|

市场调查报告书

商品编码

1937439

化妆品和香水玻璃瓶包装:市场份额分析、行业趋势和统计数据、成长预测(2026-2031)Cosmetic Perfumery Glass Bottle Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

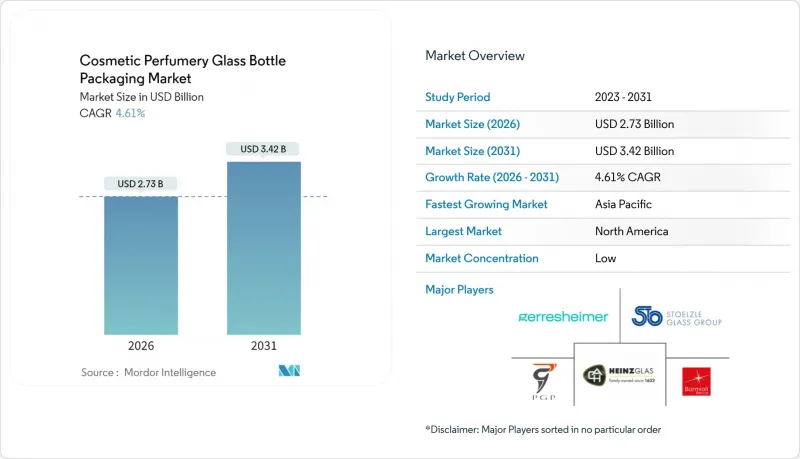

2025年化妆品香水玻璃瓶包装市场价值为26.1亿美元,预计2031年将达到34.2亿美元,而2026年为27.3亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 4.61%。

这种稳健而适度的成长轨迹反映了该行业应对供应链波动的能力,以及其掌握优质化趋势、优先选择玻璃而非其他材料的准备。市场扩张的背景是变革性的监管变化,特别是欧盟第2025/40号法规,该法规要求所有包装在2030年前必须可回收。这项法规将玻璃——一种可以无限循环利用且不会劣化——定位为战略优势。重塑产业的宏观因素在永续性需求和奢侈品定位策略的交汇点上汇聚。美妆和香水产品的优质化趋势推动了对美观包装的需求,这些包装能够传达品牌传承和产品真实性。同时,电子商务的兴起带来了双重压力:品牌需要视觉吸引力强的包装来进行数位行销,同时也需要寻求抗衝击解决方案,以最大限度地减少因破损造成的退货。

全球化妆品香水玻璃瓶包装市场趋势及洞察

美容和香水产品的优质化

奢华美妆和香水品牌正日益将玻璃包装作为体现产品品质和品牌传承的手段,推动消费者逐渐摒弃塑胶包装。随着消费者对奢华化妆品支付溢价的意愿日益增强,这一趋势正在加速发展,尤其是在新兴市场,玻璃包装被视为正品和尊贵的象征。优质化效应形成了一个良性循环:产品价格上涨证明了玻璃包装成本的合理性,这反过来又强化了产品的奢侈定位,并允许价格进一步上涨。新款奢华香水上市时,通常会采用客製化玻璃瓶,其独特的形状、颜色和装饰元素是塑胶包装无法复製的,这进一步巩固了玻璃作为奢侈品象征的地位。数位行销也加速了这一趋势,因为玻璃包装在社群媒体和电商平台上的出色表现,为那些注重视觉差异化的品牌创造了附加价值。

推动永续性,实现玻璃的无限循环利用

法规结构和企业永续发展措施都在强调玻璃包装相对于塑胶包装的无限可回收优势。欧盟的《包装和包装废弃物条例》规定,到2030年所有包装都必须回收利用,其中玻璃的回收率达到了74%,而塑胶的回收率则低得多。玻璃回收形成了闭合迴路系统,废旧玻璃(玻璃屑)可以作为原料重新用于生产新瓶子,并且质量最多劣化82%,OI的碳中和“Estampe”瓶就证明了这一点。企业永续发展策略越来越重视玻璃包装对减少范围3排放的贡献。像SGD Pharma这样的品牌已经推出了专为化妆品应用设计的瓶子,其中含有20%的消费后回收材料。这项永续发展措施尤其受到Z世代消费者的青睐,他们重视环保,并将玻璃视为比塑胶更优越的替代品。

塑胶包装的成本和重量优势

塑胶包装在成本和物流方面具有显着优势,阻碍了玻璃包装的普及,尤其是在价格敏感的大众化妆品市场,因为该领域的高端材质选择有限。塑胶容器通常比同类玻璃包装便宜 40-60%,重量也轻得多,从而降低了运输成本和大众分销相关的碳排放。先进的塑胶配方技术正透过透明聚合物和表面处理,不断复製玻璃的美感,在不增加成本的情况下创造出高端质感。对于大件产品和多件套装而言,重量差异尤其明显,玻璃包装的运输成本可能是塑胶包装的两倍。电子商务的蓬勃发展进一步加剧了这些担忧,因为品牌商都在优化包装,以实现成本效益高的配送,同时最大限度地减少因破损造成的退货和客户不满。

细分市场分析

截至2025年,香水将占化妆品香水玻璃瓶包装市场46.28%的份额,凸显了香水製造商对惰性玻璃容器的依赖,以保存其复杂的香氛成分。这一主导份额是化妆品香水玻璃瓶包装市场中最大的单一组成部分。定製香水瓶与奢侈品牌形象的长期关联,使品牌即使在成本上涨时期也能维持高端定价,从而受益于此细分市场。设计师品牌的强力行销支援也保证了稳定的复购量,使化妆品香水玻璃瓶包装市场能够抵御邻近美妆品类需求的波动。

儘管美甲护理品类规模相对较小,但预计到2031年将以6.05%的复合年增长率成长,成为目标产品中成长最快的品类。这主要得益于消费者对装在订製玻璃瓶中的沙龙级指甲油的偏好。网红们对美甲艺术的日益关注推动了市场规模的成长,而配方师则倾向于使用玻璃包装以最大限度地减少溶剂挥发。护肤和护髮产品线正经历中等个位数的成长,玻璃滴管瓶和护理罐象征着视网醇精华、安瓶和高浓度面膜的卓越功效。虽然彩妆领域对玻璃瓶的应用有限,但化妆品和香水玻璃瓶包装市场依然涵盖多种美容产品,奢侈品牌也开始采用手工玻璃瓶填充用限量版脸部喷雾和气垫粉底。

区域分析

到2025年,北美将占全球化妆品香水玻璃瓶包装市场收入的37.10%,这主要得益于成熟的设计师香水市场、订阅式美妆盒以及完善的回收计划(鼓励消费者回收空瓶)。奢侈品牌持续将手工玻璃瓶作为品牌标誌进行推广,而D2C新兴企业则推出填充用填充的玻璃瓶,以减少废弃物。加拿大的「生产者延伸责任制」(EPR)计画为玻璃废料的回收津贴,这些废料被送到当地的熔炉,形成闭合迴路循环,从而支撑了化妆品香水玻璃瓶包装市场的规模。

亚太地区是快速成长的引擎,预计到2031年将以5.36%的复合年增长率成长,这主要得益于TikTok引领的美容潮流以及中国、印度和印尼可支配收入的成长。中国当地对香水的需求不断增长,推动了定製香水瓶订单的订单;而印度消费者越来越将厚壁玻璃视为正品的标誌,从而推动了化妆品香水玻璃瓶包装市场的需求。韩国的K-Beauty出口商率先推出了双腔玻璃安瓿,这种安瓿可以分离并保存活性成分直至激活,这表明区域研发正在显着改变传统的包装形式。

欧洲得益于欧盟法规2025/40的监管力度,以及格拉斯、伊达尔-奥伯施泰因和帕尔马等成熟的香水产业丛集。成熟的回收体系使生产商能够实现较高的玻璃屑回收率,参与企业能够在不支付压低价格的全新玻璃附加费的情况下,达到品牌碳排放目标。东欧利用低能源价格供应注重性价比的燧石瓶,而西欧加工商则专注于装饰性和高端饰面。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美容和香水产品的优质化

- 推动永续性,实现玻璃的无限循环利用

- 电子商务需要美观且抗衝击的包装。

- 利用雷射技术进行个人化和防伪雕刻

- 欧盟2025/40号法规:建议使用可回收的单一材料包装

- 透过电气化和轻型炉降低成本和减少排放排放

- 市场限制

- 塑胶包装的成本和重量优势

- 能源和碱灰投入价格波动

- 欧盟包装最小化法规限制了重型、装饰性瓶子的使用。

- 电子商务中易碎玻璃製品的破损率和退货率很高

- 产业供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 产业间竞争

第五章 市场规模与成长预测

- 依产品类型

- 香水

- 护肤

- 指甲护理

- 护髮

- 其他产品类型

- 按产能

- 0~50 mL

- 50~150 mL

- >150 mL

- 按颜色

- 燧石

- 琥珀色

- 磨砂

- 特殊颜色

- 其他颜色

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 智利

- 其他南美洲

- 欧洲

- 英国

- 德国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Verescence France SASU

- Gerresheimer AG

- Pochet SAS

- HEINZ-GLAS GmbH & Co. KGaA

- Bormioli Luigi SpA

- Vitro, SAB de CV

- PGP Glass Private Limited

- Stoelzle Glass Group

- Zignago Vetro SpA

- Berlin Packaging LLC

- Saver Glass SAS

- Pragati Glass Pvt Ltd

- Baralan International SpA

- Lumson SpA

- vetroelite packaging srl

- Feemio Group Co., Ltd.

- Brandsamor Commerce LLC

第七章 市场机会与未来展望

The cosmetic perfumery glass bottle packaging market was valued at USD 2.61 billion in 2025 and estimated to grow from USD 2.73 billion in 2026 to reach USD 3.42 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

This moderate yet resilient growth trajectory reflects the sector's ability to navigate supply-chain volatility while capitalizing on premiumization trends that favor glass over alternative materials. The market's expansion occurs against a backdrop of transformative regulatory shifts, particularly EU Regulation 2025/40, which mandates that all packaging be recyclable by 2030. This regulation positions glass as a strategic advantage, given its infinite recyclability without degradation in quality. Macro forces reshaping the industry center on sustainability mandates intersecting with luxury positioning strategies. The premiumization wave in beauty and fragrance products drives demand for aesthetically superior packaging that conveys brand heritage and product integrity. Simultaneously, e-commerce expansion creates dual pressures: brands require visually compelling packaging for digital marketing while needing impact-resistant solutions to minimize breakage-related returns.

Global Cosmetic Perfumery Glass Bottle Packaging Market Trends and Insights

Premiumisation of Beauty and Fragrance Products

Premium beauty and fragrance brands increasingly position glass packaging as a tangible expression of product quality and brand heritage, driving specification shifts away from plastic alternatives. This trend accelerates as consumer willingness to pay premium prices for luxury cosmetics increases, particularly in emerging markets where glass packaging is seen as a symbol of authenticity and prestige. The premiumization effect creates a virtuous cycle: higher product prices justify the costs of glass packaging, while glass packaging reinforces premium positioning and enables further price increases. Luxury fragrance launches consistently specify custom glass flacons with unique shapes, colors, and decorative elements that plastic cannot replicate, cementing glass as the material of choice for high-end positioning. Digital marketing amplifies this trend, as glass packaging photographs better for social media and e-commerce platforms, creating additional value for brands that invest in visual differentiation.

Sustainability Push for Infinitely-Recyclable Glass

Regulatory frameworks and corporate sustainability commitments converge to favor the infinite recyclability advantage of glass packaging over plastic alternatives. The EU's Packaging and Packaging Waste Regulation mandates that all packaging be recyclable by 2030, with glass achieving 74% recycling rates compared to significantly lower plastic recycling performance. Glass recycling creates a closed-loop system where post-consumer cullet can constitute up to 82% of new bottle content without quality degradation, as demonstrated by O-I's carbon-neutral Estampe bottle. Corporate sustainability strategies are increasingly recognizing the contribution of glass packaging to Scope 3 emissions reduction, with brands like SGD Pharma launching bottles with 20% post-consumer recycled content, specifically designed for cosmetics applications. The sustainability narrative resonates particularly strongly with Gen Z consumers, who prioritize environmental credentials and view glass as a superior alternative to plastic.

Plastic Packaging Cost and Weight Advantage

Plastic packaging maintains significant cost and logistics advantages that hinder the adoption of glass, particularly in mass-market cosmetic segments where price sensitivity limits the selection of premium materials. Plastic containers typically cost 40-60% less than equivalent glass packaging, while weighing substantially less, which reduces shipping costs and the carbon footprint associated with high-volume distribution. Advanced plastic formulations are increasingly replicating glass aesthetics through clear polymers and surface treatments, enabling premium positioning without the costs associated with glass. The weight differential becomes particularly pronounced for large-format products and multi-product sets, where glass packaging can double shipping costs compared to plastic alternatives. E-commerce growth amplifies these concerns as brands optimize packaging for cost-effective fulfillment while minimizing damage-related returns and customer dissatisfaction.

Other drivers and restraints analyzed in the detailed report include:

- E-commerce Demand for Aesthetic, Impact-Resistant Packs

- Laser-Enabled Personalisation and Anti-Counterfeit Engraving

- Volatile Energy and Soda-Ash Input Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Perfumes accounted for a 46.28% portion of the cosmetic perfumery glass bottle packaging market in 2025, underscoring how fragrance houses rely on inert glass containers to preserve complex scent profiles. This dominant foothold equates to the single-largest slice of the cosmetic perfumery glass bottle packaging market share. The segment benefits from a well-established association between bespoke flacons and luxury positioning, enabling brands to maintain premium price points even during cost-inflation cycles. Strong marketing support from designer labels sustains steady reorder volumes, keeping the cosmetic perfumery glass bottle packaging market resilient to demand swings in adjacent beauty categories.

Nail care, although still comparatively smaller, is expanding at a 6.05% CAGR through 2031, the fastest growth among all tracked products, as consumers trade up to salon-quality lacquers packaged in custom glass vials. Growing influencer interest in nail art has expanded the addressable market, and formulators prefer glass to minimize solvent evaporation. Skin-care and hair-care lines report mid-single-digit advances as glass dropper bottles and treatment jars signal efficacy for retinol serums, ampoules, and concentrated masks. Although make-up remains selective in its use of glass, prestige brands tap artisanal flacons for limited-edition face mists and cushion-compact refills, keeping the cosmetic perfumery glass bottle packaging market diversified across multiple beauty rituals.

The Cosmetic Perfumery Glass Bottle Packaging Market Report is Segmented by Product Type (Perfumes, Skin Care, Nail Care, Hair Care, and More), Capacity (0-50 Ml, 50-150 Ml, and >150 Ml), Color (Flint, Amber, Frosted, Special-Coloured, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 37.10% of the worldwide cosmetic perfumery glass bottle packaging market revenue in 2025, driven by its established designer-fragrance ecosystem, subscription beauty boxes, and robust take-back programs that reward consumers for returning empty primary containers. Prestige houses continue to champion artisanal glass flacons as brand icons, while direct-to-consumer startups integrate refill pods to cut waste. Canada's Extended Producer Responsibility regime subsidizes cullet collection, which feeds regional furnaces and supports a closed-loop stream that bolsters the cosmetic perfumery glass bottle packaging market size.

The Asia-Pacific region is the sprinting growth engine, with a 5.36% CAGR to 2031, driven by TikTok-driven beauty trends and rising disposable incomes in China, India, and Indonesia. Mainland China's fragrance awakening triggers record custom-flacon briefs, and Indian consumers increasingly associate heavy-walled glass with authenticity, steering incremental demand toward the cosmetic perfumery glass bottle packaging market. South Korea's K-Beauty exporters innovate dual-chamber glass ampoules that keep active powders separate until activation, demonstrating how regional R&D leapfrogs legacy formats.

Europe remains anchored by regulatory muscle EU Regulation 2025/40 and storied perfumery clusters in Grasse, Idar-Oberstein, and Parma. Producers harvest high cullet ratios from mature collection schemes, allowing cosmetic perfumery glass bottle packaging market participants to hit brand carbon targets without price-crippling virgin-batch surcharges. Eastern Europe supplies value-centric flint bottles, leveraging lower energy tariffs, while Western converters focus on decoration excellence and luxury finishing.

- Verescence France SASU

- Gerresheimer AG

- Pochet SAS

- HEINZ-GLAS GmbH & Co. KGaA

- Bormioli Luigi S.p.A.

- Vitro, S.A.B. de C.V.

- PGP Glass Private Limited

- Stoelzle Glass Group

- Zignago Vetro S.p.A.

- Berlin Packaging LLC

- Saver Glass SAS

- Pragati Glass Pvt Ltd

- Baralan International S.p.A.

- Lumson S.p.A.

- vetroelite packaging s.r.l

- Feemio Group Co., Ltd.

- Brandsamor Commerce LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumisation of beauty and fragrance products

- 4.2.2 Sustainability push for infinitely-recyclable glass

- 4.2.3 E-commerce demand for aesthetic, impact-resistant packs

- 4.2.4 Laser-enabled personalisation and anti-counterfeit engraving

- 4.2.5 EU-2025/40 regulation favouring recyclable mono-material packs

- 4.2.6 Electrified and lightweight furnaces cutting cost and CO2

- 4.3 Market Restraints

- 4.3.1 Plastic packaging cost and weight advantage

- 4.3.2 Volatile energy and soda-ash input prices

- 4.3.3 EU packaging-minimisation rules curbing heavy, ornate flacons

- 4.3.4 High e-commerce breakage / return rates for fragile glass

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Perfumes

- 5.1.2 Skin Care

- 5.1.3 Nail Care

- 5.1.4 Hair Care

- 5.1.5 Other Product Type

- 5.2 By Capacity

- 5.2.1 0-50 ml

- 5.2.2 50-150 ml

- 5.2.3 >150 ml

- 5.3 By Color

- 5.3.1 Flint

- 5.3.2 Amber

- 5.3.3 Frosted

- 5.3.4 Special-coloured

- 5.3.5 Other Color

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Australia

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Verescence France SASU

- 6.4.2 Gerresheimer AG

- 6.4.3 Pochet SAS

- 6.4.4 HEINZ-GLAS GmbH & Co. KGaA

- 6.4.5 Bormioli Luigi S.p.A.

- 6.4.6 Vitro, S.A.B. de C.V.

- 6.4.7 PGP Glass Private Limited

- 6.4.8 Stoelzle Glass Group

- 6.4.9 Zignago Vetro S.p.A.

- 6.4.10 Berlin Packaging LLC

- 6.4.11 Saver Glass SAS

- 6.4.12 Pragati Glass Pvt Ltd

- 6.4.13 Baralan International S.p.A.

- 6.4.14 Lumson S.p.A.

- 6.4.15 vetroelite packaging s.r.l

- 6.4.16 Feemio Group Co., Ltd.

- 6.4.17 Brandsamor Commerce LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

2026年全球包装与标籤服务市场报告

2026年全球包装与标籤服务市场报告 气泡膜市场:2026-2032年全球市场预测(依材料、厚度、应用、最终用户及通路划分)復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)全球电子顺磁共振波谱仪市场(按产品类型、频率、工作模式、组件、应用和最终用户划分)预测(2026-2032年)按包装类型、材料、最终用途、分销管道和应用分類的常温纸盒市场—全球预测,2026-2032年

气泡膜市场:2026-2032年全球市场预测(依材料、厚度、应用、最终用户及通路划分)復古包装市场:按材料、类型、最终用途、印刷技术和通路-2026-2032年全球预测纸质復古包装市场:依材料、包装类型、销售管道、最终用户、应用程式划分,全球预测(2026-2032)多功能零件市场按产品类型、价格范围、应用、垂直产业和分销管道划分,全球预测(2026-2032年)纸塑包装器材市场:依机器类型、材料、操作类型和应用划分,全球预测(2026-2032年)全球电子顺磁共振波谱仪市场(按产品类型、频率、工作模式、组件、应用和最终用户划分)预测(2026-2032年)按包装类型、材料、最终用途、分销管道和应用分類的常温纸盒市场—全球预测,2026-2032年 新加坡包装市场

新加坡包装市场 包装市场分析及预测(至2035年):类型、产品类型、材料类型、技术、应用、最终用户、功能、服务、流程、解决方案

包装市场分析及预测(至2035年):类型、产品类型、材料类型、技术、应用、最终用户、功能、服务、流程、解决方案