|

市场调查报告书

商品编码

1939096

线控系统:市场占有率分析、产业趋势与统计资料、成长预测(2026-2031 年)X-by-wire System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

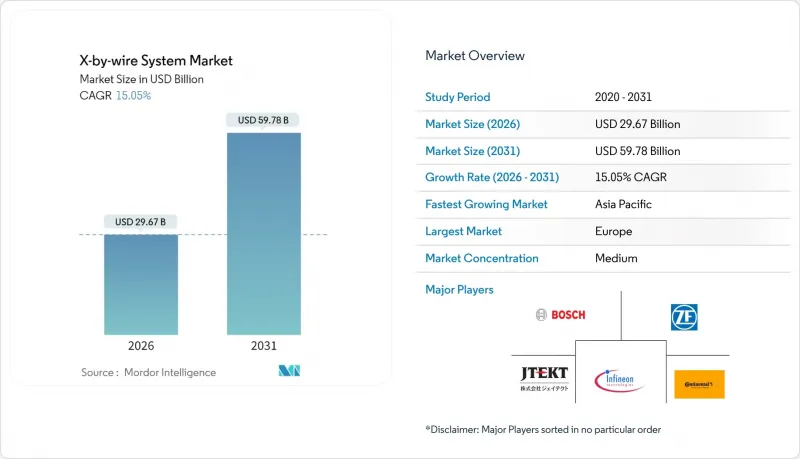

据估计,到 2026 年,线控系统市场价值将达到 296.7 亿美元,高于 2025 年的 257.9 亿美元,预计到 2031 年将达到 597.8 亿美元。

预计2026年至2031年年复合成长率(CAGR)为15.05%。

加速推进电气化、向软体定义车辆转型以及自动驾驶需求的共同作用,正促使机械联锁装置被可程式设计电子控制系统所取代,这些控制系统用于控製油门、煞车、转向、泊车和换檔功能。电池式电动车(BEV)已主导这一普及趋势,因为其电气基础设施和滑板式平台消除了实体布线限制并减轻了重量。诸如修订后的ECE R 79.01标准(允许线控转向而无需机械备份)等监管里程碑正在扫清剩余的核准障碍。儘管各方竞相提供将转向、煞车和驱动系统整合到紧凑、无线可调单元中的模组化架构,但功能安全和网路安全合规性仍然是限制因素。

全球线控系统市场趋势与洞察

推广高级驾驶辅助系统和自动驾驶

不断提升的自动化程度要求实现瞬时、可重复的控制执行,而这只有电子系统才能做到。一款大型纯电动皮卡上安装的线控转向系统,因其性能优于机械转向柱,荣获了一项着名的技术奖。 4-5级自动化需要超过1000 TOPS的运算负载,要求致动器在微秒级做出回应。新型车辆的感测器套件会收集数百个资料流,需要透过线控介面将其转换为精确的动态资讯。功能安全和网路安全法规(ISO 26262和ISO/SAE 21434)确立了明确的合规路径,但也延长了开发週期。

全球安全和二氧化碳排放法规正在推动向电子产品的转变

欧盟2025-2034年平均排放气体法规实际上强制推行电气化,这反过来又促进了能够优化能源管理的电子控制子系统的应用。 ECE R 79.01标准正式批准了全电子转向系统,并取消了机械备用系统的要求,这表明监管机构对冗余电子安全通道充满信心。强制性的高级紧急煞车和盲点监测系统也依赖线控精度,这加速了汽车製造商从液压和电缆式系统向电子控制系统的转型。

功能安全认证的障碍

取得线控系统 (X-by-wire) 的 ISO 26262 功能安全认证十分复杂,耗时耗力。线控系统的汽车安全完整性等级 (ASIL) 要求通常为 ASIL-C 或 ASIL-D 等级,并需要进行广泛的检验流程,与传统机械系统相比,这可能会使开发时间延长 18 至 24 个月。人工智慧和机器学习演算法的整合也为 ISO PAS 8800 认证带来了额外的挑战。线控系统全面获得 ASIL-D 认证的测试和检验成本可能超过 5,000 万美元,这对中小型原始设备製造商 (OEM) 和一级供应商而言,无疑是一笔巨大的财务负担。

细分市场分析

到2025年,线控煞车系统将占据线控系统市场39.42%的份额,这反映了该系统在ADAS煞车距离保障和能量回收煞车优化方面的重要性。随着电动车的普及和能源回收策略对电煞车驱动的依赖性增强,线控制动系统的市场规模预计将显着扩大。受监管合规性和自动驾驶技术进步的推动,线控转向系统将以16.23%的复合年增长率实现最快成长。油门、停车和换檔等功能也逐渐取代电缆和液压系统,但它们的相对价值贡献仍然较低。

合约的签订体现了规模经济效应:一家北美汽车製造商采购了500万套线控煞车系统,将电子后煞车与液压前煞车相结合,以平衡成本。在电子转向系统领域,一款中国豪华轿车获得了政府核准,采用全电子转向系统,为其他製造商树立了先例。供应商的研发蓝图目前正趋向于将电子转向系统和线控煞车系统整合到一个密封单元中的角落模组,从而缩短组装时间并简化认证流程。

到2025年,乘用车将占线控制动系统出货量的73.65%,反映了轻型车辆的整体需求趋势。然而,受车队电气化强制令以及线控制动系统在商业应用中带来的营运优势的推动,中型和重型卡车市场将以17.78%的复合年增长率加速成长。预计到2031年,商用卡车线控制动系统的市场规模将显着成长,这主要得益于基于运作週期的投资回收期计算,例如煞车能量回收和维护成本降低。

车队管理人员对电子驱动技术带来的空中下载 (OTA) 诊断和预测性维护功能讚赏有加。初步试点计画已证实,采用线控转向技术可实现拖车自动定位,将场内操作时间缩短约 40%。轻型商用车 (LCV) 市场正经历稳定成长,其中整合线控系统的电动平台越来越受到「最后一公里」配送应用的青睐。 REE Automotive 的 Leopard EV 就是一个典型的例子,它采用角式模组化架构,可实现自主配送作业。

区域分析

欧洲在2025年仍维持主导,市占率将达35.20%。严格的二氧化碳排放目标和全面的安全法规系统性地优先考虑电子控制系统,而非传统的机械控制系统。德国和法国的汽车製造商将首先在高端电动车中引入有线控制系统,待成本下降后再推广到大众市场车型。区域供应商正利用其数百年来累积的底盘技术经验,同时转型发展控制器软体的专业知识。 ECE R 79.01法规所体现的监管确定性,为现有企业和新参与企业提供了投资信心。

亚太地区将成为成长引擎,到2031年将维持18.06%的复合年增长率。中国电动车的快速普及以及线控转向量产车的早期获批,为该地区的推广应用树立了典范。该地区凭藉其成熟的电子製造能力和供应链,能够以具有竞争力的成本满足线控转向系统对复杂感测器和致动器的需求。日本和韩国提供高精度致动器和整合式转角模组原型,这些产品已在无人计程车上进行实地测试。

北美市场正稳步成长,这主要得益于自动驾驶技术的大规模投资以及商用车电气化的强制要求。特斯拉大规模订购线控煞车订单标誌着这一扩张势头强劲。美国半导体製造能力为先进的网域控制器提供了支持,网路安全框架也在不断发展以符合国际ISO标准。随着皮卡和SUV平台向滑板式电动车架构转型,释放出用于电子执行机构的封装空间,电动车的普及速度正在加快。

其他福利:

- Excel格式的市场预测(ME)表

- 分析师支持(3个月)

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 推广先进的驾驶辅助系统和自动驾驶技术

- 全球安全标准和二氧化碳排放法规赋予电子产品优势。

- 电动车包装和轻量化优势

- 采用数位底盘的成本节约型平台

- 支援OTA调优的软体定义底盘

- 适用于车队的转角模组电动滑板

- 市场限制

- 功能安全认证的障碍

- 传统平台整合成本高昂

- 车载网路安全挑战

- 冗余级感测器供不应求

- 价值/供应链分析

- 监管环境

- 技术展望 - 线控架构

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 按类型

- 线控油门系统

- 线控煞车系统

- 线控转向系统

- 线控泊车系统

- 线控换檔系统

- 按车辆类型

- 搭乘用车

- 轻型商用车

- 中型和重型商用车辆

- 按组件

- 感应器和踏板模组

- 致动器

- 电控系统(ECU)

- 依推进类型

- 内燃机车辆

- 混合动力汽车

- 电池式电动车

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Continental AG

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- JTEKT Corporation

- Nexteer Automotive

- Infineon Technologies AG

- Nissan Motor Corporation

- Tesla Inc.

- Audi AG

- Toyota Motor Corporation

- Hitachi Astemo Ltd.

- Denso Corporation

- Curtiss-Wright Corporation

- CTS Corporation

- Valeo SA

- Orscheln Products LLC

- Torc Robotics

- Jaguar Land Rover

- REE Automotive

第七章 市场机会与未来展望

X-by-wire systems market size in 2026 is estimated at USD 29.67 billion, growing from 2025 value of USD 25.79 billion with 2031 projections showing USD 59.78 billion, growing at 15.05% CAGR over 2026-2031.

Accelerated electrification mandates, the software-defined-vehicle shift, and autonomy requirements are converging to displace mechanical linkages with programmable electronic control across throttle, brake, steer, park, and shift functions. Battery-electric vehicles (BEVs) already dominate adoption because their electrical infrastructure and skateboard platforms eliminate physical routing constraints while lowering weight. Regulatory milestones, such as the revised ECE R 79.01 that now permits steer-by-wire without a mechanical backup, are removing remaining approval bottlenecks. Competitive intensity is climbing as suppliers race to deliver corner-module architectures that bundle steering, braking, and drive systems into compact, over-the-air-tunable units, while functional-safety and cybersecurity compliance remain gating factors.

Global X-by-wire System Market Trends and Insights

Advanced-driver-assistance and Autonomy Push

Growing levels of automated driving demand instantaneous, repeatable control execution that only electronic systems can provide. A steer-by-wire implementation on a leading battery pickup recently earned a high-profile technology award, highlighting the performance leap over mechanical columns. Computing loads for Level 4-5 autonomy exceed 1,000 TOPS, making micro-second-scale actuator response mandatory. Sensor suites in new vehicles now collect hundreds of data streams; translating them into precise dynamics requires by-wire interfaces. Functional-safety and cybersecurity regulations (ISO 26262 and ISO/SAE 21434) establish clear compliance paths but lengthen development cycles.

Global Safety and CO2 Rules Favour Electronics

The EU's 2025-2034 fleet-average emissions limits effectively compel electrification, and by extension, electronic control subsystems that optimize energy management. ECE R 79.01 now formally allows full electronic steering systems, eliminating the mechanical fallback requirement and signaling regulators' trust in redundant electronic safety channels. Mandated advanced emergency braking and blind-spot monitoring systems similarly rely on by-wire precision, accelerating OEM migration away from hydraulics and cables.

Functional-safety Certification Hurdles

The complexity of achieving ISO 26262 functional safety certification for X-by-wire systems presents significant time and cost barriers. Automotive Safety Integrity Level (ASIL) requirements for by-wire systems typically demand ASIL-C or ASIL-D ratings, necessitating extensive validation processes that can extend development timelines by 18-24 months compared to traditional mechanical systems. The integration of AI and machine learning algorithms introduces additional certification challenges under ISO PAS 8800. Testing and validation costs for X-by-wire systems can exceed USD 50 million for comprehensive ASIL-D certification, creating financial barriers particularly challenging for smaller OEMs and tier-1 suppliers.

Other drivers and restraints analyzed in the detailed report include:

- EV Packaging and Weight-saving Benefits

- Digital Chassis Cost-saving Platforms

- High Integration Cost for Legacy Platforms

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Brake-by-wire secured a 39.42% X-by-wire systems market share in 2025, reflecting the system's centrality to ADAS stop-distance guarantees and regenerative-braking optimization. The X-by-wire systems market size for braking is projected to expand significantly as EV penetration rises and energy-recuperation strategies depend on electric brake actuation. Steer-by-wire shows the fastest upswing at 16.23% CAGR, enabled by regulatory acceptance and autonomy programs. Other functions like throttle, park, and shift continue to replace cables and hydraulics steadily, but their relative value content remains lower.

Contract awards reveal scale economies: a single North American OEM sourced brake-by-wire for 5 million units, combining electronic rear brakes with hydraulic fronts to balance cost. In steer-by-wire, a Chinese flagship sedan won government approval for full electronic steering, setting a precedent others will follow. Supplier roadmaps now converge on corner modules merging steer and brake-by-wire into sealed units, slashing assembly time and simplifying homologation.

Passenger cars represented 73.65% of the X-by-wire systems market 2025 shipments, mirroring overall light-vehicle demand. Nevertheless, medium and heavy trucks are accelerating at an 17.78% CAGR, driven by fleet electrification mandates and the operational advantages that X-by-wire systems provide in commercial applications. The X-by-wire systems market size for commercial trucks is expected to grow significantly by 2031, underpinned by duty-cycle-driven payback calculations linked to brake regeneration and reduced maintenance.

Fleet managers value over-the-air diagnostics and predictive maintenance unlocked by electronic actuation. Early pilots show steer-by-wire enabling automated trailer positioning, cutting yard maneuver time by approximately 40%. Light Commercial Vehicles experience moderate growth as last-mile delivery applications increasingly favor electric platforms with integrated by-wire controls, exemplified by REE Automotive's Leopard EV, which utilizes corner-module architecture for autonomous delivery operations.

The X-By-Wire Systems Market Report is Segmented by Type (Throttle-By-Wire, Brake-By-Wire, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Component (Sensors and Pedal Modules, Actuators, and ECUs), Propulsion Type (Internal-Combustion Engine, Hybrid, and Battery-Electric), and Geography (North America, South America, Europe, and More). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe retained leadership at 35.20% share in 2025 owing to stringent CO2 emission targets and comprehensive safety regulations that systematically favor electronic control systems over traditional mechanical alternatives. German and French OEMs deploy by wire on premium EVs first, then cascade to mass segments once cost curves dip. Regional suppliers exploit centuries of chassis know-how while pivoting to domain-controller software expertise. Regulatory certainty, embodied in ECE R 79.01, gives investment confidence to both incumbents and new entrants.

Asia-Pacific is the growth engine with an 18.06% CAGR through 2031. China's rapid BEV uptake and early approval of steer-by-wire production vehicles have created the blueprint for regional adoption. The area benefits from established electronics manufacturing capabilities and supply chains supporting X-by-wire systems' complex sensor and actuator requirements at competitive costs. Japan and South Korea contribute high-precision actuators and integrated corner-module prototypes that are already being field-tested on the robotaxis.

North America posts steady gains, supported by significant investments in autonomous driving technologies and commercial vehicle electrification mandates. A high-volume brake-by-wire award to Tesla underlines scaling momentum. U.S. semiconductor capacity supports advanced domain controllers, while cybersecurity frameworks evolve to align with global ISO standards. Uptake accelerates as pickup-truck and SUV platforms transition to skateboard EV architectures, freeing packaging for electronic actuation.

- Continental AG

- ZF Friedrichshafen AG

- Robert Bosch GmbH

- JTEKT Corporation

- Nexteer Automotive

- Infineon Technologies AG

- Nissan Motor Corporation

- Tesla Inc.

- Audi AG

- Toyota Motor Corporation

- Hitachi Astemo Ltd.

- Denso Corporation

- Curtiss-Wright Corporation

- CTS Corporation

- Valeo SA

- Orscheln Products LLC

- Torc Robotics

- Jaguar Land Rover

- REE Automotive

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Advanced-driver-assistance and Autonomy Push

- 4.2.2 Global Safety and CO2 Rules Favour Electronics

- 4.2.3 EV Packaging and Weight-saving Benefits

- 4.2.4 Digital Chassis Cost-saving Platforms

- 4.2.5 OTA-tunable Software-defined Chassis

- 4.2.6 Corner-module EV Skateboards for Fleets

- 4.3 Market Restraints

- 4.3.1 Functional-safety Certification Hurdles

- 4.3.2 High Integration Cost for Legacy Platforms

- 4.3.3 In-vehicle-network Cyber-security Gaps

- 4.3.4 Supply Crunch of Redundancy-grade Sensors

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook - X-by-wire Control Architectures

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Type

- 5.1.1 Throttle-by-wire System

- 5.1.2 Brake-by-wire System

- 5.1.3 Steer-by-wire System

- 5.1.4 Park-by-wire System

- 5.1.5 Shift-by-wire System

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Component

- 5.3.1 Sensors and Pedal Modules

- 5.3.2 Actuators

- 5.3.3 Electronic Control Units (ECUs)

- 5.4 By Propulsion Type

- 5.4.1 Internal-Combustion Engine Vehicles

- 5.4.2 Hybrid Vehicles

- 5.4.3 Battery-Electric Vehicles

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Russia

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Continental AG

- 6.4.2 ZF Friedrichshafen AG

- 6.4.3 Robert Bosch GmbH

- 6.4.4 JTEKT Corporation

- 6.4.5 Nexteer Automotive

- 6.4.6 Infineon Technologies AG

- 6.4.7 Nissan Motor Corporation

- 6.4.8 Tesla Inc.

- 6.4.9 Audi AG

- 6.4.10 Toyota Motor Corporation

- 6.4.11 Hitachi Astemo Ltd.

- 6.4.12 Denso Corporation

- 6.4.13 Curtiss-Wright Corporation

- 6.4.14 CTS Corporation

- 6.4.15 Valeo SA

- 6.4.16 Orscheln Products LLC

- 6.4.17 Torc Robotics

- 6.4.18 Jaguar Land Rover

- 6.4.19 REE Automotive

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

全球线传系统市场规模、份额、趋势和成长分析报告(2026-2034年)

全球线传系统市场规模、份额、趋势和成长分析报告(2026-2034年) 日本线控系统市场报告(按车辆类型(乘用车、商用车)、应用类型(油门线控系统、煞车线控系统、转向线控系统、驻车线控系统、换檔线控系统)和地区划分,2026-2034 年)

日本线控系统市场报告(按车辆类型(乘用车、商用车)、应用类型(油门线控系统、煞车线控系统、转向线控系统、驻车线控系统、换檔线控系统)和地区划分,2026-2034 年) X-by-Wire 系统市场(按组件、推进类型、系统类型、技术、销售管道和车辆类型)—2025 年至 2032 年全球预测

X-by-Wire 系统市场(按组件、推进类型、系统类型、技术、销售管道和车辆类型)—2025 年至 2032 年全球预测 X-by-Wire 市场,按组件类型、按系统类型、按自主级别、按技术、按应用、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测2025 年至 2033 年 X-by-Wire 系统市场报告(按类型(线控油门系统、线控制动系统、线控转向系统、线控驻车系统、线控换檔系统)、车辆类型(乘用车、商用车)和地区)

X-by-Wire 市场,按组件类型、按系统类型、按自主级别、按技术、按应用、按国家和地区 - 2025 年至 2032 年全球行业分析、市场规模、市场份额和预测2025 年至 2033 年 X-by-Wire 系统市场报告(按类型(线控油门系统、线控制动系统、线控转向系统、线控驻车系统、线控换檔系统)、车辆类型(乘用车、商用车)和地区) 汽车线控系统市场规模、份额和趋势分析报告:按车辆、类型、地区和细分市场预测,2024-2030 年

汽车线控系统市场规模、份额和趋势分析报告:按车辆、类型、地区和细分市场预测,2024-2030 年