|

市场调查报告书

商品编码

1937329

装饰照明:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Decorative Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

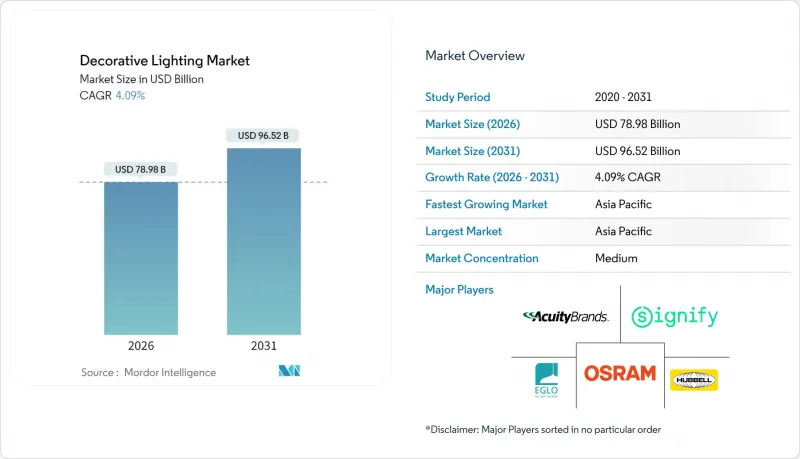

2025年装饰照明市场价值为758.8亿美元,预计到2031年将达到965.2亿美元,而2026年为789.8亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.09%。

LED成本下降、智慧家庭普及以及持续的维修热潮,共同推动了这一稳定成长。随着语音生态系统的日益普及,製造商正从独立的装饰元素转向原生支援Matter和Thread的灯具,将照明转变为更广泛的住宅和商业物联网架构中的功能节点。在美国对中国产品征收104%关税后,生产网路正在重新调整。拥有成熟的多国采购和铜对冲策略的公司能够在保持交货可靠性的同时,缓解成本衝击。无线充电灯、均匀发光的OLED面板和太阳能混合动力花园灯丰富了消费者的选择,而设计师则将以人性化的灯光模式和色彩变换功能融入设计,以提升职场和酒店等场所的舒适度。永续性的要求,特别是欧洲的循环经济政策,有利于那些记录产品可回收性、发布环境产品声明(EPD)并提供可拆卸灯具的品牌。

全球装饰照明市场趋势与洞察

LED价格大幅下降,效率不断提高。

到2025年,LED组件价格将降至每瓦0.12美元以下,装饰灯具将实现75%的节能效果和5万小时的使用寿命,从而重塑整体拥有成本的计算方式。随着显色指数(CRI)超过90,饭店品牌无需再为了提高效率而牺牲色彩的温暖度,从而加快了大厅、餐厅和客房的灯具更换週期。住宅用户正从白炽灯氛围照明转向以灯丝为基础的LED灯,后者在保持復古美感的同时,能耗仅为白炽灯的一半。同时,更小的散热器使得以往大型灯体无法实现的雕塑感设计成为可能。这些经济效益正推动着控制光束扩散的光学技术的研究与开发,使设计师能够分层布置重点照明和工作照明,而不会出现明显的光斑。

智慧家庭平台整合(Matter、Thread)

Matter认证使得单一装饰吊灯即可与亚马逊、Google和苹果的智慧家庭中心同步,避免了零售商SKU的繁杂。 Thread的低功耗网状网路技术解决了砖石建筑的讯号覆盖范围难题,使无线床头壁灯能够可靠地回应语音指令。物业管理人员正竞相采购支援Matter技术的水晶灯,以便维修人员无需亲临现场即可远端排查高层建筑的故障。饭店正在部署集中式控制面板,只需轻轻一触即可将大厅氛围从日间切换至温馨的夜晚,从而在整个连锁饭店中强化一致的品牌体验。随着整合商采用开放通讯协定,采购团队除了专注于产品外观,也开始优先考虑其耐用性和网路安全认证。

装饰玻璃和金属产品供应链的波动

对中国製造的照明灯具征收关税显着提高了到岸成本,迫使供应商网路有限的小众品牌寻找替代货源。虽然越南和墨西哥正在消化部分需求,但专用于厚玻璃工艺的熔炉供应仍然有限,导致交货时间延长,与快速发展的装饰市场需求相衝突。此外,铜价持续在每磅5美元以上波动,加剧了依赖黄铜外壳的吊灯製造商的成本压力。规模较大、业务多元化的公司正透过采取避险策略和引入模组化设计来缓解这些挑战,这些模组化设计便于材料替代,例如用钢代替黄铜而无需对设备进行重大改造。同时,小规模的工坊则延后产品发布或缩减订单量以维持现金流。这些趋势凸显了产业相关人员在不断变化的市场环境下所面临的营运和财务压力。

细分市场分析

预计到2025年,吸顶灯和水晶灯的市场收入将达到265.8亿美元,占装饰照明市场35.02%的份额。这一市场主导地位的驱动力源于新建和维修项目中预算增加的趋势,这些项目将「吸睛」灯具作为客厅和大堂空间的视觉焦点。计划设计师正在利用LED灯丝灯泡和半透明压克力扩散器打造出比传统石英灯更轻盈、更具立体感的造型,从而便于在石膏板天花板中安装。同时,製造商正在整合Matter智慧驱动器,使用户能够透过语音助理调节色温,从暖白光(用餐)到冷白光(工作)。入门级建筑商正在采用预接线座舱罩,以加快室内设计流程并减少现场施工。而高端住宅则委託捷克和穆拉诺的工坊定制水晶灯,并将模组化组件运送到现场进行组装。这为手工玻璃製程的发展指明了方向,将智慧驱动系统与精密加工的铝製框架结合。

预计到2025年,檯灯和落地灯的市场规模将达到119.3亿美元,并在2031年之前以5.21%的最快成长。这主要得益于锂电池密度的提升,使其无线使用时间长达15小时。随着灵活办公模式的普及,房间的功能界限变得模糊,消费者可以自由地在办公桌、沙发和露台之间移动灯具,而无需拖曳电线。各大品牌正将灯具打造为多功能中心,在其底座中整合USB-C充电接口和Qi无线充电板,方便为智慧型手机和耳机充电。零售产品系列正趋向于采用雾面黄铜饰面的中世纪风格设计,而AR应用程式的分析也证实了灯具摆放在餐边柜和床头柜上的趋势。同时,壁灯内建PIR感测器,可用于实现走廊和卫生间的自动化照明,从而促进与整合式环境照明的镜子进行交叉销售。轨道灯也不断扩展其产品线,采用模组化设计,可将磁性灯头吸附在天花板轨道上。零售商正在销售包含聚光灯模组和洗墙透镜的入门套件,提案画廊式的住宅展示效果。

到2025年,LED技术将占据装饰照明市场70.12%的份额,这主要得益于其类似白炽灯的灯丝状灯泡,这些灯泡能够模拟白炽灯的光线,同时达到110流明/瓦的能效。製造商正在探索分段式光学设计,将窄光束重点模组与漫射背光结合在单一水晶灯中,展现了LED的多功能性。随着2026年公用事业补贴的结束,人们的焦点将从投资回报转向健康,可调光白光LED灯具的价格也将因此走高。同时,OLED面板和太阳能混合动力系统在2025年的营收将达到25.3亿美元,复合年增长率(CAGR)为4.88%。超薄OLED面板兼具气氛照明和墙面装饰的功能,目前已在东京和柏林的精品设计店中销售。由于采用了高效能单晶硅面板和可循环充放电超过 3000 次的磷酸铁锂电池,太阳能花园灯的输出亮度已飙升至 1800 流明。

随着监管日益严格,白炽灯和卤素灯的市场份额将萎缩至装饰照明市场规模的5%以下。然而,精品饭店的设计师仍坚持在酒吧等隐密场所使用2400K色温的白炽灯泡,他们认为这种温暖的怀旧感是某些LED仿製品无法复製的。由于严格的色温标准,萤光和节能灯的市场份额正在下降,而维修需求则完全转向LED灯管或整合式驱动器。展望未来,微型LED阵列的研发投入将带来更大的设计自由度,这种阵列具有类似OLED的表面发光特性,但使用寿命更长。

区域分析

预计到2025年,亚太地区市场规模将达到270.9亿美元,占全球整体市场的35.70%,并预计在2031年之前以5.98%的复合年增长率增长,增长最快。中国广东出口基地继续主导玻璃帘子和压铸外壳的生产,随着都市区公寓的竣工,国内消费不断增长,进一步巩固了其市场主导地位。印度的模组化开关市场正以7.99%的复合年增长率成长,这标誌着电气化进程的推进以及装饰灯具升级的趋势。新加坡、马来西亚和泰国正在鼓励住宿设施走廊进行智慧LED维修,以达到能源强度目标,从而维持了对连网壁灯的需求。在日本,高阶OLED壁灯正逐渐受到欢迎,以解决微型公寓的空间限制问题。同时,澳洲住宅维修热潮推动了耐盐雾粉末涂层户外吊灯的销售。

在北美,强劲的住宅净值和智慧音箱的广泛普及推动了灯具更换需求。 Matter 的互通性尤其受到青睐,因为住宅更倾向于使用应用程式来管理水晶灯、嵌入式下照灯和装饰灯,只需一个语音指令即可完成控制。商业房地产正在采用人性化的大厅照明设计,以吸引采用混合办公模式的员工;而供应链回流则促使零售商选择可以规避关税的墨西哥製造的金属机壳供应商。

在欧洲,永续性是重中之重,公共竞标要求提供环境产品声明 (EPD) 文件,并优先考虑可拆卸式灯具。在德国,受包浩斯风格启发的再生铝製吊灯深受环保意识强的消费者欢迎;而在义大利,传统的穆拉诺玻璃与调暗时会发热的 LED 灯丝相结合。在荷兰,循环租赁模式正在试验推行,允许饭店在五年后归还吊灯进行翻新和再利用,从而将循环经济理念融入品牌故事。英国脱欧带来的复杂局面持续为进口分销带来挑战,当地仓库正努力延长前置作业时间。

儘管拉丁美洲和中东地区的收入份额较小,但受大规模酒店计划的推动,这些地区的成长速度高于平均水平。沙乌地阿拉伯的娱乐区正在指定使用具有可程式设计RGBW节点的巨型动态水晶灯,这迫使当地的系统整合商提升其DMX程式设计技能。在巴西,度假村业者更倾向于使用太阳能混合式花园灯笼,这种灯笼可以降低偏远海滩场所的钻孔成本。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- LED价格大幅下降,效率不断提高。

- 智慧家庭平台整合(Matter、Thread)

- 新冠疫情后,DIY室内装修改造热潮兴起

- 电子商务视觉化工具(AR/VR)

- 政府对节能照明的奖励措施

- 可支配收入的增加推动了对高檔配件的消费

- 市场限制

- 装饰玻璃和金属製品供应链波动性

- 大众市场住宅者的价格敏感度

- 智慧照明设备的前期成本较高

- 假冒仿冒品产品的氾滥

- 产业价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解近期产业发展动态(新产品发布、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模及成长预测(金额:美元)

- 依产品类型

- 吸顶灯和水晶灯

- 吊坠

- 壁挂式照明灯具

- 檯灯和落地灯

- 轨道灯

- 其他产品类型

- 透过光源

- LED

- 白炽灯泡

- 萤光/节能灯

- 卤素

- 其他(有机发光二极体、太阳能发电等)

- 最终用户

- 住宅

- 商业的

- 透过分销管道

- B2C/零售通路

- 大卖场和超级市场

- 家居建材商店

- 专业照明商店

- 在线的

- 其他分销管道

- B2B/直销和计划

- B2C/零售通路

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 秘鲁

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 比荷卢经济联盟(比利时、荷兰、卢森堡)

- 北欧国家(丹麦、芬兰、冰岛、挪威、瑞典)

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 东南亚(新加坡、马来西亚、泰国、印尼、越南、菲律宾)

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Acuity Brands Lighting

- Artemide SpA

- Cree Lighting

- Eglo Leuchten GmbH

- FLOS SpA

- Foscarini Srl

- General Electric Co.

- Havells India Ltd

- Hubbell Incorporated

- Jaquar Lighting

- Kichler Lighting LLC

- Lamps Plus

- Lutron Electronics Co., Inc.

- Nora Lighting

- Opple Lighting

- Osram Licht AG

- Signify(Philips Lighting)

- Vibia Lighting

- WAC Lighting

- Xiaomi(Yeelight)

第七章 市场机会与未来展望

The decorative lighting market was valued at USD 75.88 billion in 2025 and estimated to grow from USD 78.98 billion in 2026 to reach USD 96.52 billion by 2031, at a CAGR of 4.09% during the forecast period (2026-2031).

LED cost erosion, rising smart-home adoption, and a sustained renovation boom jointly underpin this steady expansion. As voice-enabled ecosystems normalize, manufacturers pivot from isolated aesthetic pieces toward fixtures that natively support Matter and Thread, thereby converting lighting into a functional node within a larger residential or commercial IoT stack. Production networks are re-balancing after 104% U.S. tariffs on Chinese imports; firms that lock in multi-country sourcing and copper hedges buffer cost shocks while maintaining delivery reliability. Cordless rechargeable lamps, uniform-emission OLED panels, and solar-hybrid garden lanterns broaden consumer choice, while designers rely on human-centric light profiles that shift hue to boost wellness in workplaces and hospitality venues. Sustainability imperatives-especially Europe's circular-economy mandates-favor brands that document recyclability, publish Environmental Product Declarations, and engineer fixtures for disassembly.

Global Decorative Lighting Market Trends and Insights

Rapid LED Price Erosion & Efficiency Gains

LED component prices slid below USD 0.12 per watt in 2025, letting decorative fixtures deliver 75% energy savings and 50,000-hour lifespans that recast total ownership calculations. As CRI values exceed 90, hospitality brands no longer trade color warmth for efficiency, accelerating replacement cycles across lobbies, restaurants, and guest rooms. Residential adopters migrate from incandescent ambience toward filament-style LEDs that keep vintage aesthetics yet halve power draw. Simultaneously, miniaturized heat sinks unlock sculptural designs once infeasible with bulkier lamp bodies. These economics redirect R&D toward optics that modulate beam spread, empowering designers to layer accent and task lighting without perceptible hotspots.

Smart-Home Platform Integration (Matter, Thread)

Matter certification now ensures a single decorative pendant can sync with Amazon, Google, and Apple hubs, sparing retailers from SKU proliferation. The thread's low-power mesh solves coverage gaps in masonry-heavy dwellings, enabling cordless bedside sconces to respond reliably to voice commands. Facility managers insist on Matter-ready chandeliers so maintenance staff can troubleshoot remotely rather than accessing high-ceiling installations. Hotels deploy centralized dashboards that change lobby ambience from daylight to evening warmth at a touch, fortifying brand experience consistently chain-wide. As integrators standardize open protocols, procurement teams weigh longevity and cybersecurity certifications alongside style.

Supply-Chain Volatility for Decorative Glass & Metals

The imposition of tariffs on Chinese fixtures has substantially increased landed costs, compelling niche brands with limited supplier networks to explore alternative sourcing options. While Vietnam and Mexico have absorbed some of the demand, the availability of furnaces designed for thick artisan glass remains limited, leading to extended lead times that conflict with the fast-evolving decor market. Additionally, copper prices, which have been fluctuating above USD 5.00 per pound, are exacerbating cost pressures for pendant manufacturers reliant on spun brass housings. Larger, diversified players are mitigating these challenges by employing hedging strategies and adopting modular designs that facilitate material substitution, such as replacing brass with steel, without requiring significant retooling. Conversely, smaller ateliers are deferring product launches or reducing collection sizes to preserve cash flow. These dynamics highlight the operational and financial pressures faced by industry participants amid shifting market conditions.

Other drivers and restraints analyzed in the detailed report include:

- DIY Interior-Upgrade Boom Post-COVID

- E-commerce Visualization Tools (AR/VR)

- Counterfeit Low-Quality Products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ceiling lights and chandeliers accounted for USD 26.58 billion of 2025 revenue, representing 35.02% of the decorative lighting market size. Their dominance stems from new-build construction and renovation priorities that allocate budget to a central "statement" piece anchoring living or lobby spaces. Project designers exploit LED filament bulbs and translucent acrylic diffusers to craft voluminous forms that weigh less than legacy crystal models, easing installation on gypsum ceilings. At the same time, manufacturers integrate Matter-ready drivers so owners can adjust color temperature from warm-white dinners to cool-white task settings via voice assistants. Entry-level builders adopt pre-wired canopies that accelerate fit-out schedules, reducing job-site labor. Luxury homeowners commission bespoke chandeliers from Czech and Murano studios that ship modular sections for on-site assembly, demonstrating how artisan glass survives by aligning with smart drivers and precision-cut aluminum frames.

Table and floor lamps, valued at USD 11.93 billion in 2025, deliver the fastest 5.21% CAGR through 2031, catalyzed by lithium-battery density improvements that enable 15-hour cordless operation. As flexible working blurs room functions, consumers reposition lamps between desks, sofas, and terraces without trailing cords. Brands emphasize USB-C charging and Qi wireless pads in bases, converting lamps into multi-utility hubs that power phones and earbuds. Retail assortments skew toward mid-century silhouettes in matte-brass finishes, verified by AR app analytics that flag user placement preferences for sideboards and bedside tables. Meanwhile, wall sconces integrate PIR sensors to automate hallways and powder rooms, seeding cross-sales of matching mirrors with embedded perimeter lighting. Track lighting rounds out the product hierarchy with modular magnetic heads that snap onto ceiling rails, letting retailers market starter kits bundled with accent spot modules and wash lenses for gallery-style residential displays.

LED technology secured 70.12% of the decorative lighting market share in 2025 as filament-style bulbs replicate the incandescent glow while delivering 110 lm/W efficiencies. Manufacturers pursue segmented optics that combine narrow beam accent modules with diffuse backlights inside a single chandelier, showcasing LED versatility. Utility rebate sunsets after 2026 shift conversation from payback to wellness, positioning tunable-white LEDs at premium price points. Simultaneously, OLED panels and solar-hybrid engines together logged USD 2.53 billion in 2025 revenue, advancing at a 4.88% CAGR. Paper-thin OLED sheets enable wall art that doubles as mood lighting, selling through design-forward boutiques in Tokyo and Berlin. Solar garden lanterns leap to 1,800 lumen outputs courtesy of higher-efficiency mono-crystalline panels and LiFePO4 batteries that cycle 3,000+ times.

Incandescent and halogen categories shrink below 5% of the decorative lighting market size as regulatory bans tighten. Yet boutique hospitality designers still specify 2,400 K filament bulbs in speakeasy bars, citing warm nostalgia unsatisfied by some LED replicas. Fluorescent and CFL units fade under harsh color critique, redirecting retrofit demand squarely into LED tubes or integrated drivers. Looking forward, R&D invests in micro-LED arrays that promise OLED-like surface emission but longer lifespans, foreshadowing another leap in design freedom.

The Global Decorative Lighting Market Report is Segmented by Product Type (Ceiling Lights & Chandeliers, Pendants, Wall Sconces, and More), Light Source (LED, Incandescent, Fluorescent & CFL, Halogen, Others), End-User (Residential, Commercial), Distribution Channel (B2C/Retail Channels, B2B/Direct Sales & Projects), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated USD 27.09 billion in 2025, translating to 35.70% of global value and the fastest 5.98% CAGR through 2031. China's export clusters in Guangdong continue to dominate glass shade and die-cast housing output even as domestic consumption climbs with urban condominium completions. India's modular switch segment, growing at 7.99% CAGR, signals broader electrification that dovetails with decorative fixture upgrades. Singapore, Malaysia, and Thailand incentivize smart LED retrofits in hospitality corridors to hit energy-intensity targets, sustaining demand for networkable sconces. Japan tilts toward premium OLED wall art addressing space constraints in micro-apartments, while Australia's home-renovation wave fuels sales of coastal-proof outdoor pendants powder-coated against salt spray.

North America displays replacement-driven dynamics underpinned by robust housing equity and wide smart-speaker penetration. Matter interoperability gains particular traction as homeowners declutter apps, preferring one voice command to operate chandeliers, recessed cans, and accent lanterns. Commercial retrofits install human-centric lobby lighting aimed at enticing employees back in hybrid work patterns, while supply-chain reshoring steers retailers toward Mexican metallic housing suppliers that skirt tariffs.

Europe foregrounds sustainability, requiring EPD documentation for public tenders and favoring fixtures engineered for disassembly. Germany's Bauhaus-inspired armature lamps in recycled aluminum resonate with eco-savvy consumers, whereas Italy merges heritage Murano glass with dim-to-warm LED filaments. The Netherlands pilots circular-leasing contracts where hotels return pendants after five years for refurbish-and-reuse cycles, embedding circularity into brand narratives. Brexit complexities continue to challenge U.K. import flows, prompting local warehouses to buffer lead times.

Latin America and the Middle East, though smaller in revenue share, record above-average growth courtesy of hospitality megaprojects. Saudi Arabia's entertainment districts specify large-scale kinetic chandeliers with programmable RGBW nodes, pushing local integrators to upskill in DMX programming. Brazilian resort operators favor solar-hybrid garden lanterns that cut trenching costs in remote beach properties.

- Acuity Brands Lighting

- Artemide S.p.A.

- Cree Lighting

- Eglo Leuchten GmbH

- FLOS S.p.A.

- Foscarini S.r.l.

- General Electric Co.

- Havells India Ltd

- Hubbell Incorporated

- Jaquar Lighting

- Kichler Lighting LLC

- Lamps Plus

- Lutron Electronics Co., Inc.

- Nora Lighting

- Opple Lighting

- Osram Licht AG

- Signify (Philips Lighting)

- Vibia Lighting

- WAC Lighting

- Xiaomi (Yeelight)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED price erosion & efficiency gains

- 4.2.2 Smart-home platform integration (Matter, Thread)

- 4.2.3 DIY interior-upgrade boom post-COVID

- 4.2.4 E-commerce visualisation tools (AR/VR)

- 4.2.5 Government incentives for energy-efficient lighting

- 4.2.6 Rising disposable income driving premium decor spend

- 4.3 Market Restraints

- 4.3.1 Supply-chain volatility for decorative glass & metals

- 4.3.2 Price sensitivity in mass-market residential buyers

- 4.3.3 High upfront cost of connected/smart luminaires

- 4.3.4 Proliferation of counterfeit low-quality products

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Ceiling Lights & Chandeliers

- 5.1.2 Pendants

- 5.1.3 Wall Sconces

- 5.1.4 Table & Floor Lamps

- 5.1.5 Track Lights

- 5.1.6 Other Product Types

- 5.2 By Light Source

- 5.2.1 LED

- 5.2.2 Incandescent

- 5.2.3 Fluorescent & CFL

- 5.2.4 Halogen

- 5.2.5 Others (OLED, Solar, etc.)

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 B2C/Retail Channels

- 5.4.1.1 Hypermarkets and Supermarkets

- 5.4.1.2 Home Centers

- 5.4.1.3 Specialty Lighting Stores

- 5.4.1.4 Online

- 5.4.1.5 Other Distribution Channels

- 5.4.2 B2B/Direct Sales & Projects

- 5.4.1 B2C/Retail Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Peru

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.5.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Acuity Brands Lighting

- 6.4.2 Artemide S.p.A.

- 6.4.3 Cree Lighting

- 6.4.4 Eglo Leuchten GmbH

- 6.4.5 FLOS S.p.A.

- 6.4.6 Foscarini S.r.l.

- 6.4.7 General Electric Co.

- 6.4.8 Havells India Ltd

- 6.4.9 Hubbell Incorporated

- 6.4.10 Jaquar Lighting

- 6.4.11 Kichler Lighting LLC

- 6.4.12 Lamps Plus

- 6.4.13 Lutron Electronics Co., Inc.

- 6.4.14 Nora Lighting

- 6.4.15 Opple Lighting

- 6.4.16 Osram Licht AG

- 6.4.17 Signify (Philips Lighting)

- 6.4.18 Vibia Lighting

- 6.4.19 WAC Lighting

- 6.4.20 Xiaomi (Yeelight)

7 Market Opportunities & Future Outlook

- 7.1 LED Innovation Enhancing Energy Efficiency Appeal

- 7.2 Customizable Fixtures Catering to Personal Lifestyles

- 7.3 Premium Aesthetics Influencing High-End Adoption

装饰照明市场:全球市场按产品类型、技术、销售管道、应用和最终用户分類的预测——2026-2032年

装饰照明市场:全球市场按产品类型、技术、销售管道、应用和最终用户分類的预测——2026-2032年 2026年全球装饰照明市场报告太阳能串灯市场:按分销管道、应用、最终用户、安装类型、功率和连接方式划分,全球预测(2026-2032年)

2026年全球装饰照明市场报告太阳能串灯市场:按分销管道、应用、最终用户、安装类型、功率和连接方式划分,全球预测(2026-2032年) 装饰照明市场规模、份额、趋势及预测(按产品类型、光源、分销管道、最终用户和地区划分),2026-2034年

装饰照明市场规模、份额、趋势及预测(按产品类型、光源、分销管道、最终用户和地区划分),2026-2034年 装饰照明市场-全球产业规模、份额、趋势、机会和预测:按产品、应用、销售管道、地区和竞争格局划分,2021-2031年

装饰照明市场-全球产业规模、份额、趋势、机会和预测:按产品、应用、销售管道、地区和竞争格局划分,2021-2031年 装饰性住宅照明市场预测至2032年:按产品类型、材料、价格范围、分销管道和地区分類的全球分析

装饰性住宅照明市场预测至2032年:按产品类型、材料、价格范围、分销管道和地区分類的全球分析 装饰照明市场规模、份额及成长分析(按产品、类型、光源、应用和地区划分)-2026-2033年产业预测

装饰照明市场规模、份额及成长分析(按产品、类型、光源、应用和地区划分)-2026-2033年产业预测 全球装饰照明市场

全球装饰照明市场 装饰照明市场规模、份额、趋势分析报告:按产品、按应用、按光源、按地区、细分市场预测,2025-2030LED窗帘灯的全球市场

装饰照明市场规模、份额、趋势分析报告:按产品、按应用、按光源、按地区、细分市场预测,2025-2030LED窗帘灯的全球市场