|

市场调查报告书

商品编码

1937344

氯化聚乙烯:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Chlorinated Polyethylene - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

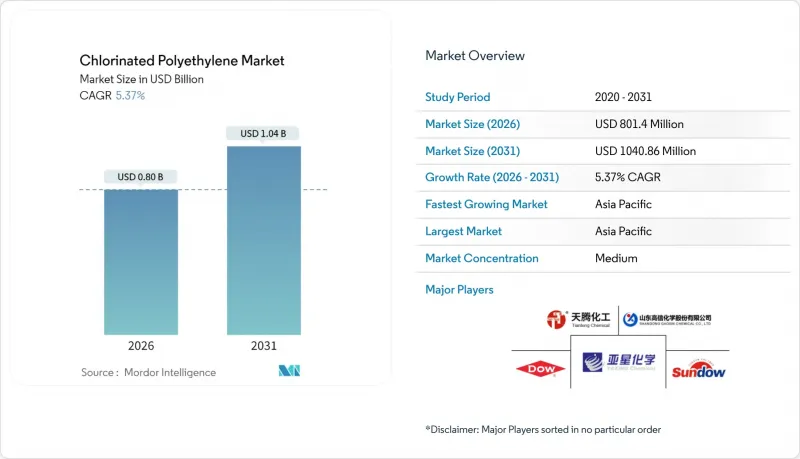

预计到 2026 年,氯化聚乙烯市场规模将达到 8.014 亿美元,高于 2025 年的 7.6056 亿美元。

预计到 2031 年将达到 10.4086 亿美元,2026 年至 2031 年的复合年增长率为 5.37%。

这种持续增长反映了该聚合物作为热可塑性橡胶的作用日益增强,弥合了传统橡胶和塑胶之间的差距,并越来越多地应用于电缆护套、衝击改质剂和软管等领域。强劲的需求主要受三个因素驱动:电动车的加速普及、日益严格的建筑规范鼓励使用耐用型PVC共混物,以及东亚氯碱一体化产业丛集所提供的价格竞争力。能够提供符合无卤防火安全标准、高介电强度和循环经济倡议的配方的供应商,正在赢得汽车製造商和建筑承包商的青睐。山东省产能的快速扩张和内部氯气采购持续对全球价格构成下行压力,但其生产规模的扩大也降低了长期供不应求的风险。同时,欧洲对氯化塑胶的公共采购限制和原材料价格的波动,为成本转嫁带来了挑战,只有技术灵活的生产商才能应对。

全球氯化聚乙烯市场趋势及洞察

绿建筑应用领域对PVC的需求激增

随着建筑师转向使用再生PVC门窗和墙板,永续建筑标准推动了氯化聚乙烯(CPE)消费量的成长。这些材料即使在低温下也需要优异的抗衝击性能。氯化聚乙烯135A优化了高回收配方中的熔融性能,使加工商能够在保持韧性的同时减少对其他加工助剂的需求。寻求LEED和BREEAM认证积分的建筑商现在指定使用CPE改质型材,因为实验数据证实,与未改质PVC相比,CPE改质型材在更宽的温度范围内具有稳定的延展性。添加生物基增塑剂的聚合物共混物进一步增强了这一优势,减少了原生氯的总体用量——这是绿色政府采购竞标中的关键论点。因此,在再生PVC流中能够展现稳定Izod衝击值的氯化聚乙烯等级在大都会圈维修专案中获得了销售优势。

电动车的快速普及推动了对电缆护套材料的需求。

电动车平台依赖高压线束、充电线和电池冷却管路,这些部件必须能够承受液体飞溅、热循环和电磁干扰。氯化聚乙烯具有过氧化物硫化三元乙丙橡胶 (EPDM) 所缺乏的关键介电强度和低温柔柔软性,这使得汽车製造商在从 400V 架构过渡到 800V 架构时能够标准化护套材料。设计工程师特别重视其对磷酸酯类冷却剂的耐受性,这种失效模式限制了许多热塑性硫化橡胶的应用。随着软管直径因电池加热迴路的全面普及而增大,氯化聚乙烯弹性体在低温下保持弯曲半径的优势变得更加显着。目前,UL 94 V-0 认证、无卤素、预着色氯化聚乙烯 (CPE) 化合物的供应商表示,他们已收到来自原始设备製造商 (OEM) 的多年采购承诺,并明确了报废回收目标。

氯气和乙烯价格波动

受苛性钠供需动态以及氧化铝精炼厂需求变化的影响,氯气现货价格在12个月内波动超过60%,给在公开市场上采购氯气的非一体化氯乙烯(CPE)生产商带来了压力。同时,美国墨西哥湾沿岸蒸汽裂解装置的停产扩大了乙烯合约溢价,并提高了下游氯化聚乙烯原料的成本。高能耗的膜电解进一步加剧了电价飙升,将变动成本推入了「下游需求中断转嫁区」。虽然一体化生产商更有能力抵御价格波动,但需要透过原物料库存来缓衝价格波动,这加剧了其营运资金紧张的局面。混炼商透过调整配方降低氯含量来抵消部分影响,但这种策略限制了最高热变形温度,并缩小了应用范围。

细分市场分析

2025年,CPE 135A的销售量将保持在52.90%,这得益于其均衡的分子量分布,从而确保了硬质PVC在墙板和型材挤出生产线中具有更高的韧性。 135A级产品相对较低的慕尼粘度降低了混炼成本,因此深受高产能建筑型材挤出机的青睐。同时,CPE 135B预计将以5.46%的复合年增长率成长,因为软管、管材和耐化学腐蚀垫片的混炼商愿意为其卓越的耐油耐酸性能支付溢价。需求加速成长主要集中在氢气软管领域,由于压力评级的提高,该领域对渗透性能的要求也越来越高。具有客製化氯含量的特种等级产品占总价值的18%,这得益于太阳能电池板背板共挤出这一细分市场,该市场要求产品在145°C下经两小时的烘箱老化稳定性。

本产品领域的创新主要围绕在以135B为基础的无卤阻燃型产品展开,这些产品兼具V-0阻燃等级和300%的断裂伸长率。製造商采用反应挤出技术将磷基团直接锚定到聚合物链上,从而减少泛白和表麵粉化。虽然产量仍处于早期阶段,但其在铁路垫片应用中的早期应用已证明了商业性可行性。一些过氧化氢交联的氯化聚乙烯(CPE)虽然技术上不属于标准编号系统,但由于它们无需更换模具即可替代过氧化物硫化的三元乙丙橡胶(EPDM),因此具有很强的议价能力。这些趋势表明,未来氯化聚乙烯市场的产品组合变化不仅取决于价格,还取决于性能差异化。

氯化聚乙烯市场报告按产品(CPE 135A、CPE 135B、其他产品)、应用(衝击改质剂、电线电缆涂层、软管和管材、黏合剂、其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区、中东和非洲地区)进行细分。市场预测以以金额为准和销售两种形式提供。

区域分析

到2025年,亚太地区将占总收入的72.10%,巩固其主导地位,这主要得益于中国一体化的氯碱联合企业和不断扩张的下游PVC产业。到2031年,亚太地区5.70%的复合年增长率凸显了东南亚、印度和韩国的成长势头,这些地区正在建设电动车电池超级工厂,建设支出持续成长。当地自有氯气供应降低了现金成本,并吸引西方混料生产商签订加工合约以规避运费风险。日本特种电缆製造商也依赖区域供应,但为了满足其独特的防火安全标准,他们需要从欧洲进口高价值的母粒,这反映了区域内CPE性能特征的贸易往来。

在美国,一波电动车补贴浪潮刺激了高压电缆的需求。然而,由于北美只有两家工厂生产这种聚合物,转换器公司不得不从太平洋沿岸进口以补充需求。墨西哥的乘用车组装和家电工厂正在推动当地需求,而美墨加协定(USMCA)的条款正在促进线束组件的采购,鼓励洲内采购。

在欧洲,由于禁止公共采购氯化塑料,扩张速度放缓。然而,永续性的压力正在推动CPE回收的研究与发展。目前,一家德国型材挤出製造商正在测试一种基于溶剂的剥离循环工艺,以从窗框边角料中回收含CPE的组件。在中东和非洲,由于卡达和沙乌地阿拉伯的大型企划需要能够承受紫外线和沙粒磨损的耐用电线涂层,预计需求将温和成长。巴西是南美洲的关键市场,当地住宅建设的復苏正在推动对CPE抗衝击改质PVC管材的需求。然而,汇率波动限制了需求的快速成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 绿建筑应用领域对PVC的需求激增

- 电动车的快速电气化正在推动对电缆护套材料的需求。

- 向无卤阻燃CPE混合材料过渡

- 透过扩大中国供给面来增强价格竞争力

- 用于氢气加註基础设施的耐油软管

- 市场限制

- 氯气和乙烯价格波动

- 欧盟公共采购中禁止使用氯化塑料

- 提高TPV作为替代弹性体的性能

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 副产品

- CPE 135A

- CPE 135B

- 其他产品

- 透过使用

- 衝击改质剂

- 电线电缆护套材料

- 软管和管件

- 黏合剂

- 其他用途

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Aurora Material Solutions

- Bontecn Group China Co. Ltd

- Dow

- Dycon Chemicals

- Epigral Limited

- Hangzhou Keli Chemical Co. Ltd

- Jiangsu Tianteng Chemical Industry Co. Ltd

- Resonac Holdings Corporation

- Shandong Gaoxin Chemical Co. Ltd

- Shandong Ketian Chemical Co. Ltd

- Shandong Novista Chemical Ltd(Novista Group)

- Shandong Rike Chemical Co.,Ltd

- Shandong Xiangsheng New Materials Technology Co. Ltd

- Shandong Xuye New Materials Co. Ltd

- Sundow Polymers Co. Ltd

- Weifang Yaxing Chemical Co. Ltd

第七章 市场机会与未来展望

Chlorinated Polyethylene Market size in 2026 is estimated at USD 801.4 million, growing from 2025 value of USD 760.56 million with 2031 projections showing USD 1040.86 million, growing at 5.37% CAGR over 2026-2031.

This sustained expansion mirrors the polymer's expanding role as a thermoplastic elastomer that bridges traditional rubber and plastic functions, finding growing use across cable jacketing, impact modifiers, and flexible hose products. Demand resilience stems from three visible forces: accelerating electric-vehicle electrification, stricter building codes favoring durable PVC blends, and the competitive pricing unlocked by integrated chlor-alkali clusters in East Asia. Suppliers that align formulations with halogen-free fire-safety rules, elevated dielectric thresholds, and circular-economy ambitions are capturing specification wins from automakers and construction contractors. Rapid capacity additions in Shandong, coupled with captive chlorine sourcing, continue to pressure global price floors, yet that same manufacturing scale reduces the risk of chronic shortages. Conversely, public-procurement restrictions on chlorinated plastics in Europe and raw-material price gyrations raise cost-pass-through challenges that only technologically agile producers can navigate.

Global Chlorinated Polyethylene Market Trends and Insights

Surging PVC Demand in Green Building Applications

Sustainable-building rules spur incremental chlorinated polyethylene consumption as architects shift toward recycled PVC doors, windows, and siding that still need robust impact performance at low temperatures. Chlorinated polyethylene 135A optimizes fusion in high-recycled-content formulations, letting converters cut separate processing aids without sacrificing toughness. Builders seeking LEED or BREEAM points now specify CPE-modified profiles because lab data confirm stable ductility across a wider temperature band than unmodified PVC. Polymer blends that integrate bio-based plasticizers push that advantage further by reducing overall virgin chlorine intensity, a key talking point in green-public-procurement bids. Consequently, chlorinated polyethylene grades that can demonstrate consistent Izod impact values in secondary PVC streams are winning volume awards in metropolitan retrofits.

Rapid EV Electrification Driving Cable Jacketing Demand

Electric-vehicle platforms rely on high-voltage harnesses, charging cords, and battery-coolant lines that must withstand fluid splash, thermal cycling, and electromagnetic interference. Chlorinated polyethylene delivers the critical dielectric strength and low-temperature flexibility missing in peroxide-cured EPDM, enabling automakers to standardize jacketing compounds even as they move from 400 V to 800 V architectures. Design engineers particularly value the polymer's resistance to phosphate-ester coolant exposure, a failure mode that limits many thermoplastic vulcanizates. Shifts toward full-battery heating loops enlarge hose diameters, magnifying the benefit of low-temperature bend radius retention inherent to chlorinated polyethylene elastomers. Suppliers offering pre-colored halogen-free CPE compounds with UL 94 V-0 ratings now report multi-year sourcing nominations from original-equipment manufacturers unabashedly targeting end-of-life recyclability targets.

Volatile Chlorine and Ethylene Costs

Spot prices for chlorine swung by more than 60% within 12 months as caustic-soda dynamics shifted with alumina-refining demand, squeezing non-integrated CPE producers that purchase chlorine on the open market. Meanwhile, ethylene contract premiums widened on steam-cracker outages in the U.S. Gulf Coast, raising polyethylene feedstock costs for downstream chlorination. Energy-intensive membrane-cell electrolysis further magnifies electricity price spikes, pushing variable costs into a territory where passing them downstream risks demand destruction. Integrated producers withstand turbulence better, yet even they face higher working-capital locks because raw-material inventories must buffer price whiplash. Compounders offset part of the impact by reformulating with lower chlorination levels, but that strategy caps achievable heat-deflection temperatures and thus limits application windows.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Halogen-Free Flame-Retardant CPE Hybrids

- Chinese Supply-Side Expansion Enhancing Price Competitiveness

- EU Public-Procurement Bans on Chlorinated Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CPE 135A retained 52.90% of 2025 volumes because its balanced molecular-weight distribution reliably boosts rigid PVC toughness in siding and profile extrusion lines. Grade 135A's relatively low Mooney viscosity keeps compounding costs contained, which appeals to high-throughput construction profile extruders. Conversely, CPE 135B demonstrates a 5.46% CAGR projection as formulators in hose, tubing, and chemical-tolerant gaskets pay premiums for its superior oil and acid resistance. Demand acceleration concentrates in hydrogen-service hoses where permeation limits tighten with rising pressure ratings. Specialty grades with custom chlorine content represent 18% of value, benefitting from co-extrusion niches in solar-panel back-sheets that need two-hour oven-aging stability at 145 °C.

Innovation inside the product landscape orbits around halogen-free flame-retardant variants built on the 135B backbone that marry V-0 flame rating with 300% elongation at break. Producers deploy reactive extrusion to lock phosphorus moieties directly into the polymer chain, reducing blooming and surface chalking. Although volumes remain nascent, early adopters in rail-transit gasket applications validate commercial readiness. Some high-dicumyl-peroxide cross-linkable CPEs, while technically outside standard numbering, command strong bargaining power because they replace peroxide-cured EPDM without tooling changes. These dynamics underline how performance differentiation rather than price alone will define future product-mix shifts inside the chlorinated polyethylene market.

The Chlorinated Polyethylene Market Report is Segmented by Product (CPE 135A, CPE 135B, and Other Products), Application (Impact Modifiers, Wire and Cable Jacketing, Hose and Tubing, Adhesives, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value and Volume.

Geography Analysis

Asia-Pacific generated 72.10% of 2025 revenue, reaffirming the region's leadership anchored in China's integrated chlor-alkali complexes and its expansive downstream PVC industries. A 5.70% CAGR to 2031 underscores momentum across Southeast Asia, India, and South Korea, where EV battery gigafactories sprout and construction spending persists. Local captive chlorine supplies compress cash-cost curves, drawing in Western compounders that set up tolling deals to hedge against freight volatility. Japan's specialty cable producers also lean on regional supply, though they import premium halogen-free masterbatches from Europe for distinct fire-safety norms, reflecting an intra-regional trade of performance flavors of CPE.

The United States benefits from an EV subsidy wave that accelerates high-voltage cable demand. However, only two North American plants produce the polymer, forcing converters to backfill via Pacific-coast imports. Mexico's passenger-vehicle assembly lines and appliance factories enhance regional pull, aided by USMCA provisions that favor continental sourcing of wiring content.

Europe faces slower expansion given public procurement bans on chlorinated plastics. Sustainability pressures nonetheless trigger research and development on CPE recycling, with German profile extruders trialing solvent-based delamination loops to harvest CPE-rich fractions from window offcuts. Middle-East and Africa hold modest but rising prospects as megaprojects in Qatar and Saudi Arabia demand durable wire-coating materials that cope with UV and sand abrasion. Brazil anchors South America, where residential-building rebounds lift demand for CPE impact-modified PVC pipes, yet currency volatility tempers aggressive uptake.

- Aurora Material Solutions

- Bontecn Group China Co. Ltd

- Dow

- Dycon Chemicals

- Epigral Limited

- Hangzhou Keli Chemical Co. Ltd

- Jiangsu Tianteng Chemical Industry Co. Ltd

- Resonac Holdings Corporation

- Shandong Gaoxin Chemical Co. Ltd

- Shandong Ketian Chemical Co. Ltd

- Shandong Novista Chemical Ltd (Novista Group)

- Shandong Rike Chemical Co.,Ltd

- Shandong Xiangsheng New Materials Technology Co. Ltd

- Shandong Xuye New Materials Co. Ltd

- Sundow Polymers Co. Ltd

- Weifang Yaxing Chemical Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PVC Demand in Green Building Applications

- 4.2.2 Rapid EV Electrification Driving Cable Jacketing Demand

- 4.2.3 Shift Toward Halogen-Free Flame-Retardant CPE Hybrids

- 4.2.4 Chinese Supply-Side Expansion Enhancing Price Competitiveness

- 4.2.5 Oil-Resistant Hoses for Hydrogen Refuelling Infrastructure

- 4.3 Market Restraints

- 4.3.1 Volatile Chlorine and Ethylene Costs

- 4.3.2 EU Public-Procurement Bans on Chlorinated Plastics

- 4.3.3 TPV Performance Advances as Substitute Elastomers

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 CPE 135A

- 5.1.2 CPE 135B

- 5.1.3 Other Products

- 5.2 By Application

- 5.2.1 Impact Modifiers

- 5.2.2 Wire and Cable Jacketing

- 5.2.3 Hose and Tubing

- 5.2.4 Adhesives

- 5.2.5 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aurora Material Solutions

- 6.4.2 Bontecn Group China Co. Ltd

- 6.4.3 Dow

- 6.4.4 Dycon Chemicals

- 6.4.5 Epigral Limited

- 6.4.6 Hangzhou Keli Chemical Co. Ltd

- 6.4.7 Jiangsu Tianteng Chemical Industry Co. Ltd

- 6.4.8 Resonac Holdings Corporation

- 6.4.9 Shandong Gaoxin Chemical Co. Ltd

- 6.4.10 Shandong Ketian Chemical Co. Ltd

- 6.4.11 Shandong Novista Chemical Ltd (Novista Group)

- 6.4.12 Shandong Rike Chemical Co.,Ltd

- 6.4.13 Shandong Xiangsheng New Materials Technology Co. Ltd

- 6.4.14 Shandong Xuye New Materials Co. Ltd

- 6.4.15 Sundow Polymers Co. Ltd

- 6.4.16 Weifang Yaxing Chemical Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Research and Development on Advanced CPE Grades

氯化聚乙烯市场:依形态、性能等级、应用、终端用户产业及通路划分-2026-2032年全球预测

氯化聚乙烯市场:依形态、性能等级、应用、终端用户产业及通路划分-2026-2032年全球预测 2025-2033年氯化聚乙烯市场报告(依等级类型、应用、最终用途产业及地区)

2025-2033年氯化聚乙烯市场报告(依等级类型、应用、最终用途产业及地区) 氯化聚乙烯 (CPE) 市场、全球需求分析、地区、应用及 2034 年预测

氯化聚乙烯 (CPE) 市场、全球需求分析、地区、应用及 2034 年预测 氯化聚乙烯市场规模、份额和成长分析(按产品、氯含量、应用、最终用途行业和地区)- 2025-2032 年行业预测

氯化聚乙烯市场规模、份额和成长分析(按产品、氯含量、应用、最终用途行业和地区)- 2025-2032 年行业预测 2030 年氯化聚乙烯市场预测:按等级、应用和地区进行的全球分析氯化聚乙烯市场、规模、占有率、趋势、行业分析报告:依产品、应用和地区 - 市场预测(2025-2034)氯化聚乙烯的全球市场(2018年~2034年)

2030 年氯化聚乙烯市场预测:按等级、应用和地区进行的全球分析氯化聚乙烯市场、规模、占有率、趋势、行业分析报告:依产品、应用和地区 - 市场预测(2025-2034)氯化聚乙烯的全球市场(2018年~2034年) 2024 年至 2031 年氯化聚乙烯市场(按等级、应用和地区划分)

2024 年至 2031 年氯化聚乙烯市场(按等级、应用和地区划分)