|

市场调查报告书

商品编码

1937346

美国陶瓷砖:市场占有率分析、产业趋势与统计、成长预测(2026-2031)US Ceramic Tiles - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

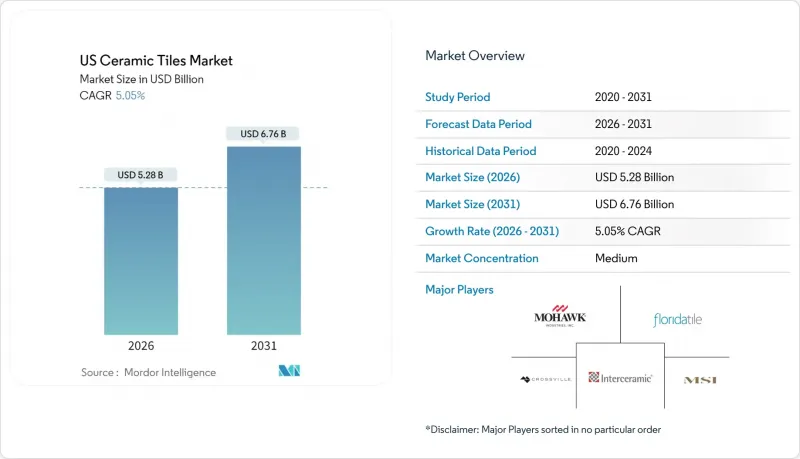

美国磁砖市场预计将从 2025 年的 50.3 亿美元成长到 2026 年的 52.8 亿美元,到 2031 年达到 67.6 亿美元,2026 年至 2031 年的复合年增长率为 5.05%。

住宅翻新需求的成长、阳光地带稳定的住宅开工量以及低VOC建筑材料的监管激励措施,都支撑着这项扩张。随着反倾销税减少低成本进口产品,以及天然气价格下跌降低烧製成本并支持国内生产竞争力,国内製造商的市场份额正在扩大。数位印刷技术、大尺寸瓷砖和地暖设计的普及,拓展了应用范围并推高了平均售价。同时,熟练安装人员的人手不足以及来自硬芯LVT(强化复合乙烯基瓷砖)日益激烈的竞争,限制了绝对销量的成长。

美国陶瓷砖市场趋势与分析

阳光地带的住宅开工量依然强劲。

儘管其他地区的建筑需求放缓,但阳光地带的建筑需求仍然强劲,预计佛罗里达州2024年的建筑材料销售额将达到9.976亿美元。有利的气候、人口涌入以及有利于商业发展的政策,使得建筑许可数量保持相对稳定,从而为瓷砖製造商提供了可预测的订单。製造商正在优化围绕这些高需求地区的物流网络,以降低运输成本并缩短交货时间。炎热气候下的节能标准认可了陶瓷的蓄热性能,并鼓励建筑师指定使用陶瓷材料。瓷砖的防潮性和耐用性,以及持续的气候调适投资,进一步提升了其吸引力。

扩大大块瓷砖的使用

建筑设计对无缝表面的偏好推动了6毫米和12毫米瓷砖面板的普及,这种面板减少了接缝,缩短了安装时间。路易斯维尔瓷砖公司(Louisville Tile)于2025年推出的6毫米瓷砖面板就是一个很好的例子,它展示了预切割瓷砖如何解决安装人员短缺的问题,同时又能实现高端定价。道尔托伊尔公司(Daltoil)在2025年KBIS展会上推出的超大尺寸瓷砖“ONE Quartz”,将大理石的美感延伸至人流量大的区域,且无需重复图案。数位喷墨技术的进步使得在大尺寸表面上复製逼真的条纹成为可能,这使其区别于传统的方形瓷砖。资本密集的瓷砖窑炉和抛光生产线构成了准入门槛,有利于拥有规模优势的现有企业。这种规格也符合医疗保健、饭店和豪华住宅计划的卫浴趋势。

天然气价格波动推高了炉子的成本。

能源成本约占瓷器生产预算的30%,其中90%由天然气供应。美国能源资讯署(EIA)预测,天然气价格在2024年触底至每百万英热单位2.21美元后,到2026年将上涨超过每百万英热单位4美元,这将给陶瓷製造商带来压力。大型企业集团可以透过多年期合约和汽电共生对冲来降低风险,而中小型独立製造商则面临利润率压力和价格转嫁。能源价格波动也会重新平衡价格竞争力,因为进口的燃煤窑炉会影响价格,让定价竞争更加复杂。投资电窑炉可以提供长期稳定性,但需要大量资金和电网升级,而这些都需要时间才能见效。

细分市场分析

截至2025年,陶瓷瓷砖在美国陶瓷砖市场占有55.12%的份额,这主要得益于其低吸水率及适用于室内外无缝衔接的特性。先进的喷墨列印技术实现了深纹理、混凝土外观和纺织纹理的呈现,突破了传统设计的限制。製造商正在拓展瓷砖产品线,推出2公分厚的铺路砖和6毫米厚的薄板,应用范围从透气外墙延伸至家具檯面。在成本优先于性能的场合,釉药瓷砖依然具有竞争力,为注重性价比的零售产品组合提供了支持。无釉陶土砖适用于摩擦係数超过0.8的商用厨房。马赛克和手工砖则占据了客製化的小众市场,其价格通常是平均每平方英尺价格的数倍。回收玻璃粉和蕴藏量回收技术的应用,降低了碳排放,提升了整个产业的永续性永续性。这些创新措施充分展现了美国陶瓷砖市场如何同时满足主流和特殊需求。

投资欧洲式Continua Plus压机,可生产无限尺寸的瓷砖,包括1.6米 x 3.2米的板材,只需三道工序即可切割成檯面坯料。这些生产线提高了产量和产量比率,同时减少了人工成本,即使在通用瓷砖价格面临下行压力的情况下,也能保持稳定的利润率。製造商正利用专有釉药实现抗菌、防滑或太阳反射表面,从而为进入医疗、交通和覆材等领域创造了机会。扩大国内产能还能缩短供应链,确保及时补货,进而保护美国瓷砖市场免受未来关税衝击的影响。持续的技术创新使瓷质砖成为成长引擎,同时也使其在与其他地板材料竞争中脱颖而出。

到2025年,地板材料应用将占美国瓷砖市场的68.05%,主要应用于浴室、厨房和人流量大的商业走廊。承重性能、抗污性和终身耐磨保证符合设施管理人员的优先考虑因素。承重限制的放宽推动了多层住宅计划中大型瓷砖面板的采用,从而减轻了业主共同的维护负担。同时,墙面覆层的复合年增长率高达5.36%,增长最为迅猛,主要得益于垂直方向统一石材纹理设计的流行趋势,以营造统一的视觉效果。零售商店采用瓷砖装饰墙来传达高端品牌形象,同时满足消防安全标准。医疗机构的走廊采用瓷砖檐底,以承受强效化学清洁剂的侵蚀。屋顶虽然仍是小众市场,但在寻求隔热和防水的豪华地中海风格住宅中,需求不断增长。这些趋势表明,美国瓷砖市场能够灵活满足各种表面的美观、功能和法规需求。

高黏结力、低VOC黏合剂的进步缩短了固化时间,从而加快了墙面安装速度,并加快了维修。机械式卡扣系统使得维修中能够安装20毫米厚的透气墙板,显着降低了建筑围护结构的能耗。製造商提供包含装饰条、窗台和圆角等多种选择的样品库,方便客户进行全空间规格製定。行销强调,整个楼层使用统一的材料可以减少视觉上的杂乱感,并最大限度地减少未来翻新时可能出现的差异。随着消费者将墙面视为自我表达的画布,金属质感、织物质感和几何浮雕瓷砖的市场份额正在不断增长。这些趋势共同推动了美国整体瓷砖市场墙面瓷砖细分市场的成长,而地砖的销售量则保持稳定。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 阳光地带的住宅开工量依然强劲。

- 大尺寸磁砖板材的应用日益广泛

- 节能型辐射地板暖气的需求趋势

- 新冠疫情后商业设施维修热潮

- 室内空气品质法规建议使用低挥发性有机化合物(VOC)瓷砖。

- 联邦紧急事务管理局 (FEMA) 为防洪建材提供的韧性津贴

- 市场限制

- 天然气价格波动推高了窑炉烧製成本。

- 合格的瓷砖安装工人手不足

- 与LVT/SPC硬质芯材地板的竞争格局

- 某些釉药添加剂有 PFAS 诉讼风险

- 产业价值链分析

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

- 洞察市场最新趋势与创新

- 深入了解近期产业发展动态(新产品发布、策略性倡议、投资、合作、合资、扩张、併购等)

第五章 市场规模及成长预测(金额:美元)

- 依产品类型

- 陶瓷瓷砖

- 釉药磁砖

- 无釉陶瓷砖

- 马赛克瓷砖

- 其他(装饰瓷砖、图案瓷砖、手工瓷砖)

- 透过使用

- 地板材料

- 墙

- 屋顶材料

- 最终用户

- 住宅

- 商业的

- 饭店业(饭店、度假村)

- 零售店

- 办公室和公共设施

- 卫生保健

- 教育设施

- 交通枢纽(机场、捷运、客运站)

- 其他商业用户

- 依建筑类型

- 新建工程

- 维修和更换

- 透过分销管道

- 磁砖和石材专卖店

- 居家装潢和DIY专卖店

- 线上零售

- 直接向承包商销售

- 按地区

- 东北

- 中西部

- 东南

- 西南

- 西方

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Mohawk Industries(Dal-Tile, Marazzi, American Olean)

- Florida Tile

- Crossville Inc.

- Interceramic USA

- MSI Surfaces

- Emser Tile

- Porcelanosa USA

- Roca Tile USA

- Bedrosians Tile & Stone

- Anatolia Tile+Stone

- Walker Zanger

- Artistic Tile

- American Wonder Porcelain

- Mariner USA

- Dal-Tile Mexico Imports

- StonePeak Ceramics

- LAUFEN Bathrooms(US)

- Florim USA

- IWT Florida(Tesoro)

- Vitromex USA

第七章 市场机会与未来展望

The United States ceramic tiles market is expected to grow from USD 5.03 billion in 2025 to USD 5.28 billion in 2026 and is forecast to reach USD 6.76 billion by 2031 at 5.05% CAGR over 2026-2031.

Strong residential remodeling demand, steady Sun Belt housing starts, and regulatory preferences for low-VOC building materials underpin this expansion. Domestic producers are gaining ground as antidumping duties reduce low-priced imports, while favorable natural-gas prices lower firing costs and support competitive local manufacturing . Digital printing, large-format porcelain slabs, and radiant-floor compatible designs are widening application potential and average selling prices. At the same time, labor shortages in qualified installers and intensifying competition from rigid-core LVT restrain absolute volume growth.

US Ceramic Tiles Market Trends and Insights

Resilient Housing Starts in Sun Belt States

Sun Belt construction continues to anchor demand even as other regions cool, with Florida's construction materials revenue reaching USD 997.6 million in 2024. Favorable climate, population inflows, and pro-business policies keep building permits comparatively stable, supporting predictable orders for tile producers. Manufacturers optimize logistics networks around these high-volume corridors, trimming freight costs and delivery lead times. Energy-efficient codes in hot climates reward the thermal-mass benefits of ceramic, nudging architects toward specification. Ongoing climate-adaptation investments further elevate tile's appeal because of its moisture resistance and durability.

Growing Adoption of Large-Format Porcelain Slabs

Architectural preference for seamless surfaces is accelerating 6 mm and 12 mm porcelain panels, which reduce grout lines and installation time. Louisville Tile's 6 mm panels launched in 2025 demonstrate how pre-cut formats address installer scarcity while commanding premium pricing. Daltile's ONE Quartz extra-large slabs unveiled at KBIS 2025 extend marble aesthetics into high-traffic zones without repeat patterns. Digital inkjet advances generate photorealistic veining on macro surfaces, differentiating from conventional squares. Capital-intensive slab kilns and polishing lines act as entry barriers, favoring incumbents with scale advantages. The format also aligns with hygiene trends in healthcare, hospitality, and luxury residential projects.

Volatile Natural-Gas Prices Inflating Kiln Costs

Energy constitutes roughly 30% of porcelain production budgets, and natural gas supplies 90% of that load. After bottoming at USD 2.21 per MMBtu in 2024, EIA projects prices will climb past USD 4.00 by 2026, pressuring kiln operators. Larger groups hedge exposure through multiyear contracts and co-generation, but smaller independents face squeezed margins or pass-through price hikes. Energy volatility also resets parity against imports from regions with coal-fired kilns, complicating competitive pricing. Investments in electric kilns offer long-run stability yet require substantial capital and grid upgrades, delaying widespread adoption.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficient Radiant-Heated Flooring Demand

- Post-Covid Commercial Renovation Wave

- Labor Shortages in Qualified Tile Installers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Porcelain holds 55.12% of United States ceramic tiles market share as of 2025, reflecting its low water-absorption rating and suitability for indoor-outdoor continuity. Advanced inkjet printing now renders deep veining, concrete patina, and textile textures, erasing historical design constraints. Manufacturers expand into 2 cm thick pavers and 6 mm thin panels, broadening end-uses from ventilated facades to furniture tops. Glazed ceramic remains relevant where cost sensitivity outweighs performance, sustaining value-oriented retail assortments. Unglazed quarry tiles cater to commercial kitchens that require coefficient-of-friction ratings exceeding 0.8. Mosaic and handmade formats occupy bespoke niches, often commanding multiples of average price per square foot. Sustainability credentials strengthen across categories as recycled glass frit and waste-heat recovery lower embodied carbon. Collectively, the mix illustrates how innovation allows the United States ceramic tiles market to serve mainstream and specialist demand simultaneously.

Investment in European-style Continua+ presses enables endless porcelain sizes, including 1.6 m-by-3.2 m slabs that cut to countertop blanks in three passes. These lines boost throughput and yield while reducing labor, supporting margin resilience even as commodity squares face price compression. Producers leverage proprietary glazes to deliver antimicrobial, anti-slip, or solar-reflective surfaces that open doors to healthcare, transportation, and exterior cladding specifications. Domestic capacity expansion also shields the United States ceramic tiles market from future tariff shocks by shortening supply chains and ensuring just-in-time replenishment. Continuous technological improvements position porcelain as both the growth engine and the competitive moat against substitute floorings.

Floor layouts account for 68.05% of United States ceramic tiles market size in 2025, rooted in bathrooms, kitchens, and high-traffic commercial corridors. Heavy-duty ratings, stain resistance, and lifetime wear warranties align with facility manager priorities. In multistory residential projects, dead-load limits increasingly permit large porcelain panels, reducing grout maintenance for owners. Conversely, wall cladding registers the fastest CAGR at 5.36%, propelled by design trends that run identical stone looks vertically for cohesion. Retail stores embrace tile feature walls to convey premium branding while meeting fire-code requirements. Health-care corridors adopt tiled wainscoting to survive aggressive chemical cleaning. Roofing, though niche, grows in Mediterranean-style luxury builds seeking thermal insulation and rain-shedding performance. These dynamics show the United States ceramic tiles market flexibly adapting to aesthetic, functional, and regulatory needs across surfaces.

Advances in high-bond, low-VOC mastics shorten cure times, allowing accelerated wall installations that fit compressed renovation schedules. Mechanical clip systems make 20 mm ventilated facades viable even for retrofit, slashing building-envelope energy loads. Manufacturers pack sample libraries with matching trims, thresholds, and bullnose options to encourage full-room specifications. Marketing emphasizes that uniform material across planes reduces visual clutter and future touch-up variance. As consumers view walls as canvases for personal expression, tile with metallic, fabric-inspired, or geometric relief finishes gains share. Collectively, these trends keep floor volume stable while elevating wall-segment growth within the broader United States ceramic tiles market.

The United States Ceramic Tiles Market Report is Segmented by Product Type (Porcelain Tiles, Glazed Ceramic Tiles and More), Application (Floor, Wall, Roofing), End-User (Residential, Commercial), Construction Type (New Construction, Renovation and Replacement), Distribution Channel (Specialty Stores and More), and Geography (Northeast, Midwest and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mohawk Industries (Dal-Tile, Marazzi, American Olean)

- Florida Tile

- Crossville Inc.

- Interceramic USA

- MSI Surfaces

- Emser Tile

- Porcelanosa USA

- Roca Tile USA

- Bedrosians Tile & Stone

- Anatolia Tile + Stone

- Walker Zanger

- Artistic Tile

- American Wonder Porcelain

- Mariner USA

- Dal-Tile Mexico Imports

- StonePeak Ceramics

- LAUFEN Bathrooms (U.S.)

- Florim USA

- IWT Florida (Tesoro)

- Vitromex USA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Resilient housing starts in Sun-Belt states

- 4.2.2 Growing adoption of large-format porcelain slabs

- 4.2.3 Energy-efficient radiant-heated flooring demand

- 4.2.4 Post-Covid commercial renovation wave

- 4.2.5 Indoor-air-quality regulations favoring low-VOC tiles

- 4.2.6 FEMA resilience grants for flood-resistant building materials

- 4.3 Market Restraints

- 4.3.1 Volatile natural-gas prices inflating kiln firing costs

- 4.3.2 Labor shortages in qualified tile installers

- 4.3.3 Competition from LVT/SPC rigid core flooring

- 4.3.4 PFAS litigation risk in certain glaze additives

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Industry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product Type

- 5.1.1 Porcelain Tiles

- 5.1.2 Glazed Ceramic Tiles

- 5.1.3 Unglazed Ceramic Tiles

- 5.1.4 Mosaic Tiles

- 5.1.5 Others (Decorative, Patterned, Handmade)

- 5.2 By Application

- 5.2.1 Floor

- 5.2.2 Wall

- 5.2.3 Roofing

- 5.3 By End-User

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.2.1 Hospitality (Hotels, Resorts)

- 5.3.2.2 Retail Spaces

- 5.3.2.3 Offices & Institutions

- 5.3.2.4 Healthcare

- 5.3.2.5 Educational Facilities

- 5.3.2.6 Transport Hubs (Airports, Metro, Bus Terminals)

- 5.3.2.7 Other Commercial Users

- 5.4 By Construction Type

- 5.4.1 New Construction

- 5.4.2 Renovation and Replacement

- 5.5 By Distribution Channel

- 5.5.1 Specialty Tile & Stone Stores

- 5.5.2 Home Improvement & DIY Stores

- 5.5.3 Online Retail

- 5.5.4 Direct Sales to Contractors

- 5.6 By Geography

- 5.6.1 Northeast

- 5.6.2 Midwest

- 5.6.3 Southeast

- 5.6.4 Southwest

- 5.6.5 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mohawk Industries (Dal-Tile, Marazzi, American Olean)

- 6.4.2 Florida Tile

- 6.4.3 Crossville Inc.

- 6.4.4 Interceramic USA

- 6.4.5 MSI Surfaces

- 6.4.6 Emser Tile

- 6.4.7 Porcelanosa USA

- 6.4.8 Roca Tile USA

- 6.4.9 Bedrosians Tile & Stone

- 6.4.10 Anatolia Tile + Stone

- 6.4.11 Walker Zanger

- 6.4.12 Artistic Tile

- 6.4.13 American Wonder Porcelain

- 6.4.14 Mariner USA

- 6.4.15 Dal-Tile Mexico Imports

- 6.4.16 StonePeak Ceramics

- 6.4.17 LAUFEN Bathrooms (U.S.)

- 6.4.18 Florim USA

- 6.4.19 IWT Florida (Tesoro)

- 6.4.20 Vitromex USA

7 Market Opportunities & Future Outlook

- 7.1 AI-assisted design personalization portals

- 7.2 Carbon-neutral tile certifications & EPD labeling

2026年全球水泥瓦市场报告2026年全球瓷器和陶瓷马赛克市场报告2026年全球磁砖填缝剂市场报告2026年全球陶瓷地砖和墙砖市场报告

2026年全球水泥瓦市场报告2026年全球瓷器和陶瓷马赛克市场报告2026年全球磁砖填缝剂市场报告2026年全球陶瓷地砖和墙砖市场报告 陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年

陶瓷砖市场报告:按类型、应用和地区划分 2026-2034 年 防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年全球陶瓷砖市场:机会与策略展望(至2034年)

防滑瓷砖市场规模、份额和成长分析:按类型、商业模式、应用、最终用途、地区和行业预测,2026-2033年全球陶瓷砖市场:机会与策略展望(至2034年) 陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分

陶瓷砖市场分析及预测(至2035年):依类型、产品、技术、应用、材质、最终使用者、安装方式、解决方案及销售形式划分 西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年

西班牙瓷砖市场:市场份额分析、行业趋势与统计、成长预测(2026-2031)日本水泥瓦市场:规模、份额、趋势和预测:按类型、应用和地区划分,2026-2034年