|

市场调查报告书

商品编码

1939098

蓝牙音箱:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Bluetooth Speaker - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

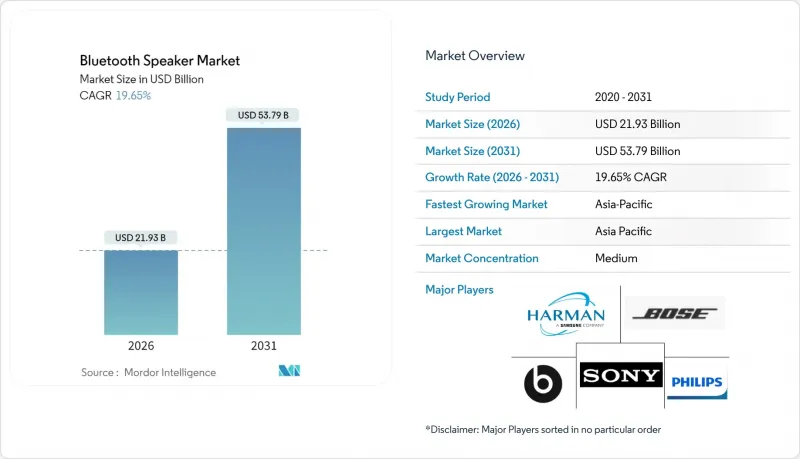

2025年蓝牙音箱市场价值为183.2亿美元,预计到2031年将达到537.9亿美元,而2026年为219.3亿美元。

预测期(2026-2031 年)的复合年增长率预计为 19.65%。

强劲的需求主要得益于智慧家庭的普及、音乐串流媒体的大众化、电池成本的下降以及蓝牙低功耗音讯的商业化,这些因素都在扩大目标用户群的同时缩短更换週期。亚太地区凭藉其强大的製造地和快速壮大的中产阶级,目前在销量方面领先。同时,北美和欧洲由于智慧家庭的早期普及,实现了较高的平均售价。支援语音助理的型号是成长最快的品类,而仅支援蓝牙的音箱仍然是最大的细分市场,它们无需Wi-Fi即可提供简单、低延迟的体验。竞争格局正朝着整合的方向发展,成熟品牌收购高阶音响製造商以确保其专利技术和品牌价值,从而提高了普通产品厂商的进入门槛。

全球蓝牙音箱市场趋势与洞察

智慧家庭生态系统的快速普及

透过 Matter 标准实现的无缝互通性,正推动蓝牙音箱从独立的娱乐设备转型为多功能智慧家庭中心。亚马逊 2025 年推出的 Echo Show 系列正是这一转变的体现,它将 Fire TV 服务、带自动取景功能的视讯通讯以及对 Matter、Zigbee 和 Thread 的全面支援整合于一体。品牌间相容性的提升降低了转换成本,刺激了那些希望透过语音控制音箱实现照明、暖通空调和安防控制的家庭对高级产品更换产品的需求。像 LegatoXP 这样的中国 ODM 平台缩短了产品开发週期,使技术预算有限的中阶品牌也能进入智慧家庭市场。这些因素共同加速了智慧家庭的普及,加剧了品牌竞争,并推动了对蓝牙音箱的整体需求。

音乐串流服务的扩展

预计到2024年,音乐串流服务的付费用户数量将超过7.5亿,这将推动对能够播放高解析度和空间音讯的硬体的需求。随着LC3、LDAC和aptX Lossless等转码器技术的日益成熟,使用者越来越意识到传统设备和新一代扬声器在音质上的差异,从而刺激了更换需求。订阅平台也鼓励用户选择原生支援多人聆听的多装置套餐,这使得多房间扬声器比单房间扬声器系统更具优势。串流媒体的循环收入模式鼓励促销商品搭售,折扣扬声器可以作为吸引新用户的手段,进一步刺激预测期内硬体的销售成长。

假冒伪劣商品和盗版商品猖獗

未经授权的工厂大量复製热门设计,以低劣的假冒商品充斥电商管道,给正品品牌带来价格压力,并损害消费者信任。仿冒品通常缺乏安全电路,增加电池起火的风险,并增加品牌透过认证技术、区块链标籤和法律诉讼等手段进行保护的成本。虽然高端製造商正在实施安全全息图和供应链追踪,但小型供应商由于缺乏资金进行大规模监控,面临收入损失和声誉受损的风险。

细分市场分析

到2025年,桌上型和壁挂式蓝牙音箱将占据68.75%的市场份额,这表明消费者偏好能够与电视和多房间平台无缝整合的主动音箱系统。此细分市场稳定的收入基础为製造商提供了可预测的升级週期,这与智慧家庭维修计划密切相关。同时,受都市区户外活动和远距办公行动性需求的推动,可携式音箱的复合年增长率将达到21.95%。

固定式蓝牙音箱注重高音质、低音表现和语音助理控制——这些特性推高了平均售价,并促进了与串流媒体服务的捆绑销售。同时,可携式音箱则优化了坚固耐用的结构、轻巧的设计和超长的电池续航时间,吸引了新兴市场的新买家。因此,这两个细分市场正在同步发展,互不蚕食,为整个蓝牙音箱市场提供了多元化的收入来源。

到2025年,住宅安装将占蓝牙音箱市场的60.55%,维持21.85%的最快复合年增长率,这表明疫情封锁期间形成的以家庭为中心的娱乐习惯已经根深蒂固。智慧家庭的持续升级已将更换週期缩短至四年以下,远低于传统高传真音响设备的平均更换週期。

商业场所(餐厅、饭店、小规模办公室)对高阶安装系统的需求依然重要,但面临着冗长的采购流程和日益紧张的资金预算。随着语音助理技术的日趋成熟,住宅音响正日益成为照明和暖通空调控制中心,将功能性与娱乐性融为一体,巩固了主导地位。

区域分析

预计到2025年,亚太地区将占据蓝牙音箱市场31.45%的份额,并在2031年之前以21.15%的复合年增长率增长,这主要得益于製造业规模、年轻消费群体以及智慧型手机的快速普及。中国OEM厂商正利用其在印刷基板和电池供应链方面的地理接近性,缩短前置作业时间,以满足国内对专业影音设备的需求。预计到2030年,国内市场对专业影音设备的需求将超过5.8兆元。政府对物联网生态系统的扶持政策进一步加速了智慧音箱的普及,巩固了主导地位。

北美地区的销售量虽然落后于其他国家,但平均售价却位居全球最高之列。智慧家庭的早期普及以及消费者对语音助理整合功能的付费意愿,支撑了该地区高于平均的毛利率。从国家公园露营到都市区屋顶聚会,户外休閒趋势推动了对具备多设备连接功能的坚固耐用产品的需求。强大的品牌忠诚度使得像 Sonos 这样的行业领导者能够在价格竞争中保持高端销售地位。

欧洲市场维持了稳健成长,成长速度在15%左右。严格的品质和网路安全标准赋予了成熟品牌优势,而将于2024年8月生效的修订版无线电设备指令(RED)将要求安全启动和网路安全保护,从而有效地淘汰了那些没有合规预算的低成本进口产品。由于消费者会根据合规性来评估产品价格,国内外製造商正将早期认证和CE标誌作为差异化因素。这将继续推动全球蓝牙音箱市场收入的成长。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 智慧家庭生态系统的快速普及

- 不断扩大的音乐串流服务用户

- 锂离子电池平均售价(ASP)下降

- 户外休閒与房车生活热潮

- 隆重推出蓝牙低功耗音讯和 Auracast

- 对身临其境型课堂音讯的需求日益增长

- 市场限制

- 假冒伪劣商品和盗版商品猖獗

- 价格竞争导致利润率下降

- 与电池起火相关的安全召回

- 欧盟收紧30瓦以上扬声器的电磁干扰法规。

- 价值链分析

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 移动性别

- 可携式的

- 固定式/壁挂式

- 透过使用

- 住宅

- 商业的

- 透过连接技术

- 限蓝牙

- 蓝牙+Wi-Fi(支援多房间连线)

- 附语音助理的智慧音箱

- 透过分销管道

- 仅限线上零售商

- 全通路电子产品量贩店

- 按价格范围

- 经济型(50 美元以下)

- 中檔(50-199美元)

- 高级版(超过 200 美元)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 韩国

- 印度

- 亚太其他地区

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Sony Group Corporation

- Samsung Electronics Co., Ltd.(Harman International Industries, Inc.)

- Panasonic Holdings Corporation

- Bose Corporation

- Beats Electronics LLC(Apple Inc.)

- Koninklijke Philips NV

- LG Electronics Inc.

- Logitech International SA

- Sonos, Inc.

- Bang & Olufsen A/S

- Yamaha Corporation

- Altec Lansing LLC

- JVCKENWOOD Corporation

- Anker Innovations Technology Co., Ltd.

- Ultimate Ears(Logitech)

- Tribit Audio(Thesy Technology Co., Ltd.)

- Onkyo Home Entertainment Corporation

- Zebronics India Pvt. Ltd.

- AOMAIS Audio(Shenzhen Jin Wen Hua)

- SoundBot Inc.

第七章 市场机会与未来展望

The Bluetooth Speaker Market was valued at USD 18.32 billion in 2025 and estimated to grow from USD 21.93 billion in 2026 to reach USD 53.79 billion by 2031, at a CAGR of 19.65% during the forecast period (2026-2031).

Robust demand stems from smart-home adoption, mass music-streaming uptake, battery cost declines, and the commercialization of Bluetooth LE Audio, each widening the addressable user base while shortening replacement cycles. Asia-Pacific leads current unit volumes thanks to competitive manufacturing clusters and a rapidly expanding middle class, while North America and Europe deliver premium average selling prices (ASPs) on the back of early smart-home penetration. Voice-assistant-enabled models are the fastest-growing category, yet Bluetooth-only speakers still represent the largest sub-segment because they deliver a simple, low-latency experience that does not rely on Wi-Fi. Competitive dynamics are shifting toward consolidation as established brands purchase luxury audio houses to secure patented technologies and brand cachet, thereby raising entry barriers for commodity players.

Global Bluetooth Speaker Market Trends and Insights

Rapid Adoption of Smart-Home Ecosystems

Seamless interoperability delivered by the Matter standard elevates Bluetooth speakers from stand-alone entertainment devices to multifunction smart-home hubs. Amazon's 2025 Echo Show range illustrates the shift by embedding Fire TV services, auto-framing video communications, and full Matter, Zigbee, and Thread support in a single unit. Inter-brand compatibility lowers switching costs and drives premium replacement demand as households unify lighting, HVAC, and security control via voice-enabled speakers. Chinese ODM platforms such as LegatoXP shorten product development cycles, letting second-tier brands enter the smart-home space with smaller engineering budgets. Collectively, these forces accelerate household penetration, intensify brand competition, and enlarge the total volume opportunity for the Bluetooth speaker market.

Expansion of Music-Streaming Subscriptions

Music-streaming services surpassed 750 million paid subscribers in 2024, boosting demand for hardware capable of high-resolution and spatial-audio playback. As codecs such as LC3, LDAC, and aptX Lossless mature, users recognize audible quality deltas between legacy devices and next-generation speakers, prompting replacement purchases. Subscription platforms also encourage multi-device plans that natively support group listening, thereby favoring multi-room speakers over single-speaker setups. Streaming's recurring revenue model fosters promotional bundling, where discounted speakers act as customer-acquisition vehicles, further stimulating hardware volumes throughout the forecast window.

Rampant Counterfeiting and Piracy

Unauthorized factories replicate popular designs, flooding e-commerce channels with low-quality imitations that undercut legitimate brands on price and erode consumer trust. Counterfeits often omit essential safety circuits, raising the risk of battery fires and accelerating brand-protection expenditures for authentication technologies, blockchain labeling, and legal enforcement. While premium players deploy security holograms and supply-chain tracing, smaller vendors lack capital for large-scale monitoring, exposing them to revenue leaks and reputational damage.

Other drivers and restraints analyzed in the detailed report include:

- Bluetooth LE Audio and Auracast Roll-out

- Outdoor Recreation and Van-Life Boom

- Safety Recalls Tied to Battery Fires

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fixed and wall-mounted units accounted for 68.75% of the Bluetooth speaker market share in 2025, illustrating consumers' preference for power-fed systems that integrate seamlessly with televisions and multi-room platforms. This segment's steady revenue base gives manufacturers predictable upgrade cycles tied to smart-home renovation projects. Portable speakers, however, post a 21.95% CAGR, gaining from urban outdoor activities and remote-work mobility.

Fixed solutions emphasize audio fidelity, bass response, and voice-assistant control, traits that favor higher ASPs and bundling with streaming services. Portable designs optimize for rugged builds, lighter weight, and prolonged battery life, attracting first-time buyers in emerging markets. The two sub-segments, therefore, expand in parallel rather than cannibalize, yielding a diversified revenue structure for the overall Bluetooth speaker market.

Residential settings delivered 60.55% of the Bluetooth speaker market size in 2025 and also hold the fastest 21.85% CAGR, underscoring the permanence of home-centric entertainment habits formed during pandemic lockdowns. Continuous smart-home upgrades keep the replacement cycle under four years, far shorter than the historical averages for legacy hi-fi components.

Commercial demand, restaurants, hotels, and small offices, remains important for premium installed systems but faces elongated procurement processes and tighter capital budgets. As voice assistants mature, residential speakers increasingly serve as hubs for lighting and HVAC control, blending functional utility with leisure use and cementing their primacy in long-term demand projections for the Bluetooth speaker market.

The Global Bluetooth Speaker Market Report is Segmented by Portability (Portable, Fixed/Wall-Mounted), Application (Residential, Commercial), Connectivity Technology (Bluetooth-Only, and More), Distribution Channel (Online-Only Retailers, and More), Price Range (Economy Less Than USD 50, and More), and Geography (North America, South America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 31.45% of the Bluetooth speaker market share in 2025, generating a 21.15% CAGR to 2031 on the back of manufacturing scale, youth-oriented consumption, and rapid smartphone proliferation. Chinese OEMs leverage proximity to printed-circuit and battery supply chains to compress lead times and capitalize on domestic demand, which is forecast to surpass CNY 5.8 trillion for professional AV equipment by 2030. Government incentives for IoT ecosystems further accelerate the adoption of smart speakers, solidifying regional leadership in both volume and innovation.

North America trails in unit volumes yet achieves the highest ASPs. Early smart-home adoption and consumer willingness to pay for voice-assistant integration keep the region's gross margins above global averages. Outdoor recreation trends-from national park camping to city rooftop gatherings- stimulate demand for ruggedized models with multi-device pairing. Brand loyalty is strong, allowing category leaders such as Sonos to maintain premium shelf space even amid price-based competition.

Europe posts steady mid-teen growth, backed by stringent quality and cybersecurity standards that favor established brands. The updated Radio Equipment Directive effective August 2024 mandates secure boot and network safeguards, effectively filtering out low-end imports lacking compliance budgets. Consumers reward compliance with premium pricing, prompting local and international manufacturers to certify early and use CE markings as marketing differentiators, sustaining a value-heavy contribution to global Bluetooth speaker market revenues.

- Sony Group Corporation

- Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- Panasonic Holdings Corporation

- Bose Corporation

- Beats Electronics LLC (Apple Inc.)

- Koninklijke Philips N.V.

- LG Electronics Inc.

- Logitech International S.A.

- Sonos, Inc.

- Bang & Olufsen A/S

- Yamaha Corporation

- Altec Lansing LLC

- JVCKENWOOD Corporation

- Anker Innovations Technology Co., Ltd.

- Ultimate Ears (Logitech)

- Tribit Audio (Thesy Technology Co., Ltd.)

- Onkyo Home Entertainment Corporation

- Zebronics India Pvt. Ltd.

- AOMAIS Audio (Shenzhen Jin Wen Hua)

- SoundBot Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid adoption of smart-home ecosystems

- 4.2.2 Expansion of music-streaming subscriptions

- 4.2.3 Falling ASPs of lithium-ion batteries

- 4.2.4 Outdoor recreation and van-life boom

- 4.2.5 Bluetooth LE Audio and Auracast roll-out

- 4.2.6 Growing demand for immersive classroom audio

- 4.3 Market Restraints

- 4.3.1 Rampant counterfeiting and piracy

- 4.3.2 Margin erosion from price wars

- 4.3.3 Safety recalls tied to battery fires

- 4.3.4 Stricter EU EMI limits for more than 30 W speakers

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Portability

- 5.1.1 Portable

- 5.1.2 Fixed / Wall-Mounted

- 5.2 By Application

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Connectivity Technology

- 5.3.1 Bluetooth-only

- 5.3.2 Bluetooth + Wi-Fi (Multi-room)

- 5.3.3 Smart Speakers w/ Voice Assistant

- 5.4 By Distribution Channel

- 5.4.1 Online-Only Retailers

- 5.4.2 Omnichannel Consumer-Electronics Stores

- 5.5 By Price Range

- 5.5.1 Economy (Less than USD 50)

- 5.5.2 Mid-range (USD 50-199)

- 5.5.3 Premium (More than USD 200)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Sony Group Corporation

- 6.4.2 Samsung Electronics Co., Ltd. (Harman International Industries, Inc.)

- 6.4.3 Panasonic Holdings Corporation

- 6.4.4 Bose Corporation

- 6.4.5 Beats Electronics LLC (Apple Inc.)

- 6.4.6 Koninklijke Philips N.V.

- 6.4.7 LG Electronics Inc.

- 6.4.8 Logitech International S.A.

- 6.4.9 Sonos, Inc.

- 6.4.10 Bang & Olufsen A/S

- 6.4.11 Yamaha Corporation

- 6.4.12 Altec Lansing LLC

- 6.4.13 JVCKENWOOD Corporation

- 6.4.14 Anker Innovations Technology Co., Ltd.

- 6.4.15 Ultimate Ears (Logitech)

- 6.4.16 Tribit Audio (Thesy Technology Co., Ltd.)

- 6.4.17 Onkyo Home Entertainment Corporation

- 6.4.18 Zebronics India Pvt. Ltd.

- 6.4.19 AOMAIS Audio (Shenzhen Jin Wen Hua)

- 6.4.20 SoundBot Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment

可携式蓝牙音箱市场:依防水等级、价格范围、设计类型和销售管道划分-2026-2032年全球市场预测蓝牙音箱市场:依产品类型、应用和销售管道-2026-2032年全球市场预测

可携式蓝牙音箱市场:依防水等级、价格范围、设计类型和销售管道划分-2026-2032年全球市场预测蓝牙音箱市场:依产品类型、应用和销售管道-2026-2032年全球市场预测 蓝牙音箱市场报告:按便携性、类型、价格、销售管道和地区划分(2026-2034 年)户外迷你音箱市场:按连接类型、电池容量、价格范围、防水等级、扬声器输出功率、分销管道和应用领域划分-全球预测,2026-2032年

蓝牙音箱市场报告:按便携性、类型、价格、销售管道和地区划分(2026-2034 年)户外迷你音箱市场:按连接类型、电池容量、价格范围、防水等级、扬声器输出功率、分销管道和应用领域划分-全球预测,2026-2032年 蓝牙音箱市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、销售管道、地区和竞争格局划分,2021-2031年)防水蓝牙音箱市场 - 全球产业规模、份额、趋势、机会、预测:按充电技术、应用、地区和竞争格局划分,2021-2031年可携式户外扬声器市场:按连接技术、价格范围、产品类型、电源、扬声器配置、分销管道和最终用户划分-2026-2032年全球预测蓝牙音箱晶片市场:按蓝牙版本、模组类型、应用、最终用户和分销管道划分,全球预测(2026-2032年)日本蓝牙音箱市场规模、份额、趋势及预测(依便携性、类型、价格、通路及地区划分,2026-2034年)

蓝牙音箱市场 - 全球产业规模、份额、趋势、机会及预测(按类型、技术、销售管道、地区和竞争格局划分,2021-2031年)防水蓝牙音箱市场 - 全球产业规模、份额、趋势、机会、预测:按充电技术、应用、地区和竞争格局划分,2021-2031年可携式户外扬声器市场:按连接技术、价格范围、产品类型、电源、扬声器配置、分销管道和最终用户划分-2026-2032年全球预测蓝牙音箱晶片市场:按蓝牙版本、模组类型、应用、最终用户和分销管道划分,全球预测(2026-2032年)日本蓝牙音箱市场规模、份额、趋势及预测(依便携性、类型、价格、通路及地区划分,2026-2034年)