Commercial Seed Processing Plants, Seed Producers, Research Institutions, and More), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a 34.02% of the seed processing machinery market share in 2025, supported by extensive facilities in the Corn Belt and Pacific Northwest. Significant investments, including Syngenta's USD 15 million Pasco facility upgrade and Beck's new soybean plant in Missouri, demonstrate sustained replacement demand. While tariff uncertainties affect combined sales, processors continue facility modernization to meet export market phytosanitary requirements. The region's seed processing machinery market benefits from established financing options and an extensive network of service contractors maintaining high operational efficiency.

Asia-Pacific shows the highest growth at 6.86% CAGR, driven by India's 50% subsidy program, Indonesia's equipment distribution initiatives, and facility investments from KPAGRO and Advanta Seeds. Local manufacturers provide cost-effective cleaners and semi-automatic graders, while international companies supply advanced optical sorters. The market gains momentum from increased commercial seed adoption in rice and hybrid vegetables. The 10% Chinese tariffs on U.S. equipment have encouraged supply-chain localization, strengthening regional manufacturing capabilities.

Europe maintains a stable market performance through environmental regulations and modernization initiatives. Incotec's transition to microplastic-free coating technologies necessitates processor upgrades and equipment replacement. Poland's Agriculture 4.0 program, with EUR 2.5 billion (USD 2.7 billion) in funding, supports investment in advanced processing lines. Energy efficiency incentives in Germany and France encourage the adoption of low-heat dryers and solar-assisted cleaners. Despite economic challenges, environmental compliance requirements ensure consistent equipment upgrades across European operations.

- Cimbria A/S (American Industrial Partners)

- PETKUS Technologie GmbH

- Westrup A/S (John Fowler (India) Private Ltd.)

- Buhler AG (ASKO Holdings)

- Satake Corporation

- Alvan Blanch Development Company Limited

- Lewis M. Carter Manufacturing, Inc.

- Ag Growth International Inc.

- Spectrum Industries

- Shijiazhuang Synmec International Trading Limited (Hebei Ruixue Grain Selecting Machinery CO.,Ltd)

- Agrosaw Private Limited

- Bratney Companies

- Zhengzhou Weiwei Machinery Co., Ltd.

- SKIOLD A/S

- Sukup Manufacturing Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Automated Optical Sorting Adoption

- 4.2.2 Rising Demand for Treated, Value-added Seeds

- 4.2.3 Government Subsidies for Agro-Mechanization

- 4.2.4 Expansion of Commercial Seed Multiplication Hubs

- 4.2.5 Integration of AI-Based Predictive Maintenance

- 4.2.6 Growing Investment in Post-Harvest Loss Reduction

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost of Smart Machinery

- 4.3.2 Supply-Chain Volatility for Specialty Components

- 4.3.3 Data-Ownership and Cybersecurity Concerns

- 4.3.4 Uncertain Return on Investment for Smallholder-Focused Models

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Machinery Type

- 5.1.1 Pre-cleaners

- 5.1.2 Cleaners

- 5.1.3 Dryers

- 5.1.4 Graders

- 5.1.5 Coaters

- 5.1.6 Separators

- 5.1.7 Polishers

- 5.1.8 Optical Sorters

- 5.1.9 Seed Packagers

- 5.1.10 Other Machinery Type (Seed Teating Equipment, etc.)

- 5.2 By Operation Mode

- 5.2.1 Automatic

- 5.2.2 Semi-automatic

- 5.3 By End-User

- 5.3.1 Commercial Seed Processing Plants

- 5.3.2 Seed Producers

- 5.3.3 Research Institutions

- 5.3.4 On-Farm Facilities

- 5.3.5 Grain Handling Facilities

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 France

- 5.4.2.3 Italy

- 5.4.2.4 Spain

- 5.4.2.5 United Kingdom

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Rest of Middle East

- 5.4.6 Africa

- 5.4.6.1 South Africa

- 5.4.6.2 Egypt

- 5.4.6.3 Rest of Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Cimbria A/S (American Industrial Partners)

- 6.4.2 PETKUS Technologie GmbH

- 6.4.3 Westrup A/S (John Fowler (India) Private Ltd.)

- 6.4.4 Buhler AG (ASKO Holdings)

- 6.4.5 Satake Corporation

- 6.4.6 Alvan Blanch Development Company Limited

- 6.4.7 Lewis M. Carter Manufacturing, Inc.

- 6.4.8 Ag Growth International Inc.

- 6.4.9 Spectrum Industries

- 6.4.10 Shijiazhuang Synmec International Trading Limited (Hebei Ruixue Grain Selecting Machinery CO.,Ltd)

- 6.4.11 Agrosaw Private Limited

- 6.4.12 Bratney Companies

- 6.4.13 Zhengzhou Weiwei Machinery Co., Ltd.

- 6.4.14 SKIOLD A/S

- 6.4.15 Sukup Manufacturing Co.

7 Market Opportunities and Future Outlook

钻石单晶加工设备市场:依製程、设备类型、自动化程度和终端用户产业划分-2026-2032年全球预测

钻石单晶加工设备市场:依製程、设备类型、自动化程度和终端用户产业划分-2026-2032年全球预测 全球石材加工机械市场规模、份额、趋势和成长分析报告:2026-2034年全球老虎机市场规模、份额、趋势和成长分析报告(2026-2034)

全球石材加工机械市场规模、份额、趋势和成长分析报告:2026-2034年全球老虎机市场规模、份额、趋势和成长分析报告(2026-2034) 精密加工市场规模、份额和趋势分析报告:按营运方式、类型、最终用途、地区和细分市场预测,2026-2033年种子加工机械市场-2026-2031年预测

精密加工市场规模、份额和趋势分析报告:按营运方式、类型、最终用途、地区和细分市场预测,2026-2033年种子加工机械市场-2026-2031年预测 石材加工机械市场规模、份额及成长分析(按机器类型、加工材料、应用、最终用户、机器自动化程度及地区划分)-2026-2033年产业预测

石材加工机械市场规模、份额及成长分析(按机器类型、加工材料、应用、最终用户、机器自动化程度及地区划分)-2026-2033年产业预测 全球精密加工市场全球精冲工具市场全球粉末加工设备市场

全球精密加工市场全球精冲工具市场全球粉末加工设备市场 粉体加工设备市场-全球产业规模、份额、趋势、机会及预测(按技术、最终用户、地区及竞争细分,2020-2030 年)

粉体加工设备市场-全球产业规模、份额、趋势、机会及预测(按技术、最终用户、地区及竞争细分,2020-2030 年)