|

市场调查报告书

商品编码

1939012

精密农业:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Precision Farming - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

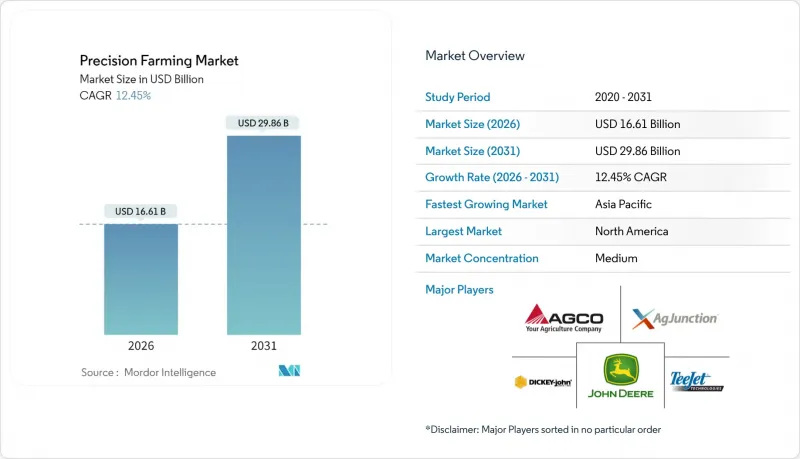

预计到 2026 年,精密农业市场规模将达到 166.1 亿美元,高于 2025 年的 147.7 亿美元。

预计到 2031 年,该市场规模将达到 298.6 亿美元,2026 年至 2031 年的复合年增长率为 12.45%。

卫星物联网卫星群、GNSS引导的自动驾驶系统以及人工智慧驱动的自主设备的广泛应用,正在扩大数位农业的范围,并将排碳权奖励转化为实际的投资回报。约翰迪尔与SpaceX合作,在通讯盲区提供亚英寸级遥测技术;AGCO与PTx Trimble合资,为混合车队开发改造解决方案;以及美国农业部的“气候智能型商品计划”,都在强化技术循环,推动可变投入优化。虽然硬体仍占据大部分支出,但软体和边缘人工智慧分析正以两位数的速度迎头赶上,反映出该产业正从数据收集转向即时决策自动化。北美仍保持最大的区域份额,而亚太地区则经历了最高的复合年增长率,这主要得益于印度的智慧农业生态系统和中国的精密农业政策。

全球精密农业市场趋势与洞察

在大型农场引入GNSS自动驾驶系统

大型农场(超过1000公顷)的GNSS自动驾驶系统采用率显着高于中型农场(52%),达70%。这一趋势是推动精密农业市场发展的关键因素,约翰迪尔的StarFire 7000接收器能够接收更多卫星频段并提高收敛速度。 SpaceX的Starlink即使在没有行动电话网路覆盖的区域也回程传输导航数据,使操作员能够昼夜不停地进行自动驾驶。 AGCO的OutRun改装套件与其他拖拉机相容,正在推动混合型车辆转向系统的升级。在劳动力日益短缺的情况下,机器人技术能够实现完美的直线行驶、防止重迭作业并节省柴油,这使其作为稀缺操作员的替代方案更提案。燃油成本的节省和运作效率的提高进一步提升了投资报酬率,延长了机器在有限的播种季节的运作距离。

频谱/热感无人机感测器的成本迅速下降

目前全球已有超过30万架农业无人机作业,覆盖超过5亿公顷的农地。大疆创新(DJI)的Mavic 3 频谱无人机价格已降至以往只有大型农场才能负担得起的水平。在蒙大拿州的麦田试验表明,配备WEED-IT视觉系统的定点喷洒无人机可将除草剂用量减少90%至95%。感测器小型化降低了有效载荷重量,并将飞行时间延长了一倍,同时保持了测量叶绿素和冠层湿度所需的光谱解析度。巴西和美国放宽了超视距飞行的作业范围,加速了其在大型农田的应用。人工智慧驱动的异常检测技术能够比肉眼提前一周检测到营养胁迫,使农民能够在产量损失发生之前采取措施。

多个製造商的机器之间资料互通性的挑战

大约73%的农民使用来自多个製造商的拖拉机、播种机和喷药机,这造成了资料孤岛,阻碍了端到端的分析。 OGC SensorThings API承诺为地理空间和机械资料提供通用封装,但专有檔案格式和不同的CAN汇流排通讯协定阻碍了无缝资料流。 AGCO和Trimble的合资企业PTx承诺提供与品牌无关的转向和数据同步,但改造旧设备成本高昂,且需要经销商的专业知识。欧洲推动开放标准和MQTT传输层是一个积极的征兆,但小型供应商由于担心产品同质化,进展缓慢。如果没有更深入的集成,农民将继续依赖U盘和云端门户,从而限制了完全自主化可能带来的生产力提升。

细分市场分析

导航系统将持续维持领先地位,2025年将占据精密农业市场37.45%的份额。强大的GNSS接收器机械设备能够以亚英寸级的精度在复杂地形中导航。受化肥和农药价格上涨推动精准施肥的驱动,变数施肥技术(VRT)精密农业市场预计到2031年将以13.55%的复合年增长率增长。无人机遥感探测利用低成本的频谱设备,大疆创新(DJI)报告称,将施肥地图与处方喷雾器连接起来,已使农药用量减少了67.78%。随着创业投资资金转向边缘人工智慧平台,机器人技术正获得越来越多的关注。 Four Growers和Bonsai Robotics已总合筹集2,400万美元,用于在50万英亩的土地上实现收割作业的自动化。卫星物联网为该技术平台提供了补充,可以传输来自没有行动电话覆盖的田地的感测器数据,并不断更新自主模组的模型。

边缘运算和云端分析协同工作:边缘硬体即时处理影像串流,而云端引擎则分析季节性模式。约翰迪尔的第二代自动驾驶技术堆迭整合了这两层,目标是在本世纪末实现玉米和大豆的完全自动驾驶。农民越来越倾向于使用混合型设备,而不是只选择单一品牌;AGCO公司凭藉其OutRun套件抓住了这一变化,该套件无需更换高成本的拖拉机。有鑑于这些趋势,能够将开放API与硬体无关组件结合的技术供应商最有优势抓住面积扩张所带来的机会。

到2025年,硬体将占精密农业市场51.20%的份额,涵盖感测器、控制器、无人机和自主平台。然而,随着边缘人工智慧在几秒钟内(即使在网路中断的情况下)提供可操作的处方笺,软体收入正以13.40%的复合年增长率成长。感测器正变得小规模农场也能安装高密度的土壤湿度网格并创建可变灌溉地图。像约翰迪尔的G5-Plus这样的显示器增加了乙太网路接口,可以将更丰富的资料集从农机具传输到驾驶室。车载电脑正在将GNSS、机器视觉和遥测功能整合到单一基板,从而显着降低自主迴路的延迟。

随着营运商越来越依赖第三方合作伙伴进行软体修补和即时网路威胁监控,精密农业託管服务的市场规模预计将会扩大。 CNH 和 Raven 的数据分析套件利用人工智慧驱动的选择性喷洒技术,可将除草剂用量减少 77%。卫星回程传输确保作业期间的处方同步,这对于 77% 缺乏 4G 网路覆盖的农田来说至关重要。随着硬体利润率的下降,供应商正寻求透过捆绑更新、演算法和排碳权报告仪表板的订阅模式来获取经常性收入。

区域分析

北美地区预计到2025年将保持41.15%的市场份额,这主要得益于成熟的全球导航卫星系统(GNSS)网路、完善的经销商体係以及允许碳排放项目进行数位化记录的法规环境。与新兴地区相比,北美地区的成长率将保持平稳,部分原因是2025年农民意向调查显示,在商品价格波动的情况下,农民会采取谨慎的资本规划。然而,旧款显示器的积极更新换代以及车队自主性的提升将继续支撑市场需求。

亚太地区精密农业市场成长最快,达到13.95%,这主要得益于印度智慧农业市场的蓬勃发展(预计到2028年将达到8.8621亿美元)以及中国对数位农业的政策支持。政府对卫星星系、低成本无人机和农村宽频的投资正在推动小规模农户采用精准农业技术。 2024年,超过12亿美元的创业投资将用于自动化果园喷药机和农业金融科技信用评分系统,将投入资金与感测器检验的田间数据结合。在澳大利亚,自动驾驶田间作业车队正在缓解长期的劳动力短缺问题,并逐步扩大耕地面积。

欧洲正稳步推进环境法规,要求到2030年将化学品使用量减少50%,并将精准喷洒作为合规手段。德国的一项试验研究证实,在不影响产量的情况下,农药使用量可减少10%至20%,这大大增强了农民的信心。拉丁美洲的精准喷洒普及率参差不齐。巴西和阿根廷因干旱造成的收入损失导致2024年拖拉机销量下降了14%,而无人机喷洒在放鬆管制后迅速发展。中东和非洲仍处于精准喷洒的早期阶段。卫星物联网是撒哈拉以南非洲农民的生命线,该地区的即时动态定位(RTK)网路覆盖率仍停滞在40%。然而,缺乏经济性和技术限制了其普及。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 大型农场快速采用GNSS自动驾驶系统

- 频谱和热成像无人机感测器的成本迅速下降

- 政府碳信用计画奖励可变比例的碳排放减排

- 卫星物联网卫星群整合实现亚英寸级精度现场遥测

- 农场保险折扣引入了基于人工智慧的风险评分

- 创业投资资金从农场管理SaaS转向边缘人工智慧机器人

- 市场限制

- 多种品牌机器之间的资料互通性差距

- 针对农业营运技术网路的农村网路安全威胁

- 撒哈拉以南非洲的RTK网路覆盖范围趋于稳定

- 农民抵制演算法决策和自主权丧失

- 产业生态系分析

- 监管环境

- 技术展望

- 波特五力分析

- 买方的议价能力

- 供应商的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过技术

- 导航系统

- GNSS/GPS

- GIS

- 可变工作技术

- 可变肥料

- 可变播种

- 可变农药

- 遥感探测

- 无人机和无人驾驶飞行器(UAV)

- 机器人和自主设备

- 边缘和云端分析平台

- 其他技术

- 导航系统

- 按组件

- 硬体

- 感测器和致动器

- 控制器和显示器

- 机上计算与连接

- 软体

- 农业管理SaaS

- 数据分析与人工智慧

- 服务

- 整合与咨询

- 託管服务

- 硬体

- 透过使用

- 产量监测

- 可变工作应用

- 田间测绘

- 土壤和作物健康监测

- 灌溉管理

- 作物巡查

- 收割自动化和物流

- 其他用途

- 按农场规模

- 小规模农场(少于100公顷)

- 中型农场(100-1000公顷)

- 大型农场(超过1000公顷)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 荷兰

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 澳洲

- 韩国

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 奈及利亚

- 肯亚

- 其他非洲地区

- 中东

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Deere and Company

- Trimble Inc.

- AGCO Corporation

- CNH Industrial NV

- Raven Industries

- Topcon Positioning Systems

- Lindsay Corporation

- TeeJet Technologies

- DICKEY-john

- BASF Digital Farming(xarvio)

- Yara International ASA

- Climate Corp(Bayer)

- Hexagon Agriculture

- CropX Technologies

- DJI Agriculture

- Farmers Edge

- Granular

- Ag Leader Technology

- Kubota Smart Agri

- Sentera

第七章 市场机会与未来展望

Precision Farming market size in 2026 is estimated at USD 16.61 billion, growing from 2025 value of USD 14.77 billion with 2031 projections showing USD 29.86 billion, growing at 12.45% CAGR over 2026-2031.

Satellite IoT constellations, GNSS-guided auto-steering, and AI-enabled autonomous equipment are widening digital farming's addressable base and translating carbon-credit incentives into tangible return on investment. John Deere's collaboration with SpaceX for sub-inch telemetry in cellular dead zones, AGCO's PTx Trimble joint venture for mixed-fleet retrofits, and the USDA's Climate-Smart Commodities program are reinforcing a technology cycle that rewards variable-rate input optimization. Hardware still dominates spending, yet software and edge-AI analytics are outpacing with double-digit growth, mirroring the industry shift from data collection to real-time decision automation. North America retains the largest regional share, while Asia Pacific delivers the fastest CAGR on the back of India's smart-ag ecosystem and China's precision farming policy mandates.

Global Precision Farming Market Trends and Insights

GNSS-Enabled Auto-Steering on Large Farms

Adoption of GNSS auto-steering has reached 70% on farms over 1,000 ha versus 52% on midsize holdings, a trend increasingly shaping the precision farming market, aided by John Deere's StarFire 7000 receiver that locks onto more satellite bands for faster convergence. SpaceX Starlink backhauls the guidance data where cellular networks fail, letting operators run autonomous passes throughout the day and night. AGCO's OutRun retrofit kit democratizes steering upgrades for mixed fleets, supporting tractors from rival brands. Labor shortages heighten the value proposition by substituting scarce operators with robotics that maintain perfectly straight rows, suppress overlap, and conserve diesel. Return on investment is amplified through reduced fuel costs and higher field-hour utilization that push machinery farther during tight planting windows.

Rapid Cost Declines in Multispectral/Thermal Drone Sensors

More than 300,000 agricultural drones now treat over 500 million ha worldwide, with DJI's Mavic 3 Multispectral priced below the threshold once reserved for large farms. Farm trials on Montana wheat show 90-95% herbicide savings when spot-spray drones are paired with WEED-IT vision systems. Sensor miniaturization has lowered payload weight, doubling flight endurance while preserving spectral resolution for chlorophyll and canopy moisture readings. Regulatory easing in Brazil and the United States has widened the operational envelope for beyond-visual-line-of-sight flights, accelerating adoption on broad-acre crops. AI-enabled anomaly detection now flags nutrient stress a week sooner than the naked eye, letting growers intervene before yield loss sets in.

Data-Interoperability Gaps Among Mixed-Brand Machinery

Roughly 73% of growers operate tractors, planters, and sprayers from multiple OEMs, creating data silos that handicap end-to-end analytics. The OGC SensorThings API promises a universal wrapper for geospatial and machinery data, yet proprietary file formats and differing CAN bus protocols block seamless flows. AGCO's PTx Trimble venture pledges brand-agnostic steering and data sync, but retrofits on legacy rigs are costly and require dealership expertise. Europe's push for open standards and MQTT transport layers is a positive signal, though adoption lags smaller vendors who fear commoditization. Without convergence, farmers continue to juggle USB sticks and cloud portals, capping the productivity gains that full autonomy could deliver.

Other drivers and restraints analyzed in the detailed report include:

- Carbon-Credit Schemes Rewarding Variable-Rate Input Cuts

- Satellite IoT Constellations for Sub-Inch Telemetry

- Rural Cybersecurity Threats Targeting Farm OT Networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Guidance Systems held the leading 37.45% precision farming market share in 2025, sustained by robust GNSS receivers that steer machinery to sub-inch paths under variable terrain. The precision farming market size for Variable-Rate Technology is forecast to grow at a 13.55% CAGR through 2031, driven by rising fertilizer and chemical prices that incentivize targeted application. Drone-based remote sensing leverages cheaper multispectral payloads, with DJI reporting a 67.78% cut in chemical volumes when maps feed prescription sprayers. Robots are gaining traction as venture funding pivots to edge-AI platforms; Four Growers and Bonsai Robotics collectively raised USD 24 million to automate harvesting on 500,000 acres. Satellite IoT rounds out the stack, relaying sensor inputs from fields outside cellular reach so models stay current for autonomy modules.

Edge and cloud analytics work in tandem: edge hardware processes vision streams in real time, while cloud engines crunch seasonal patterns. John Deere's second-generation autonomy stack merges both layers to target full corn and soybean autonomy by decade's end. Farmers increasingly prefer mixed-fleet retrofits over single-brand replacements, a shift AGCO capitalized on with its OutRun kit that omits a high-cost tractor swap. Given these dynamics, technology suppliers who pair open APIs with hardware-agnostic components are best positioned to capture incremental acreage.

Hardware captured 51.20% of the precision farming market in 2025, covering sensors, controllers, drones, and autonomous platforms. Yet, software revenue is climbing at a 13.40% CAGR as edge-AI delivers actionable prescriptions within seconds, even when the network drops. Sensors have shrunk to postage-stamp footprints, letting small farms afford dense soil-moisture grids that feed variable-rate irrigation maps. Displays like John Deere's G5-Plus add Ethernet to pass richer datasets from implements back to the cab. On-board computers integrate GNSS, machine vision, and telemetry onto a single board, slashing latency for autonomy loops.

The precision farming market size for managed services is set to widen as operators lean on third-party partners to patch software and monitor cyber threats in real time. Data analytics suites from CNH and Raven trim herbicide by 77% with AI-directed selective spraying. Satellite backhaul ensures prescriptions sync during fieldwork, a crucial fail-safe for 77% of cropland without 4G. As hardware margins compress, vendors seek recurring revenue through subscriptions that bundle updates, algorithms, and carbon-credit reporting dashboards.

The Precision Farming Market Report is Segmented by Technology (Guidance Systems, Remote Sensing, Variable-Rate Technology, Drones and UAVs, and More), Component (Hardware, Software, and Services), Application (Yield Monitoring, Variable-Rate Application, Field Mapping, Soil and Crop Health Monitoring, and More), Farm Size (Small, Medium, and Large Farms), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.15% regional share in 2025, aided by mature GNSS networks, an established dealer ecosystem, and a regulatory environment that recognizes digital records for carbon programs. The market has plateaued in growth rate relative to emerging regions, partly because 2025 farmer sentiment surveys show cautious capital plans amid volatile commodity prices. Nevertheless, active replacement cycles for legacy displays and expansion into full-machine autonomy should preserve the continent's demand floor.

The Asia-Pacific region recorded the fastest growth rate of 13.95% in the precision farming market, propelled by India's smart-ag market, projected to reach USD 886.21 million by 2028, and China's policy mandates around digital agriculture. Government-funded satellite constellations, low-cost drones, and rural broadband investments underpin adoption across smallholder plots. Venture capital flows of more than USD 1.2 billion in 2024 concentrated on automated orchard sprayers and agri-fintech credit scoring that ties input loans to sensor-verified field data. Australia adds incremental acreage with autonomous broad-acre fleets that alleviate chronic labor shortages.

Europe advances steadily under environmental legislation requiring a 50% cut in chemicals by 2030, positioning precision spraying as a compliance lever. Field trials in Germany confirm 10-20% pesticide reductions without yield sacrifice, bolstering farmer confidence. Latin America's adoption pace diverges: Brazil and Argentina slowed tractor purchases by 14% in 2024 due to drought-linked income declines, yet accelerated drone spraying after regulatory relaxation. The Middle East and Africa remain early in the curve; satellite IoT is a lifeline for Sub-Saharan growers where RTK networks stall at 40% coverage, but affordability and skills gaps temper speed.

- Deere and Company

- Trimble Inc.

- AGCO Corporation

- CNH Industrial N.V.

- Raven Industries

- Topcon Positioning Systems

- Lindsay Corporation

- TeeJet Technologies

- DICKEY-john

- BASF Digital Farming (xarvio)

- Yara International ASA

- Climate Corp (Bayer)

- Hexagon Agriculture

- CropX Technologies

- DJI Agriculture

- Farmers Edge

- Granular

- Ag Leader Technology

- Kubota Smart Agri

- Sentera

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in GNSS-enabled auto-steering adoption on large farms

- 4.2.2 Rapid cost declines in multispectral/thermal drone sensors

- 4.2.3 Government carbon-credit schemes rewarding variable-rate input cuts

- 4.2.4 Integration of satellite IoT constellations for sub-inch field telemetry

- 4.2.5 Insurance discounts for farms deploying AI-based risk scoring

- 4.2.6 Venture funding shift from farm-management SaaS to edge-AI robotics

- 4.3 Market Restraints

- 4.3.1 Data-interoperability gaps among mixed-brand machinery

- 4.3.2 Rural cybersecurity threats targeting farm OT networks

- 4.3.3 Plateauing RTK-network coverage in Sub-Saharan Africa

- 4.3.4 Farmer resistance to algorithmic decision loss of autonomy

- 4.4 Industry Ecosystem Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Guidance Systems

- 5.1.1.1 GNSS / GPS

- 5.1.1.2 GIS

- 5.1.2 Variable-Rate Technology

- 5.1.2.1 Variable-Rate Fertilizer

- 5.1.2.2 Variable-Rate Seeding

- 5.1.2.3 Variable-Rate Pesticide

- 5.1.3 Remote Sensing

- 5.1.4 Drones and UAVs

- 5.1.5 Robotics and Autonomous Equipment

- 5.1.6 Edge and Cloud Analytics Platforms

- 5.1.7 Other Technologies

- 5.1.1 Guidance Systems

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.1.1 Sensors and Actuators

- 5.2.1.2 Controllers and Displays

- 5.2.1.3 On-board Computing and Connectivity

- 5.2.2 Software

- 5.2.2.1 Farm-Management SaaS

- 5.2.2.2 Data Analytics and AI

- 5.2.3 Services

- 5.2.3.1 Integration and Consulting

- 5.2.3.2 Managed Services

- 5.2.1 Hardware

- 5.3 By Application

- 5.3.1 Yield Monitoring

- 5.3.2 Variable-Rate Application

- 5.3.3 Field Mapping

- 5.3.4 Soil and Crop Health Monitoring

- 5.3.5 Irrigation Management

- 5.3.6 Crop Scouting

- 5.3.7 Harvest Automation and Logistics

- 5.3.8 Other Applications

- 5.4 By Farm Size

- 5.4.1 Small Farms (less than 100 ha)

- 5.4.2 Medium Farms (100 - 1,000 ha)

- 5.4.3 Large Farms (greater than 1,000 ha)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Netherlands

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Deere and Company

- 6.4.2 Trimble Inc.

- 6.4.3 AGCO Corporation

- 6.4.4 CNH Industrial N.V.

- 6.4.5 Raven Industries

- 6.4.6 Topcon Positioning Systems

- 6.4.7 Lindsay Corporation

- 6.4.8 TeeJet Technologies

- 6.4.9 DICKEY-john

- 6.4.10 BASF Digital Farming (xarvio)

- 6.4.11 Yara International ASA

- 6.4.12 Climate Corp (Bayer)

- 6.4.13 Hexagon Agriculture

- 6.4.14 CropX Technologies

- 6.4.15 DJI Agriculture

- 6.4.16 Farmers Edge

- 6.4.17 Granular

- 6.4.18 Ag Leader Technology

- 6.4.19 Kubota Smart Agri

- 6.4.20 Sentera

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment

精密农业市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、流程及最终用户划分

精密农业市场分析及预测(至2035年):依类型、产品类型、服务、技术、组件、应用、形式、设备、流程及最终用户划分 全球精密农业解决方案市场规模、份额、趋势和成长分析报告(2026-2034年)

全球精密农业解决方案市场规模、份额、趋势和成长分析报告(2026-2034年) 人工智慧精准行销市场:2026-2032年全球预测(按组件、部署类型、组织规模、应用程式和最终用户划分)

人工智慧精准行销市场:2026-2032年全球预测(按组件、部署类型、组织规模、应用程式和最终用户划分) 精密农业市场规模、份额及成长分析(依产品类型、应用、最终用途及地区划分)-2026-2033年产业预测

精密农业市场规模、份额及成长分析(依产品类型、应用、最终用途及地区划分)-2026-2033年产业预测 精密农业技术市场预测至2032年:按产品、农场规模、技术、应用和区域分類的全球分析

精密农业技术市场预测至2032年:按产品、农场规模、技术、应用和区域分類的全球分析 2025年全球精密农业市场精密农业设备市场(按设备类型、技术、产品、应用和最终用户)—2025-2032 年全球预测

2025年全球精密农业市场精密农业设备市场(按设备类型、技术、产品、应用和最终用户)—2025-2032 年全球预测 精准农业市场,依产品、技术、应用、国家及地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测精密农业市场:2025-2030 年预测

精准农业市场,依产品、技术、应用、国家及地区划分-2025 年至 2032 年全球产业分析、市场规模、市场份额及预测精密农业市场:2025-2030 年预测 全球覆盖材料市场

全球覆盖材料市场