|

市场调查报告书

商品编码

1939092

非洲作物保护化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031 年)Africa Crop Protection Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

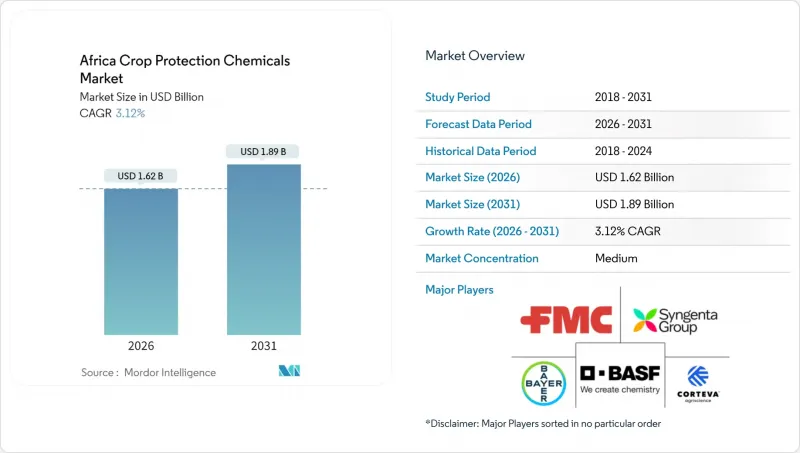

预计非洲作物保护化学品市场将从 2025 年的 15.7 亿美元成长到 2026 年的 16.2 亿美元,到 2031 年将达到 18.9 亿美元,2026 年至 2031 年的复合年增长率为 3.12%。

目前成长得益于气候变迁压力加剧导致病虫害增多、政府投入补贴增加、小规模农户行动金融科技(Fintech)普及以及南部和东部走廊农业的稳步商业化。秋尺蠖虫害加剧、供应链数位化以及生物技术核准数量的增加,正推动产品组合向高端和更具选择性的活性成分方向转型。同时,各国监管差异和运输成本波动推高了服务交付成本,促使供应商探索本地生产和合作伙伴主导的分销模式。市场竞争依然适中,这为本地专家应对打击仿冒品、整合生物农药以及缺乏「最后一公里」咨询服务等挑战提供了空间。

非洲作物保护化学品市场趋势与洞察

气候变迁加剧了害虫压力

气候变迁正在扩大害虫的活动范围并延长其繁殖週期。光是秋粘虫每年就造成高达2,000万吨玉米的损失,足以养活1亿人。农民们透过频繁叶面喷布和使用高价值的内吸性杀虫剂来应对。东非沙漠蝗虫的捲土重来加剧了季节性变化。生物防治基础设施的匮乏推动了对选择性化学农药的需求,以满足综合虫害管理(IPM)的要求。气温升高缩短了害虫的生命週期并缩小了施药窗口期,促使人们投资于预测性害虫监测工具和可最大限度减少非目标喷洒的精准喷嘴。

政府投入增值计画的补贴

尼日利亚的「锚定借款人计画」和肯亚的化肥补贴计画将农药与种子和化肥捆绑销售,保障供应商稳定的销售量。使用代金券或电子钱包付款降低了信用风险,并鼓励扩大分销网络和提前备货。由于资金限制和对捐助方的依赖,采购模式不稳定,但也造成了短期需求高峰。将补贴与农业推广培训相结合的项目提高了还款率,并巩固了产量增长,从而使供应商有理由再次购买化学农药。在政府采购清单上预先註册产品的供应商可以优先进入许可权这些大宗分销管道。

对剧毒活性成分有严格的当地法规

2024年,肯亚农业和食品管理局查获了价值340万肯亚先令(约2.6万美元)的非法农药。南非监管机构目前要求扩大环境评估范围,并将新农药註册所需时间延长至多18个月。西非国家经济共同体(西非经共体)的农药协调计画草案拟逐步淘汰30多种活性成分。重新配製农药将增加研发成本并减少产品系列,尤其是针对特定害虫的小分子农药。如果低毒替代品不易取得或价格昂贵,则在过渡期内有作物减产的风险。

细分市场分析

至2025年,杀虫剂将占非洲作物保护化学品市场份额的39.50%,这主要受西非和东非玉米和高粱作物遭受毛虫严重侵害的影响。儘管杀虫剂市场规模预计将稳定成长,但由于基因改造抗虫作物的广泛应用,其相对份额预计将会下降。除草剂的成长率最高,到2031年将达到3.55%的复合年增长率,主要得益于商业农场采用犁地耕作方式和耐除草剂品种。杀菌剂在出口导向园艺中仍然非常重要,因为精准的施药计划和高品质的活性成分对于符合残留基准值要求至关重要。在根茎类作物产区,线虫防治等特定应用的需求正在成长,这些地区因线虫造成的产量损失接近12%。

生物技术带来的是细微的改变,而非完全的替代。 TELA玉米的核准使每季杀虫剂的使用次数减少了多达三倍,但为了确保更均匀的生长条件,除草剂的使用量却增加。供应商正在透过提供将芽前除草剂与生物种子披衣相结合的组合包装来应对这项挑战。对数位化监测平台的投资使得基于阈值的杀虫剂施用成为可能,并与管理指南保持一致。最终,产品系列正朝着具有双重或多重作用机制的分子方向发展,这些分子能够延缓抗药性的产生,并符合未来的监管标准。

非洲作物保护化学品市场报告按功能(杀菌剂、除草剂、杀虫剂等)、施用方法(化学灌溉、叶面喷布、熏蒸等)、作物类型(经济作物、水果和蔬菜、谷物、豆类和油籽、草坪和观赏植物)以及地区(南非、非洲其他地区)进行划分。市场预测以价值(美元)和数量(公吨)为单位。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

- 调查方法

第二章 报告

第三章执行摘要和主要发现

第四章:主要产业趋势

- 每公顷农药用量

- 活性成分价格分析

- 法规结构

- 南非

- 价值炼和通路分析

- 市场驱动因素

- 气候变迁导致害虫发生率增加,加剧了害虫压力

- 政府对投入集约化计画的补贴

- 耐除草剂作物品种的快速传播

- 南部和东部非洲商业农业丛集的扩张

- 欧盟农药残留限量修订鼓励出口商转向使用更高品质的农药

- 透过行动农业投入金融科技平台改善农业投入品的取得途径

- 市场限制

- 对剧毒农药成分有严格的当地法规

- 加速害虫和杂草抗药性的发展

- 假农药的普遍性

- 红海和苏伊士运河运输的不稳定增加了进口成本

第五章 市场规模和成长预测(价值和数量)

- 功能

- 消毒剂

- 除草剂

- 杀虫剂

- 杀软体动物剂

- 杀线虫剂

- 如何申请

- 化学灌溉

- 叶面喷布

- 熏蒸

- 种子处理

- 土壤处理

- 作物类型

- 经济作物

- 水果和蔬菜

- 谷物和谷类

- 豆类和油籽

- 草坪和观赏植物

- 按国家/地区

- 南非

- 其他非洲地区

第六章 竞争情势

- 重大策略倡议

- 市占率分析

- 公司概况

- 公司简介

- Syngenta Group

- Bayer AG

- Corteva Agriscience

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- UPL Limited

- Wynca Group(Zhejiang Xinan Chemical Industrial Group Co., Ltd.)

- Koppert BV

- Andermatt Group AG

- Albaugh LLC

- Rotam Global AgroSciences Ltd.

- Bioceres Crop Solutions Corp.

- Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

第七章:CEO们需要思考的关键策略问题

The Africa crop protection chemicals market is expected to grow from USD 1.57 billion in 2025 to USD 1.62 billion in 2026 and is forecast to reach USD 1.89 billion by 2031 at 3.12% CAGR over 2026-2031.

Current growth rests on mounting climate pressures that increase pest outbreaks, rising government input subsidies, improving mobile fintech access for smallholders, and steady commercialization of farming in Southern and Eastern corridors. Intensifying fall armyworm damage, supply-chain digitization, and biotechnology approvals are reshaping product mix toward premium, more selective actives. Meanwhile, fragmented national regulations and shipping cost volatility raise cost-to-serve, prompting suppliers to pursue regional manufacturing and partner-led distribution models. Competitive intensity remains moderate, leaving room for local specialists to tackle counterfeit mitigation, biologics integration, and last-mile advisory gaps.

Africa Crop Protection Chemicals Market Trends and Insights

Escalating pest pressure from climate-change-driven outbreaks

Climate variability is expanding pest ranges and reproductive cycles. Fall armyworm alone destroys up to 20 million metric tons of maize annually, equal to feeding 100 million people. Farmers respond with frequent foliar sprays and premium systemic insecticides. Desert locust resurgence in East Africa magnifies seasonal volatility. Limited biological control infrastructure elevates demand for selective chemistries that align with integrated pest management mandates. Temperature increases shorten life cycles, tightening spray windows and driving investments in predictive scouting tools and precision nozzles that minimize off-target drift.

Government subsidies for input intensification programs

Nigeria's Anchor Borrowers' Programme and Kenya's subsidized fertilizer initiatives bundle pesticides with seed and fertilizer, creating assured volumes for suppliers. Voucher and e-wallet payments lower credit risk, spur distributor expansion, and stimulate early-season stocking. Fiscal constraints and donor dependency create start-stop purchasing patterns, yet still inject sizable short-term demand spikes. Programs pairing subsidies with extension advice record higher repayment rates, reinforcing yield gains that justify repeat chemical purchases. Suppliers that pre-register products within government procurement lists secure preferential access to these large-volume channels.

Stringent regional bans on high-toxicity actives

Kenya's Agriculture and Food Authority seized Kenya Shilling (KES) 3.4 million (USD 26,000) of illegal agrochemicals in 2024. South Africa's regulator now requires expanded environmental assessments, lengthening new registration timelines by up to 18 months. The Economic Community of West African States pesticide harmonization draft plans to phase out over 30 active ingredients. Reformulation increases research costs and reduces portfolios, particularly for small molecules targeting niche pests. Transition gaps risk yield losses if low-toxicity alternatives are not readily available or affordable.

Other drivers and restraints analyzed in the detailed report include:

- Rapid adoption of herbicide-tolerant crop varieties

- Expansion of commercial farming clusters

- Proliferation of counterfeit pesticides

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, insecticides secured 39.50% of the Africa crop protection chemicals market share due to acute fall armyworm infestations that imperil maize and sorghum in West and East Africa. The Africa crop protection chemicals market size for insecticides is projected to rise steadily but cede relative share as genetically modified insect-resistant crops diffuse. Herbicides enjoy the fastest 3.55% CAGR through 2031, underpinned by commercial farms adopting reduced-tillage and herbicide-tolerant cultivars. Fungicides remain vital in export-oriented horticulture where maximum residue limit compliance dictates precise scheduling and premium actives. Niche segments such as nematicides gain traction in root and tuber production hotspots where yield losses from nematodes approach 12%.

Biotechnology triggers a nuanced shift rather than outright substitution. TELA maize approval cuts insecticide sprays by up to three rounds each season, yet fosters higher herbicide usage to protect more uniform stands. Suppliers respond with combo packs that integrate pre-emergence herbicides and biological seed coatings. Investment in digital scouting platforms enables threshold-based insecticide applications, aligning with stewardship guidelines. Ultimately, the portfolio mix evolves toward molecules with dual or multiple modes of action that delay resistance and comply with future regulatory standards.

The Africa Crop Protection Chemicals Market Report is Segmented by Function (Fungicide, Herbicide, Insecticide, and More), Application Mode (Chemigation, Foliar, Fumigation, and More), Crop Type (Commercial Crops, Fruits and Vegetables, Grains and Cereals, Pulses and Oilseeds, and Turf and Ornamental), and Geography (South Africa, Rest of Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Syngenta Group

- Bayer AG

- Corteva Agriscience

- BASF SE

- FMC Corporation

- Sumitomo Chemical Co., Ltd.

- Nufarm Limited

- UPL Limited

- Wynca Group (Zhejiang Xinan Chemical Industrial Group Co., Ltd.)

- Koppert B.V.

- Andermatt Group AG

- Albaugh LLC

- Rotam Global AgroSciences Ltd.

- Bioceres Crop Solutions Corp.

- Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY and KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Consumption Of Pesticide Per Hectare

- 4.2 Pricing Analysis For Active Ingredients

- 4.3 Regulatory Framework

- 4.3.1 South Africa

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Escalating pest pressure from climate-change-driven outbreaks

- 4.5.2 Government subsidies for input intensification programs

- 4.5.3 Rapid adoption of herbicide-tolerant crop varieties

- 4.5.4 Expansion of commercial farming clusters in Southern and Eastern Africa

- 4.5.5 EU-MRL revisions shifting exporters to premium actives

- 4.5.6 Mobile agro-input fintech platforms improving input access

- 4.6 Market Restraints

- 4.6.1 Stringent regional bans on high-toxicity actives

- 4.6.2 Accelerating pest and weed resistance

- 4.6.3 Proliferation of counterfeit pesticides

- 4.6.4 Red-Sea/Suez shipping volatility inflating import costs

5 MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME)

- 5.1 Function

- 5.1.1 Fungicide

- 5.1.2 Herbicide

- 5.1.3 Insecticide

- 5.1.4 Molluscicide

- 5.1.5 Nematicide

- 5.2 Application Mode

- 5.2.1 Chemigation

- 5.2.2 Foliar

- 5.2.3 Fumigation

- 5.2.4 Seed Treatment

- 5.2.5 Soil Treatment

- 5.3 Crop Type

- 5.3.1 Commercial Crops

- 5.3.2 Fruits and Vegetables

- 5.3.3 Grains and Cereals

- 5.3.4 Pulses and Oilseeds

- 5.3.5 Turf and Ornamental

- 5.4 Country

- 5.4.1 South Africa

- 5.4.2 Rest of Africa

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Syngenta Group

- 6.4.2 Bayer AG

- 6.4.3 Corteva Agriscience

- 6.4.4 BASF SE

- 6.4.5 FMC Corporation

- 6.4.6 Sumitomo Chemical Co., Ltd.

- 6.4.7 Nufarm Limited

- 6.4.8 UPL Limited

- 6.4.9 Wynca Group (Zhejiang Xinan Chemical Industrial Group Co., Ltd.)

- 6.4.10 Koppert B.V.

- 6.4.11 Andermatt Group AG

- 6.4.12 Albaugh LLC

- 6.4.13 Rotam Global AgroSciences Ltd.

- 6.4.14 Bioceres Crop Solutions Corp.

- 6.4.15 Jiangsu Good Harvest-Weien Agrochemical Co., Ltd.

7 KEY STRATEGIC QUESTIONS FOR CROP PROTECTION CHEMICALS CEOS

作物保护化学品市场:2026-2032年全球市场预测(依产品类型、作物类型、施用方法、配方及销售管道)

作物保护化学品市场:2026-2032年全球市场预测(依产品类型、作物类型、施用方法、配方及销售管道) 作物保护化学品市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场划分(2026-2033 年)

作物保护化学品市场规模、份额和趋势分析报告:按产品、应用、地区和细分市场划分(2026-2033 年) 作物保护化学品市场规模、份额、成长率和全球市场分析:按类型、应用和地区划分,并预测至2026-2034年

作物保护化学品市场规模、份额、成长率和全球市场分析:按类型、应用和地区划分,并预测至2026-2034年 越南农作物保护化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球作物保护化学品市场规模、份额、趋势和成长分析报告(2026-2034年)

越南农作物保护化学品:市场占有率分析、产业趋势与统计、成长预测(2026-2031)全球作物保护化学品市场规模、份额、趋势和成长分析报告(2026-2034年) 2026年全球作物保护化学品市场报告

2026年全球作物保护化学品市场报告 作物保护化学品市场-全球产业规模、份额、趋势、机会、预测:按类型、原料、应用方法、地区和竞争格局划分,2021-2031年农药暴露防护市场依产品、材料、技术、最终用途产业及通路划分,全球预测(2026-2032)化肥和农药市场按产品类型、作物类型、配方、原料、作用方式、施用方法、最终用户和分销管道划分-全球预测(2026-2032 年)呋虫胺技术市场按作物类型、製剂、应用、最终用途产业和分销管道划分,全球预测,2026-2032年

作物保护化学品市场-全球产业规模、份额、趋势、机会、预测:按类型、原料、应用方法、地区和竞争格局划分,2021-2031年农药暴露防护市场依产品、材料、技术、最终用途产业及通路划分,全球预测(2026-2032)化肥和农药市场按产品类型、作物类型、配方、原料、作用方式、施用方法、最终用户和分销管道划分-全球预测(2026-2032 年)呋虫胺技术市场按作物类型、製剂、应用、最终用途产业和分销管道划分,全球预测,2026-2032年