|

市场调查报告书

商品编码

1939011

铍:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Beryllium - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

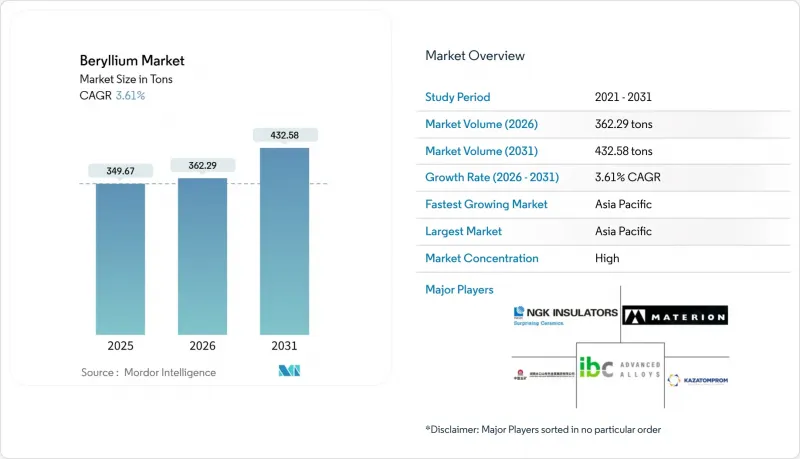

2025年铍市场价值为337.26吨,预计从2026年的349.67吨增加到2031年的418.86吨。

预计在预测期(2026-2031 年)内,复合年增长率将达到 3.68%。

其强劲成长得益于诸多特性,例如卓越的刚度重量比、优异的导热性和中子渗透性,这些特性使其成为国防、航太、电子和新兴清洁能源系统的关键材料。 5G基础设施的扩展、可重复使用火箭计划以及先进电力电子平台的进步正在推动市场需求,而更严格的职业暴露法规以及哈萨克和中国的供应链集中度则对成本和安全性构成压力。由于亚太地区的消费驱动力强劲,美国生产商的策略整合正在增强国内市场的韧性。竞争优势体现在合金创新、粉末冶金工艺和快速原型製造能力等方面,旨在为高价值应用提供轻盈耐用的零件。

全球铍市场趋势与洞察

铍铜合金在5G和毫米波基地台射频滤波器的应用日益广泛

全球5G的部署正推动对高频射频连接器前所未有的需求,而铜铍因其优异的电气和机械性能以及耐腐蚀性,是此类连接器的必要材料。毫米波基地台每个节点使用的铍铜比4G设备更多,总消耗量翻了一番。加工技术的不断进步使得生产24GHz以上系统所需的超薄精密带材成为可能。 5G基础设施被列为关键国家基础设施,从供应安全的角度来看,这进一步提升了铍市场的战略意义。虽然亚太地区仍然是需求中心,但北美和欧洲的营运商坚持严格的规格要求,优先考虑高纯度合金。

可重复使用运载火箭对轻质、高刚性结构的需求日益增长

从一次性运载火箭系统向可重复使用运载火箭系统的过渡,依赖能够承受反覆极端温度和振动而不增加质量的材料。铍的刚性重量比是钢的六倍,但重量却只有钢的四分之一,这使得製造轻型光学平台、感测器支架和结构面板成为可能。铍铝复合材料,例如 AlBeMet 和 Beralcast,在温度波动下具有尺寸稳定性,詹姆斯韦伯太空望远镜的镜面组件证明了这一点。随着商业发射业者每年进行数百次发射,对耐用铍零件的需求也随之成长。

严格的职业暴露限值和不断上涨的合规成本

美国职业安全与健康管理局 (OSHA) 已将允许暴露限值从 2 μg/m³ 降至 0.2 μg/m³,要求生产商实施更严格的通风、隔离措施和医疗监测系统,从而增加了单位成本。欧洲 REACH 法规体系下也实施了类似的规定,形成了一个更严格的法规环境。小规模加工商难以承担这些成本,加速了产业整合,提高了进入门槛,限制了整体供应成长。

细分市场分析

截至2025年,合金将占据铍市场72.86%的份额,预计到2031年将以3.95%的复合年增长率成长,这巩固了其在高性能平台中的核心地位。在这一类别中,铜铍合金在通讯连接器领域占据主导地位,而铝铍金属基复合材料则可用于航太结构的轻量化。由于合金成分可以针对强度、导电性和热性能进行调整,製造商正投入大量研发预算来开发新的合金成分,以应对新的设计限制。

纯金属仍广泛应用于核反射器和空间光学元件,因为合金化会降低其抗中子和抗热性能。氧化铍陶瓷在高密度功率模组中扮演着独特而重要的角色,这类模组需要极高的导热性。粉末冶金和热等等向性技术的进步使得製造十年前无法实现的复杂形状成为可能,这凸显了合金技术的进步正在推动铍市场的整体成长。

铍市场报告按产品类型(合金、金属、陶瓷及其他)、终端用户产业(工业零件、汽车、医疗、航太与国防、石油、天然气及其他能源等)和地区(亚太地区、北美、欧洲、南美以及中东和非洲)进行细分。市场预测以公吨为单位。

区域分析

预计到2025年,亚太地区将占全球产量的37.62%,到2031年将以4.08%的复合年增长率成长,其中中国在电子产品生产和5G基地台部署方面主导。国内加工商将上游精矿与下游合金化製程结合,维持近乎封闭的供应链,以保护本地消费者免受国际市场波动的影响。日本和韩国透过汽车电气化和高精度半导体製造设备创造了巨大的需求,而印度不断扩展的航太计画正在推动区域航太需求。

北美拥有马特里恩公司位于犹他州和俄亥俄州的综合生产基地,这是全球唯一的从矿山到冶炼的一体化製造系统,有助于提升供应链的韧性。成熟的航太和国防工业确保了稳定的基本负载消费,而《通膨控制法案》的激励措施则支持了国内电动车电池和电力电子产品的製造,这些製造都需要氧化铍基板。加拿大和墨西哥则透过航太组装和新兴的电动车出口中心,为北美市场带来渐进式成长。

欧洲在严格的职业法规与强劲的应用需求之间寻求平衡。电动车的快速普及和可再生能源产能的不断增长,推动了对高性能温度控管材料的需求,其中铍合金和陶瓷尤为突出。 NGK-Berylco法国公司正率先采用符合欧盟永续性目标的低碳加工製程。中东/非洲和南美市场规模仍然小规模,但像Beryltec卢安达这样的新加工厂标誌着公司在地域多元化方面迈出了第一步。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 铍铜合金在5G和毫米波基地台射频滤波器的应用日益广泛

- 可重复使用运载火箭对轻质、高刚性结构的需求日益增长

- 先进电动车电力电子装置对温度控管材料的需求日益增长

- 国防现代化计画推动了对卫星、飞弹导引系统和光学感测器的需求。

- 小型模组化反应器(SMR)对中子渗透性铍反射器的需求日益增长

- 市场限制

- 严格的职业暴露限值和不断上涨的合规成本

- 哈萨克和中国铍精矿供应不稳定

- 加速铝和钛金属基复合材料作为替代品的研发

- 价值链分析

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 合金

- 金属

- 陶瓷

- 其他产品类型

- 按最终用户行业划分

- 工业部件

- 车

- 卫生保健

- 航太与国防

- 石油、天然气和其他能源

- 电子与通信

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 俄罗斯

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- American Beryllia Inc.

- American Elements

- Belmont Metals

- Hunan Shuikoushan Nonferrous Metals Group Co., Ltd.

- IBC Advanced Alloys

- JSC Ulba Metallurgical Plant(JSC NAC Kazatomprom)

- Materion Corporation

- NGK INSULATORS, LTD.

- Rockland Resources Ltd.

- Texas Mineral Resources Corp.

- Tropag Oscar H. Ritter Nachf GmBH

- Xiamen Beryllium Copper Technologies Co. , Ltd.

- Xinjiang Xinxin Mining Industry Co. Ltd

第七章 市场机会与未来展望

The Beryllium Market was valued at 337.26 tons in 2025 and estimated to grow from 349.67 tons in 2026 to reach 418.86 tons by 2031, at a CAGR of 3.68% during the forecast period (2026-2031).

Robust growth stems from the metal's unmatched stiffness-to-weight ratio, superior thermal conductivity, and neutron transparency that position it as a linchpin material across defense, aerospace, electronics, and nascent clean-energy systems. Rising 5G infrastructure roll-outs, reusable launch vehicle programs, and advanced power-electronics platforms elevate demand, while tightening occupational-exposure rules and supply-chain concentration in Kazakhstan and China create cost and security pressures. Strategic integration efforts by U.S. producers strengthen domestic resilience even as Asia-Pacific leads consumption. Competitive differentiation centers on alloy innovation, powder-metallurgy processing, and rapid-prototyping capability that deliver lighter, more durable components for high-value applications.

Global Beryllium Market Trends and Insights

Rising Adoption of Be-Cu Alloys in 5G And mm-wave Base-Station RF Filters

Global 5G roll-outs drive unprecedented volumes of high-frequency RF connectors that mandate copper-beryllium for its simultaneous electrical, mechanical, and corrosion-resistant performance. Each mmWave base station uses more Be-Cu per node than 4G equipment, multiplying overall consumption. Continuous processing improvements now yield ultra-thin precision strip essential for 24 GHz-plus systems. Because 5G infrastructure is classified as critical national infrastructure, security-of-supply considerations amplify strategic interest in the beryllium market. Asia-Pacific remains the demand epicenter, yet North American and European operators maintain stringent specifications that favor high-purity alloys.

Growing Requirement for Lightweight, High-Stiffness Structures in Reusable Launch Vehicles

The shift from expendable to reusable launch systems hinges on materials that survive repeated thermal and vibrational extremes without mass penalties. Beryllium's specific stiffness is six times that of steel at one-quarter the weight, enabling lighter optical benches, sensor mounts, and structural panels. Beryllium-aluminum composites such as AlBeMet and Beralcast deliver dimensional stability across temperature swings, validated by the performance of the James Webb Space Telescope mirror segments. As commercial launch providers target hundreds of sorties per year, demand for durable beryllium components scales in tandem.

Stringent Occupational-Exposure Limits and Rising Compliance Costs

OSHA cut permissible exposure thresholds from 2 µg/m3 to 0.2 µg/m3, obligating producers to install enhanced ventilation, isolation, and medical-surveillance systems that elevate unit costs. Europe applies comparable restrictions under REACH authorization, further tightening the regulatory envelope. Smaller processors struggle to absorb these expenses, accelerating industry consolidation and raising entry barriers that constrain overall supply expansion.

Other drivers and restraints analyzed in the detailed report include:

- Escalating Demand for Thermal-Management Materials in Advanced EV Power Electronics

- Defense Modernization Programs Boosting Satellite, Missile-Seeker and Optical-Sensor Volumes

- Volatility of Beryllium Concentrate Supply from Kazakhstan and China

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Alloys captured 72.86% of the beryllium market share in 2025 and are projected to expand at a 3.95% CAGR through 2031, confirming their central role in high-performance platforms. Within this category, copper-beryllium alloys dominate telecommunications connectors, while aluminum-beryllium metal-matrix composites unlock weight savings in aerospace structures. Because alloy formulations can be tuned for strength, conductivity, or thermal properties, producers devote significant research and development budgets to new compositions that address emerging design constraints.

Pure metal continues to serve nuclear reflectors and space-optics segments where alloying would impair neutron or thermal performance. Beryllium-oxide ceramics fill niche but critical positions in high-density power modules that require extreme thermal conductivity. Powder-metallurgy advances and hot-isostatic-pressing routes enable intricate geometries unprecedented a decade ago, underscoring how alloy progress propels overall beryllium market momentum.

The Beryllium Report is Segmented by Product Type (Alloys, Metals, Ceramics, and Other Product Types), End-User Industry (Industrial Components, Automotive, Healthcare, Aerospace and Defense, Oil and Gas and Other Energy, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific generated 37.62% of 2025 volume and is forecast to log a 4.08% CAGR through 2031 as China spearheads electronics production and 5G base-station deployment. Domestic processors integrate upstream concentrate and downstream alloying, sustaining a largely closed supply loop that buffers local consumers from international volatility. Japan and South Korea contribute sizeable volumes through automotive electrification and high-precision semiconductor tooling, while India's expanding space program lifts regional aerospace demand.

North America anchors supply-chain resilience with the world's only fully integrated mine-to-mill operation at Materion's Utah-Ohio complex. Mature aerospace and defense sectors ensure stable base load consumption, and the Inflation Reduction Act incentives bolster domestic EV battery and power-electronics manufacturing that rely on Be-O substrates. Canada and Mexico add incremental growth via aerospace assembly and emerging EV export hubs.

Europe balances stringent occupational regulations with robust application demand. The continent's accelerated EV adoption and renewable-energy build-out intensify requirements for high-performance thermal-management materials, favoring beryllium alloys and ceramics. NGK Berylco France pioneers lower-carbon processing routes aligned with EU sustainability goals. While Middle East-Africa and South America remain smaller markets, new processing ventures such as BerylTech Rwanda illustrate early steps toward geographic diversification.

- American Beryllia Inc.

- American Elements

- Belmont Metals

- Hunan Shuikoushan Nonferrous Metals Group Co., Ltd.

- IBC Advanced Alloys

- JSC Ulba Metallurgical Plant (JSC NAC Kazatomprom)

- Materion Corporation

- NGK INSULATORS, LTD.

- Rockland Resources Ltd.

- Texas Mineral Resources Corp.

- Tropag Oscar H. Ritter Nachf GmBH

- Xiamen Beryllium Copper Technologies Co. , Ltd.

- Xinjiang Xinxin Mining Industry Co. Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Be-Cu Alloys in 5G and mm-wave Base-Station RF Filters

- 4.2.2 Growing Requirement for Lightweight, High-Stiffness Structures in Reusable Launch Vehicles

- 4.2.3 Escalating Demand for Thermal Management Materials in Advanced EV Power Electronics

- 4.2.4 Defense Modernization Programs Boosting Satellite, Missile-Seeker and Optical Sensor Volumes

- 4.2.5 Emerging Need for Neutron-Transparent Be Reflectors in Small Modular Reactors (SMRs)

- 4.3 Market Restraints

- 4.3.1 Stringent Occupational?Exposure Limits and Rising Compliance Costs

- 4.3.2 Volatility of Beryllium Concentrate Supply from Kazakhstan and China

- 4.3.3 Accelerating Research and Development on Aluminum and Titanium Metal-Matrix Composites as Substitutes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Alloys

- 5.1.2 Metals

- 5.1.3 Ceramics

- 5.1.4 Other Product Types

- 5.2 By End-user Industry

- 5.2.1 Industrial Components

- 5.2.2 Automotive

- 5.2.3 Healthcare

- 5.2.4 Aerospace and Defense

- 5.2.5 Oil and Gas and Other Energy

- 5.2.6 Electronics and Telecommunication

- 5.2.7 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 American Beryllia Inc.

- 6.4.2 American Elements

- 6.4.3 Belmont Metals

- 6.4.4 Hunan Shuikoushan Nonferrous Metals Group Co., Ltd.

- 6.4.5 IBC Advanced Alloys

- 6.4.6 JSC Ulba Metallurgical Plant (JSC NAC Kazatomprom)

- 6.4.7 Materion Corporation

- 6.4.8 NGK INSULATORS, LTD.

- 6.4.9 Rockland Resources Ltd.

- 6.4.10 Texas Mineral Resources Corp.

- 6.4.11 Tropag Oscar H. Ritter Nachf GmBH

- 6.4.12 Xiamen Beryllium Copper Technologies Co. , Ltd.

- 6.4.13 Xinjiang Xinxin Mining Industry Co. Ltd

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

铍市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年)

铍市场规模、份额和趋势分析报告:按应用、地区和细分市场预测(2026-2033 年) 氢氧化铍市场规模、份额及成长分析(依等级、应用、最终用户及地区划分)-2026-2033年产业预测

氢氧化铍市场规模、份额及成长分析(依等级、应用、最终用户及地区划分)-2026-2033年产业预测 铍市场规模、份额和成长分析(按等级、应用、形态、纯度和地区划分)-2026-2033年产业预测

铍市场规模、份额和成长分析(按等级、应用、形态、纯度和地区划分)-2026-2033年产业预测 全球铍市场-2025-2030年预测全球铍矿开采市场:市场规模、份额、趋势分析(按应用、最终用途和地区划分)、细分市场预测(2025-2033年)

全球铍市场-2025-2030年预测全球铍矿开采市场:市场规模、份额、趋势分析(按应用、最终用途和地区划分)、细分市场预测(2025-2033年) 铍市场按产品类型、最终用途产业、形态、纯度和应用划分-2025-2032年全球预测

铍市场按产品类型、最终用途产业、形态、纯度和应用划分-2025-2032年全球预测 2032 年铍市场预测:按产品、形态、应用和地区分類的全球分析

2032 年铍市场预测:按产品、形态、应用和地区分類的全球分析 2025-2033年铍市场报告(依产品类型、最终用途产业和地区)

2025-2033年铍市场报告(依产品类型、最终用途产业和地区)