|

市场调查报告书

商品编码

1938977

汽车座椅:市占率分析、产业趋势与统计、成长预测(2026-2031)Automotive Seats - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

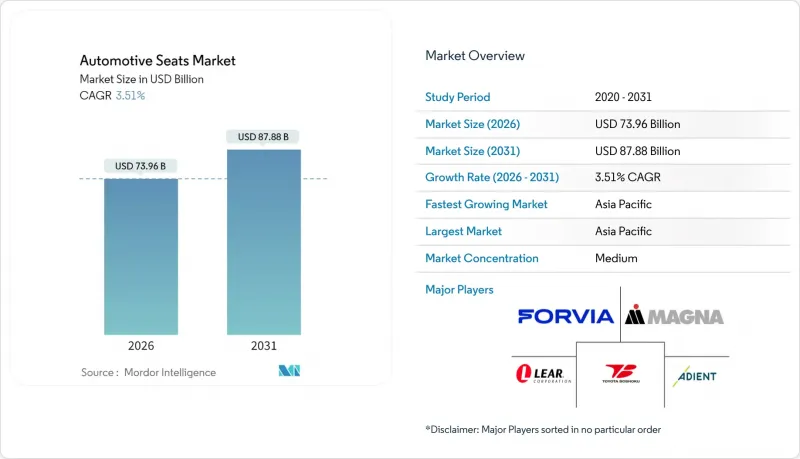

预计到 2026 年,汽车座椅市场价值将达到 739.6 亿美元,高于 2025 年的 714.5 亿美元。

预计到 2031 年将达到 878.8 亿美元,2026 年至 2031 年的复合年增长率为 3.51%。

随着消费者对电气化、自动驾驶功能和高端舒适性的偏好,座椅框架、衬垫和电子元件的设计不断改进,市场成长仍然强劲。汽车製造商持续采用轻量化结构以减轻电池重量,而消费者则继续偏好具备电动调节、通风和按摩功能的产品,从而推高了平均售价。原物料价格波动和严格的安全法规给整个价值链带来了成本压力,但一级供应商透过与车辆项目的深度整合,保持了价格优势。亚太地区正在推动销售需求和技术应用,中国、印度和日本的工厂正在扩大内燃机和电动车平台的产能。

全球汽车座椅市场趋势与洞察

全球轻型汽车产量增加,尤其是SUV产量增加

到2024年,SUV将占全球汽车销量的54%,这将增加每辆车的座位数。这将推动对侧向支撑、多排座椅配置和高端内装的需求。亚太地区的製造商正受惠于SUV销量的成长,而SUV的普及又得益于可支配收入的增加和都市化的加速。电动SUV的发展势头更加强劲。预计到2023年,纯电动SUV的销售将占SUV总销量的20%,这将刺激对轻量化车架和整合式温度控管管理系统的订单,从而抵消电池的重量。国际能源总署(IEA)的报告指出,目前大多数SUV仍然运作石化燃料,这意味着整合主动冷却和加热功能以及轻量化车身结构的电动座椅技术仍有巨大的发展潜力。

消费者对具备电动、通风和按摩功能的座椅需求不断增长

曾经只有豪华品牌才具备的高端功能,如今在中阶车型中也越来越常见。李尔公司的 ComfortMax 平台可将加热和通风响应时间缩短 40%,并将组装复杂性降低一半,从而使整车製造商能够大规模采用该平台。通风座椅是成长最快的技术领域,年复合成长率达 6.12%,因为舒适的温度有助于维持电动车的续航里程。按摩系统融入了生物回馈技术,以减轻乘客的压力。将座椅改造为健康中心,并透过软体升级,为企业带来持续的收入来源。

皮革、泡沫和高性能聚合物的价格波动

2020年至2021年间,钢材价格翻了一番多,导致每辆车的原料成本从2,200美元增至4,125美元,给座椅供应商的利润率带来了压力。由于聚氨酯泡棉(占座椅垫90%以上)的价格与原油价格波动密切相关,製造商在生产过程中难以将成本上涨转嫁给客户。供应商正透过重新设计座椅垫形状以减少泡棉用量以及使用再生聚合物混合物来应对这一问题。

细分市场分析

预计到2025年,合成皮革将占据汽车座椅市场48.20%的份额,年复合成长率达5.35%,这反映了其兼具价格优势和奢华感的双重吸引力。汽车製造商(OEM)注重合成皮革的均匀纹理、抗污性和易清洁性,这有助于减少车队服务中的保固索赔。织布座椅在入门级车型中仍占据稳固地位,而真皮座椅则继续在高端市场占有一席之地,但面临着永续性问题和采购波动带来的挑战。随着汽车製造商寻求循环利用材料,亚麻和麻等天然纤维越来越多地被用于座椅靠背和坐垫加固,但价格溢价仍然是其广泛应用的一大障碍。

丰田的SofTex皮革饰面在生产过程中比真皮减少了85%的二氧化碳排放,这有助于该公司达到其车队平均排放目标。大陆集团和麦格纳正在研发生物泡沫衬垫原型,这种衬垫无需使用混合材料黏合剂,并且更易于回收。这些进展标誌着汽车衬垫正朝着单一材料方向发展,以便在车辆报废时易于拆卸,从而符合欧盟循环经济指令的要求。

到2025年,手排调整座椅仍将占据全球57.80%的市场份额,这反映了新兴市场和入门级车型对成本的重视。同时,通风座椅的复合年增长率将达到5.89%,反映了消费者在寒冷和温暖气候下对座椅舒适性的重视。加热座椅在北美仍将是标配,而电动调整座椅则弥合了经济型和豪华型车型之间的差距,无需复杂的空调系统整合即可提供座椅记忆功能和腰部支撑模组。

能够追踪坐姿和生命体征的智慧座椅正在高端电动车领域迅速发展。现代Transsys公司在起亚EV9车型中整合了低能耗碳纤维加热器、动态身体保养演算法和倾斜式座椅功能,展示了实现完全软体定义舒适性并实现大规模量产的途径。供应商们也在整合支援OTA空中升级的控制单元,从而解锁更多未来功能,并将收益延伸至销售环节之外。

区域分析

亚太地区将继续保持领先地位,销量占比达46.40%,复合年增长率达3.69%,这主要得益于中国电动汽车的蓬勃发展、印度紧凑型SUV市场的快速增长以及日本在座椅电子领域的持续投入。预计到2025年,电动车在中国新车销售的渗透率将达到45%,座椅供应商正致力于开发轻量化框架和整合式冷却设计。在印度,政府对电动三轮车和送货车的补贴刺激了对耐用、低维护且适合高强度使用环境的座椅的需求。丰田纺织等日本创新企业已推出带有摇摆椅功能和个性化音频的放鬆座椅,展现了其对提升该地区驾乘者舒适度的承诺。

在欧洲,重点在于减少排放气体和提高可回收性。更严格的法规要求材料可追溯性和全生命週期碳计量,促使人们采用生物基泡棉材料和易于拆卸的座椅套。 Forbia 的卡车座椅平台声称与传统设计相比可减少 40% 的二氧化碳排放,这既符合法规要求,又能提升驾驶者的舒适度。在北美,皮卡和 SUV 的市占率很高,通风和加热座椅正逐渐成为中阶车型的标准配备。供应商正利用其位置底特律和墨西哥製造地的优势,推动金属衝压和坐垫生产的本地化。这降低了物流风险,并满足了美国《本地消费法案》(MCA) 的本地采购要求。

中东、非洲和南美洲蕴藏着长期的成长潜力。各国政府正支持本地组装,以建造汽车生态系统,从而催生了对结构简单、成本低廉且能经受恶劣路况考验的长椅和折迭座椅的需求。共乘和小型巴士行业的批量采购,也带动了对易于保养的合成皮革和快速更换座椅模组的需求,这些产品能够在服务基础设施有限的环境中确保车辆的运作。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 全球轻型汽车产量增加,尤其是对SUV的需求不断增长

- 消费者对电动、通风和按摩座椅的需求日益增长

- 汽车製造商力推轻量化座椅,以满足二氧化碳排放目标

- 电动滑板平台,可实现灵活的驾驶室布局

- 出行即服务车辆需要易于清洁、经久耐用的内部装潢建材。

- 人工智慧驱动的乘员监控系统需要配备内建智慧感测器的座椅。

- 市场限制

- 皮革、发泡材和先进聚合物的价格波动;

- 严格的安全和认证测试成本

- 现有汽车製造商座椅结构更新周期延迟

- 由于其他舒适系统的兴起,对高级座椅的需求正在下降。

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 供应商的议价能力

- 消费者议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 依材料类型

- 合成皮革

- 真皮

- 织物

- 天然纤维等

- 透过技术

- 标准(手动)座椅

- 电动座椅

- 通风座椅

- 座椅加热

- 按摩座椅

- 智慧/AI整合座椅

- 按销售管道

- OEM

- 售后市场

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 两轮车和三轮车

- 依座位类型

- 长条座椅/分离式长条座椅

- 凹背单人座椅

- 机长座位/个人座位

- 儿童安全座椅

- 折迭式/跳跃式座椅

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 亚太其他地区

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 埃及

- 土耳其

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Adient PLC

- Lear Corporation

- Forvia SE

- Toyota Boshoku Corporation

- Magna International Inc.

- NHK Spring Co. Ltd

- Recaro Holding GmbH

- TS Tech Co. Ltd

- Tachi-S Co. Ltd

- Yanfeng Seating

- Hyundai Transys

- Gentherm Inc.

- Martur Fompak

- Grammer AG

- Freedman Seating

第七章 市场机会与未来展望

The automotive seat market size in 2026 is estimated at USD 73.96 billion, growing from 2025 value of USD 71.45 billion with 2031 projections showing USD 87.88 billion, growing at 3.51% CAGR over 2026-2031.

Growth stays positive as electrification, autonomous driving features, and a rising preference for premium comfort push redesigns of seat frames, cushions, and electronics. Automakers continue to specify lighter structures to compensate for battery weight, while consumers favor powered, ventilated, and massage functions that lift average selling prices. Raw-material volatility and stringent safety rules place cost pressure across the value chain, yet Tier-1 suppliers maintain pricing leverage because of their deep integration with vehicle programs. Asia Pacific leads volume demand and technology adoption as Chinese, Indian, and Japanese plants expand capacity for both internal-combustion and electric platforms.

Global Automotive Seats Market Trends and Insights

Rising Global Light-Vehicle Production, Especially SUVs

SUVs reached 54% of global car sales in 2024, increasing seat content per vehicle and lifting demand for reinforced side bolsters, multi-row configurations, and premium trim. Asia Pacific manufacturers benefit as disposable income and urbanization lift SUV penetration. Electric SUVs draw further momentum; 20% of 2023 SUV sales were fully electric, triggering new orders for lightweight frames and integrated thermal management that offset battery mass. The International Energy Agency reports that most SUVs still run on fossil fuel, leaving substantial potential for electrified seat innovation that integrates active cooling, heating, and weight-optimized shells .

Growing Consumer Demand for Powered, Ventilated & Massage Seats

Premium features once limited to luxury brands increasingly appear in mid-segment models. Lear Corporation's ComfortMax platform cuts heating and ventilation response times by 40% and halves assembly complexity, enabling OEM rollouts at scale . Ventilated seats represent the fastest-growing technology slice at 6.12% CAGR because thermal comfort helps EVs preserve driving range. Massage systems now incorporate biometric feedback to reduce occupant stress, transforming seats into wellness hubs and opening recurring revenue through software-enabled upgrades.

Volatile Prices of Leather, Foam & Advanced Polymers

Steel prices more than doubled between 2020 and 2021, and raw-material content per vehicle rose from USD 2,200 to USD 4,125, compressing margins for seat suppliers. Polyurethane foam, covering more than 90% of seat cushions, tracks oil price swings, exposing manufacturers to cost spikes that are difficult to pass through mid-program. Suppliers respond by redesigning cushion geometries to reduce foam volume and by qualifying recycled polymer blends.

Other drivers and restraints analyzed in the detailed report include:

- Automaker Push for Lightweight Seats to Meet CO2 Targets

- Electrified Skateboard Platforms Enabling Flexible Cabin Layouts

- Stringent Safety & Homologation Testing Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Synthetic leather held 48.20% of the automotive seat market share in 2025 and is projected to grow at a 5.35% CAGR, underscoring its dual appeal of affordability and premium look. Original-equipment programs value their consistent grain, stain resistance, and simplified cleaning, which lowers warranty claims in fleet service. Fabric remains entrenched in entry models, whereas genuine leather persists at the top end but faces sustainability concerns and sourcing volatility. Natural fibers such as flax and hemp enter seat backs and cushion reinforcements as OEMs pursue circular materials, but price premiums still limit volume deployment.

Toyota's SofTex trim produces 85% lower CO2 during manufacture than genuine leather, helping the company align with fleet-average emissions goals. Continental and Magna prototype bio-foam pads that ease recycling by eliminating mixed material adhesives. Such developments signal a shift toward mono-material cushions designed for straightforward disassembly at vehicle end-of-life to meet European circular-economy directives.

Manual adjusters still anchor 57.80% of global share in 2025, reflecting cost sensitivity in emerging markets and base trims. Ventilated variants, however, post a 5.89% CAGR, showing how buyers reward thermal comfort in both hot and cold climates. Heated options remain a staple in North America, while power adjusters form a bridge between economy and luxury lines, offering memory profiles and lumbar modules without complex HVAC integration.

Smart seats that track posture and vital signs are advancing quickly in premium EVs. Hyundai Transys packages low-energy carbon-fiber heaters, dynamic body-care algorithms, and tilt-away walk-in functions within the Kia EV9, proving a mass-production path for fully software-defined comfort. Suppliers are also embedding over-the-air-enabled control units, allowing future features unlock that spread revenue beyond the point of sale.

The Automotive Seat Market Report is Segmented by Material Type (Synthetic Leather, Fabric, and More), Technology (Standard (Manual) Seats, Powered Seats, and More), Sales Channel (OEM and Aftermarket), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Seat Type (Bench/Split-Bench Seats, Bucket Seats, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific leads with 46.40% revenue and a 3.69% CAGR outlook, fueled by China's electric-vehicle boom, India's fast-growing compact-SUV segment, and Japan's sustained investment in seat electronics. China is forecast to reach 45% EV penetration in new-car sales in 2025, keeping seat suppliers busy with lighter frames and integrated cooling designs. Indian policies that subsidize electric three-wheelers and delivery vans accelerate demand for durable, low-maintenance trim suited to high-usage duty cycles. Japanese innovators such as Toyota Boshoku unveil relaxation seats with swing-chair motion and personalized audio, demonstrating the region's push toward holistic passenger comfort.

Europe focuses on emissions reduction and recyclability. Regulations tighten material traceability and lifecycle carbon accounting, encouraging seats built from bio-based foams and easily separable covers. FORVIA's truck seat platform claims 40% lower CO2 than conventional designs, proving compliance can coexist with driver comfort. North America, characterized by high pickup and SUV share, shows rising standardization of ventilated and heated seats in mid-trim models. Suppliers leverage proximity to Detroit and Mexico fabrication hubs to localize metal stamping and cushion production, reducing logistics risk and meeting US-MCA regional-content rules.

The Middle East, Africa, and South America provide long-run expansion potential. Governments support local assembly to develop automotive ecosystems, creating opportunities for simplified, cost-efficient bench and jump seats that meet rugged-road requirements. Fleet purchases in ride-hailing and mini-bus sectors open demand for easy-clean synthetic leather and quick-swap seat modules that preserve uptime in environments with limited-service infrastructure.

- Adient PLC

- Lear Corporation

- Forvia SE

- Toyota Boshoku Corporation

- Magna International Inc.

- NHK Spring Co. Ltd

- Recaro Holding GmbH

- TS Tech Co. Ltd

- Tachi-S Co. Ltd

- Yanfeng Seating

- Hyundai Transys

- Gentherm Inc.

- Martur Fompak

- Grammer AG

- Freedman Seating

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising global light-vehicle production, especially SUVs

- 4.2.2 Growing consumer demand for powered, ventilated & massage seats

- 4.2.3 Automaker push for lightweight seats to meet CO2 targets

- 4.2.4 Electrified skateboard platforms enabling flexible cabin layouts

- 4.2.5 Mobility-as-a-Service fleets needing easy-clean, high-durability trim

- 4.2.6 AI-driven occupant-monitoring systems requiring smart sensor-laden seats

- 4.3 Market Restraints

- 4.3.1 Volatile prices of leather, foam & advanced polymers

- 4.3.2 Stringent safety & homologation testing costs

- 4.3.3 Slow refresh cycles for seat architectures at legacy OEMs

- 4.3.4 Rise of alternative comfort systems reducing demand for premium seats

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Material Type

- 5.1.1 Synthetic Leather

- 5.1.2 Genuine Leather

- 5.1.3 Fabric

- 5.1.4 Natural Fiber and Others

- 5.2 By Technology

- 5.2.1 Standard (Manual) Seats

- 5.2.2 Powered Seats

- 5.2.3 Ventilated Seats

- 5.2.4 Heated Seats

- 5.2.5 Massage Seats

- 5.2.6 Smart / AI-Integrated Seats

- 5.3 By Sales Channel

- 5.3.1 OEM

- 5.3.2 Aftermarket

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Medium and Heavy Commercial Vehicles

- 5.4.4 Two-Wheelers and Three-Wheelers

- 5.5 By Seat Type

- 5.5.1 Bench / Split-Bench Seats

- 5.5.2 Bucket Seats

- 5.5.3 Captain / Individual Seats

- 5.5.4 Child Safety Seats

- 5.5.5 Folding / Jump Seats

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Adient PLC

- 6.4.2 Lear Corporation

- 6.4.3 Forvia SE

- 6.4.4 Toyota Boshoku Corporation

- 6.4.5 Magna International Inc.

- 6.4.6 NHK Spring Co. Ltd

- 6.4.7 Recaro Holding GmbH

- 6.4.8 TS Tech Co. Ltd

- 6.4.9 Tachi-S Co. Ltd

- 6.4.10 Yanfeng Seating

- 6.4.11 Hyundai Transys

- 6.4.12 Gentherm Inc.

- 6.4.13 Martur Fompak

- 6.4.14 Grammer AG

- 6.4.15 Freedman Seating

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

汽车座椅市场:2026-2032年全球市场预测(按座椅类型、组件、材料类型、技术、车辆类型和最终用户划分)汽车智慧座椅市场:按组件、连接方式、座椅位置、技术、应用、车辆类型、最终用户和分销管道划分-2026-2032年全球市场预测

汽车座椅市场:2026-2032年全球市场预测(按座椅类型、组件、材料类型、技术、车辆类型和最终用户划分)汽车智慧座椅市场:按组件、连接方式、座椅位置、技术、应用、车辆类型、最终用户和分销管道划分-2026-2032年全球市场预测 2026年全球汽车座椅市场报告汽车皮革座椅市场:2026-2032年全球市场预测(按材料、价格范围、座椅覆盖率、座椅类别、应用和分销管道划分)汽车座椅通风系统市场:按组件、冷却能力、安装类型、控制方式、应用、最终用户和销售管道划分-2026-2032年全球市场预测

2026年全球汽车座椅市场报告汽车皮革座椅市场:2026-2032年全球市场预测(按材料、价格范围、座椅覆盖率、座椅类别、应用和分销管道划分)汽车座椅通风系统市场:按组件、冷却能力、安装类型、控制方式、应用、最终用户和销售管道划分-2026-2032年全球市场预测 汽车智慧座椅市场:策略性洞察与预测(2026-2031年)2026年全球汽车座椅框架市场报告汽车座椅马达市场:2026-2032年全球市场预测(按马达类型、电压、功能领域、应用、最终用户和分销管道划分)电动汽车座椅马达市场:按马达类型、功率范围、车辆类型、应用和销售管道划分-2026-2032年全球预测

汽车智慧座椅市场:策略性洞察与预测(2026-2031年)2026年全球汽车座椅框架市场报告汽车座椅马达市场:2026-2032年全球市场预测(按马达类型、电压、功能领域、应用、最终用户和分销管道划分)电动汽车座椅马达市场:按马达类型、功率范围、车辆类型、应用和销售管道划分-2026-2032年全球预测 汽车座椅市场规模、份额、趋势和预测:按材料、座椅类型、车辆类型、车辆动力来源和地区划分,2026-2034年

汽车座椅市场规模、份额、趋势和预测:按材料、座椅类型、车辆类型、车辆动力来源和地区划分,2026-2034年