|

市场调查报告书

商品编码

1937438

氯气:市占率分析、产业趋势与统计、成长预测(2026-2031)Chlorine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

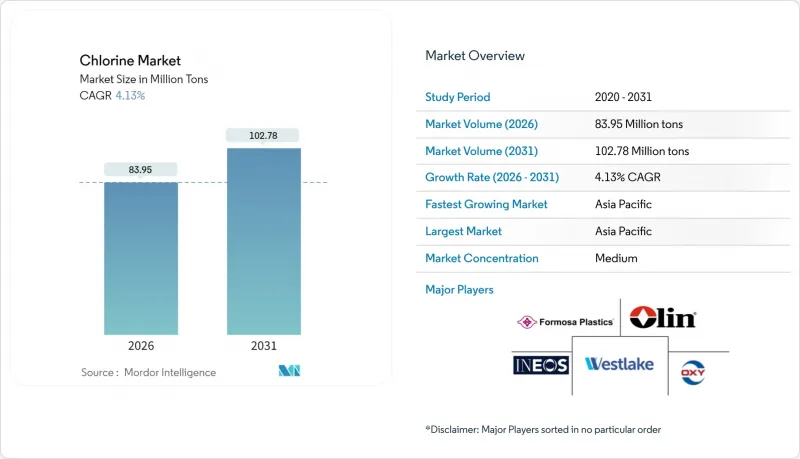

预计氯气市场将从 2025 年的 8,062 万吨成长到 2026 年的 8,395 万吨,预计到 2031 年将达到 1.0278 亿吨,2026 年至 2031 年的复合年增长率为 4.13%。

强大的基础设施投资、不断扩大的市政水处理项目以及日益增长的医药中间体产量,正助力该产品在全球产业链中保持其关键地位。由于能耗低且环保法规日益严格,膜电解池技术在所有主要地区均优于传统生产方法。管道、电缆绝缘和柔软性薄膜用聚氯乙烯树脂需求的持续增长,支撑了基础材料的强劲消耗;同时,固态电池研发、半导体蚀刻剂和高纯度中间体的应用,也为氯供应商带来了新的商机。亚太地区预计主导销售成长,并继续保持其作为主要出口枢纽的地位,这得益于综合石化中心利用了较低的物流成本和现场发电设施的优势。

全球氯气市场趋势及展望

基础设施和包装领域对PVC的需求快速成长

用于饮用水和污水处理的PVC管道网路正在推动氯气需求的持续成长,尤其是在中国、印度、印尼和越南,这主要得益于政府主导的住宅建设和交通走廊开发。在消费品包装领域,PVC的耐用性和密封性能满足了物流中心日益增长的需求。大型计划作为国家奖励策略的一部分获得资金筹措,即使在经济低迷时期也很少中断,这为氯气市场提供了可预测的基础。综合氯碱生产商正在对其工厂维修,采用节能型薄膜分离设备,以确保具有竞争力的氯乙烯单体供应,从而巩固其在沿海工业园区的市场份额。东南亚挤出产能的稳定扩张也印证了建筑商和加工商对价格合理的氯化树脂的结构性依赖。

快速投资都市污水处理

亚太走廊特大城市的人口密度要求既要建造大规模集中式水处理厂,也要为郊区提供模组化系统。氯化消毒仍然是抵御病原体最经济有效的最终屏障,这支撑了对现场电解和包装式次氯酸钠的需求。巴西、南非和菲律宾的法规强制要求对再生水进行三级消毒,预计未来的取水量将超过历史最高水准。工业园区正在推行零液体排放政策,并推广双循环循环利用,延长氯的接触时间。设备供应商指出,低盐度膜电解槽的应用正在兴起,这种电解槽可以最大限度地减少盐排放,并促进化学品的持续消耗合同,从而与城市可持续永续性章程保持一致。

加强开发中国家逐步淘汰汞电池工厂

强制遵守《水俣公约》迫使东南亚、东欧和非洲部分地区剩余的汞冶炼厂关闭或进行成本高昂的改造。过渡期停产暂时限制了当地聚氯乙烯(PVC)加工商和纺织品漂白厂的氯气供应,而跨境进口则推高了运费。无力负担膜维修的小型企业退出了该行业,推动了区域整合。原本用于支持扩张计画的营运资金被用来修復现有的污泥池。已完成维修的营运商正透过高成本进口来填补短期供不应求,这导致合约谈判出现波动。

细分市场分析

到2025年,EDC/PVC将占据氯气市场33.29%的份额,这反映了该聚合物在管道、型材和薄膜应用方面的多功能性。集中的需求使得一体化製造商能够以基本负载运作盐水迴路,从而实现高运转率和可预测的现金流。同时,以异氰酸酯和含氧化合物为主导的氯气市场预计将在2026年至2031年间以4.41%的复合年增长率增长,这主要得益于聚氨酯泡棉作为节能建筑和轻量化汽车内部装潢建材的隔热材料的应用。对高利润应用日益增长的需求正促使生产商建造专用的高纯度迴路和模组化反应器,从而提供超越大宗氯乙烯(VCM)合约的柔软性。

氯甲烷和溶剂在冷冻、硅片清洗和除草剂合成等领域需求稳定,受建筑週期波动的影响较小。环氧氯丙烷的需求预计将因用于离岸风电结构耐腐蚀涂料的水性环氧树脂而逐步成长。由氯製成的无机化学品是饮用水处理和废气处理凝聚剂混合物的基础原料,支撑着非週期性需求,尤其是在新兴亚洲城市。

氯市场报告按应用(EDC/PVC、异氰酸酯和含氧化合物、氯甲烷、溶剂和环氧氯丙烷、无机化学品、其他应用)、终端用户行业(水处理、製药、化学品、造纸和纸浆、塑胶、农业化学品、其他终端用户产业)和地区(亚太地区、北美、欧洲、南美、中东和非洲)进行分析。

区域分析

至2025年,亚太地区将占全球氯气需求的64.13%,凸显其作为氯气市场中心的地位。该地区拥有从炼厂到PVC的完整价值链,接近性中国燃煤发电厂,以及强有力的国内管道更新计划,这些因素将有助于维持该地区的高利用率。在新兴工业园区安装的可再生能源驱动的膜分离装置的推动下,预计到2031年,亚太地区氯气市场规模将以4.72%的复合年增长率进一步增长。

北美市场成熟且技术先进。投资重点在于製程自动化、改进的电极涂层以及用于生产特种中间体的自用氯循环系统。 PCC集团在科慕密西西比州的34万吨计划就是一个典型的例子,该专案将生产能力与下游的二氧化钛和MDI工厂集中布局,从而缩短了供应链并降低了运输风险。

在欧洲,永续营运和能源效率是优先事项,这反映了高昂的电价和雄心勃勃的气候法规。製药和高端涂料行业稳定的基本客群为提供优质产品提供了充分的理由,也使营运商受益。同时,高耗能工厂正在考虑搬迁和签订绿色电力购买协议,以应对成本压力。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 基础设施和包装产业对PVC的需求快速成长

- 快速投资都市污水处理

- 专利到期药物热潮推动氯代中间体的生产。

- 用于固态电池(电动车用)的电池级氯化锂金属

- 亚洲半导体製造厂对蚀刻剂的需求不断增长

- 市场限制

- 加强发展中国家汞电池工厂的逐步淘汰

- 可再生能源发展导致苛性钠供应过剩加剧(价格压力)

- 冷却塔中溴化杀菌剂替代品的趋势日益增长

- 价值链分析

- 技术趋势概述

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代产品和服务的威胁

- 竞争程度

- 定价分析

- 进出口趋势

第五章 市场规模与成长预测

- 透过使用

- EDC/PVC

- 异氰酸酯和含氧化合物

- 氯甲烷

- 溶剂和环氧氯丙烷

- 无机化学品

- 其他用途

- 按最终用户行业划分

- 水处理

- 製药

- 化学品

- 纸浆和造纸

- 塑胶

- 杀虫剂

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 义大利

- 法国

- 西班牙

- 北欧国家

- 土耳其

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- Anwil(Orlen)

- Arkema

- Covestro AG

- DOW

- Ercros SA

- Formosa Plastics Group

- Hanwha Solutions

- INEOS

- Kem One

- Kuhlmann Europe

- Nobian

- Occidental Petroleum Corporation

- Olin Corporation

- Shivtek Spechemi Industries Ltd

- Spolchemie(KAPRAIN as)

- Tata Chemicals Limited

- Tosoh Corporation

- Vencorex

- Vynova Group(ICIG HOLDING SE)

- Westlake Corporation

第七章 市场机会与未来展望

The Chlorine market is expected to grow from 80.62 million tons in 2025 to 83.95 million tons in 2026 and is forecast to reach 102.78 million tons by 2031 at 4.13% CAGR over 2026-2031.

Strong infrastructure spending, expanding municipal water treatment programs, and rising pharmaceutical intermediate output maintain the commodity's indispensable status in the worldwide process chain. Membrane-cell technology has overtaken legacy production methods in every leading region, encouraged by lower energy use and tightening environmental rules. A continued uplift in polyvinyl chloride demand for pipes, cable insulation, and flexible films keeps basic feedstock consumption robust, while solid-state battery research, semiconductor etchants, and high-purity intermediates broaden the addressable opportunity for chlorine suppliers. Asia-Pacific dominates volume growth and will remain the principal export base as integrated petrochemical hubs exploit lower logistics costs and access to captive power.

Global Chlorine Market Trends and Insights

Surging PVC Demand in Infrastructure and Packaging

PVC pipe networks for potable water and wastewater drive multi-year chlorine offtake, especially across China, India, Indonesia, and Vietnam where government-backed housing and transportation corridors are underway. The packaging of fast-moving goods favors PVC's toughness and sealing properties, supporting incremental demand from e-commerce distribution centers. Large-scale projects seldom pause during economic slowdowns because they are funded within national stimulus packages, giving the chlorine market a predictable baseline. Integrated chlor-alkali producers are retrofitting plants with energy-efficient membranes to supply vinyl chloride monomer competitively, solidifying their share in coastal industrial parks. The steady course of new extrusion capacity additions in Southeast Asia underlines the structural dependence of builders and converters on affordable chlorine-derived resins.

Rapid Urban Wastewater Investments

Population density in megacities across the Asia-Pacific corridor necessitates larger centralized plants as well as modular systems for peri-urban districts. Chlorination remains the most economical last-step barrier against pathogens, sustaining procurement of on-site electrolyzers and packaged hypochlorite. Regulations in Brazil, South Africa, and the Philippines now specify tertiary disinfection for reclaimed water, lifting future intake beyond historic peak levels. Industrial parks adopt zero-liquid-discharge policies, pushing dual-loop reuse that relies on repeated chlorine contact times. Equipment suppliers note a pivot toward low-salt-input membrane cells that minimize brine disposal, aligning with citywide sustainability charters and fostering repeat chemical consumption contracts.

Tightened Mercury-Cell Plant Phase-Outs in Developing Regions

Mandatory compliance with the Minamata Convention forces remaining mercury facilities in Southeast Asia, Eastern Europe, and parts of Africa offline or into costly conversions. Transitional shutdowns temporarily constrain chlorine availability for local PVC converters and textile bleach plants, while cross-border import flows lift freight rates. Smaller firms unable to finance membrane retrofits exit the industry, nudging regional consolidation. Environmental remediation of legacy sludge ponds absorbs working capital that might otherwise support expansion programs. Operators completing conversions hedge short-term supply gaps with higher-priced imports, contributing to volatility in contract negotiations.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Off-Patent Boom Boosting Chlorination Intermediates

- Battery-Grade Lithium-Metal Chloride for Solid-State EV Batteries

- Escalating Renewable-Power-Driven Caustic Soda Oversupply

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

EDC/PVC retained 33.29% of the chlorine market share in 2025, mirroring the polymer's ubiquity across pipe, profile, and film categories. Demand concentration allows integrated players to run brine circuits at steady baseload, facilitating high-utilization rates and predictable cash flow. Meanwhile, the chlorine market size attributed to isocyanates and oxygenates is on track to rise at a 4.41% CAGR between 2026 and 2031 as polyurethane foam insulates energy-efficient buildings and lightweight vehicle interiors. Higher margin exposure incentivizes producers to carve out dedicated purity loops or modular reactors, adding flexibility beyond bulk VCM contracts.

Chloromethanes and solvents offer stable demand in refrigeration, silicon wafer cleaning, and herbicide synthesis, shielding volumes from construction cycles. Epichlorohydrin sees incremental lift from water-borne epoxy resins used in corrosion-resistant coatings for offshore wind structures. Inorganic chemicals carved from chlorine underpin coagulant blends for potable water and flue-gas treatment, anchoring non-cyclical intake, especially inside emerging Asian municipalities.

The Chlorine Market Report is Segmented by Application (EDC/PVC, Isocyanates and Oxygenates, Chloromethanes, Solvents and Epichlorohydrin, Inorganic Chemicals, and Other Applications), End-User Industry (Water Treatment, Pharmaceutical, Chemicals, Paper and Pulp, Plastic, Pesticides, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific captured 64.13% of global demand in 2025, underscoring its function as the epicenter of the chlorine market. The combination of integrated refinery-to-PVC value chains, proximity to coal-based power in China, and a robust domestic pipe replacement agenda keeps regional utilization high. The chlorine market size enjoyed by Asia-Pacific will rise further at a 4.72% CAGR to 2031, supported by renewable-powered membrane installations located within emerging industrial parks.

North America remains a mature but technologically advanced arena. Investments focus on process automation, electrode-coating upgrades, and captive chlorine loops for specialty intermediates. PCC Group's 340,000-ton project at Chemours' Mississippi site typifies moves to colocate capacity with downstream titanium dioxide and MDI plants, shortening supply chains and lowering transport risk.

Europe prioritizes sustainable operations and energy efficiency, reflecting high electricity tariffs and ambitious climate rules. Operators benefit from an established customer base in pharmaceuticals and high-end coatings, justifying premium-grade offerings. Concurrently, energy-intensive plants weigh relocation or green-power purchase agreements to offset cost pressures.

- Anwil (Orlen)

- Arkema

- Covestro AG

- DOW

- Ercros S.A

- Formosa Plastics Group

- Hanwha Solutions

- INEOS

- Kem One

- Kuhlmann Europe

- Nobian

- Occidental Petroleum Corporation

- Olin Corporation

- Shivtek Spechemi Industries Ltd

- Spolchemie (KAPRAIN a.s.)

- Tata Chemicals Limited

- Tosoh Corporation

- Vencorex

- Vynova Group (ICIG HOLDING SE)

- Westlake Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging PVC demand in infrastructure and packaging

- 4.2.2 Rapid urban wastewater investments

- 4.2.3 Pharmaceutical off-patent boom boosting chlorination intermediates

- 4.2.4 Battery-grade Li-metal chloride for solid-state EV batteries

- 4.2.5 Semiconductor etchant expansion in Asia fabs

- 4.3 Market Restraints

- 4.3.1 Tightened mercury-cell plant phase-outs in developing regions

- 4.3.2 Escalating renewable-power-driven caustic soda oversupply (price squeeze)

- 4.3.3 Growing bromine-based biocide substitution in cooling towers

- 4.4 Value Chain Analysis

- 4.5 Technological Snapshot

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

- 4.7 Pricing Analysis

- 4.8 Import and Export Trends

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Application

- 5.1.1 EDC/PVC

- 5.1.2 Isocyanates and Oxygenates

- 5.1.3 Chloromethanes

- 5.1.4 Solvents and Epichlorohydrin

- 5.1.5 Inorganic Chemicals

- 5.1.6 Other Applications

- 5.2 By End-user Industry

- 5.2.1 Water Treatment

- 5.2.2 Pharmaceutical

- 5.2.3 Chemicals

- 5.2.4 Paper and Pulp

- 5.2.5 Plastic

- 5.2.6 Pesticides

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Spain

- 5.3.3.6 NORDIC Countries

- 5.3.3.7 Turkey

- 5.3.3.8 Russia

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Anwil (Orlen)

- 6.4.2 Arkema

- 6.4.3 Covestro AG

- 6.4.4 DOW

- 6.4.5 Ercros S.A

- 6.4.6 Formosa Plastics Group

- 6.4.7 Hanwha Solutions

- 6.4.8 INEOS

- 6.4.9 Kem One

- 6.4.10 Kuhlmann Europe

- 6.4.11 Nobian

- 6.4.12 Occidental Petroleum Corporation

- 6.4.13 Olin Corporation

- 6.4.14 Shivtek Spechemi Industries Ltd

- 6.4.15 Spolchemie (KAPRAIN a.s.)

- 6.4.16 Tata Chemicals Limited

- 6.4.17 Tosoh Corporation

- 6.4.18 Vencorex

- 6.4.19 Vynova Group (ICIG HOLDING SE)

- 6.4.20 Westlake Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

2025-2029年全球氯气市场

2025-2029年全球氯气市场 二氧化氯发生器市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年

二氧化氯发生器市场-全球产业规模、份额、趋势、机会、预测:按类型、应用、地区和竞争格局划分,2021-2031年 稳定型二氧化氯市场依产品类型、应用、最终用户和通路划分,全球预测(2026-2032年)全球氯市场(按应用、最终用途产业、生产技术、形式和分销管道)预测 2025-2032氯气加药系统市场:按系统类型、氯气类型、组件、控制类型、加药模式、应用、最终用途行业和分销渠道 - 2025-2030 年全球预测液氯市场-全球产业规模、份额、趋势、机会及预测,依销售通路、应用、区域及竞争状况细分,2020-2030 年

稳定型二氧化氯市场依产品类型、应用、最终用户和通路划分,全球预测(2026-2032年)全球氯市场(按应用、最终用途产业、生产技术、形式和分销管道)预测 2025-2032氯气加药系统市场:按系统类型、氯气类型、组件、控制类型、加药模式、应用、最终用途行业和分销渠道 - 2025-2030 年全球预测液氯市场-全球产业规模、份额、趋势、机会及预测,依销售通路、应用、区域及竞争状况细分,2020-2030 年 全球 C2 氯化溶剂市场预测(至 2034 年)

全球 C2 氯化溶剂市场预测(至 2034 年) 全球氯市场:按应用、最终用户、地区和预测

全球氯市场:按应用、最终用户、地区和预测 按类型、包装、应用和地区分類的氯市场

按类型、包装、应用和地区分類的氯市场 全球液态氯市场规模、份额及趋势分析报告(按类型(次氯酸钠、次氯酸锂、次氯酸钙等)、应用、区域展望和预测,2024 - 2031 年)

全球液态氯市场规模、份额及趋势分析报告(按类型(次氯酸钠、次氯酸锂、次氯酸钙等)、应用、区域展望和预测,2024 - 2031 年)