|

市场调查报告书

商品编码

1938985

高压釜混凝土(AAC):市场占有率分析、产业趋势与统计、成长预测(2026-2031)Autoclaved Aerated Concrete (AAC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

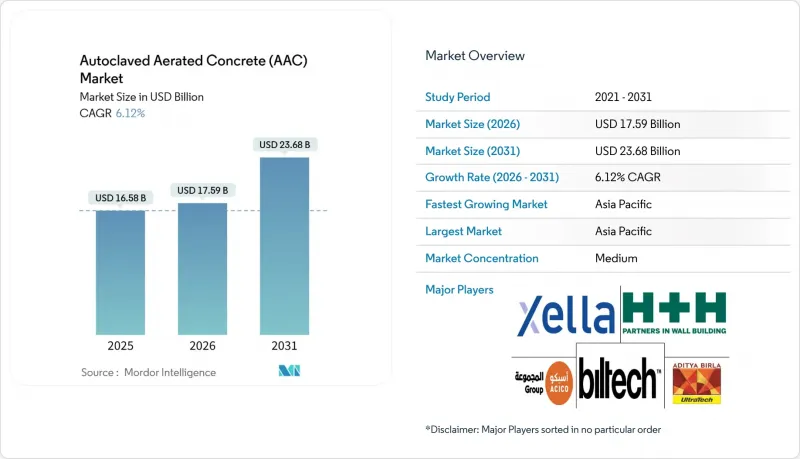

预计高压釜混凝土(AAC)市场将从 2025 年的 155.6 亿美元成长到 2026 年的 165 亿美元,到 2031 年将达到 221.1 亿美元,2026 年至 2031 年的复合年增长率为 6.04%。

更严格的绿建筑法规、对抗震结构日益增长的需求以及模组化建筑的快速普及推动了加气混凝土(AAC)市场的成长,这些因素都凸显了AAC的轻质和节能特性。虽然砌块仍然是传统砌体结构的主要组成部分,但随着预製构件加快施工速度,板材的应用正在迅速发展。亚太地区的需求量占全球近一半,这主要得益于都市化和基础设施投资;而北美和欧洲则受惠于其严格的能源和抗震规范。製造商正在扩大产能并实现工厂自动化,以满足激增的需求、优化成本结构并加强区域供应链。

全球高压釜混凝土(AAC)市场趋势与洞察

新建和维修工程的需求不断增长

随着新兴国家住宅和商业建筑的快速增长,轻质建筑材料对于降低地基荷载和缩短计划週期至关重要。加气混凝土(AAC)可减轻30-40%的重量,从而实现更轻的地基和更快的层间施工,这在人口密集的城市中心尤其重要。印度的住宅建设计划凸显了这一趋势,其本土製造商BigBloc Construction正在扩大产能,以满足都市区日益增长的住宅许可需求。加气混凝土也是维修工程的首选材料,因为其精准的砌块无需维修结构线,从而简化了施工流程。其四小时的耐火性能提高了商业维修的合规性,而其防霉基体在潮湿气候下尤其重要。这些因素共同推动了高压釜混凝土市场的持续成长。

严格的绿建筑标准和LEED认证正变得越来越普遍。

旨在减少蕴藏量排放的政策正在改变全球建筑材料的选择。美国政府为永续建筑材料基准计画提供的1.6亿美元资金,无疑支持了加气混凝土(AAC)的推广应用。美国环保署(EPA)的2024年低碳标籤为製造商提供了量化其气候优势的明确途径,从而增强了竞标在公共工程项目中的竞争力。类似的转型也正在欧洲发生,英国H+H公司致力于在2050年实现净零排放运营,以符合欧盟的脱碳目标。厚度为200毫米、隔热值R=1.43的加气混凝土,透过掺入再生飞灰,可降低10-20%的运作能耗,并符合循环经济标准。

与黏土/混凝土块相比,初始成本较高

阻碍加气混凝土(AAC)广泛应用的一个因素是其价格溢价,因为建筑商更重视采购价格而非全生命週期成本节约。然而,在印度主要都市区,传统红砖的价格已比加气混凝土高出约20%,促使人们转向更轻的替代材料。材料价格波动正在重塑比较标准。 2025年关税政策已使钢材价格上涨10-25%,混凝土价格上涨3-7%,削弱了加气混凝土的成本优势。在一些地区,由于当地工厂数量有限,交付价格也高出15-20%。宣传活动强调加气混凝土可节省30%的能源成本和减少劳动成本,这正逐步影响人们围绕总拥有成本(TCO)所做的采购决策。

细分市场分析

到2025年,砌块将占总销售额的54.10%,这反映了建筑商数十年来对砌块的熟悉程度以及其广泛的分销网络。同时,随着建筑商转向预製外墙,板材市场到2031年将以7.55%的复合年增长率成长。板材市场的蓬勃发展反映了建设产业日益工业化的趋势:工厂预製的模组可直接在现场使用,从而减少废弃物并加快施工速度。开发商更倾向于在高层住宅大楼中使用板材,因为较少的接缝可以提高隔热性能并减少热量损失。

在低层住宅领域,砌块结构仍占据主导地位,尤其是在劳动力充足且现场施工技术盛行的市场。然而,板材技术的创新动能丝毫没有减弱的迹象。钢筋混凝土墙板可作为承重墙,而导热係数仅为 0.11 W/mK 的屋顶模组则有助于实现零能耗建筑的目标。自动化锯切线和机器人搬运降低了板材的生产成本,推动了高压釜混凝土(AAC)市场从手工砌块铺设转向工业化板材组装。

区域分析

到2025年,亚太地区将占全球营收的46.40%,并在2031年之前以7.11%的复合年增长率加速成长。中国和印度将成为需求的中坚力量,这主要得益于大型住宅大型企划和国家基础设施规划。政府对低碳建筑方法的诱因进一步推动了加气混凝土(AAC)规范的采用。日本和韩国因其抗震性能而采用加气混凝土,而澳洲的住宅能源规范也支持其稳定推广。亚太地区原料的高度自给自足以及不断提高的自动化程度,使其单位成本保持竞争力,从而巩固了亚太地区的优势。

在北美,美国西部地区对建筑防火性能的要求以及各气候区日益严格的建筑围护结构法规,正推动着加气混凝土(AAC)的重新流行。美国环保署(EPA)的低碳含量标籤促进了公共采购,而加拿大修订后的《国家能源规范》也为其发展注入了动力。墨西哥的住宅奖励策略与全部区域的趋势相辅相成,共同推动了高压釜混凝土市场的强劲成长。

严格的碳排放目标正在推动欧洲成熟市场的成长。德国和英国正积极维修建筑改造,而北欧市场则加速向净零能耗标准转型。欧盟绿色交易的资金支持着工厂升级和新生产线的安装。在中欧和东欧,物流设施和资料中心的建设热潮带动了对防火隔热覆材的需求,创造了新的成长领域。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 新建和维修工程的需求不断增长

- 采用严格的绿建筑标准和LEED认证

- 政府对低碳材料的激励措施

- 模组化异地建造的兴起

- 对具有优异抗震性能的轻质砌块的需求

- 市场限制

- 初始成本高(与粘土砖和混凝土砖相比)

- 承重应用中的结构约束

- 铝粉发泡供应及价格波动

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依产品类型

- 堵塞

- 控制板

- 楣

- 瓦

- 其他(U型砖、地板/屋顶材料)

- 透过施工方法

- 现场砌筑工程

- 预製/模组化

- 透过使用

- 住宅

- 商业

- 产业

- 其他用途(道路、公用设施围护结构、隔音屏障)

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 澳洲和纽西兰

- ASEAN

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 北欧国家

- 波兰

- 荷兰

- 罗马尼亚

- 捷克共和国

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 以色列

- 卡达

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- ACICO Group

- AERCON AAC

- Asahi Kasei Corporation

- Bauroc AS

- Biltech Building Elements Limited

- BirlaNu Limited

- Eastland Building Materials Co., Ltd

- Eco Green

- Ecostone AAC

- H+H UK Limited

- JK Lakshmi Cement Ltd.

- Renacon

- SOLBET

- Starken AAC Sdn Bhd

- STT Turk Gazbeton

- Thomas Armstrong(Concrete Blocks)Ltd

- UAL Industries Limited

- UltraTech Cement Ltd.

- Xella International

第七章 市场机会与未来展望

The Autoclaved Aerated Concrete Market is expected to grow from USD 15.56 billion in 2025 to USD 16.5 billion in 2026 and is forecast to reach USD 22.11 billion by 2031 at 6.04% CAGR over 2026-2031.

Growth is fueled by tightening green-building mandates, rising demand for seismic-resilient structures, and the rapid adoption of modular construction, all of which highlight AAC's lightweight, energy-efficient profile. Blocks continue to dominate traditional masonry, yet panels are gaining momentum as prefabrication revamps project timelines. Asia-Pacific commands nearly half of global demand on the back of urbanization and infrastructure outlays, while North America and Europe capitalize on strict energy and seismic codes. Manufacturers are scaling capacity and automating plants to match demand spikes, improve cost structures, and strengthen regional supply chains.

Global Autoclaved Aerated Concrete (AAC) Market Trends and Insights

Growing Demand from New-Build & Renovation Construction

Surging residential and commercial starts in emerging economies have made lightweight materials indispensable because they lower foundation loads and shorten project cycles. AAC cuts dead weight by 30-40%, enabling slimmer foundations and quicker floor-to-floor progress, which is vital in dense city cores. India's housing drive illustrates the trend; domestic producer BigBloc Construction is expanding capacity to keep pace with elevated urban housing approvals. Renovation schemes also prefer AAC because its precision blocks streamline retrofits without reforging structure lines. Four-hour fire ratings boost compliance in commercial refurbishments, and its mold-proof matrix appeals in humid climates. Together, these factors underpin sustained Autoclaved Aerated Concrete market growth.

Stringent Green-Building Codes & LEED Adoption

Policies aimed at curbing embodied carbon are reshaping material selection worldwide. The US government's USD 160 million funding for sustainable-materials benchmarking explicitly encourages AAC uptake. EPA's 2024 low-carbon label gives manufacturers a clear route to quantify climate advantages, enhancing bid scores on public projects. Europe mirrors the shift; H+H UK is targeting net-zero operations by 2050, in line with EU decarbonization goals. With an R-value of 1.43 for 200 mm thickness, AAC delivers 10-20% operational energy savings and incorporates recycled fly ash, satisfying circular-economy criteria.

High Upfront Cost vs. Clay & Concrete Blocks

Perceptions of premium pricing hinder AAC's penetration where contractors prioritize purchase price over life-cycle savings. However, traditional red bricks recently became roughly 20% more expensive than AAC in key Indian metros, nudging buyers toward the lighter alternative. Material-price volatility is reshaping comparisons; 2025 tariffs elevated steel by 10-25% and concrete by 3-7%, eroding AAC's cost differential. Limited local plants in some regions still inflate delivered prices by 15-20%. Education campaigns stressing 30% energy-bill reductions and lower labor needs are gradually reframing procurement decisions around total cost of ownership.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Low-Carbon Materials

- Modular Off-Site Construction Uptake

- Volatile Supply & Price of Aluminum Powder Foaming Agent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blocks held 54.10% of 2025 revenue, reflecting decades of contractor familiarity and broad distribution networks. In parallel, panels are charting a 7.55% CAGR through 2031 as builders pivot toward prefabricated envelopes. The panel boom embodies the construction industry's industrialization push: factory-cut modules arrive field-ready, reducing waste and compressing schedules. Developers favor panels in tall residential towers because fewer joints mean tighter thermal envelopes and lower infiltration losses.

The blocks segment remains central to low-rise housing, especially in markets where labor is abundant and on-site techniques dominate. Yet panel innovation is relentless. Reinforced wall panels now handle load-bearing duties, and roof modules with thermal conductivity of 0.11 W/mK meet zero-energy-building targets. Automated saw lines and robotic handling have cut panel-fabrication costs, underpinning an Autoclaved Aerated Concrete market shift from craft-based block laying to industrial panel assembly.

The Autoclaved Aerated Concrete Market Report is Segmented by Product Type (Block, Panel, Lintel, Tile, Others), Construction Method (On-Site Masonry, Prefabricated/Modular), Application (Residential, Commercial, Industrial, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.40% of global revenue in 2025 and is accelerating at 7.11% CAGR to 2031. China and India anchor demand, driven by housing mega-projects and state infrastructure pipelines. Government incentives for low-carbon building methods further tip specifications toward AAC. Japan and South Korea adopt AAC for seismic safety, while Australia's home-energy codes sustain steady uptake. High regional self-sufficiency in raw materials and rising automation keep unit costs competitive, cementing Asia-Pacific's dominance.

North America is experiencing a renaissance in AAC usage, propelled by wildfire resilience requirements in the western United States and stricter building envelopes across climate zones. The EPA's low-embodied-carbon label is catalyzing public procurement, and Canada's national energy code revision amplifies momentum. Mexico's housing stimulus complements the regional picture, leading to a robust Autoclaved Aerated Concrete market trajectory.

Europe's mature landscape benefits from stringent carbon targets: Germany and the UK aggressively retrofit buildings, while Nordic markets edge toward near-zero-energy codes. EU Green Deal financing supports plant upgrades and new lines. Central and Eastern Europe provide white-space growth as booming logistics and data-center construction seek fire-safe, thermally efficient shells.

- ACICO Group

- AERCON AAC

- Asahi Kasei Corporation

- Bauroc AS

- Biltech Building Elements Limited

- BirlaNu Limited

- Eastland Building Materials Co., Ltd

- Eco Green

- Ecostone AAC

- H+H UK Limited

- JK Lakshmi Cement Ltd.

- Renacon

- SOLBET

- Starken AAC Sdn Bhd

- STT Turk Gazbeton

- Thomas Armstrong (Concrete Blocks) Ltd

- UAL Industries Limited

- UltraTech Cement Ltd.

- Xella International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing demand from new-build & renovation construction

- 4.2.2 Stringent green-building codes & LEED adoption

- 4.2.3 Government incentives for low-carbon materials

- 4.2.4 Modular off-site construction uptake

- 4.2.5 Demand for seismic-resilient lightweight blocks

- 4.3 Market Restraints

- 4.3.1 High upfront cost vs. clay & concrete blocks

- 4.3.2 Structural limitations in load-bearing applications

- 4.3.3 Volatile supply & price of aluminum powder foaming agent

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Block

- 5.1.2 Panel

- 5.1.3 Lintel

- 5.1.4 Tile

- 5.1.5 Others (U-blocks, floor/roof elements)

- 5.2 By Construction Method

- 5.2.1 On-site masonry

- 5.2.2 Prefabricated/modular

- 5.3 By Application

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Other Applications (roads, utility enclosures, noise-barrier walls)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Australia and New Zealand

- 5.4.1.6 ASEAN

- 5.4.1.7 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Nordic Countries

- 5.4.3.7 Poland

- 5.4.3.8 Netherlands

- 5.4.3.9 Romania

- 5.4.3.10 Czech Republic

- 5.4.3.11 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Israel

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 ACICO Group

- 6.4.2 AERCON AAC

- 6.4.3 Asahi Kasei Corporation

- 6.4.4 Bauroc AS

- 6.4.5 Biltech Building Elements Limited

- 6.4.6 BirlaNu Limited

- 6.4.7 Eastland Building Materials Co., Ltd

- 6.4.8 Eco Green

- 6.4.9 Ecostone AAC

- 6.4.10 H+H UK Limited

- 6.4.11 JK Lakshmi Cement Ltd.

- 6.4.12 Renacon

- 6.4.13 SOLBET

- 6.4.14 Starken AAC Sdn Bhd

- 6.4.15 STT Turk Gazbeton

- 6.4.16 Thomas Armstrong (Concrete Blocks) Ltd

- 6.4.17 UAL Industries Limited

- 6.4.18 UltraTech Cement Ltd.

- 6.4.19 Xella International

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment

蒸压加气混凝土市场(至 2035 年):依产品类型、应用、公司规模和地区划分的产业趋势和全球预测

蒸压加气混凝土市场(至 2035 年):依产品类型、应用、公司规模和地区划分的产业趋势和全球预测 高压釜轻质混凝土市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材质类型、製造流程、最终用户、安装类型

高压釜轻质混凝土市场分析及预测(至2035年):类型、产品、服务、技术、应用、形式、材质类型、製造流程、最终用户、安装类型 2026年全球高压釜气混凝土市场报告

2026年全球高压釜气混凝土市场报告 2025-2029年全球高压釜加气混凝土(AAC)市场

2025-2029年全球高压釜加气混凝土(AAC)市场 AAC生产线市场按产品类型、原材料、产能、自动化程度、设备类型和最终用户划分 - 全球预测 2026-2032

AAC生产线市场按产品类型、原材料、产能、自动化程度、设备类型和最终用户划分 - 全球预测 2026-2032 高压釜加气混凝土(AAC)市场规模、份额和成长分析(按类型、供应模式、成分、最终用途产业和地区划分)-产业预测,2026-2033年

高压釜加气混凝土(AAC)市场规模、份额和成长分析(按类型、供应模式、成分、最终用途产业和地区划分)-产业预测,2026-2033年 高压釜加气混凝土(AAC)-全球市占率及排名、总收入及需求预测(2025-2031年)高压釜轻质混凝土(ALC)板材:全球市场份额和排名、总收入和需求预测(2025-2031年)

高压釜加气混凝土(AAC)-全球市占率及排名、总收入及需求预测(2025-2031年)高压釜轻质混凝土(ALC)板材:全球市场份额和排名、总收入和需求预测(2025-2031年) 加气混凝土市场规模、份额和趋势分析报告:按混凝土类型、最终用途、地区和细分市场预测(2025-2033 年)按产品类型、应用、最终用途、通路、强度和密度高压釜混凝土市场-2025-2032年全球预测

加气混凝土市场规模、份额和趋势分析报告:按混凝土类型、最终用途、地区和细分市场预测(2025-2033 年)按产品类型、应用、最终用途、通路、强度和密度高压釜混凝土市场-2025-2032年全球预测