|

市场调查报告书

商品编码

1937311

生物基聚合物:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Bio-based Polymers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

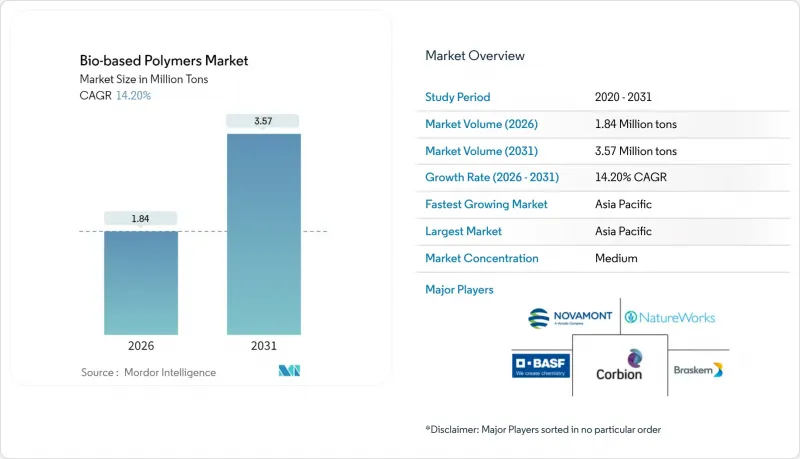

预计生物基聚合物市场将从 2025 年的 161 万吨成长到 2026 年的 184 万吨,到 2031 年达到 357 万吨,2026 年至 2031 年的复合年增长率为 14.2%。

这项快速成长得益于一次性塑胶的强制性禁令、生物精炼技术的快速成熟以及物料平衡认证,后者使得现有设施能够直接使用新树脂进行分销。生产商正与追求净零排放目标的全球品牌签署长期承购协议,这为相关人员提供了支持新资本投资的信心。从区域来看,亚太地区将占据新增产量的大部分,这主要得益于农业残余物提供的低成本原料以及鼓励可再生材料的区域政策。耐热性和生物相容性的提高正使生物基聚合物的应用范围从通用包装扩展到医疗、汽车和电子等高端领域。

全球生物基聚合物市场趋势与洞察

监管主导的一次性塑胶禁令

澳洲于2024年扩大了塑胶禁令范围,禁止使用厚购物袋和聚苯乙烯食品容器,并要求零售商改用经认证的可堆肥材料。欧盟目前正在实施生产者延伸责任制,将废弃物成本转嫁到每个包装的价格中,从而缩小与生物基聚合物市场的成本差距。加拿大于2024年底实施了联邦塑胶禁令,为可再生包装在北美创造了一个完整的市场。中国在禁止进口废弃塑胶后,加强了国内监管,强制国内加工商采购符合规定的材料。领先实施案例表明,一旦禁令生效,由于合规风险超过了价格溢价,需求会迅速转变。

消费者对永续材料的需求日益增长

一项全球调查发现,73%的消费者在购买决策中会考虑永续性声明,并且愿意为经过认证的可再生材料支付15-20%的溢价。品牌所有者正在透过实施优先采购品质平衡认证材料的采购规则来应对这一趋势,从而保护生物基聚合物市场的利润率。连锁餐厅正在透过从传统涂层转向可堆肥薄膜来满足顾客减少废弃物的期望。 B2B买家正在将碳强度评分纳入供应商评分卡,提高了化石基塑胶的进入门槛。这种不断增长的需求也蔓延到电子和服装产业,在这些产业中,生活风格品牌正日益将可再生材料作为品质的象征。

与石油基塑胶的成本比较

由于小规模工厂缺乏规模经济,生物基化学品的售价比化石基化学品高出20%至50%。虽然工厂与现有化工基地共用公用设施可以降低生产成本,但高资本密集度会延缓价格趋于一致。原油价格上涨会暂时缩小价格差距,但无法消除结构性差异。医疗设备等特殊应用领域能够接受溢价,因为生物降解性可以减轻监管负担。要实现更广泛的价格趋于一致,需要将现有产能翻番,并将固定成本分摊到更大的产量上。

细分市场分析

到2025年,其他产品类型(主要是聚丁二酸丁二醇酯和Polybutylene Adipate Terephthalate)将占生物基聚合物市场份额的44.12%。由于该树脂具有可堆肥性和良好的热封强度,生产商正越来越多地将其应用于地膜和软包装袋领域。这一大规模的市场基础正在推动特种级生物基聚合物市场的整体规模成长,并支持逐步消除瓶颈的计划。亚洲企业正在将丁二酸和己二酸整合到本地原料中,降低运输成本和外汇风险,并提高供应稳定性。

到2031年,聚乳酸(PLA)将以18.22%的复合年增长率持续成长。该行业受益于耐热等级PLA的推出,这些等级拓展了PLA在电子产品机壳和汽车内装等领域的应用。医疗创新者正利用PLA的生物可吸收特性,设计出癒合后可溶解的螺丝和钢板,以避免二次手术。阿联酋和泰国产能的扩张将扩大PLA的生产规模,降低成本,并扩大PLA应用领域的生物基聚合物市场。先前仅限于一两家公司的技术许可预计将随着新进入者的出现而加剧市场竞争。

生物基聚合物报告按产品类型(可生物降解淀粉混合物、生物聚乙烯 (bio-PE)、生物聚对苯二甲酸乙二醇酯 (bio-PET) 等)、终端用户行业(农业、医疗保健、包装、汽车及运输、纺织等)和地区(亚太地区、北美地区、欧洲地区、世界其他地区)进行细分。市场预测以吨为单位。

区域分析

到2025年,亚太地区将占全球生物基聚合物市场规模的44.02%,并在2031年之前以16.63%的复合年增长率持续成长。中国正透过税收优惠、绿色贷款以及中粮等公司营运的玉米製聚合物一体化项目,巩固其在该地区主导地位。泰国为生物化学投资提供长达八年的免税期,吸引合资企业将糖厂与聚合物生产设施结合。印度正利用剩余的甘蔗渣满足国内聚合物需求,同时也向跨国公司提供出口信贷。

欧洲拥有成熟的政策组合来支持需求,将一次性塑胶指令与生产者延伸责任制结合。德国和法国已将回收成本内部化,提高了化石基塑胶的相对成本,并鼓励加工商转向使用经认证的可生物降解材料。欧洲拥有超过3500家工业堆肥厂,使真正的循环经济成为可能。区域回收协议允许供应商锁定多年价格,从而稳定生物基聚合物市场,使其免受原材料价格波动的影响。

在北美,各州层级的法规,例如加州的SB54法案(该法案要求在2032年将一次性塑胶包装减少65%),正在加速这一进程。加拿大的联邦禁令正在协调各省的产品规格,并建立一个涵盖整个北美大陆的投资基础。企业买家正在将可再生碳配额纳入供应合同,以确保供应的稳定性。在其他地区,新兴的拉丁美洲糖业经济体和一些非洲国家正在复製相关政策模式,以加速在农业废弃物丰富的地区推广应用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 监管主导的一次性塑胶禁令

- 消费者对永续材料的需求日益增长

- 企业净零排放与可再生碳采购承诺

- 推出物料平衡认证的即用型树脂

- 扩大二氧化碳和农业废弃物生物精炼

- 市场限制

- 与石油基塑胶相比,成本较高

- 缺乏堆肥和回收基础设施

- 生质燃料强制令导致原料价格波动

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 可生物降解淀粉混合物

- 生物聚乙烯(Bio-PE)

- 生物基聚对苯二甲酸乙二酯(Bio-PET)

- 聚乳酸(PLA)

- 聚羟基烷酯(PHAs)

- 其他产品类型(例如,聚丁二酸丁二醇酯(PBS)、Polybutylene Adipate Terephthalate(PBAT))

- 按最终用户行业划分

- 农业

- 医疗保健

- 包装

- 汽车和运输设备

- 纺织业

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲

- 世界其他地区

- 南美洲

- 中东和非洲

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- Cardia Bioplastics

- CJ CHEIL JEDANG CORP.

- Corbion

- Covestro AG

- Danimer Scientific

- Eastman Chemical Company

- Emirates Biotech

- FKuR

- Futerro

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Novamont SpA

- Rodenburg Biopolymers

- Sulzer Ltd.

- Ukhi India Pvt. Ltd.

- Yield10 Bioscience, Inc.

第七章 市场机会与未来展望

The Bio-based Polymers Market is expected to grow from 1.61 million tons in 2025 to 1.84 million tons in 2026 and is forecast to reach 3.57 million tons by 2031 at 14.2% CAGR over 2026-2031.

The sharp expansion comes from mandatory single-use plastic bans, fast-maturing bio-refinery technologies, and mass-balance certification that allows drop-in resins to flow through existing assets. Producers lock in long-term offtake agreements with global brands pursuing net-zero timelines, giving financiers visibility to support new capacity. Regionally, Asia-Pacific captures much of the incremental tonnage because agricultural residues supply low-cost feedstock and local policies encourage renewable materials. Premium segments open in medical, automotive, and electronics as improved heat resistance and biocompatibility formulations move bio-based polymers beyond commodity packaging.

Global Bio-based Polymers Market Trends and Insights

Regulation-led Bans on Single-use Plastics

Australia widened its plastics prohibition in 2024 to ban heavyweight shopping bags and polystyrene food containers, pushing retailers toward certified compostable options. The European Union now enforces extended producer responsibility that prices end-of-life costs into each package, narrowing the cost gap with the bio-based polymers market. Canada implemented a federal plastics prohibition in late 2024, creating a contiguous North American market for renewable packaging. China tightened domestic restrictions after banning waste plastic imports, forcing local converters to source compliant materials. Early adopters show that once bans enter force, demand shifts quickly because compliance risk outweighs price premiums.

Rising Consumer Demand for Sustainable Materials

Global surveys show that 73% of shoppers weigh sustainability claims in purchase decisions and will pay 15-20% more for verified renewable content. Brand owners translate this signal into procurement rules that favor mass-balance certified feedstocks, protecting margins in the bio-based polymers market. Food service chains swap conventional coatings for compostable films to meet customer expectations on waste reduction. B2B buyers embed carbon intensity scores in supplier scorecards, raising entry barriers for fossil plastics. The demand pull spreads to electronics and apparel as lifestyle brands position renewable materials as a marker of quality.

Higher Cost vs. Petro-plastics

Bio-based grades sell at 20-50% premiums compared with fossil alternatives because smaller plants lack scale efficiencies. Production costs ease when plants share utilities with existing chemical hubs, yet capital intensity delays parity. Price spikes in crude oil narrow the gap temporarily but do not erase structural differences. Specialty uses such as medical devices absorb premiums because biodegradability trims regulatory burdens. Broader parity depends on doubling current capacity so fixed costs spread across more tons.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-zero and Renewable-carbon Sourcing Pledges

- Scale-up of CO2- and Agri-waste-based Biorefineries

- Limited Composting and Recycling Infrastructure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Other product types, dominated by polybutylene succinate and polybutylene adipate terephthalate, accounted for 44.12% of bio-based polymers market share in 2025. Producers win adoption in mulch films and flexible pouches because these resins combine compostability with heat-seal strength. Their large base lifts the overall bio-based polymers market size for specialty grades and supports incremental debottlenecking projects. Supply security improves as Asian firms integrate succinic acid and adipic acid back to local feedstock, trimming freight and currency risk.

Polylactic acid leads growth at an 18.22% CAGR to 2031. The segment benefits from recent heat-stable grades that unlock electronics housings and automotive trim. Medical innovators exploit PLA's bioresorption to design screws and plates that dissolve after healing, avoiding secondary surgeries. Capacity expansions in the UAE and Thailand add scale and lower cost floors, which enlarges the bio-based polymers market size for PLA applications. Competitive intensity rises as new entrants license technology that had been confined to one or two players.

The Bio-Based Polymers Report is Segmented by Product Type (Biodegradable Starch Blends, Bio Polyethylene (Bio-PE), Bio-Polyethylene Terephthalate (Bio-PET), and More), End-User Industry (Agriculture, Medical and Healthcare, Packaging, Automotive and Transportation, Textiles, and Others), and Geography (Asia-Pacific, North America, Europe, and Rest of World). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific captured 44.02% of the bio-based polymers market size in 2025 and is expanding at a 16.63% CAGR to 2031. China anchors regional leadership through tax rebates, green loans, and integrated corn-to-polymer complexes run by COFCO and peers. Thailand grants eight-year tax holidays on bio-chemical investments, luring joint ventures that colocate sugar mills with polymer units. India leverages surplus bagasse to backfill domestic polymer demand while exporting credits to multinationals.

Europe supports demand with a mature policy mix that combines the Single-Use Plastics Directive and mandatory extended producer responsibility. Germany and France internalize collection fees that make fossil plastics relatively more expensive, steering converters toward certified compostables. Industrial composting coverage surpasses 3,500 sites, enabling true circularity claims. Regional offtake agreements let suppliers lock multi-year prices, stabilizing the bio-based polymers market against feedstock swings.

North America accelerates through state-level laws such as California's SB 54 that requires a 65% cut in single-use plastic packaging by 2032. Canada's federal ban synchronizes product specifications across provinces, creating a continental platform for investment. Corporate buyers formalize renewable-carbon quotas in supplier contracts, delivering predictable tonnage. Elsewhere, emerging Latin American sugar economies and selected African nations replicate policy templates that fast-track adoption where agricultural residues are plentiful.

- BASF

- Biome Bioplastics

- BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- Braskem

- Cardia Bioplastics

- CJ CHEIL JEDANG CORP.

- Corbion

- Covestro AG

- Danimer Scientific

- Eastman Chemical Company

- Emirates Biotech

- FKuR

- Futerro

- Mitsubishi Chemical Group Corporation

- NatureWorks LLC

- Novamont S.p.A.

- Rodenburg Biopolymers

- Sulzer Ltd.

- Ukhi India Pvt. Ltd.

- Yield10 Bioscience, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulation-led bans on single-use plastics

- 4.2.2 Rising consumer demand for sustainable materials

- 4.2.3 Corporate net-zero and renewable-carbon sourcing pledges

- 4.2.4 Mass-balance certified drop-in resins adoption

- 4.2.5 Scale-up of CO2- and agri-waste-based biorefineries

- 4.3 Market Restraints

- 4.3.1 Higher cost vs. petro-plastics

- 4.3.2 Limited composting and recycling infrastructure

- 4.3.3 Feedstock price volatility from biofuel mandates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Biodegradable Starch Blends

- 5.1.2 Bio Polyethylene (Bio-PE)

- 5.1.3 Bio-Polyethylene Terephthalate (Bio-PET)

- 5.1.4 Polylactic Acid (PLA)

- 5.1.5 Polyhydroxyalkanoate (PHA)

- 5.1.6 Other Product Types (Polybutylene Succinate (PBS), Polybutylene Adipate Terephthalate (PBAT), etc.)

- 5.2 By End-user Industry

- 5.2.1 Agriculture

- 5.2.2 Medical and Healthcare

- 5.2.3 Packaging

- 5.2.4 Automotive and Transportation

- 5.2.5 Textiles

- 5.2.6 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 Rest of the World

- 5.3.4.1 South America

- 5.3.4.2 Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 BASF

- 6.4.2 Biome Bioplastics

- 6.4.3 BIOTEC Biologische Naturverpackungen GmbH & Co. KG.

- 6.4.4 Braskem

- 6.4.5 Cardia Bioplastics

- 6.4.6 CJ CHEIL JEDANG CORP.

- 6.4.7 Corbion

- 6.4.8 Covestro AG

- 6.4.9 Danimer Scientific

- 6.4.10 Eastman Chemical Company

- 6.4.11 Emirates Biotech

- 6.4.12 FKuR

- 6.4.13 Futerro

- 6.4.14 Mitsubishi Chemical Group Corporation

- 6.4.15 NatureWorks LLC

- 6.4.16 Novamont S.p.A.

- 6.4.17 Rodenburg Biopolymers

- 6.4.18 Sulzer Ltd.

- 6.4.19 Ukhi India Pvt. Ltd.

- 6.4.20 Yield10 Bioscience, Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

生物聚合物创新市场预测至2034年:按聚合物类型、原料、应用和地区分類的全球分析

生物聚合物创新市场预测至2034年:按聚合物类型、原料、应用和地区分類的全球分析 蓖麻油衍生生物聚合物市场:2026-2032年全球市场预测(按聚合物类型、製造流程、形态和应用划分)生物聚合物薄膜市场:按材料、薄膜类型、应用和最终用途产业划分-2026-2032年全球市场预测

蓖麻油衍生生物聚合物市场:2026-2032年全球市场预测(按聚合物类型、製造流程、形态和应用划分)生物聚合物薄膜市场:按材料、薄膜类型、应用和最终用途产业划分-2026-2032年全球市场预测 永续晶圆回收市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、材料类型、製程、最终用户及功能划分自消毒表面市场分析及预测(至2035年):依类型、产品类型、技术、应用、材质、最终用户、製程、部署类型、设备及解决方案划分

永续晶圆回收市场分析及预测(至2035年):依类型、产品、服务、技术、组件、应用、材料类型、製程、最终用户及功能划分自消毒表面市场分析及预测(至2035年):依类型、产品类型、技术、应用、材质、最终用户、製程、部署类型、设备及解决方案划分 永续生物聚合物:全球市场

永续生物聚合物:全球市场 2026年全球生物聚合物市场报告

2026年全球生物聚合物市场报告 生物聚合物市场-2026-2031年预测

生物聚合物市场-2026-2031年预测 电气和电子生物聚合物市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年D,L-聚乳酸市场按形态、类型、生产製程、分子量和最终用途产业划分-2026-2032年全球预测

电气和电子生物聚合物市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年D,L-聚乳酸市场按形态、类型、生产製程、分子量和最终用途产业划分-2026-2032年全球预测