|

市场调查报告书

商品编码

1937316

汽车铝挤型:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Automotive Aluminium Extrusion - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

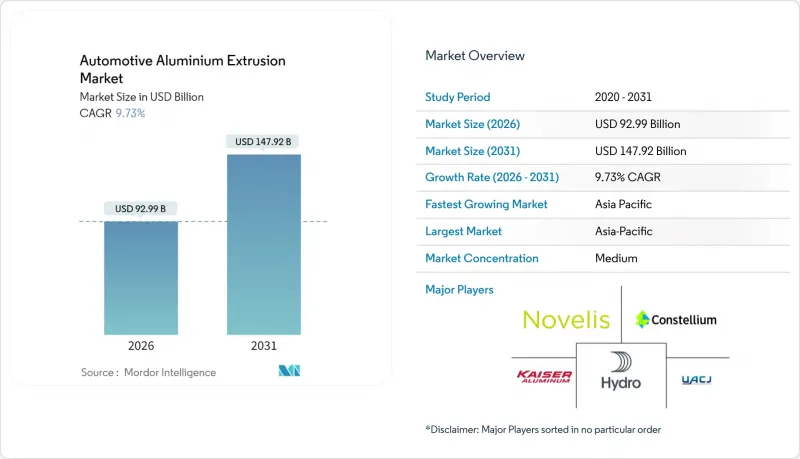

2025年汽车铝挤型市场价值为847.5亿美元,预计到2031年将达到1,479.2亿美元,而2026年为929.9亿美元。

预测期(2026-2031 年)的复合年增长率预计为 9.73%。

电动车平台加速转型是推动市场需求成长的主要动力,挤压铝材可用于製造轻量化白色车身结构、碰撞吸能导轨以及高效能电池的隔热外壳。合金化学和冲压技术的不断进步,使得製造复杂的中空型材成为可能,从而在不影响结构完整性的前提下减轻车辆重量。受美墨加协定(USMCA)和欧盟碳边境调节机制(CBAM)的推动,区域近岸外包正在重塑供应链,使其与国内冲压能力相匹配,预计仅在北美地区就将带来可观的资本投资。随着一体化铝生产商提高上游冶炼和下游挤压生产线的产能,以确保铝坯供应并实现闭合迴路回收,市场竞争日益激烈。同时,专业的Tier 1级製造商正透过复合材料连接技术和精密模具设计来提升自身竞争力。

全球汽车铝挤型市场趋势与洞察

美国、欧盟和中国的汽车二氧化碳排放法规和燃油效率标准

美国企业平均燃油经济性标准(CAFE)要求美国车辆到2026年平均燃油经济性达到40.4英里/加仑(约17.3公里/公升),而欧盟标准则规定到2025年二氧化碳排放不得超过95克/公里,并力争2035年实现近零排放。中国的双轨制同样鼓励轻量化材料,并对不达标者进行处罚。挤压铝材能够帮助汽车製造商减轻电池重量,避免高达数千美元的罚款,使其成为一种经济高效的优质材料。可预测的监管时间表增强了供应商对投资新模具和产能的信心。挤压成型具有可回收性、成熟的碰撞性能数据和可扩展的生产能力,使其优于镁合金和碳纤维等其他轻量化材料。

电池温度控管机壳需要复杂的中空挤压成型製程。

随着电池化学成分的温度范围日益收窄,多腔挤压成型製程将结构连接件和液冷路径整合到单一部件中,从而减少了接头和洩漏点。未来的固态电池将更加集中热量,对冷却的需求也随之增加,而钣金无法满足这项需求。整合式歧管可降低压力降和重量,表面处理则可提高其在乙二醇环境中的耐腐蚀性。跨车型标准化的电池组设计使挤压成型製造商能够实现规模经济,并优化合金成分以获得更优异的导热性能。连续焊接的中空型材简化了组装,从而实现了电动车的大量生产。

大型电动车型材生产线缺口超过3500万条。

儘管3500万吨以上的压平机仅占汽车行业设备容量的不到五分之一,但它们提供的长尺寸冲压能力对于生产电动车滑板车架和电池机壳至关重要。一条高吨位生产线造价可能在5000万美元到1亿美元之间,从下单到运作需要长达三年时间,这会延误供应。此外,由于设计复杂,可用的模具製造商数量也受到限制。区域差异依然存在。虽然亚洲在产能方面领先,但北美和欧洲的电动车产量远超过当地产能,迫使企业进口昂贵的大型零件。因此,汽车製造商正在与大型压平机机营运商签订多年产能预订协议,改变了传统的现货采购模式。

细分市场分析

受电动车电池组广泛应用的推动,电池机壳和温度控管模组将呈现最高的成长率,到2031年复合年增长率将达到9.79%。车身结构零件将保持最大份额,到2025年将占汽车铝挤型市场规模的37.21%,这得益于铝材优异的碰撞安全性。汽车铝挤型市场受益于巨型铸造技术,该技术需要在铸造的大型零件周围使用挤压加强筋。碰撞管理系统中可控制的变形特性有助于降低维修成本。由于其耐腐蚀性和可实现的高品质表面处理,外部饰件将保持稳定的市场份额。由于轻量化需求,座椅框架等内装模组在高端市场的需求不断增长。

零件配置正朝着多功能设计方向发展,将冷却、布线和结构负载路径整合到单一型材中。供应商利用有限元素分析来优化壁厚,并在无需机械加工的情况下整合凸台。边角料的闭合迴路回收符合原始设备製造商 (OEM) 的再生材料含量标准,进一步加强了买家与挤压合作伙伴之间的联繫。增材摩擦搅拌焊接技术无需热影响区即可连接长挤压件,从而形成连续的侧梁组件,取代多个冲压件。随着电动车的普及,电池专用组件将从利基市场走向主流市场,重塑全球冲压厂的订单结构。

预计到2025年,乘用车产量将占总产量的51.84%,年复合成长率(CAGR)为9.80%。这将是所有车型中占比最高的,因为消费者对电动车的接受速度超过了重型车辆基础设施的建设速度。轻型商用车将效仿电商物流车辆,实现城市道路的电气化。中型和重型卡车由于电池能量密度的限製而发展滞后,但随着兆瓦级充电技术的成熟,它们仍有成长空间。用于公车的铝挤型材提高了耐腐蚀性,有助于降低公共运输的生命週期成本。

与内燃机车相比,搭乘用电动车专案每辆车使用的挤压件数量更多,即使销量持平,也能带来更高的单车收入。 OEM平台在轿车、跨界车和掀背车衍生上采用通用挤压副车架,从而实现规模经济。随着商用车有效负载容量的重要性日益凸显,挤压地板樑和车顶拱架取代了冲压钢材,以减轻电池重量。随着法规日益严格,乘用车铝材用量将持续成为供应商生产力计画的重要指标。

区域分析

亚太地区将持续维持领先地位,到2025年将占全球需求的39.55%,复合年增长率达9.83%。光是中国一国在2024年提炼了大量原生铝,为下游挤压丛集提供具有成本竞争力的铝坯。国内电动车销量超过800万辆,确保了国内需求。日本在高端合金研发方面贡献力量,而韩国则凭藉其汽车组装的专业技术。从矾土开采到最终压铸钢轨的一体化生产模式缩短了前置作业时间,并降低了成本波动。

北美地区的成长得益于对挤压机设备和回收能力的计画投资。诺贝丽斯位于贝米内特的工厂新增60万吨产能,并与废料重熔环节全面整合,实现循环供应链。海德鲁公司位于宾夕法尼亚州的工厂扩建进一步巩固了在该地区的地位。美墨加协定(USMCA)的原产地规则以及对中国挤压件征收的反倾销税有助于维持其国内市场份额。加拿大丰富的水力发电资源减少了钢坯的碳足迹,从而支持了原始设备製造商(OEM)的永续性承诺。

欧洲高昂的能源价格和碳边境调节机制(CBAM)的引入,在推动低碳倡议的同时,也为传统冶炼厂带来了压力。挪威广泛采用水力发电锭和废钢原料,将有助于缓解成本压力。德国和瑞典的高阶OEM厂商正在指定使用先进的中空型材进行Gigacast增强,这使得供应商能够获得更高的利润。回收的强制性要求需要可追溯的废钢流通,从而推动了数据密集型价值链的发展,使数位化挤压製造商数位化受益。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国、欧盟和中国的车队二氧化碳排放和燃油经济性标准

- 电池温度控管机壳需要复杂的中空挤压件

- 一级挤出产能的近岸外包(美墨加协定、欧盟-CBAM)

- 电动车渗透率的提高将加速轻量化白车身的采用。

- 闭合迴路挤出生产线可节省成本并带来废料回收效益

- 用于高端电动车的超高速铸造和挤压成型混合底盘结构

- 市场限制

- 大型电动车型材压机缺口超过3,500条

- LME铝价波动与供应链投机

- 工程塑胶和碳纤维增强复合材料替代材料(用于内装应用)

- 欧盟碳税和区域碳排放税的转嫁风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(金额)

- 依组件类型

- 身体结构

- 碰撞管理系统

- 电池机壳和散热模组

- 外部装饰条和车顶行李架

- 内部模组

- 其他部件

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和大型卡车

- 巴士和长途汽车

- 按合金系列

- 可进行 6xxx 热处理

- 7xxx 高强度

- 5xxx 不可热处理

- 钪和新型合金

- 印刷能力

- 15分钟或更短

- 16~25 MN

- 26-35 MN

- 35分钟或以上

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 南美洲其他地区

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Constellium SE

- Novelis Inc.

- Norsk Hydro ASA

- Kaiser Aluminum Corp.

- UACJ Corp.

- Arconic Corp.

- Kobe Steel Ltd.

- Benteler International

- Bonnell Aluminum

- Hindalco Industries Ltd.

- Guangdong Hongtu

- ETEM Automotive

- Talco Aluminium Company

- Granges AB

- Press-Metal Aluminium

- Sapa Extrusions

- Exlabesa

- Walter Klein GmbH

- Omnimax International

- Innoval Technology

第七章 市场机会与未来展望

The Automotive Aluminium Extrusion Market was valued at USD 84.75 billion in 2025 and estimated to grow from USD 92.99 billion in 2026 to reach USD 147.92 billion by 2031, at a CAGR of 9.73% during the forecast period (2026-2031).

Demand momentum stems from the accelerated shift to electric vehicle (EV) platforms, where extruded aluminum supports lightweight body-in-white structures, crash-energy absorption rails, and high-efficiency battery thermal enclosures. Continual improvements in alloy chemistry and press technology unlock complex hollow profiles that shave curb weight without sacrificing structural integrity. Regional near-shoring, prompted by USMCA rules and the EU Carbon Border Adjustment Mechanism (CBAM), is realigning supply chains toward domestic press capacity, and capital expenditure commitments exceed a huge amount in North America alone. Competitive intensity rises as integrated aluminum producers fortify upstream smelting with downstream extrusion lines to guarantee billet availability and closed-loop recycling. At the same time, specialized Tier-1 houses differentiate through multi-material joining and precision die design.

Global Automotive Aluminium Extrusion Market Trends and Insights

Fleet CO2 & Fuel-Economy Mandates in the U.S., EU, China

Corporate Average Fuel Economy rules require 40.4 mpg U.S. fleet averages by 2026, while EU standards fix 95 g CO2/km for 2025 and move toward near-zero emissions by 2035 . China's dual-credit system likewise rewards lightweight materials and penalizes non-compliance. Extruded aluminum enables automakers to offset battery weight and avoid multi-thousand-dollar fines, making the material premium cost-effective. Predictable regulation timetables give suppliers confidence to fund new tooling and capacity. Proven recyclability, mature crash performance data, and scalable production tip the balance of extrusion over competing lightweighting options such as magnesium or carbon fiber.

Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

As battery chemistries tolerate narrower temperature windows, multi-chamber extrusions combine structural mounting with liquid-coolant paths in a single part, cutting joints and leak points. Future solid-state batteries concentrate heat, intensifying cooling needs that sheet metal cannot meet. Integrated manifolds lower pressure drop and weight, while surface treatments boost corrosion resistance in glycol environments. Standardized pack designs across vehicle lines allow extrusion houses to realize economies of scale and refine alloy recipes for superior thermal conductivity. Continuous-weld hollow profiles also simplify assembly, enabling high-volume EV production.

Scarcity of More Than 35 MN Press Lines for Large EV Profiles

Presses above 35 MN account for less than one-fifth of installed automotive capacity, yet EV skateboard frames and battery enclosures require the extended lineal lengths these machines provide. A single high-tonnage line costs USD 50-100 million and needs up to three years from order to commissioning, slowing supply response. The design complexity further limits the number of qualified toolmakers. Regional imbalances persist: Asia leads installed base, while North American and European EV output surges past local capability, forcing expensive oversize component imports. Consequently, OEMs sign multi-year capacity reservations with large-press operators, altering traditional spot-buy sourcing models.

Other drivers and restraints analyzed in the detailed report include:

- Near-Shoring of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- LME Aluminum Price Volatility & Supply-Chain Speculation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Battery enclosures and thermal modules deliver the fastest 9.79% CAGR through 2031 as EV packs proliferate. Body structure elements still generated the largest 37.21% slice of the automotive aluminum extrusion market size in 2025, underscoring aluminum's crash-worthiness. The automotive aluminum extrusion market benefits from gigacasting, which necessitates extruded reinforcement rails around cast mega-components. Controlled deformation characteristics in crash-management systems lower repair costs. Exterior trim maintains a steady share thanks to corrosion resistance and premium finish opportunities. Interior modules like seat frames gain traction in luxury segments that chase every kilogram of savings.

The component mix evolves with multi-functional designs integrating cooling, routing, and structural load paths in a single profile. Suppliers leverage finite-element modeling to optimize wall thickness and incorporate bosses without machining. Closed-loop recycling of off-cuts meets OEM recycled-content quotas, further tying buyers to extrusion partners. Additive friction stir welding joins long extrusions without heat-affected zones, enabling contiguous side-sill assemblies that replace multiple stampings. As EV adoption accelerates, battery-specific components will rise from niche to mainstream, reshaping order books across global presses.

Passenger cars accounted for 51.84% of 2025 volumes and are forecast to grow at a 9.80% CAGR-the highest among vehicle classes-because consumer EV uptake outpaces infrastructure build-out for heavier segments. Light commercial vans follow as e-commerce logistics fleets electrify inner-city routes. Medium and heavy trucks lag due to battery-energy density limits, but present upside once megawatt charging matures. Aluminum extrusions in buses improve corrosion resistance, lowering lifetime operating costs for public transit agencies.

Passenger EV programs feature higher extrusion kilograms per vehicle than combustion variants, driving per-unit revenue growth even in flat volume scenarios. OEM platforms share common extruded sub-frames across sedan, crossover, and hatchback derivatives, boosting economies of scale. Commercial vehicles emphasize payload, so extruded floor beams and roof bows substitute press-formed steel, offsetting battery mass. As regulatory milestones tighten, passenger car aluminum intensity remains the bellwether for supplier capacity planning.

The Automotive Aluminum Extrusion Market Report is Segmented by Component Type (Body Structure, Crash-Management Systems, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Alloy Series (6xxx Heat-Treatable and More), Press Capacity (Less Than or Equal To15 MN, 16-25 MN, 26-35 MN, and More Than 35 MN), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 39.55% of 2025 demand, and its 9.83% CAGR keeps the region in pole position. China alone smelted over a high amount of primary aluminum in 2024, furnishing cost-competitive billet to downstream extrusion clusters. Domestic EV sales exceed 8 million units, guaranteeing local offtake. Japan contributes high-end alloy R&D, while South Korea leverages automotive assembly expertise. Integrating bauxite mines to final crash rails compresses lead times and dampens cost volatility.

North America's growth is supported by announced investments in extrusion presses and recycling capacity. Novelis's Bay Minette mill adds 600,000 tonnes of capacity, fully integrated with scrap re-melt for closed-loop supply. Hydro's Pennsylvania upgrade further embeds regional capability. USMCA rules of origin and antidumping duties on Chinese extrusions fortify the domestic share. Abundant hydropower in Canada cuts billet carbon footprint, supporting OEM sustainability pledges .

Europe's high energy prices and CBAM implementation squeeze legacy smelters but stimulate low-carbon initiatives. Norwegian hydro-powered ingot and broader adoption of scrap feedstock mitigate cost headwinds. Premium-segment OEMs in Germany and Sweden specify advanced hollow profiles for gigacast reinforcement, enabling suppliers to command value-added margins. Recycling mandates demand traceable scrap loops, promoting data-rich supply chains that reward digitalized extruders.

- Constellium SE

- Novelis Inc.

- Norsk Hydro ASA

- Kaiser Aluminum Corp.

- UACJ Corp.

- Arconic Corp.

- Kobe Steel Ltd.

- Benteler International

- Bonnell Aluminum

- Hindalco Industries Ltd.

- Guangdong Hongtu

- ETEM Automotive

- Talco Aluminium Company

- Granges AB

- Press-Metal Aluminium

- Sapa Extrusions

- Exlabesa

- Walter Klein GmbH

- Omnimax International

- Innoval Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Fleet Co2 & Fuel-Economy Mandates In US, EU, China

- 4.2.2 Battery Thermal-Management Enclosures Require Complex Hollow Extrusions

- 4.2.3 Near-Shoring Of Tier-1 Extrusion Capacity (USMCA, EU-CBAM)

- 4.2.4 Rising EV Penetration Accelerates Lightweight Body-In-White Adoption

- 4.2.5 Cost-Out & Scrap-Recycling Gains From Closed-Loop Extrusion Lines

- 4.2.6 Gigacasting-Extrusion Hybrid Chassis Architectures In Premium EVs

- 4.3 Market Restraints

- 4.3.1 Scarcity Of More Than 35 Mn Press Lines For Large EV Profiles

- 4.3.2 LME Aluminum Price Volatility & Supply-Chain Speculation

- 4.3.3 Engineering Plastics & CFRP Alternatives For Interiors

- 4.3.4 EU-CBAM & Regional Carbon-Tax Pass-Through Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Component Type

- 5.1.1 Body Structure

- 5.1.2 Crash-Management Systems

- 5.1.3 Battery Enclosures and Thermal Modules

- 5.1.4 Exterior Trim and Roof Rails

- 5.1.5 Interior Modules

- 5.1.6 Other Components

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy-Duty Trucks

- 5.2.4 Buses and Coaches

- 5.3 By Alloy Series

- 5.3.1 6xxx Heat-Treatable

- 5.3.2 7xxx High-Strength

- 5.3.3 5xxx Non-Heat-Treatable

- 5.3.4 Scandium & Novel Alloys

- 5.4 By Press Capacity

- 5.4.1 Less than or equal to 15 MN

- 5.4.2 16-25 MN

- 5.4.3 26-35 MN

- 5.4.4 More than 35 MN

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Constellium SE

- 6.4.2 Novelis Inc.

- 6.4.3 Norsk Hydro ASA

- 6.4.4 Kaiser Aluminum Corp.

- 6.4.5 UACJ Corp.

- 6.4.6 Arconic Corp.

- 6.4.7 Kobe Steel Ltd.

- 6.4.8 Benteler International

- 6.4.9 Bonnell Aluminum

- 6.4.10 Hindalco Industries Ltd.

- 6.4.11 Guangdong Hongtu

- 6.4.12 ETEM Automotive

- 6.4.13 Talco Aluminium Company

- 6.4.14 Granges AB

- 6.4.15 Press-Metal Aluminium

- 6.4.16 Sapa Extrusions

- 6.4.17 Exlabesa

- 6.4.18 Walter Klein GmbH

- 6.4.19 Omnimax International

- 6.4.20 Innoval Technology

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment