|

市场调查报告书

商品编码

1937384

非洲汽车机油市场份额分析、产业趋势与统计、成长预测(2026-2031)Africa Automotive Engine Oils - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

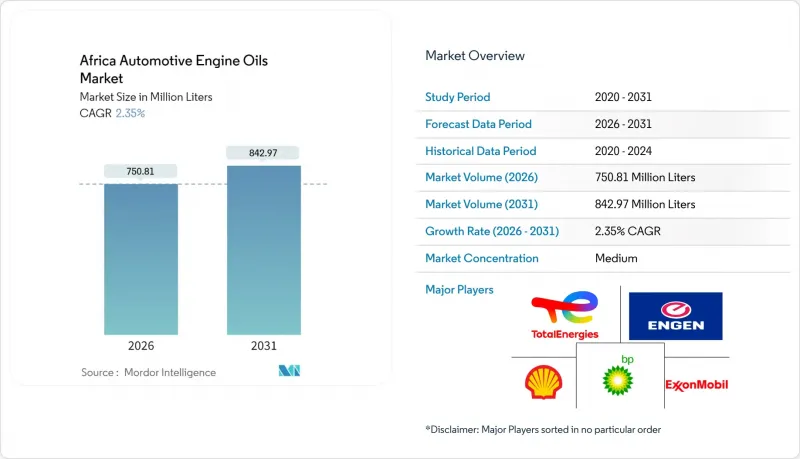

2025年非洲汽车机油市场价值为7.3357亿公升,预计到2031年将达到8.4297亿公升,而2026年为7.5081亿升。

预计在预测期(2026-2031 年)内,复合年增长率将达到 2.35%。

市场扩张依赖车辆的持续成长、工业化进程的加快以及产品结构从单一黏度矿物油向多黏度合成油的逐步转变。然而,南非、肯亚和奈及利亚炼油厂的持续停产导致当地基础油供应紧张,并增加了对进口的依赖。这迫使调配公司与全球贸易商重新谈判供应合约。同时,假冒仿冒品产品的平行通路不断侵蚀合法需求,迫使各大品牌投资于序列化、防篡改包装和技术人员培训专案。总体而言,儘管面临基础设施方面的挑战,但市场稳定的需求基础、不断扩大的分销网络以及燃油和排放气体标准的统一监管,都支撑着中期前景的乐观。

非洲汽车机油市场趋势与洞察

汽车保有量增加和道路车辆尺寸增大

非洲每千人仅有44辆汽车的低车普及率表明,其车队规模仍有很大的成长空间。摩洛哥以出口为导向的製造地,以及加纳和卢安达国内组装的不断增长,正在推动出厂和售后市场润滑油消费的成长。在肯亚,96%的进口车辆以及衣索比亚和奈及利亚80%的二手车销量都支撑了对换油週期较短的传统润滑油的需求。人口结构也是一个决定性因素:75%的非洲人口年龄在35岁以下,这推动了对个人出行的需求。预测模型显示,非洲大陆4,500万辆汽车的保有量可能在20年内成长两倍,这将直接增加对引擎润滑油产品的基准需求。

扩大汽车售后市场和维护意识

肯亚的行动电话普及率超过65%,产品资讯可触及超过5亿用户,进而提升驾驶对润滑油的认知。维修店正利用社群媒体和简讯宣传活动来推广换油提醒和品牌宣传,逐步引导偏好转向具有真伪验证功能的优质包装产品。肯亚的润滑油消费量为53,500吨,占国内需求的87%,其中商用车和私家车的需求量最大。随着消费者逐渐意识到选择合适的润滑油能够降低车辆营运成本,品牌商正在为维修技师开发忠诚度计画,结合培训、促销资料和小包装奖励,鼓励他们更换利润更高的多级润滑油。

大量非法进口二手对新油需求带来压力

走私货和假润滑油规避了品质检验,价格比官方价格低40%,严重侵蚀了授权经销商的利润。据尼日利亚润滑油调配商协会称,高硫假润滑油正流入公开市场和授权服务中心,导致引擎过早磨损,并损害品牌信誉。坦尚尼亚监管机构发现,2017年该国消耗的3,700万公升润滑油中,有三分之一来自使用假冒认证标籤的无证商贩。这种流通现象扭曲了需求预测,使库存计画更加复杂,并迫使品牌所有者投入资金进行公共宣传宣传活动和支持执法工作。

细分市场分析

到2025年,乘用车引擎油(PCMO)将维持非洲汽车机油市场54.92%的份额。该细分市场受益于相对较短的换油週期(5000-8000公里)和广泛的消费群,包括在非正规研讨会保养的车辆。同时,儘管重型机油(HDMO)的车辆保有量较小,但由于其单车用油量不成比例地高(铰接式卡车的单车用油量可达40公升),因此对市场的贡献也相当显着。摩托车机油虽然基数较小,但预计将保持最高的成长势头,复合年增长率(CAGR)将达到2.58%,这主要得益于肯亚、乌干达和奈及利亚摩托车的广泛使用以及「最后一公里」配送体系的完善。黏度等级的变化显示其正在逐步现代化。预计到2026年,单一黏度SAE40机油的市占率将下降至37%,而多黏度15W-40机油在乘用车和商用车领域的应用将持续扩大。在授权经销商是保固合规性基础的主要都会区,优质的OEM认证5W-30合成机油正在兴起。汽车引擎机油市场主要由乘用车机油(PCMO)、商用车机油(HDMO)和摩托车机油市场所构成,不同车型和保养方式的差异反映了它们各自的成长动态。

次生影响在连接港口和内陆消费中心的商业运输走廊沿线显而易见。超载卡车、多尘环境和燃油品质波动加剧了润滑油的氧化压力,促使车队营运商倾向于选择CI-4和CK-4类别中通用的更具侵略性的添加剂配方。同时,Bolt和Uber等叫车服务在都市区的高频使用率不断上升,推动了对符合严格挥发性和沈淀物控制参数的PCMO的需求。随着政府车队更新计画优先考虑本地组装的公车,需求弹性正转向高容量HDMO,这凸显了HDMO的战略重要性,儘管PCMO在非洲汽车机油市场拥有销售优势。具有延长换油週期的合成油混合物越来越多地与滤清器套装和资料登录服务合约捆绑销售,为生命週期管理提案奠定了基础。

非洲汽车引擎油市场报告按树脂类型(乘用车引擎油、重型车辆引擎油、摩托车机油)、基础油(矿物油、合成油、半合成油、生物基油)和地区(南非、埃及、奈及利亚和非洲其他地区)进行细分。市场预测以公升为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 汽车保有量和道路上车辆数量的增加

- 提高汽车售后市场和维护意识

- 工业化和基础设施发展

- 引入先进引擎和更严格的排放气体法规

- 过渡到使用优质合成润滑油

- 市场限制

- 大量非法进口废油正在抑制对新油的需求。

- 取消燃油补贴会阻碍车辆行驶里程(VKT)的成长。

- 由于萨普列夫和LOBP油田关闭,基础油供应紧张。

- 价值炼和通路分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 产业间竞争

- 法律规范

- 汽车产业的趋势

第五章 市场规模与成长预测

- 依树脂类型

- 乘用车引擎机油(PCMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 单黏度等级

- 其他年级

- 重型机油(HDMO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 单黏度等级

- 其他年级

- 摩托车机油(MCO)

- 0W-XX

- 5W-XX

- 10W-XX

- 15W-XX

- 单黏度等级

- 其他年级

- 乘用车引擎机油(PCMO)

- 基础油

- 矿物油

- 合成油

- 半合成油

- 生物基

- 按地区

- 南非

- 埃及

- 奈及利亚

- 其他非洲地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Afriquia

- Astron Energy Pty Ltd

- BP plc(Castrol)

- Chevron Corporation

- Engen Petroleum Ltd

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- LUKOIL

- Motul

- Oando PLC

- OLA Energy

- PETRONAS Lubricants

- Shell plc

- TotalEnergies

- Saudi Arabian Oil Co.

第七章 市场机会与未来展望

第八章:执行长面临的关键策略挑战

The Africa Automotive Engine Oils Market was valued at 733.57 Million Liters in 2025 and estimated to grow from 750.81 Million Liters in 2026 to reach 842.97 Million Liters by 2031, at a CAGR of 2.35% during the forecast period (2026-2031).

Market expansion hinges on sustained fleet growth, progressive industrialization, and a gradual shift in product mix from monograde mineral oils to multigrade synthetic formulations. Ongoing refinery shutdowns in South Africa, Kenya, and Nigeria, however, have tightened local base-oil availability, prompting greater reliance on imports and pushing blenders to renegotiate supply contracts with global traders. Parallel counterfeit trade channels continue to erode legitimate demand, compelling leading brands to invest in serialization, tamper-evident packaging, and mechanic-level training schemes. On balance, the market's steady demand base, broadening distribution networks, and regulatory alignment on fuel and emissions standards create favorable medium-term prospects despite infrastructural headwinds.

Africa Automotive Engine Oils Market Trends and Insights

Rising Vehicle Ownership and Expanding On-Road Fleet Size

Africa's low motorization rate of 44 vehicles per 1,000 inhabitants underscores substantial room for fleet enlargement. Morocco's export-oriented manufacturing hubs, together with rising domestic assembly in Ghana and Rwanda, accelerate vehicle additions that consume factory-fill and aftermarket oil volumes. Used-vehicle imports comprise 96% of Kenya's inflows and 80% of sales in Ethiopia and Nigeria, sustaining demand for conventional formulations that require shorter drain intervals. Demographic momentum is equally decisive; 75% of Africans are under 35, driving personal mobility aspirations. Projection models indicate that the continent's 45 million-unit fleet could triple within two decades, directly translating into increased baseline demand for engine lubrication products.

Growing Automotive Aftermarket and Maintenance Awareness

Mobile penetration above 65% enables the delivery of product information to more than 500 million subscribers, thereby elevating lubricant literacy among motorists. Workshops leverage social media and SMS campaigns to promote oil-change reminders and branded promotions, gradually shifting consumer preference toward premium packaging with verifiable authenticity features. Kenya's finished lubricant consumption of 53,500 metric tonnes illustrates how 87% of national demand is accumulated from commercial and private automotive applications. As consumers begin to equate proper oil selection with lower total vehicle operating costs, brand owners deploy mechanic loyalty programs that bundle training, point-of-sale materials, and small-pack incentives, stimulating trade-up to higher-margin multigrade oils.

Illicit Bulk Imports of Used Oils Depressing Virgin Demand

Smuggled or adulterated lubricants evade quality inspection protocols and undercut branded pricing by as much as 40%, undermining the margins of legitimate distributors. Nigeria's association of lubricant blenders reports that high-sulfur counterfeit oils are infiltrating both open markets and formal service centers, inducing premature engine wear and eroding brand trust. Tanzania's regulator traced one-third of 37 million liters consumed in 2017 to unlicensed traders applying falsified certification stickers. Such leakage distorts demand estimates, complicates inventory planning, and forces brand owners to fund public-education campaigns and legal enforcement support.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Industrialization and Infrastructure Development

- Introduction of Advanced Engines and Stricter Emission Norms

- Tight Base-Oil Supply Amid SAPREF and LOBP Closures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger car motor oil (PCMO) retained 54.92% of the Africa Automotive Engine Oils market share in 2025. The segment benefits from relatively short drain intervals of 5,000 - 8,000 km and a broad consumer base, with vehicles serviced through informal workshops. Heavy-duty motor oil (HDMO), however, accounts for a disproportionately higher volume per sump-up to 40 liters for articulated trucks-ensuring a material contribution even at lower vehicle counts. Motorcycle engine oil, albeit starting from a smaller base, displays the highest forward momentum with a 2.58% CAGR, propelled by two-wheeler proliferation in Kenya, Uganda, and Nigeria's last-mile delivery ecosystems. Viscosity-grade evolution illustrates gradual modernization: the share of monograde SAE 40 is sliding toward 37% by 2026, as multigrade 15W-40 gains traction in both passenger and commercial categories. Premium OEM-approved 5W-30 synthetics are emerging in Tier-1 metro areas where authorized dealerships anchor warranty compliance. Collectively, PCMO, HDMO, and motorcycle oils account for the bulk of Africa Automotive Engine Oils market size, with differentiated growth dynamics reflecting varied fleet compositions and service practices.

Second-order effects are pronounced in commercial haulage corridors that connect ports with inland consumption hubs. Overloaded trucks, dusty environments, and variable fuel quality heighten oxidative stress on lubricants, driving fleet operators to favor robust additive packages common in CI-4 and CK-4 categories. In parallel, ride-hailing services such as Bolt and Uber increase high-frequency urban use cycles, raising demand for PCMO meeting tight volatility and deposit-control parameters. As government fleet-renewal schemes prioritize locally assembled buses, demand elasticity shifts toward volume-draining HDMO, reinforcing its strategic relevance despite PCMO's numeric supremacy within Africa automotive engine oils market. Synthetic blends marketed under extended drain promises are increasingly bundled with filter packages and data-logging service contracts, setting the stage for life-cycle-management propositions.

The Africa Automotive Engine Oils Market Report is Segmented by Resin Type (Passenger Car Motor Oil, Heavy Duty Motor Oil, and Motorcycle Engine Oil), Base Stock (Mineral, Synthetic, Semi-Synthetic, and Bio-Based), and Geography (South Africa, Egypt, Nigeria, and Rest of Africa). The Market Forecasts are Provided in Terms of Volume (Liters).

List of Companies Covered in this Report:

- Afriquia

- Astron Energy Pty Ltd

- BP plc (Castrol)

- Chevron Corporation

- Engen Petroleum Ltd

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International

- LUKOIL

- Motul

- Oando PLC

- OLA Energy

- PETRONAS Lubricants

- Shell plc

- TotalEnergies

- Saudi Arabian Oil Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising vehicle ownership and expanding on-road fleet size

- 4.2.2 Growing automotive aftermarket and maintenance awareness

- 4.2.3 Increasing industrialization and infrastructure development

- 4.2.4 Introduction of advanced engines and stricter emission norms

- 4.2.5 Shift toward premium and synthetic lubricants

- 4.3 Market Restraints

- 4.3.1 Illicit bulk imports of used oils depressing virgin demand

- 4.3.2 Fiscal removal of fuel subsidies scuttling VKT growth

- 4.3.3 Tight base-oil supply amid Sapref and LOBP closures

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

- 4.6 Regulatory Framework

- 4.7 Automotive Industry Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Resin Type

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.1.1.1 0W-XX

- 5.1.1.2 5W-XX

- 5.1.1.3 10W-XX

- 5.1.1.4 15W-XX

- 5.1.1.5 Monogrades

- 5.1.1.6 Other Grades

- 5.1.2 Heavy Duty Motor Oil (HDMO)

- 5.1.2.1 0W-XX

- 5.1.2.2 5W-XX

- 5.1.2.3 10W-XX

- 5.1.2.4 15W-XX

- 5.1.2.5 Monogrades

- 5.1.2.6 Other Grades

- 5.1.3 Motorcycle Engine Oil (MCO)

- 5.1.3.1 0W-XX

- 5.1.3.2 5W-XX

- 5.1.3.3 10W-XX

- 5.1.3.4 15W-XX

- 5.1.3.5 Monogrades

- 5.1.3.6 Other Grades

- 5.1.1 Passenger Car Motor Oil (PCMO)

- 5.2 By Base Stock

- 5.2.1 Mineral

- 5.2.2 Synthetic

- 5.2.3 Semi-Synthetic

- 5.2.4 Bio-Based

- 5.3 By Geography

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 Nigeria

- 5.3.4 Rest of Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Production Capacity, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Afriquia

- 6.4.2 Astron Energy Pty Ltd

- 6.4.3 BP plc (Castrol)

- 6.4.4 Chevron Corporation

- 6.4.5 Engen Petroleum Ltd

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Gulf Oil International

- 6.4.9 LUKOIL

- 6.4.10 Motul

- 6.4.11 Oando PLC

- 6.4.12 OLA Energy

- 6.4.13 PETRONAS Lubricants

- 6.4.14 Shell plc

- 6.4.15 TotalEnergies

- 6.4.16 Saudi Arabian Oil Co.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs

机油添加剂市场:按类型、功能、销售管道和应用划分-2026-2032年全球市场预测汽车化妆品市场:依产品类别、车辆类型、技术、应用和销售管道划分-2026-2032年全球预测汽车添加剂市场:依产品类型、功能、原料、形态、车辆类型和销售管道-2026-2032年全球预测

机油添加剂市场:按类型、功能、销售管道和应用划分-2026-2032年全球市场预测汽车化妆品市场:依产品类别、车辆类型、技术、应用和销售管道划分-2026-2032年全球预测汽车添加剂市场:依产品类型、功能、原料、形态、车辆类型和销售管道-2026-2032年全球预测 全球汽车添加剂市场规模、份额、趋势和成长分析报告(2026-2034)

全球汽车添加剂市场规模、份额、趋势和成长分析报告(2026-2034) 汽车外观化学品市场报告:按应用、最终用途和地区划分 2026-2034 年

汽车外观化学品市场报告:按应用、最终用途和地区划分 2026-2034 年 汽车化妆品化学品市场-全球产业规模、份额、趋势、机会和预测:按产品类型、车辆类型、销售管道、地区和竞争格局划分,2021-2031年

汽车化妆品化学品市场-全球产业规模、份额、趋势、机会和预测:按产品类型、车辆类型、销售管道、地区和竞争格局划分,2021-2031年 汽车引擎机油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)日本汽车机油市场报告(按等级(矿物油、半合成油、全合成油)、引擎类型(汽油、柴油、替代燃料)、车辆类型(商用车、摩托车、乘用车)和地区划分,2026-2034)

汽车引擎机油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)日本汽车机油市场报告(按等级(矿物油、半合成油、全合成油)、引擎类型(汽油、柴油、替代燃料)、车辆类型(商用车、摩托车、乘用车)和地区划分,2026-2034) 汽车外观化学品市场(按产品类型、车辆类型、应用、国家和地区)—2025 年至 2032 年的行业分析、市场规模、市场份额和预测

汽车外观化学品市场(按产品类型、车辆类型、应用、国家和地区)—2025 年至 2032 年的行业分析、市场规模、市场份额和预测 汽车售后燃料添加剂市场:按产品类型、按燃料类型、按车辆类型、按分销管道、按最终用户、按地区

汽车售后燃料添加剂市场:按产品类型、按燃料类型、按车辆类型、按分销管道、按最终用户、按地区