|

市场调查报告书

商品编码

1937354

东协电动车:市场占有率分析、产业趋势与统计、成长预测(2026-2031)ASEAN Electric Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

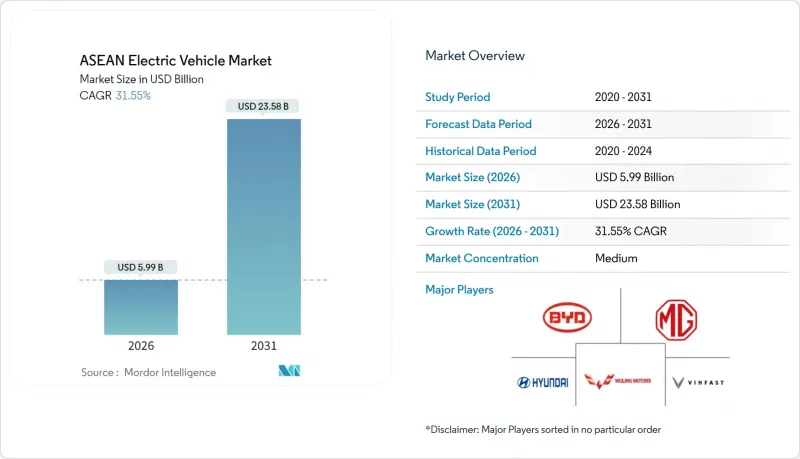

预计东协电动车市场将从 2025 年的 45.5 亿美元成长到 2026 年的 59.9 亿美元,并预计到 2031 年将达到 235.8 亿美元,2026 年至 2031 年的复合年增长率为 31.55%。

这一成长轨迹得益于政府积极的激励措施、丰富的镍蕴藏量支撑着本地电池供应链,以及公共和私人充电基础设施的快速发展。泰国的电动车3.5补贴计画、印尼的豪华车税收豁免政策以及越南的多年註册费豁免政策,在扩大消费者购买电动车的同时,也鼓励汽车製造商在本地生产。中国汽车製造商正透过积极的定价策略和领先生产投资抢占市场份额,而日本、韩国和区域品牌也在加速推进其市场扩张策略。东协电网的併网计画以及摩托车电池更换生态系统的发展,正在为服务、软体和二手电池等领域开闢新的收入来源。

东协电动车市场趋势与洞察

政府采购支援和消费税收优惠政策优惠

积极的财政政策正在推动东协电动车市场快速普及。泰国实施了一项340亿泰铢的补贴计划,要求电动车在当地组装。印尼也采取了类似的政策,对电动车免征0%的奢侈品税和1%的增值税,直至2025年。越南已将註册费免税期延长至2027年,马来西亚则计划透过降低购置税和免进口关税,到2030年实现电动车销量占比达到20%。菲律宾的《电动车产业发展法》规定,政府和企业车队中必须有5%的车辆为电动车,并透过免税进口进一步降低在地采购成本。这些协调一致的措施促进了泰国电动车销量的成长,并推动了越南电动机车销量的激增。

促进原始设备製造商本地化的倡议

东协电动车市场正从进口主导模式转向本地化生产和供应模式。比亚迪投资10亿美元在印尼建设的工厂计划于2025年底运作,年产能将达到15万辆;现代汽车在雅加达附近投资15.5亿美元建设的工厂也将新增25万辆的产能。泰国已获得来自中国汽车製造商超过30亿美元的投资承诺,其中长城汽车和奇瑞汽车领先。 VinFast的国际扩张计画包括在印尼和印度新建生产线;吉利汽车透过与印尼汉达尔汽车公司(PT Handal Indonesia Motor)的合资企业,计画在三年内新增100家零售店。这些工厂将满足日益增长的在地采购需求,降低物流成本,并为建立涵盖电池、电力电子和软体等零件的生态系统奠定基础。

与内燃机车辆的零售价格差异

在东协地区,入门级电动车的价格通常是同级内燃机车型的两倍,这限制了其在大众市场的普及。印尼在2025年上半年的销售量激增了267%,但市场渗透率仅9.1%。这是由于较高的残值让注重成本的消费者望而却步。在泰国,随着奖励的减少,豪华车细分市场的需求放缓,凸显了市场对补贴取消的需求弹性。儘管货运业者指出中型卡车的初始成本较高,但电池更换试点计画表明,其生命週期成本可以降低30%至40%。本地生产的电池组以及新建区域工厂带来的规模经济效益对于持续降低价格至关重要。

细分市场分析

2025年,乘用车将占东协电动车市场的46.55%,而越南电动摩托车销量在2025年上半年出现激增,这主要得益于VinFast平台国内销量成长488%。摩托车和三轮车正在改写成长格局,预计到2031年将达到32.40%的复合年增长率。印尼和泰国也透过免除停车费和牌照费等共享出行激励措施,复製了类似的成长势头。轻型商用车市场正在蓬勃发展,电子商务配送车辆的燃油成本可节省20-30%,这推动了物流业者的电气化转型。中型和重型卡车的发展相对滞后,仍在等待高密度电池的广泛应用以及能够抵消初期成本差异的财政措施。

都市区配送骑士称讚换电网路的便利性,充电时间缩短至两分钟以内。越南的目标是到2030年实现100万辆零排放两轮车上路,这一目标与河内市的拥挤费豁免政策相辅相成。新加坡已开始试行电动车调度许可证制度,优先保障排放排放车辆在高密度机场候车区行驶,进而改善驾驶人的经济状况。巴士和长途客车也受惠于当地的采购目标,新加坡的目标是到2030年实现50%的巴士电动化,而越南义安省则计划从2025年起全面实现更多车辆的电动化。这些政策正在加速东协电动车市场的模式多元化发展。

到2025年,电池式电动车(BEV)将占东协电动车市场85.70%的份额,并且是大多数汽车製造商(OEM)2031年发展蓝图的基石。电池价格下降、能量密度提高以及充电基础设施的扩展正在增强消费者的信心。插电式混合动力汽车(混合动力汽车。

燃料电池电动车将小规模规模成长,并在2026年至2031年间实现38.90%的最高复合年增长率。印尼国营电力公司(PLN)将于2024年在雅加达开设该地区首个加氢站,并计画兴建22座绿色氢气工厂,年产能达203吨。新加坡正在港口附近的专用车道上进行氢燃料公车试验,马来西亚国家石油公司(Petronas)正在评估用于商用车的蓝氢混合燃料。一个东协范围内的工作小组正在製定燃料电池安全标准,旨在符合联合国第134号法规,这是大规模进口的先决条件。这种技术多样性有助于保护东协电动车市场免受原材料价格波动的影响。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府采购及消费税收优惠政策优惠

- 促进原始设备製造商本地化的倡议

- 快速部署直流快速充电走廊

- 高镍电池的供应优势

- 电动车跨境零关税贸易

- 扩大摩托车电池更换生态系统

- 市场限制

- 与内燃机(ICE)的价格差异与比较

- 主要城市以外地区缺乏充电基础设施

- 电力系统不稳定和尖峰负载削减

- 不同文化对柴油皮卡的偏好

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方和消费者的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元)及销售量(单位))

- 按车辆类型

- 两轮车和三轮车

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 公车和长途客车

- 透过驱动系统

- 电池式电动车(BEV)

- 插电式混合动力电动车(PHEV)

- 燃料电池电动车(FCEV)

- 混合动力电动车(HEV)

- 按电荷等级

- 交流慢充/2级

- 直流快速充电(50kW 或以上)

- 按最终用户类型

- 适用于个人/家庭

- 商用车辆/物流

- 政府和公共交通

- 按国家/地区

- 印尼

- 泰国

- 马来西亚

- 越南

- 菲律宾

- 新加坡

- 缅甸

- 柬埔寨

- 寮国

- 汶莱

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- BYD Co. Ltd.

- SAIC Motor/MG Motor

- Hyundai Motor Company

- Toyota Motor Corporation

- Honda Motor Co., Ltd.

- Mitsubishi Motors Corporation

- Nissan Motor Corporation

- VinFast Auto Ltd.

- Wuling Motors

- Great Wall Motor

- GAC Aion

- Chery Automobile

- Tesla Inc.

- BMW Group

- Mercedes-Benz Group

- Kia Corp.

- Isuzu Motors

- BAIC Group

- Stellantis NV

- UD Trucks

第七章 市场机会与未来展望

The ASEAN electric vehicle market is expected to grow from USD 4.55 billion in 2025 to USD 5.99 billion in 2026 and is forecast to reach USD 23.58 billion by 2031 at 31.55% CAGR over 2026-2031.

Spirited government incentives, abundant nickel reserves that underpin local battery supply chains, and the rapid build-out of public and private charging infrastructure anchor this trajectory. Thailand's EV3.5 subsidy program, Indonesia's luxury-tax exemptions, and Vietnam's multi-year registration-fee waivers widen consumer access while compelling original-equipment manufacturers (OEMs) to localize production. Chinese automakers leverage aggressive pricing and early-mover manufacturing investments to dominate early market share positions while Japanese, Korean, and regional brands accelerate catch-up strategies. Grid integration initiatives under the ASEAN PowerGrid and maturing battery-swap ecosystems for two-wheelers open fresh revenue pools across services, software, and second-life battery streams.

ASEAN Electric Vehicle Market Trends and Insights

Government Purchase and Excise-Tax Incentives

Aggressive fiscal programs underpin early adoption across the ASEAN electric vehicle market. Thailand channels 34 billion baht in subsidies that require local assembly for eligibility, a policy mirrored by Indonesia's 0% luxury tax and 1% VAT on battery electric vehicles through 2025. Vietnam has extended registration-fee exemptions until 2027, while Malaysia targets a 20% EV sales mix by 2030 via purchase-tax relief and import-duty waivers. The Philippines mandates a 5% EV share in government and corporate fleets under the Electric Vehicle Industry Development Act, further reducing landed costs through zero-tariff imports. These coordinated instruments have lifted Thailand's EV sales and turbocharged Vietnam's electric-motorcycle sales volumes.

OEM Localization Commitments

The ASEAN electric vehicle market is shifting from import-led to locally manufactured supply. BYD's USD 1 billion Indonesian hub coming online in late 2025 will produce 150,000 vehicles annually, while Hyundai's USD 1.55 billion complex near Jakarta adds 250,000-unit capacity. Thailand has secured over USD 3 billion in Chinese OEM pledges, anchored by Great Wall Motor and Chery. VinFast's outward expansion includes new lines in Indonesia and India, and Geely enters via a joint venture with PT Handal Indonesia Motor to scale 100 retail outlets in three years. These factories meet rising local-content thresholds, compress logistics costs, and seed component ecosystems across batteries, power electronics, and software.

High Retail Price Gap Vs. ICE

Entry-level EVs across ASEAN are often priced at twice that of comparable internal-combustion models, curbing mass-market uptake. Indonesia's penetration reached 9.1% in 1H 2025 despite a 267% sales spike, as the remaining sticker premium deters cost-sensitive buyers. Thailand's premium-car sub-segment experienced softening demand once incentives tapered, revealing elasticity to subsidy removal. Freight operators highlight elevated upfront costs for medium-duty trucks, even though battery-swap pilots hint at 30-40% lifetime savings. Continual price compression depends on localized battery packs and scale economics from new regional plants .

Other drivers and restraints analyzed in the detailed report include:

- Rapid Roll-Out of DC Fast-Charging Corridors

- Nickel-Rich Battery Supply Advantage

- Patchy Charging Outside Tier-1 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars delivered 46.55% of the ASEAN electric vehicle market in 2025, yet electric motorcycles posted a sales jump in Vietnam in 1H 2025, powered by VinFast's 488% domestic surge. Two- and three-wheelers are rewriting the growth script, projecting a growth of 32.40% CAGR by 2031. Indonesia and Thailand replicate this momentum through ride-hail incentives that waive parking fees and license-plate charges. The light-commercial segment gains traction as e-commerce fulfillment fleets log 20-30% fuel savings, nudging logistics operators toward electrification mandates. Medium and heavy trucks lag while waiting for higher-density batteries and fiscal levers that neutralize upfront differentials.

Urban delivery riders cite the convenience of battery-swap networks that compress refueling to under two minutes. Vietnam targets 1 million zero-emission motorcycles by 2030, an ambition linked to congestion-charge exemptions in Hanoi. Singapore pilots electric ride-hail permits that prioritize emissions-free vehicles at high-density airport ranks, enhancing driver economics. Buses and coaches benefit from municipal procurement targets, with Singapore aiming for 50% electric buses by 2030 and Vietnam's Nghe An province mandating fully electric additions from 2025. Collectively, these policies accelerate modal diversification within the ASEAN electric vehicle market.

Battery electric vehicles maintained 85.70% ASEAN electric vehicle market share in 2025 and anchor most OEM roadmaps through 2031. Lower battery prices, rising energy density, and expanded charging corridors reinforce consumer confidence. Plug-in hybrids carve out a transition niche in Thailand where public skepticism over highway charger availability lingers. Toyota leverages brand equity by bundling home-charger installation and extended warranties, insulating hybrid residual values.

Fuel-cell electric vehicles register the highest 2026-2031 CAGR at 38.90% from a small base. Indonesia's PLN opened the sub-region's first hydrogen station in Jakarta in 2024 and plans 22 green-hydrogen plants producing 203 tons yearly. Singapore tests hydrogen buses on dedicated lanes near port zones, and Malaysia's Petronas evaluates blue-hydrogen blending for commercial fleets. A pan-ASEAN working group is drafting fuel-cell safety codes to align with UN Regulation 134, a prerequisite for scaled imports. This technology pluralism cushions the ASEAN electric vehicle market against raw-material volatility.

The ASEAN Electric Vehicle Market Report is Segmented by Vehicle Type (Two and Three Wheelers, Passenger Cars, and More), Drive-Train Technology (Battery Electric Vehicles (BEV), Plug-In Hybrid Electric Vehicles (PHEV), and More), Charging Level (AC Slow/Level-2, DC Fast), End-User Type, and Country (Indonesia, Thailand, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- BYD Co. Ltd.

- SAIC Motor / MG Motor

- Hyundai Motor Company

- Toyota Motor Corporation

- Honda Motor Co., Ltd.

- Mitsubishi Motors Corporation

- Nissan Motor Corporation

- VinFast Auto Ltd.

- Wuling Motors

- Great Wall Motor

- GAC Aion

- Chery Automobile

- Tesla Inc.

- BMW Group

- Mercedes-Benz Group

- Kia Corp.

- Isuzu Motors

- BAIC Group

- Stellantis NV

- UD Trucks

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government Purchase and Excise-Tax Incentives

- 4.2.2 OEM Localization Commitments

- 4.2.3 Rapid Roll-Out of DC Fast-Charging Corridors

- 4.2.4 Nickel-Rich Battery Supply Advantage

- 4.2.5 Cross-Border Zero-Tariff EV Trade

- 4.2.6 Two-Wheeler Battery-Swap Ecosystems Scaling

- 4.3 Market Restraints

- 4.3.1 High Retail Price Gap Vs. ICE

- 4.3.2 Patchy Charging Outside Tier-1 Cities

- 4.3.3 Grid Instability and Peak-Load Limits

- 4.3.4 Cultural Preference for Diesel Pick-Ups

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Two and Three Wheelers

- 5.1.2 Passenger Cars

- 5.1.3 Light Commercial Vehicles

- 5.1.4 Medium and Heavy Commercial Vehicles

- 5.1.5 Buses and Coaches

- 5.2 By Drive-train Technology

- 5.2.1 Battery Electric Vehicles (BEV)

- 5.2.2 Plug-in Hybrid Electric Vehicles (PHEV)

- 5.2.3 Fuel-Cell Electric Vehicles (FCEV)

- 5.2.4 Hybrid Electric Vehicles (HEV)

- 5.3 By Charging Level

- 5.3.1 AC Slow / Level-2

- 5.3.2 DC Fast (>= 50 kW)

- 5.4 By End-User Type

- 5.4.1 Personal / Household

- 5.4.2 Commercial Fleet and Logistics

- 5.4.3 Government and Public Transport

- 5.5 By Country

- 5.5.1 Indonesia

- 5.5.2 Thailand

- 5.5.3 Malaysia

- 5.5.4 Vietnam

- 5.5.5 Philippines

- 5.5.6 Singapore

- 5.5.7 Myanmar

- 5.5.8 Cambodia

- 5.5.9 Laos

- 5.5.10 Brunei

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BYD Co. Ltd.

- 6.4.2 SAIC Motor / MG Motor

- 6.4.3 Hyundai Motor Company

- 6.4.4 Toyota Motor Corporation

- 6.4.5 Honda Motor Co., Ltd.

- 6.4.6 Mitsubishi Motors Corporation

- 6.4.7 Nissan Motor Corporation

- 6.4.8 VinFast Auto Ltd.

- 6.4.9 Wuling Motors

- 6.4.10 Great Wall Motor

- 6.4.11 GAC Aion

- 6.4.12 Chery Automobile

- 6.4.13 Tesla Inc.

- 6.4.14 BMW Group

- 6.4.15 Mercedes-Benz Group

- 6.4.16 Kia Corp.

- 6.4.17 Isuzu Motors

- 6.4.18 BAIC Group

- 6.4.19 Stellantis NV

- 6.4.20 UD Trucks

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment

电动车虚拟原型製作市场:按组件、技术、部署模式、应用、车辆类型和最终用户划分-2026-2032年全球市场预测

电动车虚拟原型製作市场:按组件、技术、部署模式、应用、车辆类型和最终用户划分-2026-2032年全球市场预测 2026年全球V2B(车辆到建筑)电力市场报告

2026年全球V2B(车辆到建筑)电力市场报告 全电动多用途货车市场规模、份额和成长分析:按产能、应用、终端用户产业、地区和产业预测,2026-2033年

全电动多用途货车市场规模、份额和成长分析:按产能、应用、终端用户产业、地区和产业预测,2026-2033年 长续航里程电动车市场规模、份额和成长分析:按车辆类型、电池类型、充电基础设施、续航里程、消费群体、动力系统、功率输出和地区划分-2026-2033年产业预测

长续航里程电动车市场规模、份额和成长分析:按车辆类型、电池类型、充电基础设施、续航里程、消费群体、动力系统、功率输出和地区划分-2026-2033年产业预测 800V电动车架构市场规模、份额和成长分析:按车辆、架构、充电方式、组件、应用和地区划分-2026-2033年产业预测

800V电动车架构市场规模、份额和成长分析:按车辆、架构、充电方式、组件、应用和地区划分-2026-2033年产业预测 电动车售后市场规模、份额和成长分析:按零件类型、车辆类型、服务类型、动力系统、销售管道、最终用户、地区和产业预测,2026-2033年

电动车售后市场规模、份额和成长分析:按零件类型、车辆类型、服务类型、动力系统、销售管道、最终用户、地区和产业预测,2026-2033年 电动车(零能耗汽车)市场规模、份额和成长分析:按车辆类型、电源管理方法、充电基础设施、电池技术、最终用户和地区划分-产业预测(2026-2033 年)

电动车(零能耗汽车)市场规模、份额和成长分析:按车辆类型、电源管理方法、充电基础设施、电池技术、最终用户和地区划分-产业预测(2026-2033 年) 2026-2030年全球电动车市场

2026-2030年全球电动车市场 欧洲电动车市场:依动力类型(纯电动车 (BEV)、燃料电池电动车 (FCEV)、插电式混合动力车 (PHEV)、混合动力车 (HEV))、功率输出(100kW 以下、100kW-250kW)、应用(个人用途、商业用途)和地区划分 - 全球预测至 2036 年

欧洲电动车市场:依动力类型(纯电动车 (BEV)、燃料电池电动车 (FCEV)、插电式混合动力车 (PHEV)、混合动力车 (HEV))、功率输出(100kW 以下、100kW-250kW)、应用(个人用途、商业用途)和地区划分 - 全球预测至 2036 年 中国电动车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)

中国电动车市场:市场占有率分析、产业趋势与统计、成长预测(2026-2031年)