|

市场调查报告书

商品编码

1939108

农业灌溉设备:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Agricultural Irrigation Machinery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

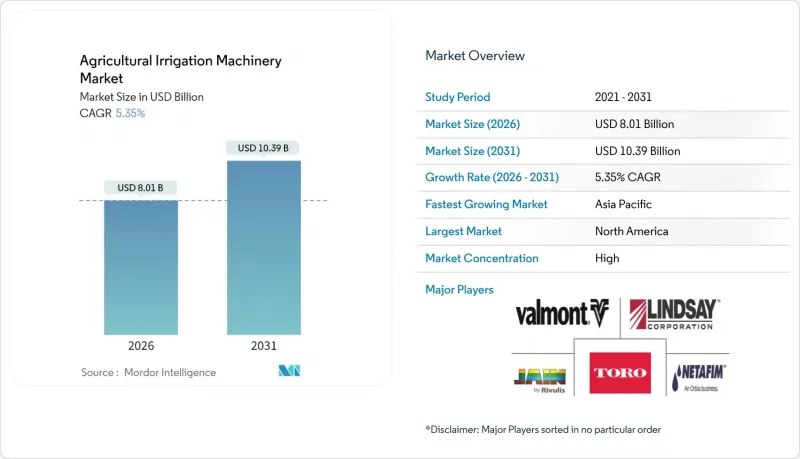

2025年农业灌溉机械市场价值为76亿美元,预计2031年将达到103.9亿美元,高于2026年的80.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 5.35%。

水资源日益短缺、精密农业的普及以及慷慨的补贴政策正在推动农业灌溉设备市场的发展,而技术赋能的服务模式则带来了新的商机。感测器和自动化领域的创新产品以及从一次性设备销售向长期资讯服务的转变,加剧了市场竞争。儘管与环境、社会和治理(ESG)相关的资金投入正在加速微灌技术的普及,但发展中地区土地所有权的分散化限制了整体成长。能够提供本地化售后服务并解决塑胶废弃物问题的製造商,将更有利于抓住农业灌溉设备市场不断增长的需求。

全球农业灌溉机械市场趋势与洞察

政府对微灌系统安装的补贴

联邦政府扩大保护资金投入,有助于降低中型生产商的前期成本。美国农业部(USDA)的环境品质奖励计画(EQIP)补贴高达75%的系统成本,并在2024财政年度拨款19亿美元用于提高效率。多年通膨控制保障鼓励製造商扩大产能,而基于绩效的指标则使供应商的产品与政策目标一致。资金筹措的确定性使设备製造商更有信心投资于产能和供应链基础设施。该计划强调可衡量的节水成果,这与製造商的精密农业技术相契合,为技术整合解决方案创造了竞争优势。

水资源日益短缺推动了精准灌溉的需求

重点农业区的水资源压力指标正加速从漫灌到精准灌溉系统的转型。联合国最新发布的《水资源发展报告》预测,全球有20亿人居住在水资源紧张的国家,到2050年,农业用水需求将增加35%。这种经济上的迫切需求不仅体现在水成本上,也体现在遵守监管规定的必要性上,因为各地对用水报告的要求日益严格。精准灌溉系统能够提供详细的用水量分析,使其不再只是提高效率的手段,而是成为不可或缺的合规工具。

枢轴系统的高初始资本成本

儘管经济效益和资金筹措方案有所改善,但中心支轴式喷灌系统的高昂资本投入仍是其推广应用的一大障碍。根据地形和技术规格的不同,整套安装中心支轴式喷灌系统的成本在每英亩 1200 美元到 2000 美元之间,这对于中型农业企业来说需要大量的资金投入。在水费适中的地区,投资回收期可能长达七到十年,这给面临价格波动的农产品生产商带来了现金流管理的挑战。设备融资通常需要 20% 到 30% 的首付,这给同时改造多个田地的经营者造成了流动性限制。製造商正在透过模组化安装方法和租赁购买计划来解决这个问题,但初始资金需求仍然是限制其普及应用的关键因素。

细分市场分析

到2025年,滴灌系统将维持46.08%的农业灌溉机械市场份额,主要得益于其卓越的用水效率和精准施肥能力。在气候压力日益加剧的情况下,这一主导地位支撑着该细分市场强劲的发展前景。喷灌系统是成长最快的细分市场,预计到2031年将以8.05%的复合年增长率成长,这主要得益于大面积面积种植机械化程度的提高。中心支轴式喷灌系统透过整合感测器缩短决策週期,进一步释放了成长潜力。 Valley Irrigation公司的AgSense 365体现了向整合式控制面板的转变,从而提升了产品的全生命週期服务价值。

此细分市场的加速成长反映了主要农业地区水费上涨和劳动力短缺带来的经济效益改善。其他灌溉方式,包括地表灌溉和漫灌,由于水资源日益短缺以及法规结构向以效率为导向的技术转变,其采用率正在下降。细分市场趋势表明,农业生产结构正在向支持数据驱动型农业管理方法的精准供水系统转变。

区域分析

2025年,北美将占总收入的32.12%,这得益于慷慨的成本分摊计划和成熟的分销网络。 2031年之前的预算稳定性将维持设备的更新换代週期,即使市场饱和限制了销售成长。加拿大注重气候适应型农业以及墨西哥以出口为导向的园艺产业,都为区域农业灌溉设备市场注入了新的动力。

亚太地区是成长最快的地区,复合年增长率达8.06%,这主要得益于中国强制性的水资源压力管理措施以及印度的「总理农业灌溉计画」(Pradhan Mantri Krishi Sinchai Yojana),该计画正推动微灌技术的快速普及。日本老化的农业人口正在加速自动化投资,而东南亚的温室丛集则对配备丰富感测器的滴灌系统有着迫切的需求。预计到2031年,这些因素将共同推动亚太地区农业灌溉机械市场规模的显着成长。

在欧洲,精准灌溉预计将在通用农业政策(CAP)的环境支柱下稳步发展,该政策将其定位为永续活动,并符合绿色金融的条件。地中海地区的干旱正在加速地下灌溉的普及,而荷兰和德国则优先发展封闭式温室灌溉。在中东和非洲,政府支持的大型农场和气候智慧型农业走廊正在推动市场需求。在南美洲的大豆产区,为缓解降雨量变化而对中心支轴式喷灌系统的投资,正在增强农业灌溉设备市场地理多元化的收入基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 政府对微灌系统安装的补贴

- 水资源短缺日益严重,推动了精准灌溉的需求。

- 劳动力短缺推动中型农场机械化

- 物联网感测器整合支援「按需收费」的服务模式。

- 透过与环境、社会及公司治理(ESG)挂钩的融资方式激励节水投资

- 针对节水技术的排碳权计画层出不穷

- 市场限制

- 枢轴系统的初始资本成本高

- 发展中国家土地所有权分散化限制了投资收益(ROI)。

- 人们越来越关注滴灌管产生的塑胶废弃物

- 互联灌溉网路中的网路漏洞

- 监管环境

- 技术展望

- 波特五力分析

- 供应商的议价能力

- 买方的议价能力

- 替代品的威胁

- 新进入者的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 透过灌溉法

- 喷水灌溉

- 泵浦组

- 管子

- 耦合器

- 喷头或喷灌头

- 配件及配件

- 感应器

- 控制器

- 注射器

- 流量计

- 滴灌

- 阀门

- 回流防止装置

- 压力调节器

- 筛选

- 发送器

- 管子

- 其他滴灌部件

- 中心支线灌溉

- 其他灌溉方法

- 喷水灌溉

- 透过使用

- 谷物和谷类

- 豆类和油籽

- 水果和蔬菜

- 其他用途

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 北美其他地区

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 荷兰

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 印度

- 日本

- 柬埔寨

- 亚太其他地区

- 南美洲

- 巴西

- 阿根廷

- 秘鲁

- 其他南美洲

- 中东

- 沙乌地阿拉伯

- 土耳其

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Netafim Ltd.(Orbia Advance Corporation)

- Valmont Industries, Inc.(Valley Irrigation)

- Lindsay Corporation

- Jain Irrigation Systems Limited(Rivulis Irrigation Limited)

- The Toro Company

- Nelson Irrigation Corporation

- Rain Bird Corporation

- Mahindra & Mahindra Limited

- Hunter Industries Incorporated

- Reinke Manufacturing Company, Inc.

- Ningbo Rainfine Irrigation Co., Ltd.

- TL Irrigation Company

- Sistemas Azud, SA

- Antelco Pty Ltd.

第七章 市场机会与未来展望

The agricultural irrigation machinery market was valued at USD 7.60 billion in 2025 and estimated to grow from USD 8.01 billion in 2026 to reach USD 10.39 billion by 2031, at a CAGR of 5.35% during the forecast period (2026-2031).

Rising water scarcity, the adoption of precision agriculture, and robust subsidy pipelines are combining to propel the agricultural irrigation machinery market, while technology-enabled service models offer fresh revenue opportunities. Competitive intensity is shaped by product innovations in sensors and automation, as well as the shift from one-off equipment sales to long-term data services. Capital availability through ESG-linked funding accelerates the deployment of micro-irrigation, yet fragmented landholdings in developing regions temper overall growth. Manufacturers that localize after-sales support and address plastic-waste concerns position themselves to capture incremental demand in the agricultural irrigation machinery market.

Global Agricultural Irrigation Machinery Market Trends and Insights

Government subsidies for micro-irrigation adoption

Expanded federal conservation funding makes upfront costs more accessible for medium-scale growers. The United States Department of Agriculture (USDA) Environmental Quality Incentives Program covered up to 75% of system outlays in fiscal 2024, allocating USD 1.9 billion to efficiency upgrades. Multi-year guarantees from the Inflation Reduction Act encourage manufacturers to boost production capacity, while outcome-based metrics align vendor offerings with policy targets. This funding certainty enables equipment manufacturers to invest in production capacity and supply chain infrastructure with confidence. The program's emphasis on measurable water savings outcomes aligns with manufacturers' precision agriculture capabilities, creating competitive advantages for technology-integrated solutions.

Rising water scarcity pushing demand for precision irrigation

Water stress indicators across major agricultural regions are accelerating the transition from flood irrigation to precision delivery systems. The United Nations' latest water development report identifies 2 billion people living in water-stressed countries, with agricultural water demand projected to increase 35% by 2050. The economic imperative extends beyond water costs to include regulatory compliance, as jurisdictions implement increasingly stringent water-use reporting requirements. Precision irrigation systems' ability to provide detailed consumption analytics positions them as essential compliance tools rather than optional efficiency upgrades.

High upfront capital cost for pivot systems

The capital intensity of center-pivot irrigation systems remains a significant barrier to adoption, despite improving economics and financing options. Complete pivot installations range from USD 1,200 to USD 2,000 per acre, depending on terrain and technology specifications, representing substantial capital commitments for mid-sized operations. The payback period extends to 7-10 years in regions with moderate water costs, posing a challenge to cash flow management for commodity producers facing price volatility. Equipment financing terms typically require down payments of 20-30%, creating liquidity constraints for operators seeking to modernize multiple fields simultaneously. Manufacturers are responding with modular installation approaches and lease-to-own programs, but adoption remains constrained by initial capital requirements.

Other drivers and restraints analyzed in the detailed report include:

- Labor shortages accelerating mechanization on mid-size farms

- Integration of IoT sensors enabling pay-as-you-grow models

- Fragmented land holdings limiting equipment ROI in developing countries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Drip systems retained 46.08% of the agricultural irrigation machinery market share in 2025 on superior water-use efficiency and fertigation precision. This dominance underpins a robust segment outlook as climate stresses intensify. Sprinkler equipment is the fastest-growing sub-segment, projected to post an 8.05% CAGR through 2031 as labor shortages spur mechanization across broad-acre grains. Pivot solutions unlock additional upside through sensor integration that shortens decision cycles. Valley Irrigation's AgSense 365 exemplifies the shift to unified control dashboards, lifting lifetime service value.

The segment's growth acceleration reflects improved economics as water costs rise and labor availability declines across major agricultural regions. Other irrigation types, including surface and flood systems, face declining adoption as water scarcity intensifies and regulatory frameworks increasingly favor efficiency-oriented technologies. The segmentation dynamics indicate a structural shift toward precision delivery systems capable of supporting data-driven agricultural management practices.

The Agricultural Irrigation Machinery Market Report is Segmented by Irrigation Type (Sprinkler Irrigation, Drip Irrigation, Pivot Irrigation, and Other Irrigation Types), by Application Type (Grains and Cereals, Pulses and Oilseeds, Fruits and Vegetables, and Other Applications), and by Geography (North America, Europe, Asia-Pacific, South America, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 32.12% of 2025 revenue, anchored by generous cost-share programs and mature distribution networks. Budget certainty through 2031 sustains replacement and upgrade cycles, even as market saturation moderates volume growth. Canada's climate-resilient farming priorities and Mexico's export-oriented horticulture add incremental momentum to the regional agricultural irrigation machinery market.

Asia-Pacific is positioned as the fastest-growing region at an 8.06% CAGR, boosted by water-stress mandates in China and rapid micro-irrigation rollouts under India's Pradhan Mantri Krishi Sinchayee Yojana. Japan's aging farmer demographic accelerates automation spending, while Southeast Asian greenhouse clusters seek sensor-rich drip systems. This confluence drives outsized gains in the agricultural irrigation machinery market size within Asia-Pacific through 2031.

Europe delivers steady expansion under the Common Agricultural Policy's environmental pillar, which labels precision irrigation as a sustainable activity eligible for green finance. Mediterranean drought episodes hasten subsurface installations, whereas the Netherlands and Germany emphasize closed-loop greenhouse watering. In the Middle East and Africa, state-backed megafarms and climate-smart corridors dominate demand. South America's soybean heartland invests in pivots to smooth rainfall variability, reinforcing a diversified geographic revenue stream across the agricultural irrigation machinery market.

- Netafim Ltd. (Orbia Advance Corporation)

- Valmont Industries, Inc. (Valley Irrigation)

- Lindsay Corporation

- Jain Irrigation Systems Limited (Rivulis Irrigation Limited)

- The Toro Company

- Nelson Irrigation Corporation

- Rain Bird Corporation

- Mahindra & Mahindra Limited

- Hunter Industries Incorporated

- Reinke Manufacturing Company, Inc.

- Ningbo Rainfine Irrigation Co., Ltd.

- T-L Irrigation Company

- Sistemas Azud, S.A.

- Antelco Pty Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government subsidies for micro-irrigation adoption

- 4.2.2 Rising water scarcity pushing demand for precision irrigation

- 4.2.3 Labor shortages accelerating mechanization on mid-size farms

- 4.2.4 Integration of IoT sensors enabling pay-as-you-grow service models

- 4.2.5 ESG-linked finance rewarding water-efficiency investments

- 4.2.6 Surge in carbon-credit schemes for water-saving technologies

- 4.3 Market Restraints

- 4.3.1 High upfront capital cost for pivot systems

- 4.3.2 Fragmented land holdings limiting equipment ROI in developing countries

- 4.3.3 Growing concern over plastic waste from drip lines

- 4.3.4 Cyber-vulnerability of connected irrigation networks

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of Substitute Products

- 4.6.4 Threat of New Entrants

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Irrigation Type

- 5.1.1 Sprinkler Irrigation

- 5.1.1.1 Pumping Unit

- 5.1.1.2 Tubing

- 5.1.1.3 Couplers

- 5.1.1.4 Spray or Sprinkler Heads

- 5.1.1.5 Fittings and Accessories

- 5.1.1.6 Sensors

- 5.1.1.7 Controllers

- 5.1.1.8 Injectors

- 5.1.1.9 Flow Meters

- 5.1.2 Drip Irrigation

- 5.1.2.1 Valves

- 5.1.2.2 Backflow Preventers

- 5.1.2.3 Pressure Regulators

- 5.1.2.4 Filters

- 5.1.2.5 Emitters

- 5.1.2.6 Tubing

- 5.1.2.7 Other Drip Irrigation Components

- 5.1.3 Pivot Irrigation

- 5.1.4 Other Irrigation Types

- 5.1.1 Sprinkler Irrigation

- 5.2 By Application Type

- 5.2.1 Grains and Cereals

- 5.2.2 Pulses and Oilseeds

- 5.2.3 Fruits and Vegetables

- 5.2.4 Other Applications

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Netherlands

- 5.3.2.6 Russia

- 5.3.2.7 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Cambodia

- 5.3.3.5 Rest of Asia-Pacific

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Peru

- 5.3.4.4 Rest of South America

- 5.3.5 Middle East

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 Turkey

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Egypt

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank or Share, Products and Services, Recent Developments)

- 6.4.1 Netafim Ltd. (Orbia Advance Corporation)

- 6.4.2 Valmont Industries, Inc. (Valley Irrigation)

- 6.4.3 Lindsay Corporation

- 6.4.4 Jain Irrigation Systems Limited (Rivulis Irrigation Limited)

- 6.4.5 The Toro Company

- 6.4.6 Nelson Irrigation Corporation

- 6.4.7 Rain Bird Corporation

- 6.4.8 Mahindra & Mahindra Limited

- 6.4.9 Hunter Industries Incorporated

- 6.4.10 Reinke Manufacturing Company, Inc.

- 6.4.11 Ningbo Rainfine Irrigation Co., Ltd.

- 6.4.12 T-L Irrigation Company

- 6.4.13 Sistemas Azud, S.A.

- 6.4.14 Antelco Pty Ltd.

7 Market Opportunities and Future Outlook

喷水灌溉系统市场:按类型、组件、移动性、场地规模和最终用户划分-2026-2032年全球市场预测灌溉喷灌系统市场:依系统类型、安装类型、应用和分销管道划分,全球预测,2026-2032年

喷水灌溉系统市场:按类型、组件、移动性、场地规模和最终用户划分-2026-2032年全球市场预测灌溉喷灌系统市场:依系统类型、安装类型、应用和分销管道划分,全球预测,2026-2032年 全球喷水灌溉市场:市场规模、份额和趋势分析(按类型、自动化程度、应用、组件、移动性和地区划分),细分市场预测(2026-2033 年)智慧锚桿钻机市场按操作模式、钻孔机类型、技术类型、最终用户产业和分销管道划分,全球预测(2026-2032年)滴灌管生产线市场:依管型、材质、直径、壁厚、应用及通路划分,全球预测,2026-2032年

全球喷水灌溉市场:市场规模、份额和趋势分析(按类型、自动化程度、应用、组件、移动性和地区划分),细分市场预测(2026-2033 年)智慧锚桿钻机市场按操作模式、钻孔机类型、技术类型、最终用户产业和分销管道划分,全球预测(2026-2032年)滴灌管生产线市场:依管型、材质、直径、壁厚、应用及通路划分,全球预测,2026-2032年 日本灌溉系统市场规模、份额、趋势及预测(按灌溉系统类型、作物类型、应用和地区划分,2026-2034年)

日本灌溉系统市场规模、份额、趋势及预测(按灌溉系统类型、作物类型、应用和地区划分,2026-2034年) 2026年全球中心支轴式喷灌系统市场报告2026年全球喷水灌溉市场报告2026年全球灌溉设备市场报告

2026年全球中心支轴式喷灌系统市场报告2026年全球喷水灌溉市场报告2026年全球灌溉设备市场报告 机械化灌溉系统市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、地区和竞争格局划分,2021-2031年

机械化灌溉系统市场-全球产业规模、份额、趋势、机会、预测:按类型、作物类型、地区和竞争格局划分,2021-2031年