|

市场调查报告书

商品编码

1937426

气煞车系统:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Air Brake System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

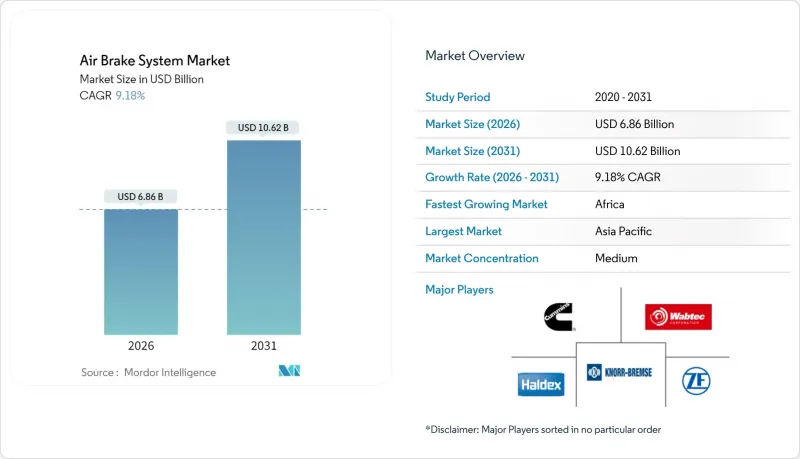

2025年全球空气煞车系统市场价值为62.8亿美元,预计到2031年将达到106.2亿美元,而2026年为68.6亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 9.18%。

监管因素,例如美国环保署 (EPA) 针对重型车辆自 2027 年车型起实施的第三阶段温室气体排放法规,正在加速原始设备製造商 (OEM) 对电控气动架构的投资,以支援柴油和零排放动力系统。高级驾驶辅助系统 (ADAS) 的整合不断提升了对精准煞车性能的需求,迫使供应商开发与自动紧急煞车 (AEB) 功能对接的电控系统(ECU) 和感测器套件。压缩机的重新设计正从引擎驱动转向电力驱动,从而降低寄生损耗,并为氢燃料电池和纯电动车提供支援。这些技术转折点,加上车队对降低总拥有成本 (TCO) 的需求,正在重塑全部区域的竞争动态,使采购偏好转向长途运输应用中的碟式煞车或混合动力配置。

全球空气煞车系统市场趋势与洞察

可电气化的气动架构

汽车製造商正在重新设计煞车系统,以实现气动迴路与电池电动和氢燃料电池动力系统的无缝整合。采埃孚(ZF)已获得约500万辆汽车的线控刹车硬体安装订单,证明了大规模部署的可行性,并为车队提供了一条即时实现能量回收煞车的途径。加拿大政府对VMAC高压压缩机计画的支持,反映了加拿大对电动辅助零件的重视。电动压缩机消除了曲轴阻力,从而提高了续航里程并降低了碳排放强度。同时,整合的温度控管软体协调能量回收制动和摩擦制动,以避免在频繁制动过程中产生热量积聚。随着这些系统从欧洲试点车队走向全球量产,那些掌握模组化电动压缩机平台的供应商将透过持续的软体更新,在整个气动煞车系统市场获得稳定的收入来源。

推动制定零排放重型卡车法规

美国环保署 (EPA) 的第三阶段标准旨在到 2032 年将 8 级卡车的二氧化碳排放减少 25%,并与加州的先进清洁卡车奖励相结合,迫使製造商重新设计气动系统以实现无油运行。欧盟 (EU) 的二氧化碳排放标准也有类似的目标,并包含合规激励措施,奖励配备节能煞车系统的车辆。供应商被要求用干式运转装置替换润滑压缩机,同时扩大储气容量以应对电能再生循环引起的需求波动。长达十年的监管政策明确性推动了车队对氢燃料原型车的预订,并促进了空气煞车系统市场采用即使在低运作循环下也能保持精确压力的电控气动空气阀。

气剎管路和阀门的维护成本高昂

电子控制阀门和感测器的普及推高了维修费用,尤其对于缺乏校准诊断工具的车队而言更是如此。克诺尔集团预计,到2024年,售后市场收入将占其商用车销售额的30.1%,凸显了服务需求的成长(knorr-bremse.com)。本迪克斯的ACom AE工具可为全球可扩展的空气处理模组提供故障码迭加显示,但技术人员需要获得新的认证,这限制了其在新兴经济体的普及率。此外,诸如高规格尼龙软管、油水分离滤芯和韧体许可费等持续性成本,也限制了气煞车系统市场的近期成长。

细分市场分析

到2025年,气鼓式煞车将占据气煞车系统市场45.78%的份额,这反映了其成本效益和广泛认可。随着美国国家公路交通安全管理局(NHTSA)收紧煞车距离法规,碟式煞车在长途牵引车领域取得了进展,但其绝对销量仍低于鼓式煞车。电控气动子细分市场虽然目前规模较小,但正以8.55%的复合年增长率快速成长,因为自动紧急煞车(AEB)、车道维持辅助和车队行驶测试都需要毫秒级的压力控制。混合式鼓盘配置填补了车队的一个过渡市场空白,这些车队需要在转向轴上采用碟式煞车的性能,而在传动轴上则使用低维护成本的鼓式煞车。精确控制设备可降低15%的空气消耗,这推动了需要节省辅助能源的纯电动底盘对电控气动解决方案的兴趣,并提升了其在整个气动系统产业的重要性。

传统的鼓式煞车平台也在不断发展。大型铸铁零件製造商正在加工轻量化的轮毂,以抵消桶形设计为节省燃油而增加的重量。同时,碟式煞车的支持者则强调转子偏移设计和螺栓式卡钳模组,以加快煞车片的更换速度,并声称每个车轮端可减少25%的工时。预计从2026年到2031年,配备电子间隙调节感测器的改装套件将提升售后市场收入,从而促进数据分析的交叉销售,以预测煞车片的磨损情况。儘管这种相互作用表明两者将保持平衡共存,但在本世纪下半叶,随着价值向软体辅助碟式煞车和电控气动煞车转移,空气煞车系统市场仍将处于不断变化之中。

到2025年,轻型商用车将占据空气煞车系统市场34.88%的最大份额,这主要得益于都市区配送的成长,尤其是在亚洲的电商走廊地区。频繁的启停循环需要快速的压力恢復,因此整车製造商倾向于采用双级压缩机搭配模组化空气干燥器。虽然重型卡车的销量目前较低,但预计其复合年增长率将达到7.52%,因为零排放目标要求使用无油压缩机、冗余ECU和高精度压力感测器。该细分市场也是技术创新的温床。戴姆勒的600kWh eActros 600将再生煞车与摩擦煞车结合,迫使供应商根据电池的充电状态来微调气压阈值。

刚性工程车辆和自动卸货卡车通常在多尘、高磨损的环境中运作,这会缩短碟式密封件的使用寿命,因此自调节鼓式煞车组件至关重要。巴士和长途客车优先考虑乘客的舒适性和安全性,采用电控气动控制系统来最大限度地减少紧急煞车时的车辆摇摆。非公路车辆和矿用车辆需要额定压力超过 30 巴的双迴路气室以及能够承受泥浆侵入的密封式间隙调节器。随着应用场景在各类车辆中的扩展,产品系列必须保持模组化,以在气煞车系统市场因运作週期和监管要求而日益多元化的情况下,保障利润率。

区域分析

到2025年,亚太地区将占据全球空气煞车系统市场44.83%的份额,这主要得益于中国强大的商用车生产能力和印度大规模的高速公路现代化。中国整车製造商正快速整合电子控制单元(ECU)和干式压缩机,以实现其2030年的电气化目标;同时,日本一级供应商则为预测性维护仪表板提供精密感测器。在东南亚,热带气候为碟式煞车的冷却带来了挑战,促使供应商和当地组装开展联合开发项目,以客製化转子涂层和通风口形状。

儘管非洲的卡车市场基数小规模,但由于快速的都市化、采矿业的扩张以及泛非贸易走廊的发展,预计到2031年,非洲卡车市场将以9.88%的复合年增长率增长。这些发展都需要具备可靠煞车性能的现代化卡车。南非和奈及利亚在监管协调方面处于主导,正逐步提高煞车性能标准,以符合ECE R13法规。高温环境下碟煞热衰减的担忧延缓了先进煞车系统的应用,但肯亚的测试车队正在试用一种鼓盘混合煞车系统,并结合水刀冷却罩来缓解温度骤升的问题。

北美和欧洲的需求模式成熟且技术密集。美国环保署第三阶段排放标准和欧盟零排放法规正在推动向电控气动线控线控刹车架构的转变,从而推高了价格。随着更严格的自动紧急煞车(AEB)和车道偏离预防法规应用于在运作中车辆,改装市场仍然保持活跃,确保了持续的收入。儘管2024年铸铁鼓和阀门供应链的供不应求依然存在,但墨西哥和东欧的产能扩张正在缓解这一瓶颈。因此,预计这三个经济体的空气煞车系统市场将反映出区域政策的严格程度、技术成熟度和气候变迁因素。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 可电气化的气动架构

- 推动制定零排放重型卡车法规

- 由于高级驾驶辅助系统(ADAS)的广泛应用,对高精度煞车的需求增加。

- 车队对将气煞车系统更换为碟式煞车系统的需求,旨在降低总拥有成本。

- 智慧压缩机与远端资讯处理系统的集成

- 氢燃料电池卡车计画对无油空气供应的需求

- 市场限制

- 气剎管路和阀门的维护成本高昂

- 热带气候下碟式煞车的热衰减问题。

- 铸铁零件供应链的紧密性

- 电子控制煞车系统中的网路安全风险

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争强度

第五章 市场规模与成长预测

- 按煞车类型

- 鼓式气煞车

- 碟式气煞车

- 混合式鼓/碟系统

- 电控气动型(E-PBS)

- 按车辆类型

- 轻型商用车

- 中型卡车

- 大型卡车

- 公车和长途客车

- 非公路和矿用卡车

- 按组件

- 压缩机

- 调压阀

- 储存槽

- 鬆弛调整器

- 煞车分泵

- 电控系统/感测器

- 按销售管道

- OEM

- 售后市场

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 荷兰

- 瑞典

- 波兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 印尼

- 泰国

- 越南

- 菲律宾

- 亚太其他地区

- 中东

- 土耳其

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 埃及

- 肯亚

- 摩洛哥

- 阿尔及利亚

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ZF Friedrichshafen AG

- Knorr-Bremse AG

- Wabtec(WABCO)Corp.

- Haldex AB

- Cummins Inc.(Meritor Inc.)

- Nabtesco Corp.

- Bendix CVS LLC

- TSE Brakes Inc.

- SORL Auto Parts Inc.

- Brakes India Ltd.

- Continental AG

- Federal-Mogul Motorparts

- Bendix Commercial Vehicle Systems LLC

第七章 市场机会与未来展望

The global Air Brake Systems market was valued at USD 6.28 billion in 2025 and estimated to grow from USD 6.86 billion in 2026 to reach USD 10.62 billion by 2031, at a CAGR of 9.18% during the forecast period (2026-2031).

Regulatory catalysts such as the United States Environmental Protection Agency's Phase 3 greenhouse-gas standards for heavy-duty vehicles, which begin with model year 2027, are accelerating OEM investment in electropneumatic architectures supporting diesel and zero-emission powertrains. Integration of advanced driver assistance systems (ADAS) has further raised precision-braking requirements, pushing suppliers to develop electronic control units (ECUs) and sensor suites that synchronize with automatic emergency braking (AEB) functionality. Compressor redesign shifting from engine-driven to electric cuts parasitic losses and readies vehicles for hydrogen fuel-cell or battery-electric operation. These technology inflections, coupled with fleet demand for lower total cost of ownership, are reshaping competitive dynamics and tipping procurement choices toward disc-brake or hybrid configurations in long-haul applications across every major air brake systems market region.

Global Air Brake System Market Trends and Insights

Electrification-Ready Pneumatic Architectures

OEMs are re-engineering brake systems so the pneumatic circuit integrates seamlessly with battery-electric and hydrogen fuel-cell drivetrains. ZF secured orders to deploy brake-by-wire hardware across nearly 5 million vehicles, proving large-scale viability and giving fleets an immediate path to regenerative braking compatibility. Canada's support of VMAC's high-voltage compressor program signals national prioritization of electric auxiliary components. Electric compressors eliminate crankshaft drag, improving range and lowering carbon intensity, while integrated thermal-management software coordinates regenerative and friction braking to avoid heat buildup during repeated stops. As these systems migrate from pilot fleets in Europe to series production worldwide, suppliers that master modular electric compressor platforms will secure recurring software-update revenue streams throughout the air brake systems market.

Regulatory Push for Zero-Emission Heavy Trucks

The EPA's Phase 3 standards target a 25% reduction in carbon dioxide for Class 8 trucks by 2032 and dovetail with California's Advanced Clean Trucks regulation, forcing manufacturers to redesign pneumatic systems for oil-free operation. The European Union's CO2 standards echo these targets and embed compliance incentives that reward vehicles with energy-efficient braking. Suppliers must therefore substitute lubricated compressors with dry-running units while enlarging air-storage capacity to balance fluctuating demands from electric regenerative cycles. Regulatory clarity over a 10-year horizon encourages fleet pre-orders of hydrogen prototypes, pushing the air brake systems market toward faster adoption of electropneumatic valves that maintain precise pressure at lower duty cycles.

High Maintenance Cost of Air-brake Lines and Valves

The growing count of electronically modulated valves and sensors raises workshop bills, especially in fleets that lack calibrated diagnostic tools. Knorr-Bremse expanded aftermarket revenue to 30.1% of commercial-vehicle sales during 2024, highlighting rising service demand knorr-bremse.com. Bendix's ACom AE tool offers fault-code overlays for global scalable air-treatment modules, but technicians require new certifications, which limits adoption velocity in emerging economies. Higher-specification nylon hoses, moisture separation cartridges, and firmware licensing fees add recurring costs that temper the near-term growth of the air brake systems market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of ADAS Requires Higher-Precision Braking

- Fleet Demand for Total-Cost-of-Ownership Reduction Via Air-disc Conversion

- Disc-brake Heat-fade Issues in Tropical Climates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air drum brake designs retained 45.78% of the air brake systems market size in 2025, reflecting cost efficiency and widespread service familiarity. Disc variants penetrated long-haul tractors after NHTSA's stricter stopping-distance rule but still sit below drums in absolute volume. The electropneumatic subset, although only a fraction today, is growing fastest at an 8.55% CAGR as AEB, lane-keeping, and platooning pilots demand millisecond-level pressure modulation. Hybrid drum-disc configurations fill a transitional niche for fleets that want disc performance on steer axles yet still rely on lower-maintenance drums on drive axles. Because precision controllers can trim air consumption by 15%, electropneumatic solutions are drawing interest from battery-electric chassis that must conserve auxiliary energy, broadening their relevance across the air brake systems industry.

Traditional drum platforms are not standing still. Large cast-iron suppliers are machining weight-optimized webs to offset the barrel-shaped mass penalties that hamper fuel economy. Conversely, disc advocates emphasize rotor offset designs and bolt-on caliper modules that accelerate pad swaps, claiming 25% labor reduction per wheel end. From 2026 to 2031, retrofit kits featuring electronic slack-adjuster sensors are forecast to lift aftermarket revenue, enabling meaningful cross-selling of data analytics to predict lining wear. This interplay suggests a balanced coexistence, yet the value pool will migrate toward software-supported disc and electropneumatic variants, keeping the air brake systems market in flux for the rest of the decade.

Light commercial vehicles represented the largest 34.88% slice of the 2025 air brake systems market size, owing to urban delivery growth, especially in Asia's e-commerce corridors. Frequent stop-start duty cycles demand rapid pressure recovery, driving OEM preference for two-stage compressors paired with modular air-dryers. Though lower in unit sales, heavy-duty trucks are forecast to expand at 7.52% CAGR, underpinned by zero-emission targets that obligate oil-free compressors, redundant ECUs, and high-accuracy pressure sensors. The segment also acts as an innovation incubator: Daimler's 600 kWh eActros 600 adopts blended regenerative and friction braking, which forces suppliers to fine-tune air-pressure thresholds based on battery state of charge.

Rigid vocational vehicles and dump trucks often operate in dusty, abrasive environments that shorten disc-seal life, making a role for self-adjusting drum assemblies. Buses and coaches prioritize passenger comfort and safety, adopting electropneumatic logic that minimizes pitch during panic stops. Off-highway and mining haulers require high-capacity dual-circuit chambers rated beyond 30 bar, with sealed slack adjusters that withstand mud ingress. Broadening use-cases across every class ensures that product portfolios must remain modular, defending margins as the air brake systems market diversifies by duty cycle and regulatory overlay.

The Air Brake System Market is Segmented by Brake Type (Drum Air Brake, Disc Air Brake, Hybrid Drum-Disc Systems and More), Vehicle Type (Light Commercial Vehicles, Medium-Duty Trucks, Heavy-Duty Trucks, and More), Component (Compressor, Governor and Valves, Storage Tank, and More), Sales Channel (OEM, and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific controlled 44.83% of the air brake systems market in 2025, anchored by China's outsized commercial-vehicle production and India's sprawling highway modernization. Chinese OEMs are quickly integrating ECUs and dry compressors to backstop the country's 2030 electrification quotas, while Japanese tier-ones supply precision sensors that feed predictive-maintenance dashboards. In Southeast Asia, the tropical climate challenges disc-brake cooling, prompting joint-development programs between suppliers and local assemblers to customize rotor coatings and vent geometries.

Africa, though starting from a modest base, is forecast to post a 9.88% CAGR through 2031 thanks to rapid urbanization, mining-sector expansion, and pan-African trade corridors that demand modern trucks with reliable braking. South Africa and Nigeria are spearheading regulatory harmonization, gradually raising brake-performance standards to align with ECE R13 provisions. Disc-fade concerns under high ambient heat have slowed advanced-brake deployment, but pilot fleets in Kenya are trialing hybrid drum-disc setups paired with water-piqued cooling shields to mitigate temperature spikes.

North America and Europe exhibit mature but technology-intensive demand patterns. EPA Phase 3 and the EU's zero-emission mandates compel a shift toward electropneumatic brake-by-wire architectures, fostering premium pricing. The retrofit market remains vibrant because tightening AEB and lane-departure regulations apply to in-service vehicles, guaranteeing recurring revenue. Supply-chain kinks for cast-iron drums and valves were pronounced in 2024, yet capacity additions in Mexico and Eastern Europe are easing bottlenecks. Consequently, the air brake systems market will mirror regional policy stringency, technology readiness, and climate considerations across these three economic blocs.

- ZF Friedrichshafen AG

- Knorr-Bremse AG

- Wabtec (WABCO) Corp.

- Haldex AB

- Cummins Inc. (Meritor Inc.)

- Nabtesco Corp.

- Bendix CVS LLC

- TSE Brakes Inc.

- SORL Auto Parts Inc.

- Brakes India Ltd.

- Continental AG

- Federal-Mogul Motorparts

- Bendix Commercial Vehicle Systems LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification-ready pneumatic architectures

- 4.2.2 Regulatory push for zero-emission heavy trucks

- 4.2.3 Rising adoption of advanced driver-assistance systems (ADAS) requiring higher-precision braking

- 4.2.4 Fleet demand for total-cost-of-ownership reduction via air-disc conversion

- 4.2.5 Smart compressor integration with telematics (under-reported)

- 4.2.6 Hydrogen fuel-cell truck programs demanding oil-free air supply (under-reported)

- 4.3 Market Restraints

- 4.3.1 High maintenance cost of air-brake lines & valves

- 4.3.2 Disc-brake heat-fade issues in tropical climates

- 4.3.3 Supply-chain crunch for cast-iron components (under-reported)

- 4.3.4 Cyber-security risks in electronically controlled braking systems (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Brake Type

- 5.1.1 Drum Air Brake

- 5.1.2 Disc Air Brake

- 5.1.3 Hybrid Drum-Disc Systems

- 5.1.4 Electropneumatic (E-PBS)

- 5.2 By Vehicle Type

- 5.2.1 Light Commercial Vehicles

- 5.2.2 Medium-Duty Trucks

- 5.2.3 Heavy-Duty Trucks

- 5.2.4 Buses & Coaches

- 5.2.5 Off-Highway & Mining Trucks

- 5.3 By Component

- 5.3.1 Compressor

- 5.3.2 Governor & Valves

- 5.3.3 Storage Tank

- 5.3.4 Slack Adjuster

- 5.3.5 Brake Chamber

- 5.3.6 Electronic Control Unit & Sensors

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Netherlands

- 5.5.3.7 Sweden

- 5.5.3.8 Poland

- 5.5.3.9 Russia

- 5.5.3.10 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Indonesia

- 5.5.4.7 Thailand

- 5.5.4.8 Vietnam

- 5.5.4.9 Philippines

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Turkey

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Kenya

- 5.5.6.5 Morocco

- 5.5.6.6 Algeria

- 5.5.6.7 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 ZF Friedrichshafen AG

- 6.4.2 Knorr-Bremse AG

- 6.4.3 Wabtec (WABCO) Corp.

- 6.4.4 Haldex AB

- 6.4.5 Cummins Inc. (Meritor Inc.)

- 6.4.6 Nabtesco Corp.

- 6.4.7 Bendix CVS LLC

- 6.4.8 TSE Brakes Inc.

- 6.4.9 SORL Auto Parts Inc.

- 6.4.10 Brakes India Ltd.

- 6.4.11 Continental AG

- 6.4.12 Federal-Mogul Motorparts

- 6.4.13 Bendix Commercial Vehicle Systems LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

空气煞车系统市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球空气煞车系统市场规模、份额、趋势和成长分析报告(2026-2034年)

空气煞车系统市场规模、份额、成长及全球产业分析:按类型、应用和地区分類的洞察,2026-2034 年预测全球空气煞车系统市场规模、份额、趋势和成长分析报告(2026-2034年) 汽车煞车带市场 - 全球产业规模、份额、趋势、机会及预测(按变速箱类型、车辆类型、推进类型、需求类别、地区和竞争格局划分,2021-2031)汽车空气煞车系统市场 - 全球产业规模、份额、趋势、竞争格局、机会及预测(按车辆类型、零件类型、煞车类型、地区和竞争格局划分,2021-2031)

汽车煞车带市场 - 全球产业规模、份额、趋势、机会及预测(按变速箱类型、车辆类型、推进类型、需求类别、地区和竞争格局划分,2021-2031)汽车空气煞车系统市场 - 全球产业规模、份额、趋势、竞争格局、机会及预测(按车辆类型、零件类型、煞车类型、地区和竞争格局划分,2021-2031) 2026-2030年全球汽车间隙调节器市场

2026-2030年全球汽车间隙调节器市场 空气煞车系统市场规模、份额及成长分析(按类型、组件、车辆类型、分销管道及地区划分)-2026-2033年产业预测

空气煞车系统市场规模、份额及成长分析(按类型、组件、车辆类型、分销管道及地区划分)-2026-2033年产业预测 2032 年汽车间隙调整器市场预测:按类型、车辆类型、应用、最终用户和地区进行的全球分析

2032 年汽车间隙调整器市场预测:按类型、车辆类型、应用、最终用户和地区进行的全球分析 按技术、分销管道和应用分類的空气煞车系统市场—2025-2032年全球预测

按技术、分销管道和应用分類的空气煞车系统市场—2025-2032年全球预测 全球汽车间隙调整器市场

全球汽车间隙调整器市场 汽车用空气制动器系统的全球市场的评估:车辆类别,剎车类别,各技术类型,各地区,机会,预测(2018年~2032年)

汽车用空气制动器系统的全球市场的评估:车辆类别,剎车类别,各技术类型,各地区,机会,预测(2018年~2032年)