|

市场调查报告书

商品编码

1937400

东南亚咨询服务:市场占有率分析、产业趋势与统计、成长预测(2026-2031)South-East Asia Consulting Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

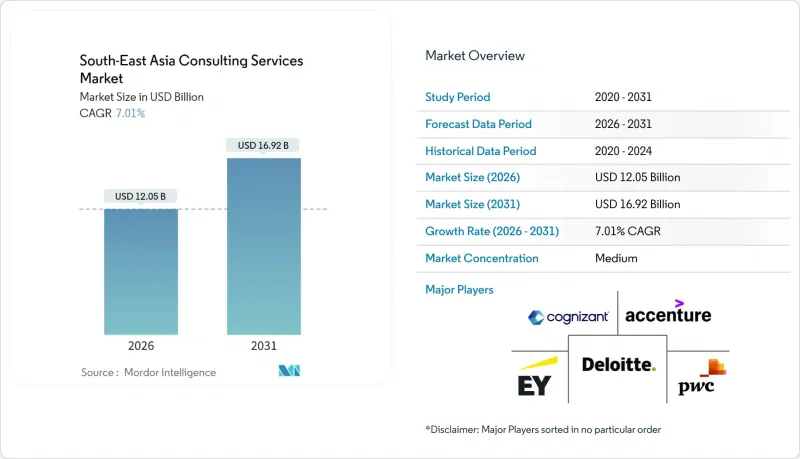

预计到 2026 年,东南亚咨询服务市场规模将达到 120.5 亿美元。

这意味着从 2025 年的 112.6 亿美元成长到 2031 年的 169.2 亿美元,2026 年至 2031 年的复合年增长率为 7.01%。

推动东协十国咨询需求的关键因素包括:政府主导的强有力的数位化蓝图、强制性的永续发展报告以及中小企业的快速发展。企业竞相升级旧有应用程式并整合人工智慧平台,因此在IT和数位化咨询上投入大量资金。同时,透明环境资讯揭露的推动也带动了对永续发展和ESG咨询的需求。此外,为了满足客户的持续需求,收入週期也在进行重组,从一次性计划转向基于订阅的咨询模式。利用云端原生交付和独立人才平台的专业顾问公司正在价格和敏捷性方面挑战传统企业。此外,「中国+1」供应链的重组正推动製造业向越南、泰国和马来西亚转移,催生了对跨境监管服务的需求。

东南亚咨询服务市场趋势与洞察

数位优先转型计划

新加坡的智慧国家计画和马来西亚的数位投资局等政府项目,全部区域的转型计划投入总计480亿美元。印尼计画将27,000个公共部门应用程式整合为9个超级应用程序,这凸显了变革管理、网路安全和云端迁移的复杂性,而这些都需要专家咨询。新加坡的Analytics.gov平台目前为超过1600个公共部门使用者提供支持,凸显了资料管治、人工智慧模型建构和多机构流程协调所需的咨询工作的重要性。泰国电力局采用PLEXOS进行电网优化,显示能源产业对资源规划咨询的需求日益增长。这些倡议表明,企业架构、管治和员工技能发展的多年合约为何是东南亚咨询服务市场稳定的收入来源。

小型企业和Start-Ups的快速成长需要扩充性的建议

占东协企业总数97%的中小微型微企业(MSMEs)面临3,000亿美元的资金缺口,促使各国政府和援助机构补贴获得咨询服务。 [HSBC.COM] 远低于传统每日350至1500美元收费标准的订阅模式已广受欢迎,使企业家能够以每日250至1600美元的价格获得独立专家的按需指导。越南的创投生态系统得到了InnoVen Capital 190笔融资的支持,显示高成长型Start-Ups对资金筹措、单位经济效益和打入市场策略咨询的需求旺盛。诸如东协社会企业发展计画4.0等机构计画提供培训和高达4万美元的种子津贴,进一步扩大了咨询基本客群。随着创办人将永续盈利放在首位,对具备资本效率和 ESG 整合专业知识的顾问的需求不断增长,从而增强了东南亚咨询服务市场的长期成长势头。

扩大内部咨询部门

像星展银行这样的金融机构正在组建内部数位转型团队,以减少对外部顾问在日常分析、网路安全和DevOps任务方面的依赖。这些专业团队拥有丰富的组织知识,并与企业文化紧密契合,其执行速度正日益达到甚至超过外部顾问的水平。随着越来越多的公司采用这种模式,一些常规咨询职能被纳入内部,导致商品化服务带来的收入成长放缓。然而,复杂的多市场转型、陌生的监管变化以及独立的董事会审核仍然需要外部的客观性,因此对高附加价值工作的需求仍然存在。咨询公司正透过深化专业化并提供难以由内部团队复製的、基于绩效的咨询服务来应对这一需求。

细分市场分析

到了2025年,IT和数位化顾问将占总营收的37.02%,这凸显了企业迫切需要逐步淘汰传统技术堆迭、采用云端原生架构并部署人工智慧工作负载。在超大规模云端投资和公共部门数位化转型的推动下,东南亚地区该领域的咨询服务市场规模预计将稳定成长。永续发展和ESG咨询将以17.55%的复合年增长率成长,这得益于新加坡2025年ESG报告强制令以及泰国SET ESG评级体系更名以与富时罗素标准接轨。随着客户对整合数位化和ESG的蓝图的需求日益增长,企业正在对技术人员进行碳核算框架的交叉培训。策略和营运咨询正受益于製造业「中国+1」策略转型,而风险和合规顾问则正利用资料本地化方法各异导致的部署架构碎片化问题获利。儘管有 30-70% 的技术职缺,但人力资源咨询依然强劲,推动了人才分析和劳动力规划计划。

顾问公司正将人工智慧助理融入交付流程,以实现文件审核和情境建模的自动化,从而缩短迭代周期并提高咨询利润率。像Tact Social Consulting这样的公司已与超大规模资料中心业者云端服务供应商合作,将云端积分与ESG咨询服务捆绑销售,并在泰国赢得了企业试点计画。随着以结果为基础的收费系统模式取代按小时计费模式,服务提供者正透过成本节约、风险缓解或碳减排指标来量化价值——这种方法引起了追求透明度的财务长们的共鸣。在东南亚咨询服务市场,儘管永续发展工作激增,但预计到2031年,数位化咨询收入的份额仍将维持在35%以上。这表明,融合技术和ESG需求的双管齐下成长模式将持续存在。

到2025年,金融服务业将占总支出的27.05%,这主要得益于全面的数位银行蓝图、开放的API支援以及严格的反洗钱措施。泰国开泰银行(KBank)旗下的KBTG以及越南MSB与Backbase的合作项目,都是机构投资全通路平台和人工智慧驱动的信贷引擎的典型案例。能源和公共产业行业将以14.06%的复合年增长率实现最快增长,这主要得益于电网现代化和可再生能源併网计划,例如泰国的PLEXOS部署和印尼东爪哇首个数位化变电站。随着电子和汽车公司重组供应链,製造业咨询的需求正在激增。同时,通讯业者正将高价值资本支出集中在5G和资料中心扩建,吸引了对基础设施咨询服务的需求。

随着印尼九大超级应用的整合,政府和公共部门的交易激增,推动了对专案管理办公室、网路安全和服务设计等领域专业知识的需求。在零售和电子商务领域,由于预计到2025年行动钱包帐户数量将达到4.4亿,客户体验重塑和诈欺分析成为关注焦点。医疗保健提供者正在向云端迁移,以缩短理赔处理时间并改善患者分诊,这为符合HIPAA标准的替代解决方案和旧有系统退役创造了咨询机会。这些领域的共同作用,维持了强劲的交易管道,再次巩固了东南亚咨询服务市场作为新兴亚洲经济体咨询业务中心的地位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场洞察

- 市场概览

- 市场驱动因素

- 数位优先转型计划

- 小型企业和Start-Ups的快速成长正在推动扩充性咨询服务的需求。

- 人工智慧、分析和云端平台采用

- 政府数位经济蓝图及外国直接投资流入

- 强制性ESG报告推动永续性咨询

- 中国+1供应链重组及东协的转型

- 市场限制

- 建立内部咨询部门

- 产品同质化导致价格下降

- 双语专家短缺

- 数据主权和居住限制

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

- 产业生态系分析

- 主要用例和案例研究

- 宏观经济趋势评估

- 投资分析

第五章 市场规模与成长预测

- 按服务类型

- 人力资源咨询

- 财务咨询

- IT与数位咨询

- 策略与商业咨询

- 风险与合规咨询

- 永续发展与ESG咨询

- 按最终用户行业划分

- 金融服务

- 生命科学与医疗保健

- IT/通讯

- 政府/公共部门

- 能源与公共产业

- 製造业

- 零售与电子商务

- 依咨询类型

- 企划为基础的咨询

- 咨询合约类型:咨询

- 託管服务/外包

- 咨询服务(订阅制)

- 按公司规模

- 中小企业

- 大公司

- 按国家/地区

- 新加坡

- 印尼

- 泰国

- 越南

- 菲律宾

- 马来西亚

- 东南亚及其他地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers International Limited(PwC)

- Ernst and Young Global Limited

- KPMG International Limited

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Bain & Company, Inc.

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Mercer LLC

- Aon plc

- Protiviti Inc.

- AT Kearney, Inc.

- Roland Berger Holding GmbH

- LEK Consulting LLC

- Frost & Sullivan, Inc.

- RSM International Limited

- YCP Holdings Limited

第七章 市场机会与未来展望

The South-East Asia consulting services market size in 2026 is estimated at USD 12.05 billion, growing from 2025 value of USD 11.26 billion with 2031 projections showing USD 16.92 billion, growing at 7.01% CAGR over 2026-2031.

Robust government-led digitalization roadmaps, mandatory sustainability reporting, and rapid SME formation are the primary forces expanding advisory demand across the ten ASEAN member states. Enterprises racing to modernize legacy applications and integrate AI platforms are channeling the largest spending into IT and Digital Consulting, while the push for transparent environmental disclosures propels Sustainability and ESG advisory uptake. Concurrently, a pivot from episodic projects to subscription-based advisory models is reshaping revenue cycles as clients favor continuous support. Boutiques leveraging cloud-native delivery and independent talent platforms now challenge incumbents on price and agility, while China+1 supply-chain realignment sends manufacturers to Vietnam, Thailand, and Malaysia, unlocking cross-border regulatory workstreams.

South-East Asia Consulting Services Market Trends and Insights

Digital-first Transformation Programmes

Government programmes such as Singapore's Smart Nation initiative and Malaysia's Digital Investment Office are collectively injecting USD 48 billion into regional transformation projects . Indonesia's plan to merge 27,000 public-sector apps into nine super-apps exemplifies the complexity of change management, cybersecurity, and cloud migration tasks that demand specialized advice. Singapore's Analytics.gov platform, now supporting more than 1,600 public-sector users, highlights the consultative work required to govern data, build AI models, and align multi-agency processes. Thailand's electricity authority chose PLEXOS for grid optimization, signaling rising need for resource-planning advisory across energy utilities. Together these initiatives demonstrate why multi-year engagements around enterprise architecture, governance, and talent upskilling form a resilient revenue stream for the South-East Asia consulting services market.

SME and Start-up Boom Demanding Scalable Advice

Ninety-seven percent of ASEAN businesses are MSMEs, and they face a USD 300 billion funding deficit, prompting governments and donors to subsidize advisory access [HSBC.COM]. Subscription models priced well below the traditional USD 350-1,500 daily rate are gaining ground, enabling founders to secure on-call guidance using independent experts billing USD 250-1,600 per day. Vietnam's venture ecosystem, supported by InnoVen Capital's 190 loans, illustrates the appetite for fundraising, unit economics, and go-to-market consulting among high-growth startups. Institutional programs such as the ASEAN Social Enterprise Development Programme 4.0 supply training and seed grants up to USD 40,000, further widening the advisory client base. As founders prioritize sustainable profitability, demand rises for consultants versed in capital efficiency and ESG integration, reinforcing long-term momentum for the Southeast Asia consulting services market.

Corporate In-house Consulting Build-outs

Financial institutions such as DBS have cultivated internal digital-transformation squads, reducing dependence on third-party advisors for day-to-day analytics, cybersecurity, and DevOps mandates. These captive units accumulate institutional knowledge and align tightly with corporate culture, often matching or outpacing external consultants on speed of execution. As more enterprises replicate the model, a portion of routine advisory spend migrates in-house, trimming revenue growth for commoditized services. However, complex multi-market transformations, unfamiliar regulatory changes, and independent board-mandated reviews still require external objectivity, preserving scope for high-value engagements. Consulting firms are responding by deepening specialization and offering outcome-based contracts that internal teams struggle to replicate.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of AI, Analytics and Cloud Platforms

- Government Digital-Economy Road-maps and FDI Inflows

- Price Erosion from Commoditized Offerings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

IT and Digital Consulting contributes 37.02% of 2025 revenue, underscoring enterprise urgency to decommission legacy stacks, adopt cloud-native architectures, and deploy AI workloads. The Southeast Asia consulting services market size for this segment is forecast to expand steadily alongside hyperscale cloud investments and public-sector digital mandates. Sustainability and ESG Consulting, growing at an 17.55% CAGR, gains momentum from Singapore's 2025 compulsory ESG reporting and Thailand's re-branded SET ESG Ratings that align with FTSE Russell standards . Clients increasingly demand integrated digital-plus-ESG roadmaps, prompting firms to cross-train technologists in carbon-accounting frameworks. Strategy and Operations Consulting benefits from manufacturers' China+1 shifts, while Risk and Compliance advisors capitalize on divergent data-localization laws that fragment deployment architectures. HR Consulting remains resilient as 30-70% of tech roles sit vacant, driving projects in talent analytics and workforce planning.

Consultancies now embed AI copilots into delivery, automating document review and scenario modeling, thus shortening sprint cycles and elevating advisory margins. Firms like Tact Social Consulting partner with hyperscalers to bundle cloud credits with ESG advisory, winning enterprise pilots across Thailand. As output-based fees displace billable-hour models, providers quantify value via cost savings, risk mitigation, or carbon-reduction metrics, an approach that resonates with CFOs seeking transparency. The South-East Asia consulting services market share of digital advisory revenue is projected to hold above 35% through 2031 despite the surge in sustainability work, indicating a durable dual-track growth pattern that fuses technology and ESG imperatives.

Financial Services represented 27.05% of 2025 spending, anchored by exhaustive digital banking roadmaps, open-API compliance, and stringent anti-money-laundering rules. KBank's KBTG unit and Vietnam's MSB-Backbase partnership are emblematic of institutions investing in omnichannel platforms and AI-enabled credit engines. Energy and Utilities produces the fastest expansion at 14.06% CAGR, fueled by grid modernization and renewable-integration projects such as Thailand's PLEXOS deployment and Indonesia's first digital substation in East Java. Manufacturing consulting demand swells as electronics and automotive firms replot supply chains, while telecom operators channel big-ticket capex into 5G and data-center buildouts, attracting infrastructure advisory.

Government and Public Sector engagements escalate with Indonesia's nine-super-app consolidation, pushing requirements for program management offices, cybersecurity, and service-design expertise. Retail and E-commerce assignments focus on customer-journey redesign and fraud analytics as mobile wallets multiply to an expected 440 million accounts by 2025. Healthcare providers pursue cloud migrations to compress claims-processing times and improve patient triage, opening avenues for HIPAA-analog compliance and legacy-system decommissioning consulting. Collectively, these verticals sustain a robust pipeline, reaffirming the South-East Asia consulting services market as the advisory hotspot within emerging Asian economies.

The Southeast Asia Consulting Services Market Report is Segmented by Service Type (HR Consulting, Financial Consulting, and More), End-User Industry (Financial Services, Life Sciences and Healthcare, IT and Telecommunications, and More), Consulting Model (Project-Based Advisory, Retainer-Based Advisory, and More), Firm Size (SMEs, and Large Enterprises), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Deloitte Touche Tohmatsu Limited

- PricewaterhouseCoopers International Limited (PwC)

- Ernst and Young Global Limited

- KPMG International Limited

- McKinsey & Company, Inc.

- Boston Consulting Group, Inc.

- Bain & Company, Inc.

- Cognizant Technology Solutions Corporation

- Tata Consultancy Services Limited

- Wipro Limited

- Mercer LLC

- Aon plc

- Protiviti Inc.

- A.T. Kearney, Inc.

- Roland Berger Holding GmbH

- L.E.K. Consulting LLC

- Frost & Sullivan, Inc.

- RSM International Limited

- YCP Holdings Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Digital-first transformation programmes

- 4.2.2 SME and start-up boom demanding scalable advice

- 4.2.3 Adoption of AI, analytics and cloud platforms

- 4.2.4 Government digital-economy road-maps and FDI inflows

- 4.2.5 Mandatory ESG-reporting fuelling sustainability advisory

- 4.2.6 China+1 supply-chain realignment into ASEAN

- 4.3 Market Restraints

- 4.3.1 Corporate in-house consulting build-outs

- 4.3.2 Price erosion from commoditised offerings

- 4.3.3 Shortage of bilingual domain experts

- 4.3.4 Data-sovereignty and residency barriers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Industry Ecosystem Analysis

- 4.9 Key Use Cases and Case Studies

- 4.10 Assessment of Macroeconomic Trends

- 4.11 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Service Type

- 5.1.1 HR Consulting

- 5.1.2 Financial Consulting

- 5.1.3 IT and Digital Consulting

- 5.1.4 Strategy and Operations Consulting

- 5.1.5 Risk and Compliance Consulting

- 5.1.6 Sustainability and ESG Consulting

- 5.2 By End-user Industry

- 5.2.1 Financial Services

- 5.2.2 Life Sciences and Healthcare

- 5.2.3 IT and Telecommunications

- 5.2.4 Government and Public Sector

- 5.2.5 Energy and Utilities

- 5.2.6 Manufacturing

- 5.2.7 Retail and E-commerce

- 5.3 By Consulting Model

- 5.3.1 Project-based Advisory

- 5.3.2 Retainer-based Advisory

- 5.3.3 Managed Services / Outsourcing

- 5.3.4 Advisory-as-a-Service (Subscription)

- 5.4 By Firm Size

- 5.4.1 Small and Medium Enterprises (SMEs)

- 5.4.2 Large Enterprises

- 5.5 By Country

- 5.5.1 Singapore

- 5.5.2 Indonesia

- 5.5.3 Thailand

- 5.5.4 Vietnam

- 5.5.5 Philippines

- 5.5.6 Malaysia

- 5.5.7 Rest of Southeast Asia

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Deloitte Touche Tohmatsu Limited

- 6.4.3 PricewaterhouseCoopers International Limited (PwC)

- 6.4.4 Ernst and Young Global Limited

- 6.4.5 KPMG International Limited

- 6.4.6 McKinsey & Company, Inc.

- 6.4.7 Boston Consulting Group, Inc.

- 6.4.8 Bain & Company, Inc.

- 6.4.9 Cognizant Technology Solutions Corporation

- 6.4.10 Tata Consultancy Services Limited

- 6.4.11 Wipro Limited

- 6.4.12 Mercer LLC

- 6.4.13 Aon plc

- 6.4.14 Protiviti Inc.

- 6.4.15 A.T. Kearney, Inc.

- 6.4.16 Roland Berger Holding GmbH

- 6.4.17 L.E.K. Consulting LLC

- 6.4.18 Frost & Sullivan, Inc.

- 6.4.19 RSM International Limited

- 6.4.20 YCP Holdings Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

咨询4.0市场:2026-2032年全球预测(依产品类型、技术、应用、最终用户及通路划分)企业敏捷转型服务市场:2026-2032年全球市场预测(依服务类型、调查方法、转型阶段、合约模式、部署模式、产业及组织规模划分)

咨询4.0市场:2026-2032年全球预测(依产品类型、技术、应用、最终用户及通路划分)企业敏捷转型服务市场:2026-2032年全球市场预测(依服务类型、调查方法、转型阶段、合约模式、部署模式、产业及组织规模划分) 2026年全球IT咨询市场报告2026年全球企业敏捷转型服务市场报告

2026年全球IT咨询市场报告2026年全球企业敏捷转型服务市场报告 企业敏捷转型服务市场规模、份额、趋势和预测:按方法论、服务类型、组织规模、产业和地区划分,2026-2034 年2026年全球公司秘书服务市场报告2026年全球房地产咨询服务市场报告2026年全球精算咨询服务市场报告2026年全球设计、研究、促销与咨询服务市场报告

企业敏捷转型服务市场规模、份额、趋势和预测:按方法论、服务类型、组织规模、产业和地区划分,2026-2034 年2026年全球公司秘书服务市场报告2026年全球房地产咨询服务市场报告2026年全球精算咨询服务市场报告2026年全球设计、研究、促销与咨询服务市场报告 2026-2030年全球行销咨询市场

2026-2030年全球行销咨询市场