|

市场调查报告书

商品编码

1939122

防腐蚀涂料:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Anti-Corrosion Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

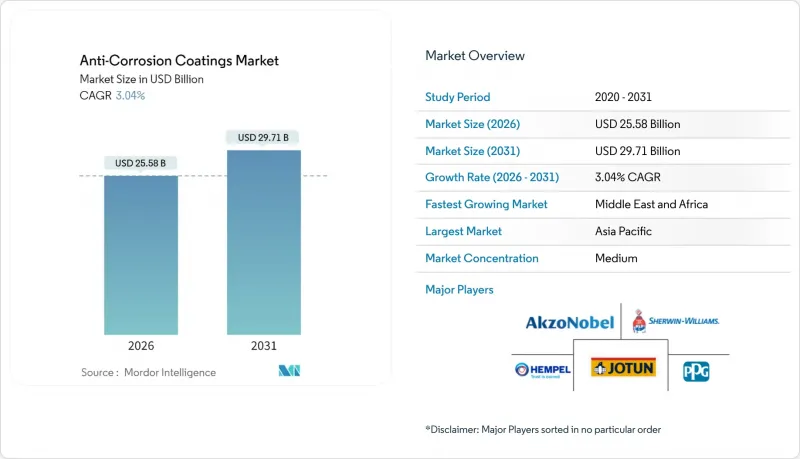

预计防腐蚀涂料市场将从 2025 年的 248.2 亿美元成长到 2026 年的 255.8 亿美元,到 2031 年将达到 297.1 亿美元,2026 年至 2031 年的复合年增长率为 3.04%。

公共部门基础设施投资的增加、离岸风力发电电场规范的日益严格以及浮式生产储油卸油设备油船(FPSO)维修週期的延长,正推动防腐蚀涂料市场从以销量主导主导的模式向以性能主导的模式转变。虽然水性涂料在严格监管的领域越来越受欢迎,但在失效风险大于环境影响的领域,溶剂型涂料仍然占据主导地位。树脂技术的创新也不断进步,生物基环氧树脂和混合聚氨酯系统在兼顾永续性和耐久性竞标越来越受到关注。液化天然气(LNG接收站对隔热材料下防腐蚀解决方案日益增长的需求,凸显了市场正从通用维护涂料到特定应用工程涂料的转变。

全球防腐蚀涂料市场趋势及洞察

美国、欧盟和日本的基础建设更新超级週期

大规模政府专案正在推动对高性能涂料的需求,这些涂料的使用寿命远远超过传统的维护週期。美国《基础建设投资与就业法案》拨款5,500亿美元用于维修使用寿命长的桥樑、铁路和港口设施。欧洲绿色交易的资金优先考虑低挥发性有机化合物(VOC)和耐用产品,引导设计负责人采用生物基环氧树脂和混合聚氨酯系统。日本国家韧性计画要求隧道和海岸防御设施采用柔软性且抗震的涂层,推动了对更坚韧的聚氨酯弹性体化学的研究。这些协同效应正在推动涂料从基础醇酸树脂涂料稳步过渡到可提供25-30年保护週期的工程系统。能够提供全生命週期保固和快速反应的现场技术支援的供应商正在获得更高的利润,因为业主将涂料视为策略性的风险缓解工具,而不是消耗品。

离岸风力发电电场涂料需求激增

到2030年,全球离岸风力发电装置容量预计将超过380吉瓦,将对单桩基础、过渡段和机舱保护等零件提出特殊要求。涡轮机部件需要能够承受循环盐雾、漂浮物衝击和阴极剥离的涂层。奈米陶瓷增强环氧底漆与脂肪族聚氨酯面漆的组合正逐渐成为标准,因为它们能够在25年的使用寿命内保持光泽和阻隔性能。在联邦政府30吉瓦蓝图的推动下,美国东海岸的计划越来越多地采用水性或高固态涂料,这些涂料既符合严格的VOC法规,又不会影响性能。製造涡轮机导管架的亚洲造船厂正在加快类似系统的认证,以确保符合欧洲开发商的竞标要求,这加剧了全球特殊防腐蚀原料供应链的压力。

全球更严格的挥发性有机化合物(VOC)法规和异氰酸酯暴露限值

美国和欧盟部分地区对挥发性有机化合物(VOC)含量限制(50克/公升)的调整,给溶剂型聚氨酯涂料的销售带来了压力。製造商被迫转向水性涂料和高固态涂料,而这些涂料对固化时间和现场湿度控制的要求越来越高。额外的培训、设备改造和第三方认证成本正在挤压利润空间,同时,与传统溶剂型技术相比,性能差距仍然是船舶和重工业用户关注的问题。同时,关于二异氰酸酯标籤的新REACH法规增加了跨境运输双组分聚氨酯的物流障碍,并延长了关键维护期间的前置作业时间。

细分市场分析

到2025年,环氧涂料将占据防腐蚀涂料市场38.92%的份额,这主要得益于其卓越的附着力和耐化学性(尤其是在船舶安定器舱和桥樑樑体中)。近期开发的生物基环氧涂料正在蚕食传统双酚A基涂料的市场份额,因为它们符合绿色采购标准,且不影响盐雾试验时间(耐腐蚀性)。儘管原料成本有所波动,但该细分市场仍保持强劲势头,配方师正透过优化稀释剂来稳定交付价格。

聚氨酯的销售成长最为迅猛,年复合成长率高达3.79%,这主要得益于开发商选择其柔性薄膜用于离岸风力发电塔架,以吸收振动并增强抗机械分层性能。在地震频繁的亚洲地区,聚氨酯在交通隧道中的应用日益广泛,进一步缩小了其与环氧树脂之间的差距。儘管醇酸树脂、聚酯树脂和乙烯基酯树脂在成本至关重要或需要极高耐化学性的细分市场中仍占有一席之地,但环氧底漆与聚氨酯面漆相结合的混合技术正在成为长寿命钢结构的主要涂料选择。

防腐蚀涂料报告按树脂类型(环氧树脂、醇酸树脂、聚酯树脂、聚氨酯树脂等)、技术(水性、溶剂型、粉末涂料、紫外光固化涂料等)、终端用户产业(石油天然气、船舶、电力、基础设施、工业、航太与国防等)以及地区(亚太地区、北美地区、欧洲地区等)进行细分。市场预测以美元计价。

区域分析

受中国「一带一路」港口扩建、印度离岸风力发电订单以及日本抗震基础设施建设规划的推动,亚太地区预计到2025年将占全球收入的46.60%。国内製造商受益于一体化的树脂生产基地,缩短了前置作业时间并降低了外汇风险;同时,日益严格的当地环保法规也推动了沿海省份水性涂料的普及。东南亚造船厂正在采用符合国际海事组织(IMO)PSPC核准的涂料系统,以订单,这进一步提振了对全球高端品牌的需求。

北美市场继续占据较大份额,这主要得益于《基础设施投资和就业创造法案》下桥樑和隧道维修计划的持续推进,以及美国墨西哥湾沿岸石化工厂不断上涨的维护成本。为了加快恢復速度,最大限度地减少繁忙州际公路的车道封闭,涂料製造商正转向使用高固态环氧涂料。

在欧洲,绿色交易补贴正在催生一个成熟的市场,资金与低挥发性有机化合物(VOC)、生物基和再生材料製成的涂料挂钩。为了满足更严格的健康法规,北海的船舶修理厂正在采用先进的硅酸锌基底漆,这种底漆与快干、无溶剂面漆相容。

预计到2031年,中东和非洲地区的复合年增长率将达到3.36%,主要得益于沙乌地阿拉伯NEOM新城和奈及利亚海事中心等大型企划的推动。高紫外线照射、砂粒磨损和高盐度环境要求使用高品质的含氟聚合物面漆,并结合玻璃鳞片环氧树脂。技术优势而非价格优势是赢得合约的关键因素。阿曼和卡达炼油厂产能的扩张正在推动对耐腐蚀底涂层(CUI)内衬的需求稳定成长,这些内衬将应用于数公里长的保温管道。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 美国、欧盟和日本的基础建设更新超级週期

- 离岸风力发电涂料需求快速成长

- 拉丁美洲和西非的FPSO维修日益增多

- LNG接收站的隔热材料层下腐蚀(CUI)失效

- 生物基树脂创新确保「绿色采购」竞标

- 市场限制

- 全球范围内VOC法规和异氰酸酯暴露限值日益收紧

- 奈米陶瓷分散生产线需要高资本投入

- 环氧树脂原料价格波动(BisA、ECH)

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 依树脂类型

- 环氧树脂

- 醇酸树脂

- 聚酯纤维

- 聚氨酯

- 乙烯基酯树脂

- 其他树脂类型

- 透过技术

- 水性涂料

- 溶剂型

- 粉末

- 紫外线固化

- 按最终用户行业划分

- 石油和天然气

- 海上

- 电力

- 基础设施

- 产业

- 航太与国防

- 运输

- 其他终端用户产业

- 按地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 东南亚国协

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 西班牙

- 义大利

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 南非

- 奈及利亚

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率/排名分析

- 公司简介

- Akzo Nobel NV

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India

- Carboline

- Chugoku Marine Paints, Ltd.

- HB Fuller Company

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila

第七章 市场机会与未来展望

The Anti-Corrosion Coatings Market is expected to grow from USD 24.82 billion in 2025 to USD 25.58 billion in 2026 and is forecast to reach USD 29.71 billion by 2031 at 3.04% CAGR over 2026-2031.

Strong public-sector infrastructure spending, more demanding offshore wind specifications, and the expanding refurbishment cycle for floating production storage offloading (FPSO) vessels are shifting the anti-corrosion coatings market from a volume-led arena to a performance-driven ecosystem. Water-borne chemistries are advancing in regulatory-sensitive regions, yet solvent-borne systems still dominate where failure risk outweighs environmental trade-offs. Resin innovation is also accelerating, with bio-based epoxies and hybrid polyurethane systems gaining traction in bids that score sustainability alongside lifetime durability. Greater demand for corrosion-under-insulation solutions at LNG terminals highlights the market's transition from generalized maintenance paints toward application-specific engineered coatings.

Global Anti-Corrosion Coatings Market Trends and Insights

Infrastructure Renewal Super-cycle in U.S., EU and Japan

Massive government programs are steering demand toward high-performance coatings that extend service life well beyond conventional maintenance cycles. The Infrastructure Investment and Jobs Act in the United States earmarked USD 550 billion for upgrades that prioritize long-life bridge, rail, and port assets. European Green Deal allocations link funding to low-VOC, high-durability products, nudging specifiers toward bio-based epoxy and hybrid polyurethane systems. Japan's national resilience plan requires flexible, seismic-resistant finishes for tunnels and coastal defenses, propelling research into tougher polyurethane elastomer chemistries. The combined effect is a steady replacement of basic alkyd films with engineered systems offering 25-30-year protection intervals. Suppliers capable of lifecycle assurance and rapid on-site technical support are capturing premium margins as owners view coatings as strategic risk mitigators rather than consumables.

Offshore Wind Farm Coating Demand Surge

Global offshore wind capacity is targeted to exceed 380 GW by 2030, driving specialized needs for monopile, transition-piece, and nacelle protection. Turbine components demand coatings that withstand cyclical salt spray, impact from floating debris, and cathodic disbondment. Nano-ceramic-reinforced epoxy primers topped with aliphatic polyurethane finishes are emerging as a standard stack because they retain gloss and barrier integrity for 25-year service windows. U.S. East Coast projects, galvanized by a federal roadmap for 30 GW of installations, are specifying water-borne or high-solids variants to honor strict VOC caps without compromising performance. Asian yards fabricating turbine jackets are fast-tracking qualification of similar systems to stay compliant with European developer tenders, tightening global raw-material supply chains for specialty anticorrosive pigments.

Tightening Global VOC Caps and Isocyanate Exposure Limits

Revised limits of 50 g/L VOC in several U.S. and EU districts are squeezing solvent-borne polyurethane sales. Manufacturers must invest in water-borne or high-solids upgrades, often accepting slower cure times and stricter humidity controls on job sites. The added training, equipment adaptation, and third-party certification expenses erode margins while the performance gap relative to legacy solvent technologies still worries marine and heavy-industrial users. In parallel, new REACH rules on di-isocyanate labeling raise logistical hurdles for shipping two-pack polyurethanes across borders, extending lead times in critical maintenance windows.

Other drivers and restraints analyzed in the detailed report include:

- Growing FPSO Refurbishments in Latin America and West Africa

- Corrosion-under-insulation Failures in LNG Terminals

- High Capex for Nano-ceramic Dispersion Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy systems accounted for 38.92% of the anti-corrosion coatings market size in 2025, thanks to unmatched adhesion and chemical resistance, especially in marine ballast tanks and bridge girders. Recent bio-based epoxy variants satisfy green-procurement scoring without sacrificing salt-spray hours, pulling share from conventional bis-A formulations. The segment remains resilient despite raw-material cost swings, as formulators lean on diluent optimization to keep delivered prices stable.

Polyurethane volumes are expanding fastest, supported by a 3.79% CAGR as developers choose flexible films that absorb vibration and resist mechanical chipping on offshore wind towers. Growing polyurethane acceptance in seismic-prone Asian transport tunnels further narrows the gap to epoxy. Alkyd, polyester, and vinyl ester niches maintain relevance where cost sensitivity or extreme chemical resistance dictates, but hybrid technology blending epoxy primers with polyurethane topcoats now dominates specification sheets for long-life steel infrastructure.

The Anti-Corrosion Coatings Report is Segmented by Resin Type (Epoxy, Alkyds, Polyester, Polyurethane, and More), Technology (Water-Borne, Solvent-Borne, Powder, and UV-Cured), End-User Industry (Oil and Gas, Marine, Power, Infrastructure, Industrial, Aerospace and Defense, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 46.60% of 2025 revenue, driven by China's Belt and Road port expansions, India's offshore wind farm orders, and Japan's seismic infrastructure initiatives. Domestic manufacturers benefit from integrated resin production hubs that compress lead times and reduce currency risk, yet rising local environmental rules are pushing waterborne adoption in coastal provinces. Southeast Asian shipyards, eager to win EU-flag vessel contracts, are aligning with IMO PSPC-approved coating systems, adding further pull for global premium brands.

North America's share remains sizeable owing to the Infrastructure Investment and Jobs Act pipeline of bridge and tunnel rehabilitation, combined with elevated maintenance spending on U.S. Gulf Coast petrochemical plants. Specifiers are pivoting toward high-solids epoxies with rapid return-to-service properties to minimize lane-closure durations on busy interstates.

Europe hosts a sophisticated market where Green Deal subsidies tie funding to low-VOC, bio-based, or recycled-content coatings. Ship repair yards in the North Sea embrace advanced zinc-silicate primers compatible with fast-flush solvent-free topcoats to rebalance stricter health regulations.

The Middle East and Africa is projected to rise at a3.36% CAGR through 2031 due to mega-projects such as Saudi Arabia's NEOM and Nigeria's offshore hubs. High UV levels, sand abrasion, and salinity demand premium fluoropolymer topcoats paired with glass-flake epoxies, positioning technical superiority over price as the chief contract award criterion. Rising refinery capacity in Oman and Qatar fuels steady demand for CUI-resistant linings across kilometers of insulated piping.

- Akzo Nobel N.V.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India

- Carboline

- Chugoku Marine Paints, Ltd.

- H.B. Fuller Company

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Infrastructure renewal super-cycle in U.S., EU and Japan

- 4.2.2 Offshore wind farm coating demand surge

- 4.2.3 Growing FPSO refurbishments in Latin America and West Africa

- 4.2.4 Corrosion-under-insulation (CUI) failures in LNG terminals

- 4.2.5 Bio-based resin innovations securing "green procurement" bids

- 4.3 Market Restraints

- 4.3.1 Tightening global VOC caps and isocyanate exposure limits

- 4.3.2 High capex for nano-ceramic dispersion lines

- 4.3.3 Volatility in epoxy raw material prices (bis-A, ECH)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Epoxy

- 5.1.2 Alkyds

- 5.1.3 Polyester

- 5.1.4 Polyurethane

- 5.1.5 Vinyl Ester

- 5.1.6 Other Resin Types

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Powder

- 5.2.4 UV-cured

- 5.3 By End-user Industry

- 5.3.1 Oil and Gas

- 5.3.2 Marine

- 5.3.3 Power

- 5.3.4 Infrastructure

- 5.3.5 Industrial

- 5.3.6 Aerospace and Defense

- 5.3.7 Transportation

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Axalta Coating Systems, LLC

- 6.4.3 BASF

- 6.4.4 Beckers Group

- 6.4.5 Berger Paints India

- 6.4.6 Carboline

- 6.4.7 Chugoku Marine Paints, Ltd.

- 6.4.8 H.B. Fuller Company

- 6.4.9 Hempel A/S

- 6.4.10 Jotun

- 6.4.11 Kansai Paint Co., Ltd.

- 6.4.12 Nippon Paint Holdings Co., Ltd.

- 6.4.13 PPG Industries, Inc.

- 6.4.14 RPM International Inc.

- 6.4.15 Sika AG

- 6.4.16 Teknos Group

- 6.4.17 The Sherwin-Williams Company

- 6.4.18 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

腐蚀防护奈米工程半导体涂层市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材质、製程、最终用户及功能划分

腐蚀防护奈米工程半导体涂层市场分析及预测(至2035年):依类型、产品、服务、技术、应用、材质、製程、最终用户及功能划分 全球防腐蚀涂料市场规模、份额、趋势和成长分析报告(2026-2034)

全球防腐蚀涂料市场规模、份额、趋势和成长分析报告(2026-2034) 2026年全球防腐蚀涂料市场报告

2026年全球防腐蚀涂料市场报告 防腐涂料市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、最终用途、地区和竞争格局划分,2021-2031年)

防腐涂料市场-全球产业规模、份额、趋势、机会及预测(按类型、技术、最终用途、地区和竞争格局划分,2021-2031年) 2026-2030年全球防腐蚀涂料市场

2026-2030年全球防腐蚀涂料市场 桥樑涂料市场按树脂类型、基材类型、应用和最终用途划分,全球预测(2026-2032)

桥樑涂料市场按树脂类型、基材类型、应用和最终用途划分,全球预测(2026-2032) 日本防腐蚀涂料市场报告:按技术、材料、应用和地区划分(2026-2034年)

日本防腐蚀涂料市场报告:按技术、材料、应用和地区划分(2026-2034年) 防腐涂料市场规模、份额及成长分析(按类型、技术、最终用途产业和地区划分)-产业预测(2026-2033 年)防腐蚀涂料市场-2025-2030年预测

防腐涂料市场规模、份额及成长分析(按类型、技术、最终用途产业和地区划分)-产业预测(2026-2033 年)防腐蚀涂料市场-2025-2030年预测 全球防腐蚀涂料市场:预测至2032年-按类型、材料、技术、应用、最终用户和地区分類的分析

全球防腐蚀涂料市场:预测至2032年-按类型、材料、技术、应用、最终用户和地区分類的分析