|

市场调查报告书

商品编码

1937389

南美润滑油:市场占有率分析、产业趋势与统计、成长预测(2026-2031)South America Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

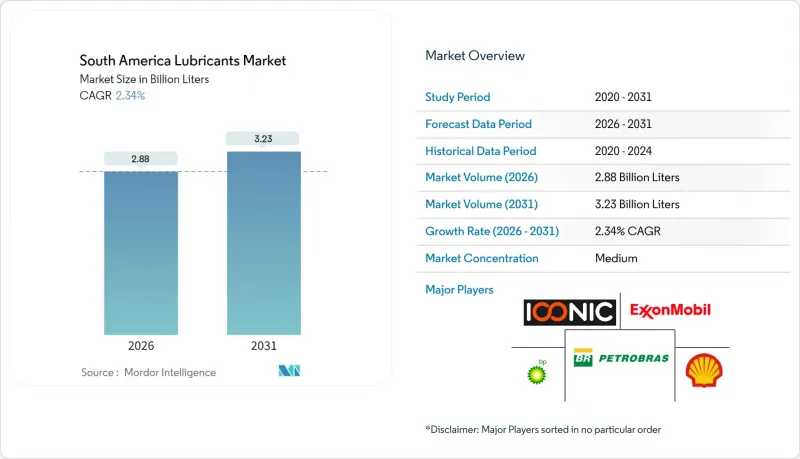

预计到 2026 年,南美润滑油市场规模将达到 28.8 亿公升。

这意味着从 2025 年的 28.1 亿公升成长到 2031 年的 32.3 亿公升,2026 年至 2031 年的复合年增长率为 2.34%。

区域货运量的回升、海上石油活动的扩张以及工业现代化进程的持续推进支撑了市场需求,而汇率波动和政策变化则带来了局部风险。巴西的汽车製造业、巴西和圭亚那的深海探勘以及智利和秘鲁的自动化采矿业共同确保了广泛的消费群体。以风能和太阳能主导的可再生能源的兴起,正在创造对涡轮机油和液压油的新需求,而更严格的排放标准正在加速向低SAPS和合成油的过渡。市场竞争强度目前仍处于中等水平,但随着跨国公司加强本地供应链以及区域公司透过併购和分销合作寻求规模化,竞争正在加剧。

南美洲润滑油市场趋势与分析

新冠疫情后陆上货运距离强劲復苏

近岸外包的兴起和电子商务的扩张推动了巴西、阿根廷和智利长途卡车运输业的发展,货运量已超过疫情前水准。光是巴西的卡车运输业就承担了该国60%以上的货运量,目前市场对能够延长换油週期并提高燃油经济性的优质机油和变速箱油的需求日益增长。大豆、玉米和铜的丰收进一步推动了物流旺季期间对润滑油的需求,巩固了短期消费激增,并为市场成长奠定了基础。

巴西和圭亚那深水能源和电力开发活动的加速推进,正在推动对高性能钻井液的需求。

巴西的盐盐层下和圭亚那的斯塔布鲁克油田都需要能够承受极端温度和深达2000公尺的合成钻井泥浆、海底齿轮油和液压油。埃克森美孚的多平台专案和巴西石油公司的海底增压合约都是专业服务模式的典范,这种模式不仅能提供溢价,还能深化供应商与客户之间的技术合作。

阿根廷的长期燃油补贴抑制了高檔润滑油的消费。

补贴低价抑制了消费者购买高效合成机油的意愿,导致许多车主必须频繁更换矿物油,阻碍了乘用车机油增值成长。补贴计画历来优先考虑销售量而非增值,鼓励消费者频繁更换传统矿物油,而非使用长效高级产品。这种情况对乘用车市场的影响尤其显着,因为注重成本的消费者更倾向于即时的节省,而非引擎的长期保护和燃油经济性。

细分市场分析

到2025年,机油将占南美润滑油市场份额的39.72%,而液压油预计到2031年将以2.66%的复合年增长率增长,这主要得益于采矿、农业和可再生能源领域自动化程度的提高。采用合成或生物基原料配製的特种液压油可确保高压系统所需的抗氧化性和耐热性。变速箱油和齿轮油将受益于车辆现代化改造计划,而润滑脂则可在严苛的海洋和工业环境中为轴承提供保护。

排放气体法规正推动机油升级,转向III类基础油和合成混合油,但价格因素意味着矿物油产品在老旧车辆中仍有市场需求。随着可再生能源的扩张,液压油的需求不断增长,而可生物降解配方更受青睐,以符合环保法规。添加剂化学领域的持续研发使区域性润滑油调配企业能够在南美洲润滑油市场提供差异化产品。

南美洲润滑油报告按产品类型(引擎油、变速箱和齿轮油、液压油、润滑脂等)、基础油(矿物油、合成油、半合成油、生物基油)、最终用户(汽车、重型机械、秘鲁和金属加工、发电、船舶和海上、其他行业)以及地区(阿根廷、巴西、智利、哥伦比亚、秘鲁、其他南美国家)进行细分。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新冠感染疾病结束后,陆运货运距离强劲復苏

- 巴西和圭亚那深水能源和电力专案的加速推进,推动了对高性能钻井液的需求。

- 逐步实施相当于欧盟6排放气体标准的法规(巴西为PROCONVE P-8)将推动低SAPS引擎机油的普及。

- 该地区大豆生物柴油混合燃料的激增将推动生物基液压油的成长。

- 智利和秘鲁矿用车辆的快速自动化正在推动长效合成齿轮油的需求。

- 市场限制

- 阿根廷的长期燃油补贴抑制了高檔润滑油的消费。

- 货币贬值风险可能导致聚醚氧化物(PAO)及其添加剂包装的进口成本增加。

- 电动摩托车在都市区日益普及,导致对摩托车机油的需求下降。

- 价值链分析

- 波特五力模型

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 竞争强度

第五章 市场规模与成长预测

- 依产品类型

- 机油

- 变速箱油和齿轮油

- 油压

- 润滑脂

- 金属加工油

- 加工油及其他

- 基础油

- 矿物油

- 合成油(PAO、酯、PAG)

- 半合成

- 生物基

- 按最终用户行业划分

- 车

- 重型机械

- 冶金与金属加工

- 发电

- 海洋/近海

- 其他行业

- 按国家/地区

- 阿根廷

- 巴西

- 智利

- 哥伦比亚

- 秘鲁

- 其他南美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- AMSOIL INC.

- BP plc(Castrol)

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International Ltd

- ICONIC

- Petrobras

- Petroliam Nasional Berhad(PETRONAS)

- Repsol

- Shell plc

- Terpel

- TotalEnergies

- YPF

- ZF Friedrichshafen AG

第七章 市场机会与未来展望

South America Lubricants Market size in 2026 is estimated at 2.88 Billion Liters, growing from 2025 value of 2.81 Billion Liters with 2031 projections showing 3.23 Billion Liters, growing at 2.34% CAGR over 2026-2031.

Recovering regional freight mileage, expanding offshore oil activity, and ongoing industrial modernization underpin demand, even as currency volatility and policy shifts create pockets of risk. Automotive manufacturing in Brazil, deep-water exploration in Brazil and Guyana, and mining automation in Chile and Peru together secure a broad consumption base. Renewable power additions, led by wind and solar, are introducing new needs for turbine and hydraulic fluids, while stricter emissions standards are accelerating migration toward low-SAPS and synthetic formulations. Competitive intensity remains moderate but rising as multinationals strengthen local supply chains and regional firms seek scale through mergers and distribution alliances.

South America Lubricants Market Trends and Insights

Strong Rebound in On-Road Freight Mileage Post-COVID

Freight activity has surpassed pre-pandemic levels as near-shoring shifts and e-commerce intensify long-haul truck movements across Brazil, Argentina, and Chile. Brazil's trucking sector alone handles more than 60% of domestic cargo and now demands premium engine and transmission oils that enable extended drain intervals and fuel economy gains. Harvest cycles for soy, corn, and copper further lift lubricant volumes during peak logistics seasons, locking in a short-term consumption surge that sustains baseline market growth.

Accelerated Deep-Water Energy and Power Activity in Brazil and Guyana Boosting Demand for High-Performance Drilling Fluids

Brazil's pre-salt fields and Guyana's Stabroek Block collectively require synthetic drilling muds, subsea gear oils, and hydraulic fluids capable of withstanding extreme temperatures and 2,000 m water depths. ExxonMobil's multiplatform program and Petrobras subsea boosting contracts exemplify the specialized service models that command premium pricing and deepen supplier-client technical ties.

Prolonged Fuel-Price Subsidies in Argentina Discouraging Premium-Lube Consumption

Subsidized pump prices reduce consumer motivation to purchase high-efficiency synthetics, locking many motorists into short-interval mineral oils and capping value growth in passenger-car motor oils. The subsidy system has historically favored volume over value, encouraging frequent oil changes with conventional mineral oils rather than extended-service premium products. This dynamic particularly affects the passenger vehicle segment, where cost-conscious consumers prioritize immediate savings over long-term engine protection and fuel economy benefits.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory Euro VI-Equivalent Emissions Phase-In (Brazil PROCONVE P-8) Driving Low-SAPS Engine-Oil Adoption

- Surge in Regional Soybean-Oil Biodiesel Blends Spurring Growth of Bio-Based Hydraulic Fluids

- Currency-Devaluation Risk Inflating Import Costs of PAO and Additive Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Engine oils retained 39.72% of the 2025 South America lubricants market share, but hydraulic fluids are poised for a 2.66% CAGR through 2031 as automation spreads in mining, agriculture, and renewables. Specialized hydraulics formulated from synthetic or bio-based stocks ensure oxidative stability and temperature resilience demanded by high-pressure systems. Transmission and gear oils gain from fleet modernization programs, whereas greases protect bearings in harsh marine and industrial environments.

Emissions mandates push engine oil upgrades toward Group III and synthetic blends, yet price sensitivity keeps mineral products relevant in older vehicles. Hydraulic-fluid demand benefits from renewable-energy build-outs, where biodegradable formulations are preferred for environmental compliance. Continuous research and development in additive chemistry allows regional blenders to position differentiated offerings in the South America lubricants market.

The South America Lubricants Report is Segmented by Product Type (Engine Oils, Transmission and Gear Oils, Hydraulic Fluids, Greases, and More), Base Oil (Mineral, Synthetic, Semi-Synthetic, and Bio-Based), End-User (Automotive, Heavy Equipment, Metallurgy and Metalworking, Power Generation, Marine and Offshore, and Other Industries), and Geography (Argentina, Brazil, Chile, Colombia, Peru, and Rest of South America).

List of Companies Covered in this Report:

- AMSOIL INC.

- BP plc (Castrol)

- Chevron Corporation

- Exxon Mobil Corporation

- FUCHS

- Gulf Oil International Ltd

- ICONIC

- Petrobras

- Petroliam Nasional Berhad (PETRONAS)

- Repsol

- Shell plc

- Terpel

- TotalEnergies

- YPF

- ZF Friedrichshafen AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Strong rebound in on-road freight mileage post-COVID

- 4.2.2 Accelerated deep-water energy and power activity in Brazil and Guyana boosting demand for high-performance drilling fluids

- 4.2.3 Mandatory Euro VI-equivalent emissions phase-in (Brazil PROCONVE P-8) driving low-SAPS engine-oil adoption

- 4.2.4 Surge in regional soybean-oil biodiesel blends spurring growth of bio-based hydraulic fluids

- 4.2.5 Rapid automation of mining fleets in Chile and Peru requiring long-drain synthetic gear oils.

- 4.3 Market Restraints

- 4.3.1 Prolonged fuel-price subsidies in Argentina discouraging premium-lube consumption

- 4.3.2 Currency-devaluation risk inflating import costs of PAO and additive packages

- 4.3.3 Rising penetration of EV two-wheelers in urban centers eroding motorcycle-oil volumes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Engine Oils

- 5.1.2 Transmission and Gear Oils

- 5.1.3 Hydraulic Fluids

- 5.1.4 Greases

- 5.1.5 Metalworking Fluids

- 5.1.6 Process Oils and Others

- 5.2 By Base Oil

- 5.2.1 Mineral

- 5.2.2 Synthetic (PAO, Esters, PAG)

- 5.2.3 Semi-synthetic

- 5.2.4 Bio-based

- 5.3 By End-User Industry

- 5.3.1 Automotive

- 5.3.2 Heavy Equipment

- 5.3.3 Metallurgy and Metalworking

- 5.3.4 Power Generation

- 5.3.5 Marine and Offshore

- 5.3.6 Other Industries

- 5.4 By Country

- 5.4.1 Argentina

- 5.4.2 Brazil

- 5.4.3 Chile

- 5.4.4 Colombia

- 5.4.5 Peru

- 5.4.6 Rest of South America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)**/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 AMSOIL INC.

- 6.4.2 BP plc (Castrol)

- 6.4.3 Chevron Corporation

- 6.4.4 Exxon Mobil Corporation

- 6.4.5 FUCHS

- 6.4.6 Gulf Oil International Ltd

- 6.4.7 ICONIC

- 6.4.8 Petrobras

- 6.4.9 Petroliam Nasional Berhad (PETRONAS)

- 6.4.10 Repsol

- 6.4.11 Shell plc

- 6.4.12 Terpel

- 6.4.13 TotalEnergies

- 6.4.14 YPF

- 6.4.15 ZF Friedrichshafen AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

拉丝润滑剂市场:2026-2032年全球市场预测(依产品类型、添加剂类型、线材类型、应用、终端用户产业和销售管道划分)外科润滑剂市场:按类型、应用、最终用户和分销管道划分-2026-2032年全球市场预测

拉丝润滑剂市场:2026-2032年全球市场预测(依产品类型、添加剂类型、线材类型、应用、终端用户产业和销售管道划分)外科润滑剂市场:按类型、应用、最终用户和分销管道划分-2026-2032年全球市场预测 2026年全球润滑油市场报告润滑油市场:按产品类型、基础油、黏度等级、最终用户和分销管道分類的全球市场预测,2026-2032年大豆油基润滑剂市场:2026-2032年全球市场预测(依产品类型、包装、应用、终端用户产业及通路划分)纺织润滑剂市场:依产品类型、剂型、应用及最终用途划分-2026年至2032年全球预测金属切削润滑剂市场:依产品类型、金属类型、应用、终端用户产业和通路划分-2026-2032年全球预测

2026年全球润滑油市场报告润滑油市场:按产品类型、基础油、黏度等级、最终用户和分销管道分類的全球市场预测,2026-2032年大豆油基润滑剂市场:2026-2032年全球市场预测(依产品类型、包装、应用、终端用户产业及通路划分)纺织润滑剂市场:依产品类型、剂型、应用及最终用途划分-2026年至2032年全球预测金属切削润滑剂市场:依产品类型、金属类型、应用、终端用户产业和通路划分-2026-2032年全球预测 润滑油过滤器市场规模、份额和成长分析:按过滤器类型、应用、材质、最终用户和地区划分 - 2026-2033 年产业预测

润滑油过滤器市场规模、份额和成长分析:按过滤器类型、应用、材质、最终用户和地区划分 - 2026-2033 年产业预测 2026-2034年全球纱线润滑剂市场规模、份额、趋势和成长分析报告

2026-2034年全球纱线润滑剂市场规模、份额、趋势和成长分析报告 玻璃润滑剂市场规模、份额和成长分析:按润滑剂基础类型、配方类型、应用方法、包装类型、最终用户产业和地区划分-2026-2033年产业预测

玻璃润滑剂市场规模、份额和成长分析:按润滑剂基础类型、配方类型、应用方法、包装类型、最终用户产业和地区划分-2026-2033年产业预测