|

市场调查报告书

商品编码

1939121

压铸:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Die Casting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

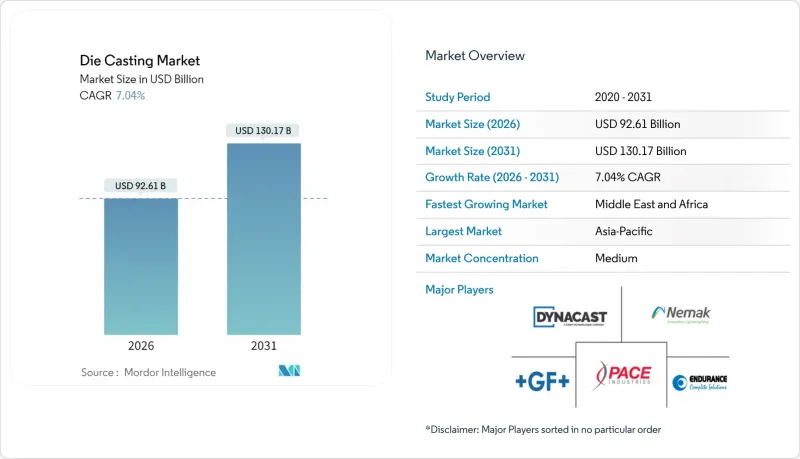

2025年压铸市场价值为865.2亿美元,预计到2031年将达到1,301.7亿美元,高于2026年的926.1亿美元。

预计在预测期(2026-2031 年)内,复合年增长率将达到 7.04%。

随着电气化重塑动力传动系统需求,原始设备製造商 (OEM) 正在用高度整合的单件铸件取代由多个冲压和焊接零件组成的组件,从而在保持结构刚性的同时减轻重量、减少零件数量。这种转变使得压铸市场即使在内燃机汽车产量趋于平稳的情况下依然保持强劲势头。由于对电池托盘、马达壳体和大型底盘铸件的需求不断增长,电动车每辆车使用的压铸件数量也在增加。除了出行领域,可再生能源基础设施、5G部署和自动化专案也在推动对复杂近净成形零件的需求。一级供应商、专业铸造厂和垂直整合的汽车製造商竞相掌握千兆压机技术、整合本地可再生能源以控製成本,并遵守模具润滑剂中禁用 PFAS 的规定,市场竞争日益激烈。

全球压铸市场趋势与洞察

在从内燃机汽车过渡到电动车的过程中,推广轻量化结构部件

儘管电池式电动车在设计上减少了零件数量,但电池外壳、马达框架和整合底盘部分等关键结构部件仍然需要采用尺寸更大的整体式铸件。特斯拉用于后底盘的巨型铸件就是一个典型的例子,它整合了多个冲压件。这表明,无论总产量如何波动,压铸对于每辆车的战略重要性和价值都在不断提升。研究表明,结构性巨型铸件可以将车辆重量减轻 10-15%,从而显着提升续航里程,同时降低组装复杂性。

用于白色车身的Gigapress近净成形压力压铸

超大型巨型压机使得以往需要多个焊接部件才能完成的一体式结构生产成为可能。传统汽车製造商正将这些压机整合到新型电动车平台中,而规模较小的铸造厂则面临早期废品率高、模具调整成本高等挑战。同时,先进的生产线正在缩短生产週期,显着降低资本投资成本,并将压铸产业整合为数量更少但规模更大的生产单位。

自2026年起,中国实施出口限制将导致镁供应面临风险

中国仍然是镁的主要供应国。然而,中国近期出台的出口许可措施显示其正在加强供应管理。此类倡议可能会扰乱下游铸造合约。西方冶炼厂需要数年时间才能提高产能,目前正面临价格波动的困扰,这使得长期汽车平臺规划更加复杂。那些利用镁比铝更轻的重量优势的汽车和航太专案正面临着艰难的抉择:重新设计零件还是囤积材料。

细分市场分析

预计到2025年,汽车应用将占总收入的61.73%,并在2031年之前以8.02%的复合年增长率成长。这表明,电动车(EV)结构件的需求正在抵消内燃机(ICE)汽车需求的下降。电池机壳、马达外壳和底盘铸件的压铸市场规模预计在预测期结束时将显着增长。汽车製造商正在调整筹资策略,将数十种冲压零件整合到少数几个大型铸件中。他们越来越重视拥有超高速压铸作业专业知识的供应商,尤其是那些拥有完美产推出週期的供应商。在汽车产业之外,可再生能源和通讯等行业的需求也在稳步增长。

同时,航太产业对钛合金和高强度铝合金作为下一代机身结构材料的兴趣日益浓厚。这项产业转型正在推动韧性合金和真空辅助填充技术的研究与开发,这两项技术均旨在满足严格的碰撞安全标准。传统上专注于引擎零件的一级供应商正在转型,改造熔炉并安装大型铸造单元,以便更专注于结构件和电池托盘的生产。这些趋势提高了中小铸造厂的准入门槛,并促使其向以枢纽为基础的工业结构转型,从而将加工和组装无缝整合到靠近原始设备製造商(OEM)车身车间的工厂中。

儘管到2025年,压力铸造仍将占总收入的55.02%,但真空铸造预计将以8.93%的复合年增长率增长,因为电动车的关键安全结构件需要可热处理和可焊接的部件。真空铸造可将孔隙率降低60-80%,使汽车製造商能够将铝製部件热处理至T6状态而无需担心断裂,然后将其雷射焊接成复合材料框架。这项技术每公斤可使价格上涨高达30%,即使合金成本上升,也能维持较高的利润率。因此,压铸市场正在增加真空室,并将冷室压铸单元改造为混合配置。

从长远来看,挤压铸造和半固体铸造过程将满足航太和重型卡车转向节等需要类似锻造微观结构的细分市场需求。然而,这些製程的生产週期仍然较长,因此在大批量生产行业,压力铸造和真空铸造仍然是首选方案,并辅以模内冷却和强化製程监控。

区域分析

到2025年,亚太地区将占全球销售额的56.21%,其中中国庞大的汽车、家电和电子产业丛集为其核心。数十年累积的专业知识、丰富的废铝供应以及垂直整合的工具钢生态系统,使其保持了成本竞争力。韩国和日本在控制系统创新方面做出了贡献,而印度则利用与生产连结奖励计画来资金筹措新的轻量化零件生产线。随着整车製造商采购管道的多元化,东南亚在低复杂度零件和备用产能方面占据了越来越大的份额,从而扩大了压铸市场在东盟的影响力。

中东和非洲地区是成长最快的地区,复合年增长率达8.42%。波湾合作理事会成员国正利用「2030愿景」基金在国内生产太阳能逆变器、风力涡轮机外壳和电动车充电器。像NEOM这样的大型企划正在推动对能够铸造铝製建筑幕墙节点和结构连接件的大吨位压平机的需求。儘管上游铝锭供应在冶炼厂扩大规模之前仍依赖进口,但土耳其的汽车出口和埃及的工业园区计划进一步刺激了该地区的订单。

北美和欧洲的成长主要由技术变革驱动,而非工厂数量的增加。在美国,针对国内采购电池和传动系统零件的税额扣抵促使原始设备製造商(OEM)在俄亥俄州、阿拉巴马州和安大略省的组装厂附近建造大型铸造厂。欧洲的碳边境调节机制提高了使用可再生能源运作再生铝熔炉的本地工厂的竞争力。在这两个地区,逐步淘汰全氟烷基和多氟烷基物质(PFAS)以及实施生命週期碳审核正在推动压铸市场的发展,加速设备升级和数位化可追溯性模组的应用。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 将内燃机汽车的轻量化结构件推广到电动车上

- 用于白色车身的Gigapress近净成形压铸

- 模内感测器可实现零缺陷“一次成型”质量

- 循环经济中的铝回收强制令推动了二次高压压铸需求

- 利用铸造厂现场可再生能源进行能源价格对冲

- 透过3D砂型列印核心实现复杂的电动车形状

- 市场限制

- 自2026年起,中国实施出口限制将导致镁供应面临风险

- 加强润滑油中 PFAS排放法规

- GigaPress 技术使原始设备製造商 (OEM) 能够自行生产,从而减少从一级供应商订单。

- 欧盟碳边境调节税提高了高耗能铸造厂的成本基础

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力模型

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模及成长预测(价值(美元))

- 透过使用

- 车

- 电气和电子设备

- 工业机械

- 航太/国防

- 消费性电子产品

- 其他的

- 透过流程

- 高压压铸

- 真空压铸

- 挤压压铸

- 重力压铸

- 按原料

- 铝

- 镁

- 锌

- 铜

- 其他(铅、锡合金)

- 透过铸造机的夹紧力

- ≤4,000 kN

- 4,001 至 10,000 千牛

- 超过10,000千牛

- 按地区

- 北美洲

- 我们

- 加拿大

- 北美其他地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 泰国

- 印尼

- 马来西亚

- 澳洲

- 亚太其他地区

- 中东和非洲

- 阿拉伯聯合大公国

- 沙乌地阿拉伯

- 土耳其

- 埃及

- 南非

- 其他中东和非洲地区

- 北美洲

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率分析

- 公司简介

- Form Technologies Inc.(Dynacast)

- Nemak SAB de CV

- Endurance Technologies Limited

- Sundaram Clayton Ltd

- Shiloh Industries, inc.

- Georg Fischer Ltd

- Gibbs Die Casting Corporation

- Bocar Group

- Engtek Group

- Rheinmetall AG

- Rockman Industries Limited

- Ryobi Die Casting

- Linamar Corporation

- Meridian Lightweight Technologies Inc.

- Sandhar Group

- Alcoa Corporation

- Pace Industries Inc.

- CIE Automotive

- China Hongqiao Group Limited

- Consolidated Metco, Inc.

第七章 市场机会与未来展望

The die casting market was valued at USD 86.52 billion in 2025 and estimated to grow from USD 92.61 billion in 2026 to reach USD 130.17 billion by 2031, at a CAGR of 7.04% during the forecast period (2026-2031).

As electrification reshapes power-train needs, OEMs are replacing multi-piece stamp-and-weld assemblies with single, high-integrity castings that cut weight and part counts while preserving structural rigidity. This pivot keeps the die casting market resilient even as internal-combustion volumes plateau, because the content-per-vehicle in electric cars rises on the back of battery trays, motor housings, and under-body megacastings. Outside mobility, renewable-energy infrastructure, 5G rollouts, and automation programs sustain demand for complex, near-net-shape components. Competitive intensity tightens as tier-1 suppliers, pure-play foundries, and vertically integrating automakers race to master giga-press technology, deploy on-site renewables for cost control, and navigate looming PFAS bans in mold lubricants.

Global Die Casting Market Trends and Insights

ICE-to-EV Structural-Parts Lightweighting Push

Battery-electric vehicles streamline their design with fewer components, yet they demand larger, integrated castings for essential structures such as battery housings, motor frames, and unified chassis sections. A prime example is Tesla's rear underbody megacasting, which consolidates several stamped parts. This underscores the rising strategic significance and value of die casting in each vehicle, regardless of fluctuations in overall production volumes. Studies indicate structural megacasting can reduce curb weight by 10-15%, bringing critical range benefits while lowering assembly complexity .

Near-Net-Shape Pressure-Die-Casting for Giga-Press Body-in-White

Ultra-large giga-presses now create single-piece structures, a feat that once demanded multiple welded components. While traditional automakers are integrating these presses into their new electric vehicle platforms, smaller foundries grapple with challenges like high initial scrap rates and expensive die adjustments. Meanwhile, advanced equipment lines are achieving quicker cycle times, a move that mitigates hefty capital costs and pushes the die-casting industry towards consolidating into fewer, yet significantly larger, production cells.

Post-2026 Magnesium Supply Risk from China Export Controls

China continues to lead as the primary source of magnesium. However, recent export licensing measures from the country hint at tighter supply controls. Such moves could potentially disrupt downstream casting contracts. Western smelters, taking years to ramp up, are grappling with price volatility, complicating long-term vehicle platform planning. Programs in the automotive and aerospace sectors, which have relied on magnesium's lightweight benefits over aluminum, now confront difficult decisions: redesigning components or stockpiling the material.

Other drivers and restraints analyzed in the detailed report include:

- In-Mold Sensors Enabling Zero-Defect "First-Shot" Quality

- Circular-Economy Aluminum-Recycling Mandates Spur Secondary HPDC Demand

- Tightening PFAS Emissions Norms on Lubricants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automotive applications contributed 61.73% of 2025 revenues and will deliver an 8.02% CAGR to 2031, illustrating how EV structural content offsets ICE decline. The die casting market size for battery enclosures, motor housings, and under-body castings will grow significantly by the end of the forecast period. Automakers are consolidating dozens of stamped components into just a few large castings, leading to a shift in sourcing strategies. They're now favoring suppliers adept at giga-press operations, especially those with flawless startup cycles. Beyond the automotive realm, sectors like renewable energy and telecom are witnessing a steady uptick in demand.

Meanwhile, the aerospace industry is showing heightened interest in titanium and high-strength aluminum, eyeing them for next-generation airframes. This industry-wide transition is spurring intensified R&D efforts into ductile alloys and vacuum-assisted filling, all in a bid to meet stringent crash safety standards. Tier-1 suppliers, previously centered on engine parts, are now pivoting. They're retrofitting furnaces and setting up massive casting cells, focusing on structural components and battery trays. Such trends are elevating entry barriers for smaller foundries and nudging the industry towards integrated hubs, seamlessly blending machining and assembly close to OEM body shops.

While pressure casting still owns 55.02% of 2025 billings, vacuum casting will clock a 8.93% CAGR as safety-critical EV structures require heat-treatable, weldable parts. When pore content falls 60-80%, automakers can T6-treat aluminum parts without blow-out risk and laser-weld them into multi-material frames. That capability lifts price realizations by up to 30% per kilogram, keeping margin potential high even where alloy cost rises. Consequently, the die casting market sees plants adding vacuum chambers or converting cold-chamber cells to hybrid configurations.

Longer term, squeeze casting and semi-solid processes address niche aerospace and heavy-truck steering knuckles that need forged-like microstructures. Yet their cycle times remain slower, so high-volume industries still favor pressure or vacuum options supplemented by in-die cooling and intensified process monitoring.

The Die Casting Market Report is Segmented by Application (Automotive, Electrical and Electronics, and More), Process (Pressure Die Casting, Vacuum Die Casting, and More), Raw Material (Aluminum, Magnesium, and More), Casting-Machine Clamping Force (<=4, 000 KN, 4, 001-10, 000 KN, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 56.21% of global sales in 2025, anchored by China's vast auto, appliance and electronics clusters. Decades of cumulative know-how, high scrap-aluminum availability, and vertically integrated tool-steel ecosystems keep cost positions sharp. Korea and Japan contribute control-system innovation, while India rides production-linked incentives that fund new lightweight-component lines. As OEMs diversify sourcing, Southeast Asia gains share for low-complexity parts and back-up capacity, broadening the die casting market footprint across ASEAN.

The Middle East & Africa region is the fastest riser at 8.42% CAGR. Gulf Cooperation Council states use Vision 2030 funds to manufacture solar inverters, wind housings, and EV chargers domestically. Megaprojects like NEOM draw demand for high-tonnage presses able to cast aluminum facade nodes and structural connectors. Turkey's auto exports and Egypt's industrial-park policies further energize regional orders, though upstream ingot supply relies on imports until smelters scale.

North America and Europe grow chiefly through technology shifts rather than plant count. United States tax credits favor domestic battery and drivetrain sourcing, causing OEMs to localize megacasting next to assembly plants in Ohio, Alabama, and Ontario. Europe's Carbon Border Adjustment Mechanism boosts competitive standing for regional shops running recycled aluminum furnaces on renewable power. Both regions further the die casting market by enforcing PFAS phase-outs and lifecycle carbon audits, spurring capital upgrades and digital traceability modules.

- Form Technologies Inc. (Dynacast)

- Nemak S.A.B. de C.V.

- Endurance Technologies Limited

- Sundaram Clayton Ltd

- Shiloh Industries, inc.

- Georg Fischer Ltd

- Gibbs Die Casting Corporation

- Bocar Group

- Engtek Group

- Rheinmetall AG

- Rockman Industries Limited

- Ryobi Die Casting

- Linamar Corporation

- Meridian Lightweight Technologies Inc.

- Sandhar Group

- Alcoa Corporation

- Pace Industries Inc.

- CIE Automotive

- China Hongqiao Group Limited

- Consolidated Metco, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 ICE-to-EV Structural-Parts Lightweighting Push

- 4.2.2 Near-Net-Shape Pressure-Die-Casting for Giga-Press Body-in-White

- 4.2.3 In-Mold Sensors Enabling Zero-Defect "First-Shot" Quality

- 4.2.4 Circular-Economy Aluminum-Recycling Mandates Spur Secondary HPDC Demand

- 4.2.5 Energy-Price Hedging via On-Site Renewables at Foundries

- 4.2.6 3D-Sand-Printed Cores Unlocking Complex EV Geometries

- 4.3 Market Restraints

- 4.3.1 Post-2026 Magnesium Supply Risk from China Export Controls

- 4.3.2 Tightening PFAS Emissions Norms on Lubricants

- 4.3.3 OEM Insourcing with Giga-Pressing Reducing Tier-1 Volumes

- 4.3.4 EU Carbon-Border Taxes Raising Cost Base for Energy-Intensive Foundries

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Automotive

- 5.1.2 Electrical and Electronics

- 5.1.3 Industrial Machinery

- 5.1.4 Aerospace and Defense

- 5.1.5 Consumer Appliances

- 5.1.6 Others

- 5.2 By Process

- 5.2.1 Pressure Die Casting

- 5.2.2 Vacuum Die Casting

- 5.2.3 Squeeze Die Casting

- 5.2.4 Gravity Die Casting

- 5.3 By Raw Material

- 5.3.1 Aluminum

- 5.3.2 Magnesium

- 5.3.3 Zinc

- 5.3.4 Copper

- 5.3.5 Others (Lead, Tin Alloys)

- 5.4 By Casting-Machine Clamping Force

- 5.4.1 <=4,000 kN

- 5.4.2 4,001-10,000 kN

- 5.4.3 Above 10,000 kN

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Thailand

- 5.5.4.6 Indonesia

- 5.5.4.7 Malaysia

- 5.5.4.8 Australia

- 5.5.4.9 Rest of Asia-Pacific

- 5.5.5 Middle-East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Egypt

- 5.5.5.5 South Africa

- 5.5.5.6 Rest of Middle-East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Form Technologies Inc. (Dynacast)

- 6.4.2 Nemak S.A.B. de C.V.

- 6.4.3 Endurance Technologies Limited

- 6.4.4 Sundaram Clayton Ltd

- 6.4.5 Shiloh Industries, inc.

- 6.4.6 Georg Fischer Ltd

- 6.4.7 Gibbs Die Casting Corporation

- 6.4.8 Bocar Group

- 6.4.9 Engtek Group

- 6.4.10 Rheinmetall AG

- 6.4.11 Rockman Industries Limited

- 6.4.12 Ryobi Die Casting

- 6.4.13 Linamar Corporation

- 6.4.14 Meridian Lightweight Technologies Inc.

- 6.4.15 Sandhar Group

- 6.4.16 Alcoa Corporation

- 6.4.17 Pace Industries Inc.

- 6.4.18 CIE Automotive

- 6.4.19 China Hongqiao Group Limited

- 6.4.20 Consolidated Metco, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment

压铸和锻造市场:2026-2032年全球市场预测(按製造流程、材料、产品类型、最终用途产业和销售管道划分)压铸市场:2026-2032年全球市场预测(依製造流程、材料、模具类型、机器类型、机器吨位、铸件尺寸及最终用途产业划分)压铸机械市场:依金属类型、机械类型、技术、夹紧力和最终用途产业划分-2026-2032年全球市场预测铝零件重力铸造市场:依产品类型、合金、重量、最终用途产业和销售管道划分-2026-2032年全球市场预测工业铸造市场:按类型、材料、应用和最终用户产业划分-2026-2032年全球市场预测真空铝铸造市场:依製程类型、合金类型、产品类型及应用划分,2026-2032年全球预测燃烧室铸件市场:按部件类型、铸造工艺、材料类型、铸造工艺技术和最终用途行业划分,全球预测,2026-2032年压铸机自动取料机市场按机器类型、金属类型、扣夹力、自动化类型、最终用途产业和销售管道划分,全球预测,2026-2032年小型热室压铸机市场(按合金、操作方式、机器类型和最终用途产业划分),全球预测(2026-2032年)

压铸和锻造市场:2026-2032年全球市场预测(按製造流程、材料、产品类型、最终用途产业和销售管道划分)压铸市场:2026-2032年全球市场预测(依製造流程、材料、模具类型、机器类型、机器吨位、铸件尺寸及最终用途产业划分)压铸机械市场:依金属类型、机械类型、技术、夹紧力和最终用途产业划分-2026-2032年全球市场预测铝零件重力铸造市场:依产品类型、合金、重量、最终用途产业和销售管道划分-2026-2032年全球市场预测工业铸造市场:按类型、材料、应用和最终用户产业划分-2026-2032年全球市场预测真空铝铸造市场:依製程类型、合金类型、产品类型及应用划分,2026-2032年全球预测燃烧室铸件市场:按部件类型、铸造工艺、材料类型、铸造工艺技术和最终用途行业划分,全球预测,2026-2032年压铸机自动取料机市场按机器类型、金属类型、扣夹力、自动化类型、最终用途产业和销售管道划分,全球预测,2026-2032年小型热室压铸机市场(按合金、操作方式、机器类型和最终用途产业划分),全球预测(2026-2032年) 压铸市场规模、份额、趋势及预测(依製造流程、原料、应用及地区划分),2026-2034年

压铸市场规模、份额、趋势及预测(依製造流程、原料、应用及地区划分),2026-2034年