|

市场调查报告书

商品编码

1939133

无线路由器:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Wireless Router - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

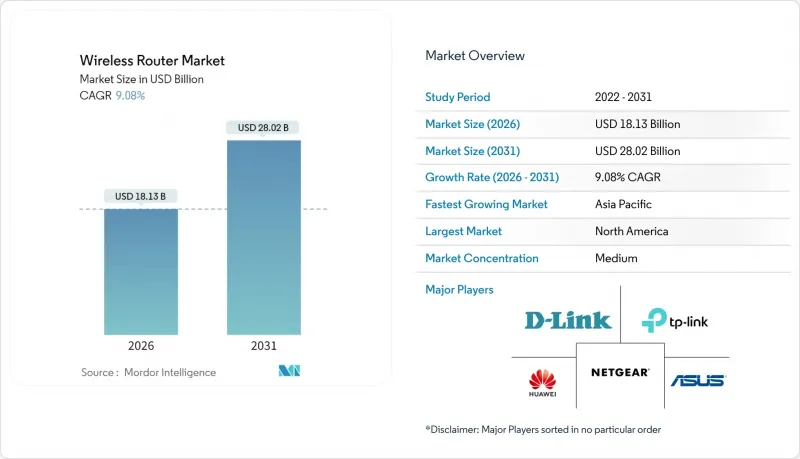

预计到 2026 年,无线路由器市值将达到 181.3 亿美元,从 2025 年的 166.2 亿美元成长到 2031 年的 280.2 亿美元。

预计2026年至2031年年复合成长率(CAGR)为9.08%。

这一成长主要得益于企业数位化的快速推进、住宅频宽需求的不断增长以及Wi-Fi 7的快速商业化。预计2024年Wi-Fi 7设备的出货量将达到2.69亿台,到2028年将超过21亿台,这印证了市场对千兆Gigabit性能日益增长的潜在需求。同时,6GHz Wi-Fi硬体也正在快速成长(预计2024年出货量将达到8.075亿台),并且已有63个国家开放了部分6GHz频谱供免许可使用,这进一步推动了Wi-Fi生态系统的发展。网状网路系统、高频宽三频设计以及ISP管理的CPE捆绑包是推动市场需求的主要因素,而固定无线存取和半导体供应的限制则导致了局部的波动。为了维持定价优势并因应来自低成本中国供应商日益激烈的竞争,各厂商正竞相为产品添加人工智慧驱动的管理和网路即服务(NaaS)功能。

全球无线路由器市场趋势与洞察

网路流量和连网设备不断增加

目前全球已有超过211亿台Wi-Fi设备运作,预计2024年还将新增41亿台。这使得传统网路不堪重负,并促使用户升级到Gigabit路由器。约五分之一的住宅宽频用户每月资料通讯使用量超过1TB,这给服务品质带来了巨大压力。物联网在智慧工厂、智慧城市和自动驾驶汽车等领域的快速发展,进一步推动了对Wi-Fi 7 320 MHz频道所能提供的低延迟吞吐量的需求。随着Wi-Fi 6网路基地台逐渐接近其实际应用极限,企业面临设备密度的挑战,迫使他们投资下一代无线设备。这导致设备更新换代週期加快,而拥有Wi-Fi 7产品线的厂商则从中受益。

企业数位化推动频宽需求

目前,已有45%的企业正在并行试点Wi-Fi 6和私人5G网络,这清楚地显示了无线基础设施一体化的发展趋势。製造工厂正在采用Wi-Fi 7来实现人工智慧机器人、亚毫秒级监控控制和机器视觉分析。到2025年,主要供应商的人工智慧基础设施路由器季度订单将超过3.5亿美元。基于订阅的网路即服务(NaaS)模式降低了资本投资门槛,并实现了快速部署。简而言之,频宽应用以及灵活的资金筹措正在推动无线路由器市场向前发展。

网路安全领域日益复杂且技能短缺

一次利用华硕路由器漏洞 CVE-2024-3080 发动的 3.8Tbps DDoS 攻击凸显了业界韧体漏洞的脆弱性。同时,通讯业者报告称,合格的网路工程师缺口高达 33%,尤其是那些能够处理新兴的 Wi-Fi 7 安全性和 WPA3 配置的工程师。由于需要专家咨询,企业面临不断上涨的部署成本和漫长的计划前置作业时间。中小企业往往配置鬆懈,这增加了安全漏洞的风险,并限制了具备高阶威胁侦测功能的高阶路由器的普及。

细分市场分析

儘管独立路由器在2025年仍将保持43.62%的市场份额,但随着用户对全覆盖和自优化性能的需求不断增长,网状路由器市场预计将在2031年之前以11.74%的复合年增长率增长。与网状网路部署相关的无线路由器市场规模预计将与Gigabit光纤的普及同步成长。网路服务供应商(ISP)采用Aginet和eero等云端管理平台也推动了市场成长。同时,随着5G无线技术的融入,行动热点路由器正在捲土重来,而工业级路由器则被设计用于满足严苛的环境要求。

如今,网状网路供应商普遍采用人工智慧演算法、Wi-Fi 7 多链路操作和 320MHz回程传输频道,并以此维持高价。独立式路由器则透过三频无线电和延迟整形引擎,瞄准游戏玩家市场。工业路由器利用 SD-WAN 迭加技术,安全地连接远端资产。这些细分市场表明,即使入门级硬体日趋商品化,创新细分市场也能保障利润率。

儘管Wi-Fi 5凭藉其面向大众市场的价格优势,仍占41.55%的市场份额,但Wi-Fi 7的出货量预计将以24.74%的复合年增长率成长,重塑无线路由器市场格局。企业对6-15 Gbps有效吞吐量的需求推动了Wi-Fi 7的早期普及,预计到本世纪末,Wi-Fi 7无线路由器市场规模将超过Wi-Fi 6。虽然认证体系的建立缓解了不同厂商间互通性的担忧,但高功率需求仍将促使PoE交换器进行升级。

Wi-Fi 6 将继续作为过渡技术,为预算有限的买家提供 OFDMA 的高效性能。传统的 Wi-Fi 4 装置仍将在成本和功耗比速度更重要的特定物联网环境中继续使用。在已开发地区,采购蓝图将逐步部署 Wi-Fi 7 并投资边缘运算,以确保未来容量的满足需求,而无需进行大规模系统升级。

区域分析

到2025年,亚太地区将占全球收入的33.55%,这主要得益于5G网路的部署、智慧城市规划以及製造业的数位化。新加坡和韩国的国家级倡议将推动Wi-Fi 7骨干网路连接的需求,而中国厂商则面临来自海外安全审查相关法规的挑战。全部区域超大规模资料中心的扩张也进一步推动了企业对高吞吐量路由器的订单。

北美地区依然是关键市场,这得益于积极的光纤部署和旨在为服务不足的农村地区提供设备的大规模BEAD资金。固定无线存取用户将在2024年超过1,200万,这将透过混合蜂窝/Wi-Fi网关对路由器销售构成压力,同时也起到补充作用。企业用户目前已占Wi-Fi 7网路基地台出货量的2%,预计到2025年这数字将成长五倍。

得益于多Gigabit光纤网路的普及和6GHz频谱的逐步开放,欧洲正经历稳定成长。法国在Wi-Fi 7的普及方面处于主导,高阶CPE设备正在区分不同的宽频等级。德国和英国优先发展工业4.0和安全网络,推动了对具备WPA3加密和人工智慧威胁分析功能的三频路由器的需求。英国脱欧后监管方面的差异持续影响认证流程,迫使供应商转向区域物流策略。

南美洲正经历最快的成长轨迹,年复合成长率高达10.47%,这主要得益于光纤到府(FTTH)的普及和农村地区的网路连接补贴。巴西在Wi-Fi 7的普及应用方面处于主导地位,而区域货币波动则迫使企业探索创造性的定价模式。中东和非洲的新兴市场正利用智慧城市计划,在饭店、教育和公共部门等领域试行Wi-Fi 7,为长期需求奠定基础。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 网路流量和连网设备不断增加

- 企业数位化推动频宽需求

- Wi-Fi 6/6E 的快速普及以及 Wi-Fi 7 的即将到来

- 由网路服务供应商 (ISP) 管理的 Mesh Wi-Fi 服务(较不普及)

- 政府资助的农村宽频CPE部署(低调)

- 新兴的Wi-Fi感测应用在环境智慧中的应用(低调)

- 市场限制

- 网路安全工程师的短缺和复杂性

- 行动/5G宽频替代风险

- 半导体供应链的波动性(潜在风险)

- 6GHz频谱全球分配不均(一个不太突出的问题)

- 价值/供应链分析

- 监管环境

- 技术展望

- 波特五力分析

- 新进入者的威胁

- 买方的议价能力

- 供应商的议价能力

- 替代品的威胁

- 竞争对手之间的竞争

第五章 市场规模与成长预测

- 依产品类型

- 独立路由器

- 网状Wi-Fi系统

- 行动热点路由器

- 工业/加固型路由器

- 按 Wi-Fi 标准

- 802.11n(Wi-Fi 4)

- 802.11ac(Wi-Fi 5)

- 802.11ax(Wi-Fi 6)

- 802.11be(Wi-Fi 7)

- 按频段

- 单频段

- 双频

- 三频/四频

- 按最终用户行业划分

- 住宅

- 企业

- BFSI

- 教育

- 卫生保健

- 媒体与娱乐

- 零售

- 政府和公共部门

- 其他公司

- 透过分销管道

- 线上零售商

- 线下(电子产品量贩店、大型超级市场)

- 按地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 俄罗斯

- 其他欧洲地区

- 亚太地区

- 中国

- 日本

- 印度

- 韩国

- 澳洲

- 亚太其他地区

- 中东和非洲

- 中东

- 沙乌地阿拉伯

- 阿拉伯聯合大公国

- 其他中东地区

- 非洲

- 南非

- 埃及

- 其他非洲地区

- 中东

- 南美洲

- 巴西

- 阿根廷

- 其他南美洲

- 北美洲

第六章 竞争情势

- 市场集中度分析

- 策略性倡议(併购、联盟、新产品发布)

- 市占率分析(前 15 家公司,2024 年)

- 公司简介

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Ubiquiti Inc.

- CommScope Holding Company, Inc.(ARRIS)

- Amazon.com, Inc.(eero)

- Google LLC(Nest Wi-Fi)

- Belkin International, Inc.(Linksys)

- Xiaomi Corporation

- Buffalo Americas, Inc.

- Zyxel Communications Corp.

- MikroTik SIA

- TOTOLINK(CJSC Est.)

- Edimax Technology Co., Ltd.

- Amped Wireless(A division of NexGen Connected LLC)

- Mercury-PC Technology Co., Ltd.

第七章 市场机会与未来趋势

- 评估差距和未满足的需求

Wireless router market size in 2026 is estimated at USD 18.13 billion, growing from 2025 value of USD 16.62 billion with 2031 projections showing USD 28.02 billion, growing at 9.08% CAGR over 2026-2031.

Growth springs from surging enterprise digitalization, rising residential bandwidth needs, and rapid commercialization of Wi-Fi 7. Device shipments for Wi-Fi 7 totaled 269 million units in 2024 and are projected to exceed 2.1 billion by 2028, underscoring pent-up demand for multi-gigabit performance. A parallel boom in 6 GHz Wi-Fi hardware-807.5 million units shipped in 2024-confirms strong ecosystem readiness as 63 nations free portions of the 6 GHz band for unlicensed use. Mesh systems, higher-bandwidth tri-band designs, and ISP-managed CPE bundles are expanding total addressable demand, while fixed-wireless access and semiconductor supply constraints create pockets of volatility. Vendors now race to add AI-powered management and network-as-a-service features to preserve pricing power and mitigate intensifying price competition from low-cost Chinese suppliers.

Global Wireless Router Market Trends and Insights

Growing Internet Traffic and Connected Devices

More than 21.1 billion Wi-Fi devices are active worldwide, and another 4.1 billion are expected to ship in 2024, saturating legacy networks and prompting upgrades to multi-gigabit routers. Roughly one-fifth of residential broadband users now exceed 1 TB of monthly data, stressing quality-of-service thresholds. IoT growth in smart factories, smart cities, and autonomous mobility deepens the need for low-latency throughput that Wi-Fi 7's 320 MHz channels can deliver. Enterprises face device-density headaches when Wi-Fi 6 access points hit practical limits, forcing investment in next-generation radios. The result is an accelerated refresh cycle favoring vendors with Wi-Fi 7 portfolios.

Enterprise Digitalization Driving Bandwidth Demand

Forty-five percent of enterprises already trial both Wi-Fi 6 and private 5G in parallel, highlighting a preference for converged wireless fabrics. Manufacturing plants adopt Wi-Fi 7 to run AI-enabled robotics, sub-millisecond supervisory control, and machine-vision analytics. Quarterly router orders tied to AI infrastructure surpassed USD 350 million among leading suppliers in 2025. Subscription-based network-as-a-service models lower capex barriers, allowing faster rollouts. In short, bandwidth-hungry applications and flexible financing coalesce to push the wireless router market forward.

Network-Security Complexity and Skill Shortages

A 3.8 Tbps DDoS attack exploiting the ASUS router CVE-2024-3080 illustrated the sector's exposure to firmware vulnerabilities. Meanwhile, telecom operators report a 33% shortfall in qualified network engineers, particularly for emerging Wi-Fi 7 security and WPA3 configurations. Enterprises face higher deployment costs due to specialist consulting needs, stretching project lead times. Small firms often default to lax settings, heightening breach risks and limiting the adoption of premium routers with advanced threat detection.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Wi-Fi 6/6E and Wi-Fi 7

- Mesh Wi-Fi as a Managed Service by ISPs

- Mobile/5G Broadband Substitution Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Standalone routers retained a 43.62% share in 2025, yet the mesh category is on track for an 11.74% CAGR through 2031 as users seek wall-to-wall coverage and self-optimizing performance. The wireless router market size tied to mesh deployments is forecast to expand in tandem with multi-gigabit fiber rollouts. ISP adoption of cloud-managed platforms such as Aginet and eero for Service Providers reinforces growth momentum. In contrast, mobile hotspot routers gain renewed relevance by embedding 5G radios, while industrial models address harsh-environment requirements.

Mesh vendors now bake in AI algorithms, Wi-Fi 7 multi-link operation, and 320 MHz backhaul channels to sustain premium pricing. Standalone designs increasingly target gamers, featuring tri-band radios and latency-shaping engines. Industrial routers leverage SD-WAN overlays to connect remote assets securely. Collectively, these sub-segments illustrate how innovation niches defend margin even as entry-level hardware commoditizes.

Wi-Fi 5 still commands 41.55% share thanks to mass-market affordability, but Wi-Fi 7 shipments are set for a 24.74% CAGR that will reshape the wireless router market. Enterprise demand for 6-15 Gbps real-world throughput pushes early adoption, and the wireless router market size linked to Wi-Fi 7 could surpass Wi-Fi 6 by the decade's end. Certification has eased multi-vendor interoperability concerns, although higher power requirements necessitate PoE switch upgrades.

Wi-Fi 6 remains a bridge technology, offering OFDMA efficiency to budget-constrained buyers. Legacy Wi-Fi 4 devices persist in niche IoT settings where cost and power trump speed. In advanced regions, procurement roadmaps now include phased Wi-Fi 7 rollouts paired with edge-compute investments, ensuring future-proof capacity without forklift overhauls.

The Wireless Router Market Report is Segmented by Product Type (Standalone Routers, Mesh Wi-Fi Systems, and More), Wi-Fi Standard (802. 11n, 802. 11ac, 802. 11ax, 802. 11be), Frequency Band (Single-Band, Dual-Band, Tri-/Quad-Band), End-User Industry (Residential, Enterprise), Distribution Channel (Online Retailers, Offline), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 33.55% of global revenue in 2025, buoyed by 5G rollouts, smart-city programs, and ongoing manufacturing digitization. National initiatives in Singapore and South Korea anchor demand for Wi-Fi 7 backbone connectivity, while Chinese vendors navigate overseas regulatory headwinds tied to security scrutiny. Hyperscale data-center expansion throughout the region further bolsters enterprise orders for high-throughput routers.

North America remains pivotal, thanks to aggressive fiber builds and sizable BEAD funding that directs equipment to underserved rural zones. Fixed-wireless access surpassed 12 million subscribers in 2024, simultaneously pressuring and complementing router sales via hybrid cellular-Wi-Fi gateways. Enterprises already account for 2% of Wi-Fi 7 AP shipments, a figure expected to quintuple by 2025.

Europe posts steady gains behind multi-gigabit fiber and phased 6 GHz clearance. France leads Wi-Fi 7 adoption, showcasing how premium CPE differentiates broadband tiers. Germany and the U.K. prioritize Industry 4.0 and secure networking, driving demand for tri-band routers with WPA3 and AI-powered threat analytics. Regulatory nuances post-Brexit still complicate certification timetables, nudging vendors toward localized logistics strategies.

South America registers the fastest trajectory at 10.47% CAGR on the back of fiber-to-the-home expansion and rural-connectivity subsidies. Brazil spearheads rollouts, while regional currency volatility forces creative pricing models. Emerging markets in the Middle East and Africa are leveraging smart-city ambitions to pilot Wi-Fi 7 in hospitality, education, and public-sector environments, laying groundwork for long-term demand.

- TP-Link Technologies Co., Ltd.

- NETGEAR, Inc.

- ASUSTeK Computer Inc.

- D-Link Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Ubiquiti Inc.

- CommScope Holding Company, Inc. (ARRIS)

- Amazon.com, Inc. (eero)

- Google LLC (Nest Wi-Fi)

- Belkin International, Inc. (Linksys)

- Xiaomi Corporation

- Buffalo Americas, Inc.

- Zyxel Communications Corp.

- MikroTik SIA

- TOTOLINK (CJSC Est.)

- Edimax Technology Co., Ltd.

- Amped Wireless (A division of NexGen Connected LLC)

- Mercury-PC Technology Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing internet traffic and connected devices

- 4.2.2 Enterprise digitalization driving bandwidth demand

- 4.2.3 Rapid adoption of Wi-Fi 6/6E and forthcoming Wi-Fi 7

- 4.2.4 Mesh-Wi-Fi as a managed service by ISPs (under-the-radar)

- 4.2.5 Government-funded rural broadband CPE roll-outs (under-the-radar)

- 4.2.6 Emerging Wi-Fi sensing applications for ambient intelligence (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Network-security complexity and skill shortages

- 4.3.2 Mobile/5G broadband substitution risk

- 4.3.3 Semiconductor supply-chain volatility (under-the-radar)

- 4.3.4 Uneven global release of 6 GHz spectrum (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Standalone Routers

- 5.1.2 Mesh Wi-Fi Systems

- 5.1.3 Mobile Hotspot Routers

- 5.1.4 Industrial/Rugged Routers

- 5.2 By Wi-Fi Standard

- 5.2.1 802.11n (Wi-Fi 4)

- 5.2.2 802.11ac (Wi-Fi 5)

- 5.2.3 802.11ax (Wi-Fi 6)

- 5.2.4 802.11be (Wi-Fi 7)

- 5.3 By Frequency Band

- 5.3.1 Single-Band

- 5.3.2 Dual-Band

- 5.3.3 Tri-/Quad-Band

- 5.4 By End-user Industry

- 5.4.1 Residential

- 5.4.2 Enterprise

- 5.4.3 BFSI

- 5.4.4 Education

- 5.4.5 Healthcare

- 5.4.6 Media and Entertainment

- 5.4.7 Retail

- 5.4.8 Government and Public Sector

- 5.4.9 Other Enterprises

- 5.5 By Distribution Channel

- 5.5.1 Online Retailers

- 5.5.2 Offline (CE Stores, Hypermarkets)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 Middle East

- 5.6.4.1.1 Saudi Arabia

- 5.6.4.1.2 United Arab Emirates

- 5.6.4.1.3 Rest of Middle East

- 5.6.4.2 Africa

- 5.6.4.2.1 South Africa

- 5.6.4.2.2 Egypt

- 5.6.4.2.3 Rest of Africa

- 5.6.4.1 Middle East

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration Analysis

- 6.2 Strategic Moves (M&A, Partnerships, Launches)

- 6.3 Market Share Analysis (Top-15, 2024)

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 TP-Link Technologies Co., Ltd.

- 6.4.2 NETGEAR, Inc.

- 6.4.3 ASUSTeK Computer Inc.

- 6.4.4 D-Link Corporation

- 6.4.5 Huawei Technologies Co., Ltd.

- 6.4.6 Cisco Systems, Inc.

- 6.4.7 Ubiquiti Inc.

- 6.4.8 CommScope Holding Company, Inc. (ARRIS)

- 6.4.9 Amazon.com, Inc. (eero)

- 6.4.10 Google LLC (Nest Wi-Fi)

- 6.4.11 Belkin International, Inc. (Linksys)

- 6.4.12 Xiaomi Corporation

- 6.4.13 Buffalo Americas, Inc.

- 6.4.14 Zyxel Communications Corp.

- 6.4.15 MikroTik SIA

- 6.4.16 TOTOLINK (CJSC Est.)

- 6.4.17 Edimax Technology Co., Ltd.

- 6.4.18 Amped Wireless (A division of NexGen Connected LLC)

- 6.4.19 Mercury-PC Technology Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 White-space and Unmet-Need Assessment

无线路由器市场:依产品类型、Wi-Fi标准、应用和销售管道划分-2026-2032年全球市场预测防爆无线路由器市场:依频段、类型、认证、应用和最终用户产业划分,全球预测(2026-2032年)

无线路由器市场:依产品类型、Wi-Fi标准、应用和销售管道划分-2026-2032年全球市场预测防爆无线路由器市场:依频段、类型、认证、应用和最终用户产业划分,全球预测(2026-2032年) 无线路由器市场规模、份额、趋势分析报告:按类型、频宽、应用、地区、细分市场预测,2025-2033美国无线路由器市场规模、份额、趋势分析报告:按类型、频宽、应用和细分市场预测,2025 年至 2033 年

无线路由器市场规模、份额、趋势分析报告:按类型、频宽、应用、地区、细分市场预测,2025-2033美国无线路由器市场规模、份额、趋势分析报告:按类型、频宽、应用和细分市场预测,2025 年至 2033 年 全球无线路由器市场:按类型、应用、分销管道、地区分類的范围和预测

全球无线路由器市场:按类型、应用、分销管道、地区分類的范围和预测 无线路由器市场规模、份额、成长分析(按类型、频宽、应用和地区)—2025 年至 2032 年产业预测

无线路由器市场规模、份额、成长分析(按类型、频宽、应用和地区)—2025 年至 2032 年产业预测 无线路由器市场:全球 2025-2029

无线路由器市场:全球 2025-2029 中东和北非无线路由器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年)

中东和北非无线路由器:市场占有率分析、行业趋势和统计、成长预测(2025-2030 年) 2030 年无线路由器市场预测:按组件、应用和地区分類的全球分析

2030 年无线路由器市场预测:按组件、应用和地区分類的全球分析