|

市场调查报告书

商品编码

1937340

基底金属:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Base Metals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

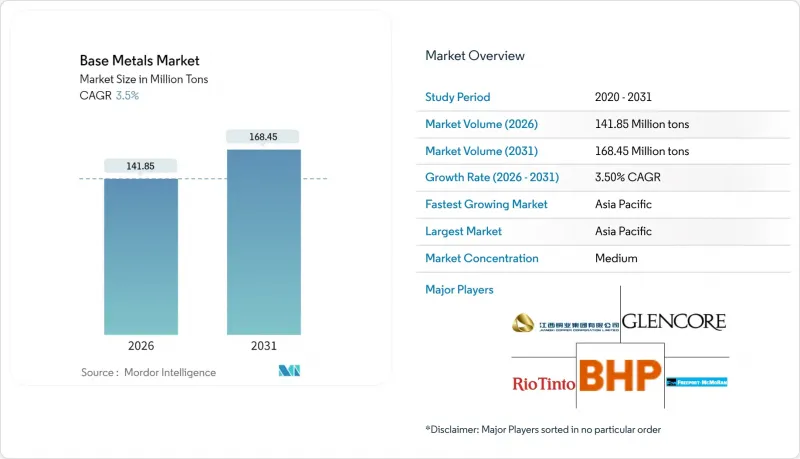

预计到 2026 年,基底金属市场规模将达到 1.4185 亿吨,高于 2025 年的 1.3705 亿吨,预计到 2031 年将达到 1.6845 亿吨。

预计从 2026 年到 2031 年,其复合年增长率将达到 3.5%。

这一稳步增长的趋势得益于持续的电气化、不断扩大的基础设施更新以及从纯粹的大规模生产向价值驱动型生产的转变。矿业公司如今优先考虑的是策略定位、供应安全和技术效率,而非激进的新资本投资。同时,下游製造商在日益增长的政策压力下,努力在成本控制和减碳之间寻求平衡。对再生材料的日益青睐,以及高效加工技术的进步,正在重塑基底金属市场的利润结构。同时,併购和长期供应伙伴关係正在取代传统的大规模收购,这标誌着竞争环境日趋成熟,风险分担和专有技术决定企业的主导。

全球基底金属市场趋势与洞察

电动车布线和充电基础设施对铜的需求不断增长

电动车的普及将使铜的需求呈指数级增长。每辆电池式电动车大约需要83公斤铜,远高于同类型的内燃机汽车(23公斤)。公共快速充电站所需的铜量是家用充电桩的8到10倍,形成了平行的基础设施成长引擎。必和必拓与宁德时代签署的2025年谅解备忘录,重点在于矿用车辆的电气化和电池回收,显示矿业公司致力于在推动循环价值链的同时,实现自身铜的消耗。政府对国家充电网路的强制性规定,尤其是在中国和美国,提高了透明度,使矿业公司能够更有信心地制定多年的采矿和扩张计划。

新兴经济体的基础设施奖励策略

开发中国家的大型公共工程项目通常计划较长,金属使用强度也高于成熟市场的维护週期。中国的「一带一路」倡议和印度1.4兆美元的国家基础设施计画将推动基底金属的使用,因为交通走廊和公共产业网路都需要从零开始建造。莱斯大学贝克研究所的一项研究显示,加速的都市化预计将使印度的人均基底金属消费量增加两倍。这种新增需求将导致需求持续趋于平稳,而非短期激增,从而为生产商持续扩大生产规模和技术投资提供了经济基础。

贸易政策波动与供应链中断

意外的关税、配额和製裁扰乱了采购週期,并推高了营运资金需求。製造商透过运行平行供应链来规避风险,这往往会导致库存和物流功能的重复配置。这种冗余增加了整个系统的成本,并转移了用于矿山开发的资金。地缘政治风险的加剧也会提高大型计划估价所使用的折现率,从而延缓产能扩张,使其无法满足市场需求。

细分市场分析

到了2025年,铜将占基底金属市场份额的44.12%,这充分展现了其在电力传输领域无与伦比的导电性能。锌虽然体积较小,但预计将以5.18%的复合年增长率强劲增长,这主要得益于其在耐腐蚀涂层和新兴锌空气电池化学体系中的应用。铝在汽车轻量化和封装应用领域保持稳健的成长势头,而镍则受益于对不銹钢生产和高镍电池正极材料的需求。铅的市场份额基本上持平,仅在某些医疗屏蔽和工业电池细分市场有所增长,而锡则由于无卤组装标准的不断提高,在电子焊料应用领域保持强劲势头。

锌的应用范围不断扩大,使其对建筑週期的依赖性降低,与铜价的关联性也减弱。专为可再生能源储存而设计的新型锌空气电池的推出,预示着一种不易受宏观週期波动影响的结构性需求来源。同时,对用于合成燃料生产的镍催化剂的研究,也拓展了基底金属在传统冶金用途之外的应用。

基底金属市场报告按金属类型(铜、铝、锌、镍、铅、锡)、终端用户行业(建筑、汽车及交通运输、电气及电子、消费品等)、来源(原生矿产、再生金属)和地区(亚太地区、北美、欧洲、南美、中东和非洲)进行细分。市场预测以吨为单位。

区域分析

亚太地区占据基底金属市场最大份额,且成长速度最快,这得益于中国协调一致的产业政策、印度快速的基础建设以及东南亚国协製造业的蓬勃发展。该地区既是消费国又是生产国,其垂直整合的产业链强化了需求与上游投资之间的反馈循环,加速了矿山自动化和低碳加工技术的创新。澳洲作为重要的出口国,凭藉着稳定的治理和接近性区域需求的地理优势,取得原料收入和加工利润。

在北美,美国的《国防生产法》为新的铜镍矿计划提供了优惠的融资和批准流程。艾芬豪电气公司和必和必拓公司的探勘合作就是一个很好的例子,它展现了公共奖励如何鼓励私人企业采用现代地球物理方法,并加速勘探週期。加强电网建设和推广电动车充电基础设施,正在建立一个可预测的需求基础,使其不易受短期经济波动的影响。

欧洲碳边境调节机制(CBAM)将为经认证的低碳基底金属创造一个差异化市场,有利于采用可再生能源和新型低温萃取製程的製造商。挪威和冰岛的铝提炼已经开始销售优质铝坯,而钢铁生产商正在试验氢基直接还原技术,以保持出口竞争力。

儘管智利进行了监管改革,但随着大型企业寻求发现风险较低的高等级矿床,南美洲正吸引新的投资。英美资源集团和智利国家铜业公司(Codelco)价值50亿美元的合作项目凸显了共同优化邻近资产的价值创造潜力,但基础设施不足和社区关係建设方面的挑战正在延长计划工期。

由于产业多元化和都市化,中东和非洲地区的需求正逐步增长。诸如西芒杜铁矿石计划等大型采矿项目具有规模优势,但也为投资者带来了管治和物流方面的挑战。中国工程企业与非洲各国政府的联合基础设施投资正在帮助降低某些区域的风险。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 电动汽车线路和充电基础设施对铜的需求不断增长

- 新兴经济体的基础设施奖励策略

- 汽车轻量化中铝的替代品

- 关键矿产安全战略储备

- 提高采矿、加工和回收能力

- 市场限制

- 能源密集冶炼中不断上涨的碳价格

- 贸易政策波动与供应链中断

- 环境监管压力

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按金属类型

- 铜

- 铝

- 锌

- 镍

- 带领

- 锡

- 按最终用户行业划分

- 建造

- 汽车和运输设备

- 电气和电子设备

- 消费品

- 医疗设备

- 其他终端用户产业

- 按原料

- 初级采矿

- 再生(回收)金属

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 澳洲

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 卡达

- 南非

- 奈及利亚

- 埃及

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Alcoa Corporation

- Anglo American PLC

- Aurubis AG

- BHP

- First Quantum Minerals Ltd.

- Freeport-McMoRan

- Glencore PLC

- Grupo Mexico

- Jiangxi Copper Corporation

- Jubilee Metals Group PLC

- Lundin Mining Corporation

- Norilsk Nickel

- Norsk Hydro ASA

- Rio Tinto

- Sumitomo Metal Mining Co., Ltd.

- Vale

- Vedanta Resources Limited

- Zijin Mining Group Co. Ltd

第七章 市场机会与未来展望

Base Metals market size in 2026 is estimated at 141.85 million tons, growing from 2025 value of 137.05 million tons with 2031 projections showing 168.45 million tons, growing at 3.5% CAGR over 2026-2031.

Continued electrification, widespread infrastructure renewal, and the shift from purely volume to value-focused production underpin this steady trajectory. Mining companies now emphasize strategic positioning, supply security, and technological efficiency instead of aggressive green-field capacity, while downstream manufacturers balance cost control with carbon-reduction imperatives as policy pressure intensifies. A growing preference for recycled feedstock, coupled with advances in high-efficiency processing, further reconfigures profit pools across the base metals market. In parallel, mergers and long-term supply partnerships are supplanting traditional large-scale acquisitions, signalling a maturing competitive environment where risk-sharing and proprietary technology determine leadership.

Global Base Metals Market Trends and Insights

Expanding Copper Demand for EV Wiring and Charging Infrastructure

Electric vehicle adoption multiplies copper intensity: each battery-electric car contains about 83 kg of copper, far exceeding the 23 kg in internal-combustion models. Public fast-charging stations require eight to ten times the copper used in home chargers, creating a parallel infrastructure growth engine. BHP's 2025 memorandum with CATL focuses on electrifying mine fleets and recycling batteries, illustrating how miners increasingly consume their own copper output while promoting closed-loop value chains. Government mandates for national charging networks, especially in China and the United States, provide transparency that allows miners to plan multi-year extraction and expansion schedules with greater confidence.

Infrastructure Stimulus in Emerging Economies

Major public works programmes in developing nations run on longer project horizons and higher metal intensities than maintenance cycles in mature markets. China's Belt and Road Initiative and India's USD 1.4 trillion National Infrastructure Pipeline elevate base-metal use as whole transport corridors and utilities networks are built from scratch. Research from Rice University's Baker Institute projects a tripling of per-capita base-metal consumption in India as urbanisation accelerates. Such green-field demand creates enduring plateaus rather than short spikes, giving producers the economic justification for sustained output growth and technological investment.

Trade Policy Volatility and Supply-Chain Disruptions

Sudden tariffs, quotas, and sanctions disrupt procurement cycles and inflate working capital needs. Manufacturers hedge by operating parallel supply chains, often duplicating inventory and logistics functions. Such redundancy raises total system costs and diverts cash away from mine development. Heightened geopolitical risk also increases the discount rates used to value large projects, thereby delaying capacity additions that might otherwise keep pace with demand.

Other drivers and restraints analyzed in the detailed report include:

- Aluminium Substitution in Automotive Lightweighting

- Improved Mining, Processing and Recycling Capabilities

- Environmental and Regulatory Pressures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Copper controlled the largest slice of the base metals market size at 44.12% in 2025, a testament to its unmatched conductivity in electricity transmission. Zinc, though smaller, is on course for a brisk 5.18% CAGR, buoyed by its roles in corrosion-resistant coatings and emerging zinc-air battery chemistries. Aluminium retains a solid growth runway from vehicle lightweighting and packaging, while nickel benefits from stainless-steel output and high-nickel battery cathodes. Lead remains range-bound, except in select medical shielding and industrial battery niches; tin stays resilient in electronics solder due to stricter halogen-free assembly standards.

The broadening application set for zinc reduces the segment's dependence on construction cycles and lowers correlation with copper pricing. Breakthrough zinc-air installations designed for renewable energy storage signal a structural demand source that is less sensitive to macro cycles. Simultaneously, nickel catalyst research for synthetic fuel production expands the scope of base-metal applications beyond traditional metallurgical uses.

The Base Metals Market Report is Segmented by Metal Type (Copper, Aluminium, Zinc, Nickel, Lead, Tin), End-User Industry (Construction, Automotive and Transportation, Electrical and Electronics, Consumer Products, and More), Source (Primary Mining, Secondary Metals), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Volume (tons).

Geography Analysis

Asia Pacific holds the largest share of the base metals market and delivers the fastest expansion, supported by coordinated industrial policy in China, India's infrastructure surge, and ASEAN manufacturing gains. The region's combined consumer-producer role underpins vertically integrated chains that tighten feedback loops between demand and upstream investment, accelerating innovation in mine automation and low-carbon processing. Australia, already a top exporter, benefits from stable governance and proximity to regional demand, capturing processing margins in addition to raw-material revenue.

North America, leveraging the US Defense Production Act, secures preferential financing and permitting for new copper and nickel projects. Ivanhoe Electric's joint exploration with BHP demonstrates how public incentives catalyse private deployment of modern geophysical methods that can accelerate discovery cycles. Grid-hardening and EV-charging roll-outs form a predictable demand baseline less sensitive to short-term economic swings.

Europe's CBAM creates a differentiated market for certified low-carbon base metals, rewarding producers that deploy renewable power or novel low-temperature extraction routes. Aluminium smelters in Norway and Iceland already sell premium billets, and steelmakers trial hydrogen-based direct-reduction technologies to maintain export competitiveness.

South America, despite Chile's regulatory resets, attracts fresh investment as majors pursue high-grade deposits with lower discovery risk. Anglo American's USD 5 billion partnership with Codelco underscores the value-creation potential in joint optimisation of adjacent assets. Infrastructure deficits and community-relations hurdles, however, lengthen project timelines.

The Middle East and Africa register incremental demand from industrial diversification and urbanisation. Large-scale mining opportunities, such as the Simandou iron ore project, demonstrate the scale advantage but also expose investors to governance and logistics challenges. Collaborative infrastructure investments between Chinese engineering firms and African governments help de-risk select corridors.

- Alcoa Corporation

- Anglo American PLC

- Aurubis AG

- BHP

- First Quantum Minerals Ltd.

- Freeport-McMoRan

- Glencore PLC

- Grupo Mexico

- Jiangxi Copper Corporation

- Jubilee Metals Group PLC

- Lundin Mining Corporation

- Norilsk Nickel

- Norsk Hydro ASA

- Rio Tinto

- Sumitomo Metal Mining Co., Ltd.

- Vale

- Vedanta Resources Limited

- Zijin Mining Group Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding copper demand for EV wiring and charging infrastructure

- 4.2.2 Infrastructure stimulus in emerging economies

- 4.2.3 Aluminium substitution in automotive lightweighting

- 4.2.4 Strategic stockpiling for critical-mineral security

- 4.2.5 Improved mining, processing, and recycling capabilities

- 4.3 Market Restraints

- 4.3.1 Rising carbon-pricing on energy-intensive smelting

- 4.3.2 Trade policy volatility and supply chain distrubtions

- 4.3.3 Environmental and Regulatory Pressures

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Metal Type

- 5.1.1 Copper

- 5.1.2 Aluminium

- 5.1.3 Zinc

- 5.1.4 Nickel

- 5.1.5 Lead

- 5.1.6 Tin

- 5.2 By End-user Industry

- 5.2.1 Construction

- 5.2.2 Automotive and Transportation

- 5.2.3 Electrical and Electronics

- 5.2.4 Consumer Products

- 5.2.5 Medical Devices

- 5.2.6 Other End-user Industries

- 5.3 By Source

- 5.3.1 Primary Mining

- 5.3.2 Secondary (Recycled) Metals

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Australia

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordics

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alcoa Corporation

- 6.4.2 Anglo American PLC

- 6.4.3 Aurubis AG

- 6.4.4 BHP

- 6.4.5 First Quantum Minerals Ltd.

- 6.4.6 Freeport-McMoRan

- 6.4.7 Glencore PLC

- 6.4.8 Grupo Mexico

- 6.4.9 Jiangxi Copper Corporation

- 6.4.10 Jubilee Metals Group PLC

- 6.4.11 Lundin Mining Corporation

- 6.4.12 Norilsk Nickel

- 6.4.13 Norsk Hydro ASA

- 6.4.14 Rio Tinto

- 6.4.15 Sumitomo Metal Mining Co., Ltd.

- 6.4.16 Vale

- 6.4.17 Vedanta Resources Limited

- 6.4.18 Zijin Mining Group Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increased Demand for Clean Energy Technologies

基底金属矿业市场:依金属类型、来源、产品形态、萃取方法和最终用途产业划分-2026-2032年全球预测基底金属市场:2026-2032年全球预测,依来源、製造流程、形状、金属类型、应用和最终用途产业划分高纯度氯化铟市场依产品类型、纯度等级、最终用途及通路划分-2026-2032年全球预测高纯铍金属市场按形态、纯度等级、製造流程、应用和最终用途产业划分,全球预测(2026-2032年)

基底金属矿业市场:依金属类型、来源、产品形态、萃取方法和最终用途产业划分-2026-2032年全球预测基底金属市场:2026-2032年全球预测,依来源、製造流程、形状、金属类型、应用和最终用途产业划分高纯度氯化铟市场依产品类型、纯度等级、最终用途及通路划分-2026-2032年全球预测高纯铍金属市场按形态、纯度等级、製造流程、应用和最终用途产业划分,全球预测(2026-2032年) 高纯度金属市场预测至2032年:按金属类型、形态、生产方法、分销管道、最终用户和地区分類的全球分析

高纯度金属市场预测至2032年:按金属类型、形态、生产方法、分销管道、最终用户和地区分類的全球分析 高纯度氧化钐:全球市场展望、详细分析及至2031年预测

高纯度氧化钐:全球市场展望、详细分析及至2031年预测 基底金属矿业市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2025-2033 年)

基底金属矿业市场规模、份额和趋势分析报告:按产品、最终用途、地区和细分市场预测(2025-2033 年)