|

市场调查报告书

商品编码

1939136

硅酮:市场占有率分析、产业趋势与统计、成长预测(2026-2031)Silicone - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

※ 本网页内容可能与最新版本有所差异。详细情况请与我们联繫。

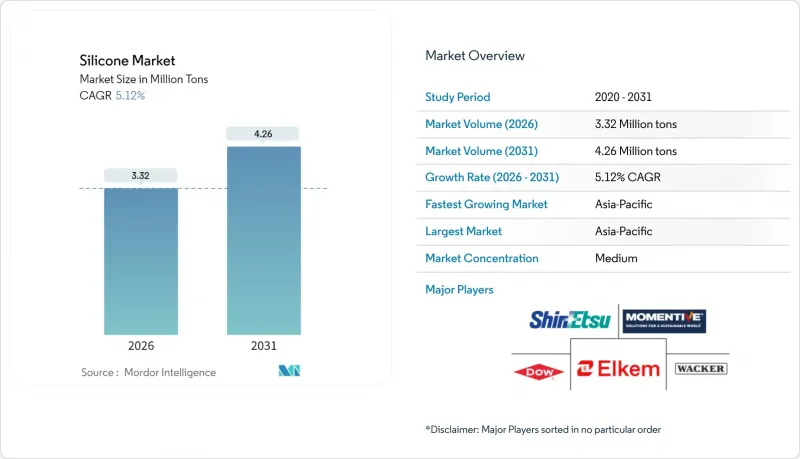

预计到 2026 年,硅酮市场规模将达到 332 万吨,高于 2025 年的 316 万吨。

预计到 2031 年将达到 426 万吨,2026 年至 2031 年的复合年增长率为 5.12%。

这种稳定成长反映了该材料在成熟终端应用领域的强势地位,同时也预示着其在次世代应用程式中的快速普及,这些应用对性能和可靠性提出了更高的要求,尤其是在电动汽车、可再生能源、先进电子产品和医疗技术领域。亚太地区强劲的基础设施投资、向电池式电动车的转型以及监管机构对更耐用、低维护材料的需求,持续支撑着基准成长。同时,用于温度控管、生物相容性和环境合规的特种等级产品能够带来溢价,使生产商能够抵御硅金属价格波动的影响,从而保障利润。竞争壁垒则源自于一体化的供应链、专有的配方技术以及安全关键型应用所需的认证流程,所有这些都为硅酮产业的现有企业提供了稳定的价值创造路径。

全球硅胶市场趋势与洞察

在汽车和电动旅游领域不断扩展的应用

电动车的广泛普及扩大了与传统弹性体的性能差距,从而推动了硅胶用量的激增。特斯拉Model Y每辆车约需15公斤硅胶用于电池组总合、热感垫和高压电缆绝缘,约内燃机轿车用量的三倍。欧洲汽车製造商目前越来越多地采用液态硅橡胶(LSR)来製造引擎室内的零件,这些零件必须能够承受高达150°C的新型防冻液温度。为了缓解硅金属价格波动,中国电动车製造商已开始同时采购高黏度橡胶和加聚液态硅橡胶,并鼓励一体化供应商签订长期合约。随着严格的零排放目标逐步实施,各大汽车製造商正在重新设计垫片、灌封材料和介面材料,为整个硅胶产业创造了对先进等级产品的持续需求。

在医疗和医疗设备领域不断扩大应用

医用级硅胶必须通过美国药典 (USP) VI 级和 ISO 10993 测试,这些通讯协定可将新产品开发蓝图延长至多 24 个月,从而保护现有供应商免受短期价格竞争的压力。穿戴式血糖监测仪、心臟导线和神经调控植入均依赖液态硅胶 (LSR) 的低致敏性和在体温下稳定的模量。医院重视其与伽马射线、蒸气和电子束灭菌方法的兼容性,有助于微创器械的高效重复使用。医疗保健的数位化,特别是远端监测,正在推动原始设备製造商 (OEM) 对半透明和光学透明硅胶薄膜的需求,这些薄膜能够整合光学感测器,同时又不影响其柔韧性。这些因素共同作用,使医疗产业成为支撑硅胶产业利润率不断增长的重要支柱。

硅金属价格波动与供应瓶颈

2024年,受能源价格波动和贸易措施的影响,现货硅金属价格在每吨1800美元至3200美元之间波动,挤压了一体化生产商和公司的利润空间。中国供应全球约68%的硅产量,因此当地的电力限制会直接影响下游硅的产量和价格。虽然长期供应合约可以起到一定的缓解作用,但大多数合约每年都会续约,这使得买家面临结构性能源成本上涨的风险。半导体製造过程中产生的边角料进行回收的试验效果有限,仅能满足不到5%的化学级需求。在低碳冶炼技术多元化和规模化之前,原物料价格波动将继续对硅产业的近期前景构成威胁。

细分市场分析

2025年,弹性体占据了硅酮市场份额的49.35%,预计到2031年将以5.33%的复合年增长率成长。在该细分市场中,用于电动车连接器和医用导管的液态硅橡胶占据了新增产量的大部分,而高黏度橡胶则确保了工业垫片的持续订单。液态硅橡胶的铂基硫化过程缩短了生产週期,并实现了多腔模具的高效放大,从而支持了批量生产。同时,室温硫化(RTV)级产品正在助力建筑和维修行业的密封剂业务发展,并创造了不受大周期波动影响的稳定需求。这些综合特性使弹性体成为硅酮产业的核心创新中心。

液态产品在产量方面占据第二大份额,这主要得益于它们作为加工助剂、润滑剂和个人护理润肤剂的用途。儘管对硅基化合物监管的加强给大宗商品循环市场带来了挑战,但对低挥发性线性液体的需求不断增长,有助于弥补损失。树脂作为电力电子和太阳能电池板等细分领域的保护性封装,其热稳定性优于环氧树脂材料,因此继续蓬勃发展。凝胶、泡沫和粉末等特殊产品丰富了产品组合,为先进纺织品、3D列印树脂和积层製造黏合剂提供原料。儘管界线日益模糊,但这些综合发展仍对硅酮市场规模保持均衡的贡献。

本硅胶市场报告按形态(流体、弹性体、树脂及其他)、应用领域(运输设备、建筑材料、电子产品、医疗、工业流程、个人护理和消费品及其他应用)和地区(亚太地区、北美地区、欧洲地区、南美地区以及中东和非洲地区)进行细分。市场预测以公吨为单位。

区域分析

预计到2025年,亚太地区将占据全球硅胶市场份额的65.10%,这主要得益于其一体化的供应链和强大的下游製造业。中国拥有众多完全后向整合的企业,这些企业将本地硅金属炉和弹性体加工厂结合,从而具备了成本竞争力并能快速扩大生产规模。

北美处于科技前沿,航太、先进汽车和医疗设备製造商对材料规格有严格的要求。 《晶片和半导体产品法案》(CHIPS Act)正在推动国内半导体生产,并刺激超低离子污染硅酮封装的新订单。中西部地区的风力发电机改造和西南部地区的太阳能发电场扩建也支撑了对耐用密封剂的需求。同时,美国食品药物管理局(FDA)对液态硅橡胶(LSR)零件的可预测核准流程正在推动医疗领域的需求。这些趋势,加上对生物基硅氧烷前体的积极研究,使该地区成为硅酮产业创新的领导者。

欧洲凭藉专业应用和监管领导地位巩固了其市场地位。生产商正投资建造闭合迴路解聚装置,将消费后弹性体废弃物转化为环状单体,以响应该地区的循环经济倡议。强制性车辆电气化推动了对耐高温、低渗漏热感垫的需求,而北海离岸风力发电的扩张则需要用于机舱封装的耐用树脂。 REACH法规虽然增加了合规成本,但也设置了阻碍直接竞争的壁垒,从而维持了欧洲有机硅产业的价值密度。

其他福利:

- Excel格式的市场预测(ME)表

- 3个月的分析师支持

目录

第一章 引言

- 研究假设和市场定义

- 调查范围

第二章调查方法

第三章执行摘要

第四章 市场情势

- 市场概览

- 市场驱动因素

- 在汽车和电动旅游领域不断扩展的应用

- 在医疗和医疗设备领域应用日益广泛

- 来自电网的需求

- 用于5G基地台的导热材料

- LSR在穿戴式医疗感测器的应用

- 市场限制

- 硅金属价格波动与供应瓶颈

- 对硅化合物排放的严格规定

- 与含氟聚合物和热塑性塑胶的竞争

- 价值链分析

- 波特五力模型

- 供应商的议价能力

- 买方的议价能力

- 新进入者的威胁

- 替代品的威胁

- 竞争程度

第五章 市场规模与成长预测

- 按形式

- 体液

- 弹性体

- 树脂

- 其他的

- 透过使用

- 运输

- 建筑材料

- 电子设备

- 卫生保健

- 工业製程

- 个人护理和消费品

- 其他用途

- 地区

- 亚太地区

- 中国

- 印度

- 日本

- 韩国

- 泰国

- 马来西亚

- 印尼

- 越南

- 亚太其他地区

- 北美洲

- 我们

- 加拿大

- 墨西哥

- 欧洲

- 德国

- 英国

- 法国

- 义大利

- 西班牙

- 俄罗斯

- 土耳其

- 北欧国家

- 其他欧洲地区

- 南美洲

- 巴西

- 阿根廷

- 哥伦比亚

- 其他南美洲

- 中东和非洲

- 沙乌地阿拉伯

- 南非

- 奈及利亚

- 埃及

- 卡达

- 阿拉伯聯合大公国

- 其他中东和非洲地区

- 亚太地区

第六章 竞争情势

- 市场集中度

- 策略趋势

- 市占率(%)/排名分析

- 公司简介

- BRB International(PETRONAS)

- CHT Germany GmbH

- DIC Corporation

- Dongyue Group

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co., Ltd

- KANEKA Corporation

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co. Ltd

- Siltech Corporation

- Wacker Chemie AG

- Wynca Tinyo Silicone Co., Ltd.

- Zhejiang Hengyecheng Organic Silicone Co., Ltd.

第七章 市场机会与未来展望

Silicone market size in 2026 is estimated at 3.32 million tons, growing from 2025 value of 3.16 million tons with 2031 projections showing 4.26 million tons, growing at 5.12% CAGR over 2026-2031.

This measured expansion reflects the material's entrenched role across mature end-uses while signaling rapid uptake in next-generation applications that demand higher performance and reliability, especially in electric mobility, renewable power, advanced electronics, and medical technology. Robust infrastructure spending in Asia-Pacific, the shift to battery-electric vehicles, and regulatory pushes for more durable, low-maintenance materials continue to underpin baseline growth. At the same time, specialty grades designed for thermal management, biocompatibility, and environmental compliance are unlocking price premiums that help producers protect margins from silicon-metal volatility. Competitive barriers remain rooted in integrated supply chains, proprietary formulations, and the qualification cycles required in safety-critical applications, all of which support a steady value-creation path for incumbents in the silicone industry.

Global Silicone Market Trends and Insights

Rising Applications in Automotive and E-mobility

Electric-vehicle (EV) adoption is multiplying the use of silicone by widening the performance gap versus traditional elastomers. Battery-pack sealing, thermal gap-pads, and high-voltage cable insulation collectively add close to 15 kg of silicone per Tesla Model Y, roughly triple that of an internal-combustion sedan. European OEMs now favor liquid-silicone rubber (LSR) for under-hood parts that must withstand new glycol-free coolants at 150 °C. Chinese EV makers have begun dual-sourcing high-consistency rubber and addition-cure LSR to buffer silicon-metal price swings, encouraging integrated suppliers to lock in long-term contracts. As stringent zero-emission targets phase in, every major automaker is redesigning gasketing, potting, and interface materials, creating an enduring pull for advanced grades across the silicone industry.

Increasing Usage in Healthcare and Medical Devices

Medical-grade silicones must clear USP Class VI and ISO 10993 testing, a protocol that can extend new-product roadmaps by up to 24 months, thereby shielding incumbent suppliers from short-cycle pricing pressure. Wearable glucose monitors, cardiac leads, and neuromodulation implants all hinge on LSR's hypoallergenic profile and stable modulus at body temperature. Hospitals value the polymer's sterilization compatibility with gamma, steam, and e-beam methods, which supports lean re-use strategies in minimally invasive tools. Digitization of care-particularly remote monitoring-has sparked OEM demand for translucent, optically clear silicone films that integrate optical sensors without compromising flex-life. Collectively, these factors cement healthcare as a margin-accretive pillar of the silicone industry.

Volatile Silicon-metal Prices and Supply Bottlenecks

Spot silicon-metal swung between USD 1,800-3,200/ton in 2024 on energy-price gyrations and trade measures, squeezing margin profiles across integrated and merchant producers alike. China supplies nearly 68% of global output, so provincial power rationing immediately reverberates through downstream silicone volumes and pricing. While long-term offtake contracts provide partial insulation, most renew annually, leaving buyers exposed to structural energy-cost inflation. Pilot recycling of semiconductor kerf scrap yields less than 5% of chemical-grade demand, offering only modest relief. Until diversified, low-carbon smelting gains scale, raw-material turbulence will shadow short-term forecasts for the silicone industry.

Other drivers and restraints analyzed in the detailed report include:

- Demand from Power Transmission and Distribution Grids

- 5G Base-station Thermal Interface Materials

- Stringent Siloxane Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Elastomers controlled 49.35% of the silicone market share in 2025 and are forecast to grow at a 5.33% CAGR through 2031. Within this group, liquid-silicone rubber for EV connectors and medical catheters captures the lion's share of incremental tonnage, while high-consistency rubber secures repeat orders in industrial gasketing. LSR's platinum-cure chemistry shortens cycle times, allowing multi-cavity molds that scale efficiently for high-volume parts. Meanwhile, room-temperature-vulcanizing (RTV) grades strength-en sealant franchises in construction rehabilitation, feeding consistent demand regardless of macro-cycles. Collectively, these attributes make elastomers the pivotal innovation hub in the silicone industry.

Fluids rank second in volume, anchored by their role as process aids, lubricants, and personal-care emollients. Although impending siloxane limits challenge commodity cyclics, linear-chain fluids with lower volatility are gaining traction and help offset losses. Resins continue to deliver niche growth as protective encapsulants in power electronics and solar panels, where their thermal stability outperforms epoxy analogs. Specialty formats-gels, foams, and powders-round out the portfolio, supplying advanced textiles, 3-D printing resins, and additive-manufacturing binders. Even as boundaries blur, the cumulative developments sustain a balanced contribution to the silicone market size.

The Silicone Report is Segmented by Form (Fluids, Elastomers, Resins, and Others), Application (Transportation, Construction Materials, Electronics, Healthcare, Industrial Processes, Personal Care and Consumer Products, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific wielded 65.10% of the global silicone market share in 2025, propelled by integrated supply chains and prolific downstream manufacturing. China features fully backward-integrated players that couple local silicon-metal furnaces to elastomer finishing plants, enabling cost competitiveness and rapid scale-up.

North America remains a technology vanguard, where aerospace, advanced automotive, and biomedical device makers impose stringent material specifications. The CHIPS Act catalyzes domestic semiconductor production, triggering new orders for ultra-low-ionic contamination silicone encapsulants. Wind-turbine repowering in the Midwest and solar-farm expansions in the Southwest anchor demand for high-durability sealants, while the U.S. Food and Drug Administration's predictable pathway for LSR components bolsters healthcare volumes. These trends, paired with active research into bio-based siloxane precursors, position the region as an innovation driver in the silicone industry.

Europe secures its role through specialty applications and regulatory leadership. Producers invest in closed-loop depolymerization units that convert spent elastomer scrap into cyclic monomers, aligning with the bloc's circular-economy vision. Automotive electrification mandates energize demand for high-temperature, low-bleed thermal pads, while offshore-wind build-outs in the North Sea necessitate robust resins for nacelle encapsulation. Although REACH obligations elevate compliance costs, they also create barriers that temper direct price competition, sustaining value density across the European silicone industry.

- BRB International (PETRONAS)

- CHT Germany GmbH

- DIC Corporation

- Dongyue Group

- Dow

- DyStar Singapore Pte Ltd

- Elkem ASA

- Evonik Industries AG

- Hoshine Silicon Industry Co., Ltd

- KANEKA Corporation

- KCC SILICONE CORPORATION

- Momentive

- Shin-Etsu Chemical Co. Ltd

- Siltech Corporation

- Wacker Chemie AG

- Wynca Tinyo Silicone Co., Ltd.

- Zhejiang Hengyecheng Organic Silicone Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising applications in automotive and e-mobility

- 4.2.2 Increasing usage in healthcare and medical devices

- 4.2.3 Demand from power transmission and distribution grids

- 4.2.4 5G base-station thermal interface materials

- 4.2.5 LSR adoption in wearable medical sensors

- 4.3 Market Restraints

- 4.3.1 Volatile silicon-metal prices and supply bottlenecks

- 4.3.2 Stringent siloxane emission regulations

- 4.3.3 Competition from fluoropolymers and thermoplastics

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Form

- 5.1.1 Fluids

- 5.1.2 Elastomers

- 5.1.3 Resins

- 5.1.4 Others

- 5.2 By Application

- 5.2.1 Transportation

- 5.2.2 Construction Materials

- 5.2.3 Electronics

- 5.2.4 Healthcare

- 5.2.5 Industrial Processes

- 5.2.6 Personal Care and Consumer Products

- 5.2.7 Other Applications

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Thailand

- 5.3.1.6 Malaysia

- 5.3.1.7 Indonesia

- 5.3.1.8 Vietnam

- 5.3.1.9 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Turkey

- 5.3.3.8 Nordics

- 5.3.3.9 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Colombia

- 5.3.4.4 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Nigeria

- 5.3.5.4 Egypt

- 5.3.5.5 Qatar

- 5.3.5.6 United Arab Emirates

- 5.3.5.7 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 BRB International (PETRONAS)

- 6.4.2 CHT Germany GmbH

- 6.4.3 DIC Corporation

- 6.4.4 Dongyue Group

- 6.4.5 Dow

- 6.4.6 DyStar Singapore Pte Ltd

- 6.4.7 Elkem ASA

- 6.4.8 Evonik Industries AG

- 6.4.9 Hoshine Silicon Industry Co., Ltd

- 6.4.10 KANEKA Corporation

- 6.4.11 KCC SILICONE CORPORATION

- 6.4.12 Momentive

- 6.4.13 Shin-Etsu Chemical Co. Ltd

- 6.4.14 Siltech Corporation

- 6.4.15 Wacker Chemie AG

- 6.4.16 Wynca Tinyo Silicone Co., Ltd.

- 6.4.17 Zhejiang Hengyecheng Organic Silicone Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet Need Assessment

硅胶市场:依产品类型、形态和最终用途产业划分-2026-2032年全球市场预测二甲基环硅氧烷市场:2026-2032年全球市场预测(依产品类型、纯度等级、应用、终端用户产业及通路划分)

硅胶市场:依产品类型、形态和最终用途产业划分-2026-2032年全球市场预测二甲基环硅氧烷市场:2026-2032年全球市场预测(依产品类型、纯度等级、应用、终端用户产业及通路划分) 硅胶隔热垫市场规模、份额和成长分析:按产品类型、材料品质、最终用户、分销管道和地区划分-2026-2033年产业预测

硅胶隔热垫市场规模、份额和成长分析:按产品类型、材料品质、最终用户、分销管道和地区划分-2026-2033年产业预测 全球硅胶市场规模、份额、趋势和成长分析报告(2026-2034年)

全球硅胶市场规模、份额、趋势和成长分析报告(2026-2034年) 硅酮聚合物市场:按类型、终端应用产业及地区划分

硅酮聚合物市场:按类型、终端应用产业及地区划分 全球硅胶市场:市场规模、份额和趋势分析(按产品、最终用途和地区划分),细分市场预测(2026-2033 年)硅环和硅电极市场(依纯度等级、形状、涂层、应用和最终用途产业划分),全球预测,2026-2032年硅酮60市场:依产品类型、形态、黏度、等级、应用及通路划分,全球预测,2026-2032年

全球硅胶市场:市场规模、份额和趋势分析(按产品、最终用途和地区划分),细分市场预测(2026-2033 年)硅环和硅电极市场(依纯度等级、形状、涂层、应用和最终用途产业划分),全球预测,2026-2032年硅酮60市场:依产品类型、形态、黏度、等级、应用及通路划分,全球预测,2026-2032年 2026年全球硅胶市场报告2026年全球硅酮(不含树脂)市场报告

2026年全球硅胶市场报告2026年全球硅酮(不含树脂)市场报告