|

市场调查报告书

商品编码

1937315

非洲废弃物管理:市场份额分析、行业趋势和统计数据、成长预测(2026-2031 年)Africa Waste Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

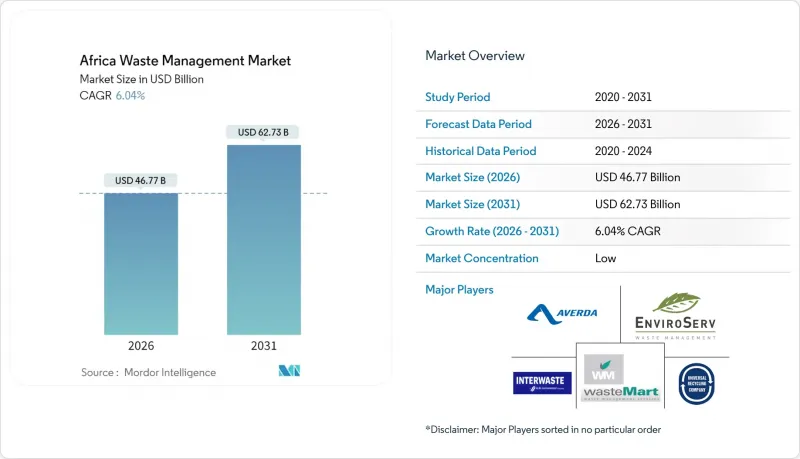

预计到 2026 年,非洲废弃物管理市场价值将达到 467.7 亿美元,高于 2025 年的 441.1 亿美元,预计到 2031 年将达到 627.3 亿美元。

预计从 2026 年到 2031 年,其复合年增长率将达到 6.04%。

快速的都市化正以前所未有的速度向本已不堪重负的市政系统注入垃圾,从而推动了对私营部门垃圾收集、处理和回收解决方案的需求。随着各国政府逐步推行生产者延伸责任制(EPR),投资人对垃圾处理的兴趣日益浓厚,而科技公司则引进人工智慧驱动的路线优化技术以提高收集效率。儘管垃圾焚化发电(WtE)营运商已获得气候融资支持,但其他大型处理设施仍面临资金缺口。市场竞争仍然分散,但不断上涨的合规成本有利于那些能够将非正规垃圾收集者纳入正规价值链的企业。

非洲废弃物管理市场趋势与洞察

城市人口成长是城市垃圾产生的主要驱动因素。

非洲都市区每年新增约2,200万居民,导致家庭消费和每日垃圾产量增加。光是拉各斯市每天就产生13,000至14,000吨废弃物,但只有0.37%的垃圾被分流到正规回收部门,凸显了基础设施的严重不足。垃圾收集车队的扩充速度跟不上需求,迫使市政当局将业务外包,并鼓励私人投资建造垃圾转运站和资源回收设施。集中式市政废弃物降低了每吨垃圾的处理成本,提高了垃圾焚化发电和垃圾分类厂的计划经济效益。因此,人口趋势将确保城市废弃物在2030年后仍将是非洲废弃物管理市场的支柱。

政府提高回收目标并推广生产者责任延伸制度

肯亚2024年的生产者责任延伸制度(EPR)要求生产者承担废弃物收集和回收的费用,这与南非《国家环境管理废弃物法》下的强制性方案类似。埃及正在製定一项永续回收倡议,将非正规废弃物收集者与持证加工商联繫起来,在提高材料品质的同时保障生计。合规成本正促使回收从自愿项目转变为法律义务,迫使品牌所有者与认证运营商签订长期服务合约。这些强制性规定正在稳步扩大塑胶、金属和电子废弃物回收设施的原料供应,从而提振整个非洲废弃物管理市场的收入。

掩埋监管和执法力度不足

东非超过90%的废弃物仍被倾倒在露天垃圾场,排放的甲烷气体和渗滤液威胁地下水。光是亚的斯亚贝巴的莱皮垃圾场就接收未经检验的废弃物,而该市的正规废弃物收集率仅65%。监管不力使得未经授权的运输者得以规避垃圾场收费,导致合规经营者无力承担高昂的营运成本,并损害了设计完善的掩埋的经济效益。缺乏统一的检查机制使得市政当局无法收回营运成本,也无法落实「污染者付费」原则,阻碍了整个非洲废弃物管理市场废弃物基础设施的现代化进程。

细分市场分析

2025年,受人口向都市区迁移导致家庭消费成长的推动,住宅废弃物将占非洲废弃物管理市场的60.45%。同时,受购物中心和办公大楼扩张的推动,商业垃圾量预计将以8.52%的复合年增长率增长,从而带动了对定期收集和安全文件销毁的需求。零售连锁店签订多年合同,以履行其在生产者延伸责任制(EPR)下的收集义务,这为综合服务提供者提供了可预测的垃圾量。工业废弃物产生者,尤其是在南非,面临日益严格的危险废弃物法规,这使得他们更加依赖获得许可的处置合作伙伴。由于医疗保健投资的增加,医疗废弃物也在增加,这为获得认证的焚烧炉创造了利润丰厚的市场。

非洲废弃物管理市场受惠于多样化的原料来源。不断增长的基础设施预算推动了建筑和拆除废弃物的增加,而农业残余物则为城郊地区的沼气化提供了机会。威立雅在多个非洲国家采用的多源服务模式,透过结合住宅和商业合同,实现了高回报特种废弃物处理量与处理量之间的平衡,展现了其价值。非正式网络在塑胶收集方面仍然发挥着重要作用,但正规的集散商正开始透过特许经营模式吸收这些网络,从而提供标准化的安全培训,并透过行动支付提高透明度。

非洲废弃物管理报告按产生来源(住宅、商业、工业、医疗保健等)、服务类型(收集、运输、分类/分类等)、废弃物类型(生活废弃物、工业危险废弃物、电子废弃物、塑胶等)和地区(奈及利亚、南非、埃及、肯亚、非洲其他地区)进行细分。市场预测以美元以金额为准为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 城市人口成长是城市垃圾产生量增加的主要原因。

- 各国政府正在提高回收目标并推广生产者延伸责任制(EPR)框架。

- 投资者对废弃物发电(WtE)计划的兴趣日益浓厚

- 数位化采集和路线优化平台

- 偏远矿区塑胶燃料生产的离网微型热解技术

- 市场限制

- 掩埋监管和执法力度薄弱。

- 缺乏用于大规模加工资产的资金

- 非正规部门的根深蒂固阻碍了正规私人投资。

- 废弃物发电厂的气候变迁保险缺口

- 价值/供应链分析

- 监管环境

- 技术展望

- 产业吸引力-波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 物流基础设施洞察

- Start-Ups创新特辑

第五章 市场规模及成长预测(价值,单位:十亿美元)

- 按来源

- 住宅

- 商业设施(零售商店、办公室等)

- 产业

- 医疗(健康和医药)

- 建筑和废弃物废弃物

- 其他(引擎废弃物、农业废弃物等)

- 按服务类型

- 收集、运输、分类和分离

- 处理/处置

- 掩埋处置

- 回收和资源回收

- 焚烧和废弃物发电

- 其他(化学处理、堆肥等)

- 其他(咨询、审核、训练等)

- 依废物类型

- 都市固态废弃物

- 工业用危险废弃物

- 电子废弃物

- 塑胶废弃物

- 医疗废弃物

- 建筑和拆除废弃物

- 农业废弃物

- 其他特殊废弃物(放射性废弃物等)

- 按地区

- 奈及利亚

- 南非

- 埃及

- 肯亚

- 其他非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Averda

- EnviroServ

- Interwaste

- WasteMart

- Universal Recycling Company

- Desco

- PETCO

- The Glass Recycling Company

- Oricol Environmental Services

- WeCyclers

- The Waste Group

- SA Waste

- Veolia Africa

- SUEZ Recycling & Recovery Africa

- Biffa South Africa

- Mr Green Africa

- TakaTaka Solutions

- EcoPost

- Stericycle(MedWaste Africa)

- Dangote Recycling

第七章 市场机会与未来展望

The Africa Waste Management Market size in 2026 is estimated at USD 46.77 billion, growing from 2025 value of USD 44.11 billion with 2031 projections showing USD 62.73 billion, growing at 6.04% CAGR over 2026-2031.

Rapid urbanization funnels unprecedented waste volumes into already-strained municipal systems, creating space for private-sector collection, treatment, and recycling solutions. Investor appetite grows as governments adopt extended producer responsibility (EPR) rules, while technology firms deploy AI-enabled route optimization to raise collection efficiencies. Waste-to-energy (WtE) developers are securing climate-finance backing, yet capital gaps persist for other large-scale treatment assets. Competition remains fragmented, but rising compliance costs favor operators able to integrate informal collectors into formal value chains.

Africa Waste Management Market Trends and Insights

Rising Urban Population Driving Municipal Solid Waste Volumes

Africa's cities gain roughly 22 million new residents every year, elevating household consumption and daily waste flows. Lagos alone generates 13,000-14,000 tons of refuse each day, yet formal recycling diverts just 0.37%, underscoring severe infrastructure gaps. Collection fleets struggle to keep pace, prompting municipalities to outsource operations and invite private investment in transfer stations and material-recovery facilities. Concentrated urban waste streams lower per-ton processing costs, improving project economics for WtE and sorting plants. Demographic trends will therefore keep municipal solid waste (MSW) the anchor of the Africa waste management market well beyond 2030.

Government Push for Higher Recycling Targets & EPR Frameworks

Kenya's 2024 EPR regulations oblige producers to finance end-of-life collection and recycling, mirroring South Africa's mandatory schemes under the National Environmental Management Waste Act. Egypt has rolled out a sustainable recycling initiative that links informal pickers to licensed processors, raising material quality while preserving livelihoods. Compliance costs are shifting recycling from voluntary programs to legally enforced obligations, pushing brand owners to sign long-term service contracts with certified operators. These mandates steadily enlarge feedstock volumes for plastic, metal, and e-waste recycling facilities, bolstering revenues across the Africa waste management market.

Weak Landfill Regulation & Enforcement

More than 90% of East Africa's waste still winds up in open dumps, releasing methane and leachate that threaten groundwater. Addis Ababa's Repi site alone receives wastes unchecked, yet only 65% of the city's refuse is formally collected. Non-enforcement allows unlicensed haulers to undercut compliant operators by dodging gate fees, eroding the economics of engineered landfills. Without uniform inspection regimes, municipalities cannot recover operating costs or enforce polluter-pays principles, delaying modernization of disposal infrastructure across the Africa waste management market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investor Interest in Waste-to-Energy Projects

- Digitized Collection & Route-Optimization Platforms

- Capital Scarcity for Large-Scale Treatment Assets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Residential streams secured 60.45% of the Africa waste management market share in 2025 as household consumption grew alongside urban migration. Commercial volumes, however, are projected to post an 8.52% CAGR, fueled by mall and office expansion that heightens demand for scheduled pickups and secure document destruction. Retail chains sign multi-year contracts to meet EPR take-back obligations, adding predictable tonnage for integrated service providers. Industrial generators confront tighter hazardous-waste regulations, particularly in South Africa, pushing them toward licensed disposal partners. Medical waste also rises with increased healthcare investment, creating a high-margin niche for certified incineration firms.

The Africa waste management market benefits from diverse feedstocks: construction and demolition debris escalates as infrastructure budgets climb, while agricultural residues present biogas opportunities in peri-urban zones. Veolia's multi-source service model across several African countries showcases the value of bundling residential and commercial contracts to balance volume with higher-yield specialty waste. Informal networks remain pivotal for plastics retrieval, yet formalized aggregators are beginning to absorb them via franchise schemes that deliver standardized safety training and mobile-payment transparency.

The Africa Waste Management Report is Segmented by Source (Residential, Commercial, Industrial, Medical, and More), by Service Type (Collection, Transportation, Sorting & Segregation, and More), by Waste Type (Municipal Solid, Industrial Hazardous, E-Waste, Plastic, and More), and by Geography (Nigeria, South Africa, Egypt, Kenya, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Averda

- EnviroServ

- Interwaste

- WasteMart

- Universal Recycling Company

- Desco

- PETCO

- The Glass Recycling Company

- Oricol Environmental Services

- WeCyclers

- The Waste Group

- SA Waste

- Veolia Africa

- SUEZ Recycling & Recovery Africa

- Biffa South Africa

- Mr Green Africa

- TakaTaka Solutions

- EcoPost

- Stericycle (MedWaste Africa)

- Dangote Recycling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising urban population driving municipal solid waste volumes

- 4.2.2 Government push for higher recycling targets & EPR frameworks

- 4.2.3 Growing investor interest in waste-to-energy (WtE) projects

- 4.2.4 Digitised collection & route-optimisation platforms

- 4.2.5 Off-grid micro-pyrolysis for plastics-to-fuel in remote mines

- 4.3 Market Restraints

- 4.3.1 Weak landfill regulation & enforcement

- 4.3.2 Capital scarcity for large-scale treatment assets

- 4.3.3 Informal sector lock-in that deters formal private investment

- 4.3.4 Climate-linked insurance gaps for WtE plants

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Force Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Logistics Infrastructure Insights

- 4.9 Startup & Innovation Spotlight

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Source

- 5.1.1 Residential

- 5.1.2 Commercial (retail, office, etc.)

- 5.1.3 Industrial

- 5.1.4 Medical (Health and Pharmaceutical)

- 5.1.5 Construction & Demolition

- 5.1.6 Others (institutional, agricultural, etc)

- 5.2 By Service Type

- 5.2.1 Collection, Transportation, Sorting & Segregation

- 5.2.2 Disposal / Treatment

- 5.2.2.1 Landfill

- 5.2.2.2 Recycling & Resource Recovery

- 5.2.2.3 Incineration & Waste-to-Energy

- 5.2.2.4 Others (Chemical Treatment, Composting, etc.)

- 5.2.3 Others (Consulting, Audit & Training, etc.)

- 5.3 By Waste Type

- 5.3.1 Municipal Solid Waste

- 5.3.2 Industrial Hazardous Waste

- 5.3.3 E-waste

- 5.3.4 Plastic Waste

- 5.3.5 Biomedical Waste

- 5.3.6 Construction & Demolition Waste

- 5.3.7 Agricultural Waste

- 5.3.8 Other Specialized Waste (radio active, etc)

- 5.4 By Geography

- 5.4.1 Nigeria

- 5.4.2 South Africa

- 5.4.3 Egypt

- 5.4.4 Kenya

- 5.4.5 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Averda

- 6.4.2 EnviroServ

- 6.4.3 Interwaste

- 6.4.4 WasteMart

- 6.4.5 Universal Recycling Company

- 6.4.6 Desco

- 6.4.7 PETCO

- 6.4.8 The Glass Recycling Company

- 6.4.9 Oricol Environmental Services

- 6.4.10 WeCyclers

- 6.4.11 The Waste Group

- 6.4.12 SA Waste

- 6.4.13 Veolia Africa

- 6.4.14 SUEZ Recycling & Recovery Africa

- 6.4.15 Biffa South Africa

- 6.4.16 Mr Green Africa

- 6.4.17 TakaTaka Solutions

- 6.4.18 EcoPost

- 6.4.19 Stericycle (MedWaste Africa)

- 6.4.20 Dangote Recycling

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

废弃物管理市场:依服务类型、废弃物类型、处理技术和最终用户划分-2026-2032年全球市场预测

废弃物管理市场:依服务类型、废弃物类型、处理技术和最终用户划分-2026-2032年全球市场预测 智慧废弃物管理市场预测至2034年-全球分析(按组件、废弃物类型、解决方案类型、技术、最终用户和地区划分)

智慧废弃物管理市场预测至2034年-全球分析(按组件、废弃物类型、解决方案类型、技术、最终用户和地区划分) 全球 PFAS废弃物管理市场:按处理技术、服务类型、最终用途产业和地区划分 - 预测(至 2031 年)

全球 PFAS废弃物管理市场:按处理技术、服务类型、最终用途产业和地区划分 - 预测(至 2031 年) 2026年全球多氟烷基物质(PFAS)废弃物管理市场报告2026年全球废弃物管理与回收服务市场报告2026年全球纺织废弃物管理市场报告2026年全球废弃物管理软体市场报告2026年全球放射性废弃物管理系统市场报告2026年全球水务和废弃物管理咨询服务市场报告

2026年全球多氟烷基物质(PFAS)废弃物管理市场报告2026年全球废弃物管理与回收服务市场报告2026年全球纺织废弃物管理市场报告2026年全球废弃物管理软体市场报告2026年全球放射性废弃物管理系统市场报告2026年全球水务和废弃物管理咨询服务市场报告 全球废弃物管理软体市场规模、份额、趋势和成长分析报告(2026-2034年)

全球废弃物管理软体市场规模、份额、趋势和成长分析报告(2026-2034年)